accounting final

1/79

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

80 Terms

3 primary responsibilities of manager

planning, directing and controlling

managerial vs finacial accounting

Managerial - Internal, No GAAP, Forward and future focused,

Financial - external, history past based, Gaap involved

Ethical Standards - IMA statements

competence - education/training

confidentiality - keeping information private

integrity - confflicts of interest purposely mistake financials

credibility - information

Chapter 2

service company

provides services, no inventory

merchandising company

buys finished goods and resells them

manufacturing

makes products and has raw material inventory, work in process inventory, and finished goods inventory

value chain

Research and Development - expensed immediately

Design - prouct/ process of making product

Production - Manufacturing / Purchases (Merchandising)

Marketing - Advertising

Distribution - Shipping to Customer

Customer Service

Direct vs Indirect Costs

Direct - easily traceable

Indirect - not easily treaceable

What are direct and indirect costs in a merchandising company?

direct - direct materials, direct labor

indirect costs - moh (made up of ID material and ID labor) plus any plant rent, or factory, glue, screws

Product vs Period Costs

Product - costs whihch go into inventory direct materials, direct labor, moh, indirect material, indirect labor, other costs with word plant, factory, freight in, assembly line workwer, anything factory

Period - cost expenses in periond incurred expenses seeling, general, administrative (HQ, SHIPPING, ACCT, HR)

Direct material Used calculation

Beginning Raw Material inventory + Purchases of Raw DM used (plus freight in) = Raw material available for use - Ending RM inventory = Direct Material used

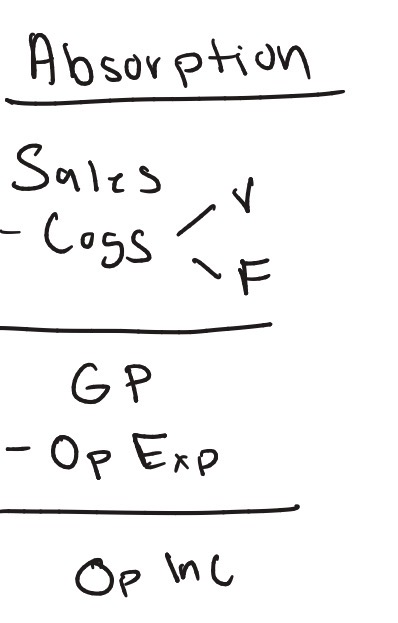

Cost of Goods Manufactured

Beginning WIP + Total manufacturing costs incurrect (DM, DL, MOH) = Total manufacturing costs to account for - end WIP inventory = Cost of Goods Mnufactured

Manufacturing Company

Beginning inventory + COGM = Cost of goods available for sale - ending finished goods inventory = COGS

Merchandising Company - COGS calculation

Beginning Inventory + Purchases ( freight in ) = GAFS - Ending Merchandising Inv = GOGS

DATA types

structured data - organized data strucutre

unstructured data - photos, videos, (social media posts)

semi structured - in between (likes on facebook posts)

chapter 3

job costing

costum unique, small batches, service

process costing

large volume, homogenous, product mix

job costing process

production schedule - bill of materials (recipe card for prod and purchases order) - material recquisition ( required material from raw material invetory to go to WIP) - job cost record ( we can see all the direct material, direct labor, and manufacturing overhead

Predetermined MOH rate

Total Estimated MOH costs / Total estimated amount of allocation

MOH allocated to a job

predetermined moh rate x actual amount of allocation base used

MOH - over or under

overallocated - allocated > incurred (overcosted)

underallocated - allocated < incurred (undercosted)

how we handle over or under

over - reduce cogs

under - increase cogs

service firm

directly traceable - DL, travel ,liscensing

Indirect costs - (operating expenses) we need to allocate these

direct - directly to the job

indirect - allocate to the job

Activity based Costing

allocating for each activity

cost hirarchy

unit - label on each bottle

batch — machine set up

product - machine lease cost

facility - supervisor custodial, utilities

traditional vs lean thinking

traditional - similar machines grouped together, karger set up times, large batches ,high inv many suppliers

lean - more efficient, self contained, shorter set up times, low inv

4 categories of quality related costing

prevention - avoid problems ( training, design, process evaluate suplies)

appraisal - inspecting or testing

internal failure - find defects before shipping rework

external failure - customer finds defects warranty or customer

correlation coefficient ( r value )

ranges from -1 to 0 to 1

-1 being least correlated (moving opposite direction)

1 being most correlated (moving same direction)

variable osts

- same per in unit basis, the more units the higher total cost

fixed costs

same costs regardless of how many units we produce

mixed

both fixed and variable costs

setp costs and curviliniar

step - a range (ex 1 babysitter for every 10 kids)

Regression analysis

(Intercept) - Y intercept (fixed cost)

