AF211 Final Exam Review Abrahim Habib

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

The CM ratio can also be calculated by dividing the contribution margin per unit by the total sales.

FALSE

The production budget must be adequate to meet budgeted sales and to provide for the desired beginning inventory for the period.

FALSE

Performance evaluation is difficult when actual activity differs from the planned level of activity.

TRUE

The contribution format income statement can be expressed in the following equation: Profit = (Sales - cost of goods sold) - Fixed expenses.

FALSE

Margin of safety in dollars = Total sales - Break-even sales

TRUE

The margin of safety cannot be expressed in terms of the number of units sold.

FALSE

If variable expenses are 70% of sales, we cannot calculate CM ratio from this information.

FALSE

A budget is a detailed qualitative plan for acquiring and using financial and other resources over a specified forthcoming time period.

FALSE

One disadvantage of budgeting is that it cannot uncover potential bottlenecks.

FALSE

A self-imposed budget or participative budget is a budget that is prepared with the full cooperation and participation of managers at all levels.

TRUE

Motivation is generally higher when individuals participate in setting their own goals than when the goals are imposed from above.

TRUE

Flexible budget can show costs that should have been incurred at the actual level of activity.

TRUE

Flexible budgets improve performance evaluation.

TRUE

Favorable variance occurs when actual revenue is less than budgeted revenue.

FALSE

The differences between the master budget amount and the flexible budget amounts are called master budgeted variances.

FALSE

How do you calculate the contribution margin ratio?

(Sales - Variable expenses) / Sales

The break-even point in unit sales is found by dividing total fixed expenses by:

the contribution margin per unit.

If Q equals the level of output, P is the selling price per unit, V is the variable expense per unit, and F is the fixed expense, then the break-even point in units is:

F / (P- V).

Menlove Company had the following income statement for the most recent year:

Sales (17,000 units) - $357,000

Variable Expenses - 255,000

Contribution Margin - 102,000

Fixed Expenses - 68,000

Net Operating Income - 34,000

Given this data, the contribution margin was:

$6 per unit

$102,000 / 17,000 units = $6 per unit

South Company sells a single product for $20 per unit. If variable expenses are 60% of sales and fixed expenses total $9,600, the break-even point will be:

$24,000 sales, 1,200 units

Which of the following is not a benefit of budgeting?

It eliminates the need for tracking actual cost activity.

Self-imposed budgets typically are:

subject to review by higher levels of management in order to prevent the budgets from becoming too loose.

Which of the following represents the correct order in which the indicated budget documents for a manufacturing company would be prepared?

Sales budget, cash budget, budgeted income statement, budgeted balance sheet

Shown below is the sales forecast for Cooper Inc. for the first four months of the coming year.

Jan. Feb. Mar. Apr.

Cash Sales: $15,000, $24,000 , $18,000 $14,000

Credit Sales: $100,000 , $120,000 , $90,000, $70,000

On average, 50% of credit sales are paid for in the month of the sale, 30% in the month following sale, and the remainder are paid two months after the month of the sale. Assuming there are no bad debts, the expected cash inflow in March is:

$119,000

Walsh Company expects sales of Product W to be 60,000 units in April, 75,000 units in May and 70,000 units in June. The company desires that the inventory on hand at the end of each month be equal to 40% of the next month's expected unit sales. Due to excessive production during March, on March 31 there were 25,000 units of Product W in the ending inventory. Given this information, Walsh Company's production of Product W for the month of April should be:

65,000 units

A static budget:

is valid for only one level of activity

Which of the following comparisons best isolates the impact of a change in activity on performance?

static planning budget and flexible budget

Which of the following would not appear on a flexible budget performance report?

The previous year's actual costs.

