Economics Chapter 2 the Allocation of resources 5-14

1/58

Earn XP

Description and Tags

ECONOMICS IGCSE CIE CHAPTER/ SECTION 2 The Allocation of Resources

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

59 Terms

What is the definition of a market?

A place where buyers and sellers can engage in trade

What do markets do?

Help allocate resources through supply and demand

Answers the 3 economic problems

What is the Market System?

-Sometimes called the Price mechanism

-establishes market equilibrium

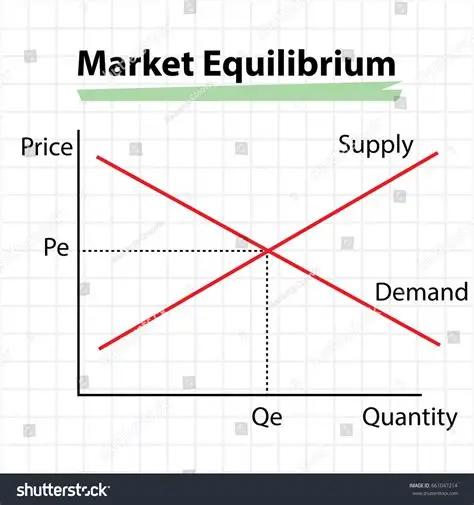

What is market equilibrium?

The price where supply and demand are equal

DRAW MARKET EQUILIBRIUM GRAPH

Like this

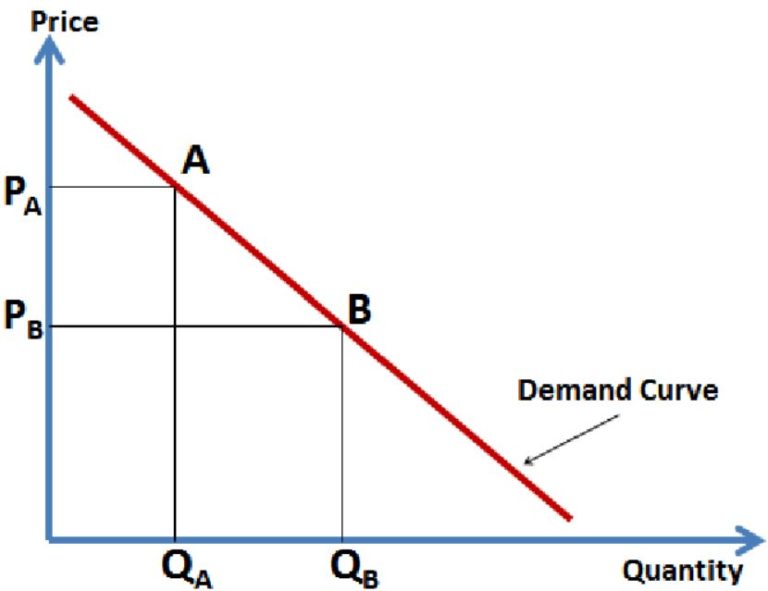

What is Economic Demand?

The quantity of goods that consumers are willing and able to buy over a period of time

What is the relationship between price and demand?

The higher the price the lower the demand.

The opposite is also true

What is the law of demand?

The quantity of demand rise as prices falls and vice versa

Why is the law of demand true?

-As the price falls people can afford to buy more of the product

-As prices falls more people could afford it

What are the determinants of Demand?

Habits, fashions, and taste

Income

Supplements and complements

Advertising

Government policies

Economy

Others

Weather

Demographics of population

DRAW the DEMAND GRAPH

What are the two types of movement and how do they happen?

-Contraction and Extension

Changes in Price

-Shifts

Changes from HISAGE Factors

What are individual and market demand?

Individual—Demand of a certain demographic

Market Demand-Demand of entire market

What is the Law of Supply?

Quantity of supply lowers as price lowers whilst it rises when prices are increased

Why is the Law of Supply the case?