X variable - Variable cost per unit

Formula

TC = VC (# of units) + FC

high low question

practice computation question

r²

from 0-1 the closes to 1 the better the fit

absorption costing

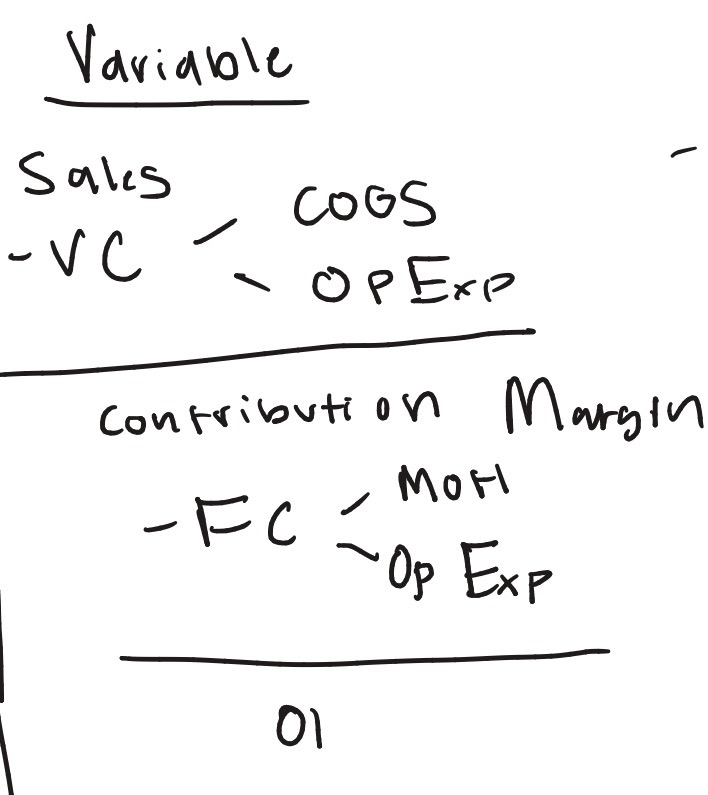

variable costing

chapter 7

Contribution Margin Formula

Sales - Variable Cost

Contribution Margin Ratio

Contribution Margin / Sales

Break Even units

Fixed Costs + Target Profit / Contribution Margin Units

Break Even Dollars

Fixed Costs + Target Profit / Contribution Margin Percentage

Be able to know the effect on contribution margin and break even point

use the formulas -

Sales - VC = CM & BE = FC/CM

Margin of Safety Dollars

Expected or Actual Sales $ - Break Even $

Ooerating Leverage

HIGH OL - high fixed costs + low variable costs

LOW OL - low fixed costs + high variable costs

Operating Leverage Factor formula

Contribution Margin / Operating Income

Chapter 8

Relevant information

Pertains to the future

Differs across alternatives

Price taker vs price setter

Price taker - product lacks uniqueness, not brand name, lots of competition, and uses target costing

Price setter - product is unique, brand name, less competition, cost plus pricing

Target costing formula

revenue @ market price - desired profit

Cost plus pricing

total cost (v +f) + desired profit

special order question

computaional - discontinuing a product/dept/store

consider

Lost CM margin

add avoidable Fixed Costs

Add operating income from space

work question s8-9

Outsourcing

proffesor said we would do an exaple in class

but use the formuala

vc + fc = vc +fc comparing make and buy

sell as is or process further

things to consider

how much revenue will we receive if we sell the product as is?

how much revenue will we receive if we sell the product after proccesing it further?

how muc hextra will it cost to process further?

make sure to ignore sunk costs

chapter 9

whats the first budget?

the sales budget

computation production budet question, direct material budget

know the formulas for both of these

MOH and operating expenses

both have variable and fixed components

Capital Expenditure Budget

plans to purchase property, plant and equipment

Cash collections budget

know its formuala

Cash pyament budget

understand the formula

Combined Cash budet

Beg Cash Balance + collection - payments = balance before borrowing (blank how much to borrow) = ending cash balance

comprehensive budget for merchandising company

Beg Invty + Purchases = GAFS - End Invty + COGS

chapter 10

decentralization advantages vs disadvantages

when a compnay splits operations into different operating segments

advatages - frees top management, encourages use of expert knowledge, iimprove customer + supplier relationships, provide training

disadvantages- duplication of costs, goal incongruence

resposinility center

cost - focus on costs only - internal dptmts (it, acct, hr, legal)

revenue - focus on revenues only - regional sales office territory, call center sales units

profit - concerned about revenues and costs - stand alone stores or restruarants

investments - c0ncerned about revenue + costs and managing assets (parent or large division of a corp)

facorale vs unfavorable

favorable - (good) sales > budget, costs <budget

unfavorable - (bad) sales < budget, costs > budget

management by exception

only investigate variances which meet some threshold

ROI

Return on investment

Operating Income/ Total Assets

Sales Margin

Operating Income / Sales

Capital Turnover

Sales/ Totall Assets

Residual INncome

Operating Income - ( Target rate of return x total assets)

Flexible Budget

budget using actual sales volume with budget per unit information

Work Happy balloon company question

solve for flexible budget and volume variance

KPI’s - key performance indicators

financial perspective - “ how do we look to shareholders” sales, growth, sales margin, gp, roi

customer perspective - customer satisfaction rating, number of repat customers.