ACC 403 Chapter 1/2

1/56

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

57 Terms

What is professional skepticism in auditing?

An attitude that includes a questioning mind and a critical assessment of evidence.

What is the purpose of Generally Accepted Auditing Standards (GAAS)?

To identify necessary qualifications and characteristics of auditors and guide the conduct of the audit examination.

What is the objective of an audit?

To obtain reasonable assurance that financial statements are free of material misstatement and to issue a report on the financial statements.

What is the role of the Public Company Accounting Oversight Board (PCAOB)?

To provide external oversight over audits of public entities and enforce auditing standards.

What is the significance of independence in auditing?

The auditor must conduct the audit in an unbiased, objective manner.

What does the term 'anchoring bias' refer to in the context of auditing?

A cognitive bias where individuals rely too heavily on the first piece of information encountered.

What is the 'availability heuristic' in decision-making?

A mental shortcut that relies on immediate examples that come to mind when evaluating a specific topic.

What is the significance of audit firm systems of quality control?

To ensure that audits are conducted in accordance with professional standards and regulations.

What are the potential consequences of failing to exercise professional skepticism?

Auditors may miss material misstatements or fraud, leading to inaccurate financial reporting.

What is the relationship between GAAS and audit quality?

GAAS provides a framework that helps ensure audits are conducted with quality and integrity.

What is the purpose of PCAOB inspections?

To assess the quality of audits performed by registered public accounting firms.

What is the first step in the auditing process according to GAAS?

Obtain an understanding of the entity and its environment, including internal controls.

What is the importance of obtaining sufficient appropriate audit evidence?

It supports the auditor's opinion on the financial statements and ensures compliance with auditing standards.

What is a common area of significant risk identified in audits?

Related parties and their transactions.

What is the significance of the audit report?

It communicates the auditor's findings and opinion on the financial statements to stakeholders.

What does the term 'material misstatement' refer to?

An error or omission in financial statements that could influence the economic decisions of users.

What is independence in fact in auditing?

Auditors' mental attitude and impartiality with respect to the client.

What does independence in appearance refer to?

The extent to which others perceive auditors to be independent.

What is due care in auditing?

Performing work at a level that would be exercised by reasonable auditors in similar circumstances.

Define professional skepticism.

A state of mind characterized by appropriate questioning and a critical assessment of evidence.

What is professional judgment in the context of auditing?

The application of relevant training, knowledge, and experience in making informed decisions during the audit engagement.

What is reasonable assurance?

Auditors are not guarantors of the entity's financial statements; risks cannot be eliminated but limited to an acceptably low level.

What does GAAS require in terms of planning and supervision?

A detailed audit plan that lists the procedures auditors need to perform and an understanding of the client's business and industry.

What is materiality in auditing?

Something is material if it is likely to influence a financial statement user's decisions.

What is risk assessment in auditing?

The process of identifying the probability that a material misstatement will occur and not be prevented or detected by the company's controls.

Define inherent risk.

The probability that material errors or frauds will occur absent internal controls.