Cover the costs of production for new firms

Old firms are able to earn higher profits

Determinants of supply?

Time

Weather

Opportunity costs

Taxes

Innovations

Production Costs

Subsidies

What are the two types of supply changes?

Shifts in supply

Caused by TWO TIPs

Contraction/ Extension

Caused by price

What are the characteristics of a price mechanism/ market system?

No government intervention in the affairs of the market

Goods and services are allocated through the market

Allocation of factors of production based on financial incentives

Competition creates opportunities for firms and consumers

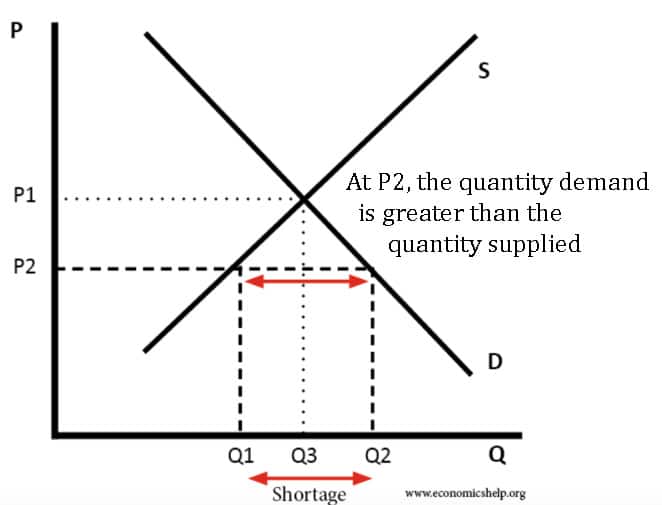

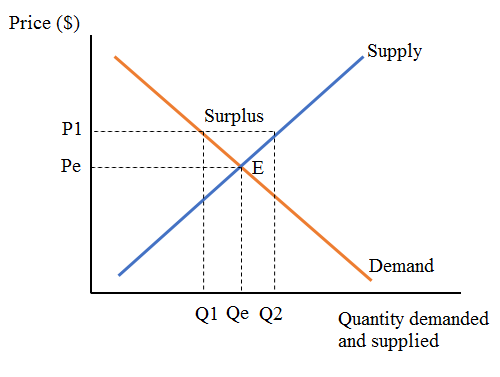

What is a shortage and what is a surplus?

-Too much demand

-Too much supply

-Causes market disequilibrium

Graph for Shortage

Graph for Surplus

What is the relationship between price/ demand and price changes?

Higher demand increases price

Lower demand decreases price

Higher supply decreases price

Lower supply increases price

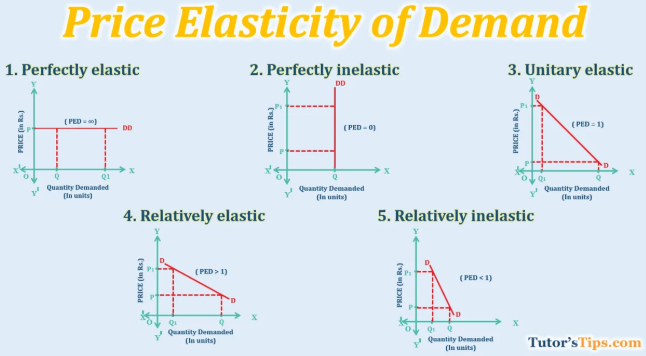

What is Price Elasticity of Demand?

How much the demand for a good/ service responds to changes in price

How to calculate PED?

Percentage Change in Demand

__________________________

Percentage change in price

What are the 5 types of PED categories

Inelastic <1

Elastic >1

Perfect Inelastic=0

Perfect Elastic= infinity

Unitary elastic=1

Draw the five types of PED graphs

What are the determinants of Price Elasticity of Demand

Substitution

Cost of Switching

Advertising

Time/ length of change

Habits

Income

Necessity

Definition

PED and pricing explain the relationship

Inelastic- would be better to raise prices to make profit

Elastic- would be better to lower prices to make profit

Why does PED matter to decision makers?

