Economics Us1

1/24

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

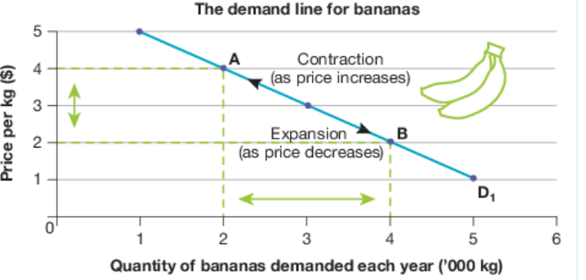

What is the difference between a movement and a shift?

Movements occur along the demand or supply curve. They are caused by a change in the price of the good or service itself, which is described by the Law of Demand and the Law of Supply.

Shifts involve a change in the position of the entire curve. These are caused by non-price factors that change the level of demand or supply at every price point.

Factors Causing a Shift

For Demand: The position of the demand curve shifts due to changes in disposable income, the prices of substitutes and complements, consumer tastes and preferences, interest rates, population demographics, and consumer confidence.

For Supply: The position of the supply curve shifts due to changes in the costs of production, technology, productivity, and climatic conditions or other disruptions.

What is a market

a market is the main instrument for allocating scarce resources, it exists in any place( doesn't have to be physical) where buyers and sellers exchange goods and services

How is market price decided

economic agents are self-interested meaning the price for which a good/service is sold at is typically a compromise between 'willing to pay'(buyers) and 'willing to accept'(sellers)

key features of Aus. Market

Aus has a market based capitalist economy/economic system where key economic decisions are made through the price or market based system where buyers and sellers negotiate the price for each type of good & service rather than relying on government direction

Perfectly Competitive Market

forms the basis of demand and supply analysis to illustrate the operations of the market (price) mechanism

Conditions of Perfectly competitive market

Large Number of Buyers and Sellers: The market consists of so many participants that no single buyer or seller has the market power to influence the price. Because each firm is too small to affect the market, they are considered price takers who must accept the prevailing market price.

Homogenous Products: All goods and services are identical (homogenous), meaning there are no differences in quality, features, or branding. Since products are perfect substitutes, consumers will always choose the cheapest option, and firms cannot compete on anything other than price.

Ease of Entry and Exit: There are no barriers to entering or leaving the market, such as high start-up costs or government restrictions. This allows new firms to enter if they see high profits and existing firms to exit if they are making losses.

Full Information (Perfect Knowledge): Both buyers and sellers have complete access to all information required to make rational economic decisions. Consumers know all prices and product qualities, while producers are aware of market conditions and costs.

Strong Competition: The market is characterized by intense competition between many firms for the same customers. This forces businesses to minimize their costs and operate as efficiently as possible to survive.

Absence of Government Control: The market operates freely without government restrictions or regulations that might dictate prices or supply.

Profit Maximisation: It is assumed that all firms are rational economic agents that use their resources specifically to maximise their profits.

What is market power

Market power is defined as the ability of a business to set or control the market price at which it sells its goods or services. The degree of market power a firm possesses is directly linked to the level of competition in that market.

Nautre of market power

Pure or Perfect Competition (Little to No Market Power): In this structure, there are so many buyers and sellers that no individual can influence the price. These firms are considered price takers because they must accept the prevailing market price. If a farmer in this market tried to raise their price, customers would simply buy the identical product from someone else.

Monopolistic Competition: This structure features a moderate number of sellers. While competition is still quite strong, businesses can gain some influence over price through product differentiation and branding.

Oligopoly: This market is dominated by a few large sellers who often watch their rivals closely when setting prices. There is a higher potential for the abuse of market power in this structure due to the lack of numerous competitors.

Pure or Perfect Monopoly (High Market Power): In a monopoly, a single seller controls the entire output of the industry. Because there are no rival sellers or close substitutes, the firm is a price maker with significant market power to set prices.

Impact of market power

Generally, high levels of competition are seen as beneficial because they limit the market power of individual firms

When market power is low due to strong competition:

Prices are lower, which increases the purchasing power of consumer incomes

Firms are forced to operate more efficiently and minimise costs to surviv

Resources are allocated more efficiently

Conversely, when a firm has excessive market power, such as in a monopoly, the government may monitor the business to prevent unfair pricing or "price gouging"

.

Strategies used by businesses to increase profits

Businesses will develop ways and strategies to sell their goods & services often referred to the 5 Ps’ of marketing namely:-

Product – eg perception of quality, differentiation

Price – Price matching, discounts, sales

People – Customer service, knowledge of staff

Place – Bricks & Mortar vs Online

Promotions – Social media, advertisements

Q: What is demand?

A: The willingness and ability of consumers to buy a good or service.

Q: What is the law of demand?

A: As price increases, quantity demanded decreases; as price decreases, quantity demanded increases.Inverse relationship

Q: Why does demand fall when price rises?

A: Consumers can’t afford it or it exceeds their willingness to pay.

Q: List non-price factors affecting demand.

A:

Disposable income

Prices of substitutes & complements

Preferences & tastes

Interest rates

Population

Consumer sentiment

Government intervention

Q: What is supply?

A: The willingness and ability of producers to sell goods and services.

Q: What is the law of supply?

A: As price increases, quantity supplied increases; as price decreases, quantity supplied decreases.

What is the difference between quantity demanded and an increase in demand?

Quantity demanded: Amount of a good bought at a specific price. Changes only when price changes → movement along the demand curve.

Increase in demand: More of a good is bought at all prices. Caused by non-price factors (e.g. income, tastes) → shift of the demand curve to the right.

What is the difference between quantity supplied and an increase in supply?

Quantity supplied: Amount of a good producers are willing to sell at a specific price. Changes only when price changes → movement along the supply curve.

Increase in supply: More of a good is supplied at all prices. Caused by non-price factors (e.g. lower production costs, technology improvements) → shift of the supply curve to the right.

What market scenarios cause shifts or movements in demand and supply?

Movements along the curve: caused by a change in price only

Demand: change in quantity demanded

Supply: change in quantity supplied

Shifts of the curve: caused by non-price factors

Demand shifts: income changes, tastes/fashion, population, prices of substitutes/complements, expectations

Supply shifts: production costs, technology, number of sellers, government policies (taxes/subsidies), weather (for agriculture)

Non price factors affecting supply

Non-price factors of supply (shift supply curve):

Cost of production (wages, materials)

Technology improvements

Number of sellers in the market

Government policies (taxes, subsidies, regulations)

Natural conditions (weather for agriculture)

Front: What causes movements along demand or supply curves?

Back: A change in the price of the good itself only.

Front: What causes shifts in demand and supply?

Back: Non-price factors such as income, tastes, costs of production, technology, government policies, and population.

Front: What scenarios cause a movement along the demand or supply curve?

Back: A change in the price of the good/service itself.

Demand: price change → movement along demand curve

Supply: price change → movement along supply curve

Front: What scenarios cause a shift in demand or supply?

Back: Non-price factors cause shifts in the curve:

Demand: income, tastes, population, substitutes/complements, expectations

Supply: production costs, technology, number of sellers, government policy, weather/natural events