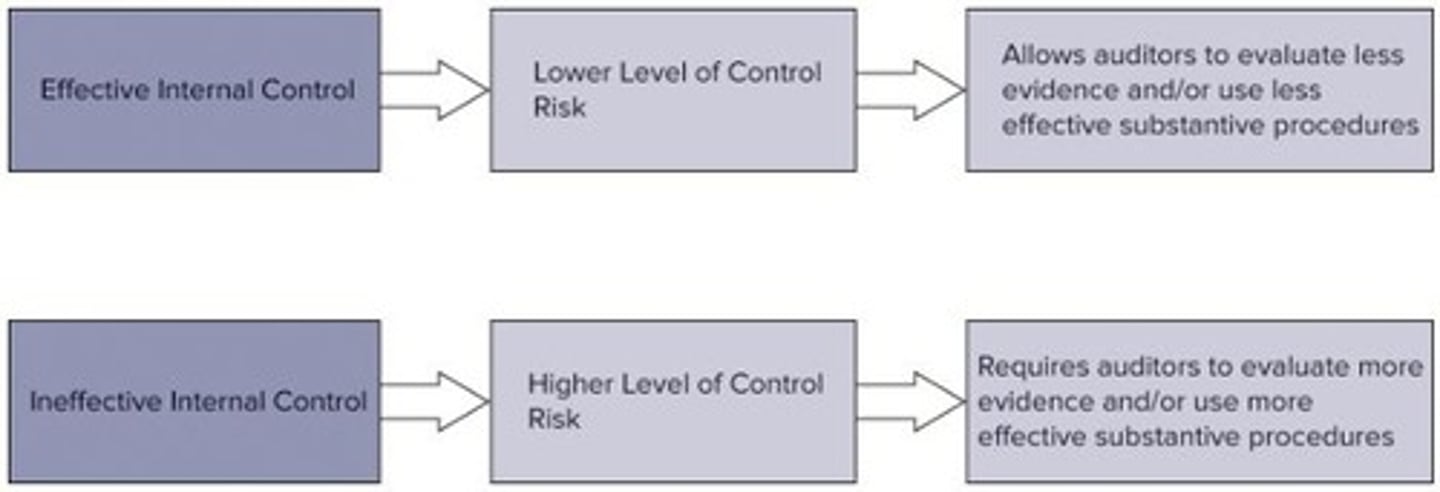

What is control risk?

The likelihood that internal controls will not prevent or detect material errors or frauds.

What are substantive procedures?

Detailed audit and analytical procedures designed to detect material misstatements in account balances and footnote disclosures.

What factors affect the quality of audit evidence?

Reliability (external > internal, direct > indirect, original > copies) and relevance (related to the assertion of interest).

What is detection risk?

The likelihood that the auditors' substantive procedures will fail to detect a material misstatement that exists.

How can auditors lower detection risk?

By increasing the quality and/or quantity of evidence gathered.

What are the four types of audit opinions that can be issued?

1. Unmodified (or unqualified), 2. Qualified (except for), 3. Adverse, 4. Disclaimer.

What is a system of quality control in audit firms?

Implemented to ensure that work is of high quality and meets professional standards.

What are the components of a system of quality control?

1. Leadership responsibilities, 2. Relevant ethical requirements, 3. Acceptance and continuance, 4. Human resources, 5. Engagement performance, 6. Monitoring.

How often is an audit firm subject to PCAOB inspection?

The frequency varies, but firms are regularly inspected to ensure compliance with standards.

What types of deficiencies might the PCAOB identify?

Deficiencies in audit areas that could lead to incorrect opinions being issued.

What is the role of engagement planning in auditing?

To establish a framework for the audit process, ensuring all necessary procedures are outlined.

What is the importance of understanding the client's business and industry?

It helps auditors assess risks and tailor their audit approach accordingly.

What is the impact of better controls on control risk?

Better controls lead to lower control risk and less substantive audit work necessary.

What is the primary purpose of an audit?

To enhance the trustworthiness and reliability of company-reported information.

What is business risk?

The risk that an entity will fail to meet its objectives.

What do internal decision makers need for effective business management?

Timely, relevant, and reliable information.

What is information risk?

The probability that the information circulated by a company will be false or misleading.

What is the role of auditors in mitigating information risk?

Auditors enhance the trustworthiness and reliability of company-reported information.