Helping producers decide their pricing strategies

Predicting the producer’s change’s impact

Price discrimination- charging different prices for the same product for different demographics

Deciding where to raise sales-tax

Determining tax policies

Wage negotiations

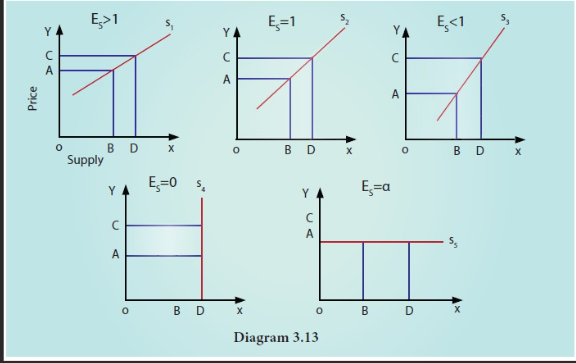

How to calculate Price elasticity of supply?

percentage change in quantity supplied

Percentage change in price

How to draw the five of PES

Determinants of PES

Degree of Spare capacity

The Level of stocks remaining

The number of firms in an industry

Time frame

The ease of factor substitution

What is an economic system?

A way an economy is ran and organized

What are the two main modern types of economic systems and their definitions?

Market Economy-relies on the private sector market forces to allocate scare resources through monetary incentives with minimal governmental interference.

Mixed Economy-a mix of government resources allocation and market systems

What are the advantages of a market system?

Efficiency-firms are forced to pay attention to what consumers desire and innovate to compete

Freedom of choice-consumers are free to choose what to purchase and pursue

incentives-monetary incentives make people work

What are the disadvantages of a market system?

Income and wealth inequalities-the economy is geared to meet the needs of the wealthy and neglect those who cannot pay

environmental issues- pollution, resource depletion, and destruction for profit

Social hardships-basic necessities may not be provided

Wasteful competition-useless spending such advertising

What is market failure?

When market forces fail to allocate resources efficiently leading to effects on a third-party

What are Private costs, benefits, external benefits, external costs, and social cost?

Social costs-Private+External costs

Private benefits-individual benefits

Private costs-individual costs

External costs-negative side-affects

External benefits-positive side effects

What are public goods and market failures related?

Public goods do not produce profits and do not get built unless governmental forces step in causing bad effects on the public

What are merit and demerit goods?

merit-external benefits

demerit-external costs

How is abuse of monopoly an example of market failure?

without government they would exploit the consumers

What are the main points for and against mixed economies?

For-Best of both worlds

able to provide both necessary and consumer goods

Against

higher taxes

Same problems as market economy still

Ways to regulate market failure?

Maximum price

Minimum price

Subsidies

Regulation

Education

Privatization

Nationalization

Direct provision

Quotas

Maximum price good

-Prevents giant rise

-allows consumers to afford necessary goods and services

maximum price bad

-shortages

-unofficial markets will rise

-excess demand

Minimum price good

-guarantee supply

-more incentives to work

-encourages supply

Minimum bad

excess supply

Subsidies good

-increases supply

Subsidies bad

-opportunity costs

Rules and regulations good

-Less of demerit goods

-more merit goods

R&R bad

-unofficial markets

-Break rules

-require necessary punishment

Education good

-awareness of demerit and merit goods

Private good

-one off payments

-less debts

no maintenance

earns revenue from tax

corporate tax

-reduce tax-payer burden

-incentive to be more efficient

Private bad

-private monopolies

-intervention may still be needed

-opportunity cost

Direct provision good

accessible to all

help maintain high quality

Direct provision bad

-cost of opportunity

-over consumption

who to prioritize

some may take advantage

quotas good

-no over production

-protects environment

Quotas bad

-may increase price

-may be too expensive to implement