Principles of Finance

1/49

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

50 Terms

Short-term debt securities

promise 1 cash flow in the future

Use simple interest

such as treasury note, promissory note/one name paper, bill of exchange/bank bill

Treasury note

A short-term debt security issued by the government

Promissory note/one name paper

A short-term debt security issued by a company, with higher risk than a treasury note but higher yield

Bills of exchange/bank bill

a guarantee of repayment by a bank if the borrower is unable to pay

Stated vs effective interest rate

Stated: rate without frequency of compounding per period

Effective: rate with

Capital market efficiency/efficient market hypothesis

A market is informationally efficient if prices quickly and unbiasedly reflect all avaliable, relevant information

When do diversification benefits exist

When securities’returns are less than perfectly positvely correlated

Logical foundations to capital market efficiency

large number of profit-maximising participants that analyse and value securities independent of each other

estimates adjusted quickly without bias

no expectation of abnormal returns

Unrealised return

Holding on to shares without selling them

Realised return

Selling shares and not holding on to them

Systematic risk

Risk that cannot be diversified

Calculated with beta

When a portfolio is formed, it is averaged not eliminated

Also called covariance/market risk

Share split

a company issues additional new shares for shares already owned by shareholders

NPV

Accept if NPV>0

Reject if NPV<0

Alternatives to NPV

IRR

Payback rule

Payback rule

Accept if the payback period<than a pre-specified length of time

Reject if the payback period>than a pre-specified length of time

Internal rate of return/IRR

accept, if the cost of capital < IRR

reject, if the cost of capital > IRR

Drawbacks of payback rule

Arbitrary cut off period in summing cash flows

Doesn’t discount future cashflows

Ignores time value of money, but sums cash flows and compares them to cash outflow in the present

Ignores cash flows after the payback period

Choosing between projects

Independent projects: do all of the projects with a positive NPV

Mutually exclusive projects: choose the project with the highest NPV

Equivalent annual annuity (EAA)

The level annual cash flow with the same present value as the cash flows of the project

used to evaluate projects with different lives

Free cash flows

the cash generated by the firm's operations that is available after funding all operating expenses

Capital budgeting

analysing investment opportunities and deciding which ones to accept

Modigliani–Miller Propositions 1

Firm value is independent of capital structure

The project's operating cash flows determine total value

Modigliani–Miller Propositions 2

The cost of capital of levered equity is equal to the cost of capital of unlevered equity plus a premium that is proportional to the debt–equity ratio (measured using market values).

Interest tax shield

gain to investors from the tax deductibility of interest payments

Formula: Corporate tax rate x Interest payments

How does debt decrease agency costs

keeps ownership more concentrated, improving managerial oversight

requires regular interest and principal payments, reducing cash under managers' discretion

Consequences of asymmetric payoffs

Risk shifting ("rolling the dice"): taking excessively risky, negative-NPV projects.

Asset stripping: paying out cash to shareholders before creditors take over.

Underinvestment: conserving cash instead of funding good projects.

New investment requires cash today (often funded by equity or internal funds).

Investment going to debt and not shareholders

Information asymmetry

Managers know the firm and cash flows better than investors

So they can adjust firm’s capital structure, which could misprice securities

Adverse selection

Investors fear that equity is being sold because it is overvalued

How to avoid adverse selection

Use retained earnings/internal cash

Pecking order hypothesis

First choice: retained earnings

Second choice: debt

Last resort: equity

Declaration date of dividends

date the Board of Directors announces the dividend per share

Ex-dividend date

If shareholders buy shares BEFORE this date, they get the dividends

Uses of free cash flow

Invest in new projects

Increase cash reserves (do nothing)

pay out dividends

repurchase shares

Record date of dividend

5.00pm, day company closes share register to determine which shareholders get the current dividend

Payable date

The date company pays dividends

Cum dividend period

Period up to, EXCLUDING ex dividend date

Special dividend

Dividend paid due to either selling off an assets or provide shareholder with tax benefits

Open market repurchase

A firm repurchases their shares through buying them back from the market over time

Off market buyback

A firm invites its shareholders to offer to sell their shares to the firm by way of a tender process/offer

Dutch auction

investors indicate the shares they want to sell and then the firm tries to bid for them at the lowest price

Modigliani-Miller and dividend irrelevance

In perfect capital markets, holding fixed the investment policy of a firm, the firm’s choice of dividend policy is irrelevant and does not affect the initial share price

Classical tax system

No imputation/franking credits, investor is taxed twice

Imputation tax system

Yes franking credits

Dividend smoothing

maintaining relatively constant dividends

Dividend signaling

dividend changes reflect managers' views about a firm's future earnings prospects

Hedging

Investor has put option to protect them against downward movement in the market

Factors affecting option prices

Exercise date

volatility

market price of share

risk free rate

Option prices and exercise date

American: Exercise date further away, option increases

European: Exercise date further away, option decreases

Black-Scholes option pricing formula

Nd1, Nd2 are probabilities

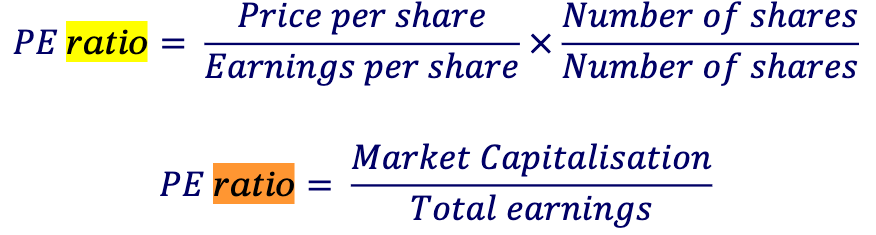

P/E ratio

How much the market values each $ of earnings