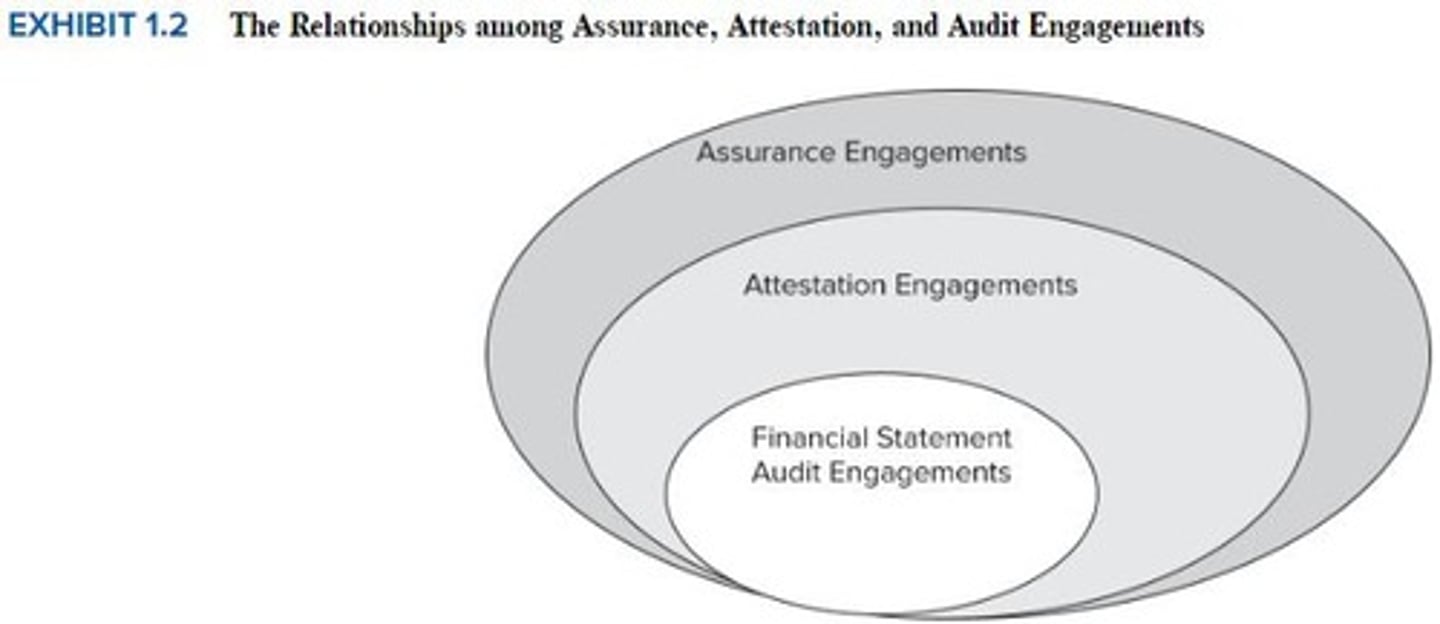

Define assurance in the context of auditing.

The lending of credibility to information.

What is attestation?

A professional service resulting in a report on an assertion about subject matter that is the responsibility of another party.

How is auditing defined?

The systematic process of objectively obtaining and evaluating evidence regarding assertions about economic actions and events.

What are assurance services?

Independent professional services that improve the quality of information for decision makers.

Give an example of an assurance service.

Cybersecurity risk assessment and assurance.

What is an attestation engagement?

An engagement where a practitioner examines whether management's assertions about a subject matter can be relied upon.

What must CEOs and CFOs certify under Section 302 of the Sarbanes-Oxley Act?

They have read the financial statements, are not aware of false statements, and believe the statements present an accurate picture of the company's financial condition.

What are the PCAOB assertions?

Existence or Occurrence, Completeness, Valuation or Allocation, Rights and Obligations, Presentation and Disclosure.

What does the existence or occurrence assertion address?

Whether assets or liabilities exist at a given date and whether recorded transactions have occurred.

What does the completeness assertion address?

Whether all transactions and accounts that should be presented in the financial statements are included.

What does the valuation or allocation assertion address?

Whether asset, liability, equity, revenue, and expense components are included at appropriate amounts.

What does the rights and obligations assertion address?

Whether assets are the rights of the entity and liabilities are the obligations of the entity.

What does the presentation and disclosure assertion address?

Whether components of the financial statements are properly classified, described, and disclosed.