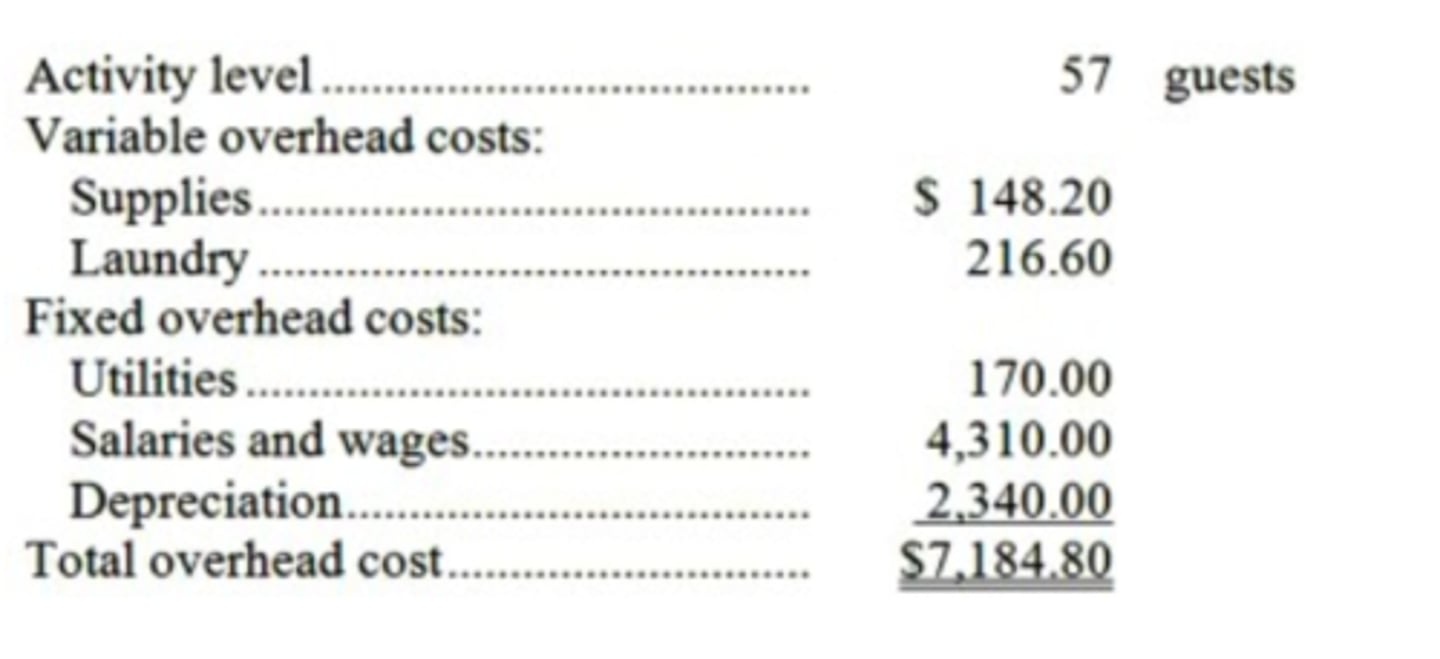

Salyers Family Inn is a bed and breakfast establishment in a converted 100- year-old mansion. The Inn's guests appreciate its gourmet breakfasts and individually decorated rooms. The Inn's overhead budget for the most recent month appears below:

The Inn's variable overhead costs are driven by the number of guests. What would be the total budgeted overhead cost for a month if the activity level is 53 guests?

$7,159.20

Wadhams Snow Removal's cost formula for its vehicle operating cost is $1,900 per month plus $430 per snow-day. For the month of December, the company planned for activity of 16 snow-days, but the actual level of activity was 21 snow- days. The actual vehicle operating cost for the month was $11,470. The vehicle operating cost in the planning (Master) budget for December would be closest to:

$8,780

Static Planning / Master Budget

A budget created before the period begins that is anchored to a single, specific planned level of activity.

Which budget is prepared before the period begins and remains unchanged regardless of the actual level of activity achieved?

Flexible Budget

A budget that estimates what revenues and costs should have been, given the actual level of activity achieved during the period.

An accounting report that recalculates a company's standard cost formula ($Y = a + bX$) using the actual level of activity ($X$) is known as a:

Actual Results

The real revenues earned and expenses physically paid out during the current operational period.

When evaluating a monthly performance report, the numbers in the "Actual Results" column represent:

Activity Variance

The difference between the flexible budget amounts and the static planning budget amounts, caused solely by the difference in volume.

The variance that isolates the impact of a change in activity level on costs and revenues by comparing the Flexible Budget to the Static Planning Budget is the

Flexible Budget Variance (Spending/Revenue Variance)

The difference between the actual results and the flexible budget, measuring how efficiently costs were controlled and how effectively items were priced.

If a manager wants to know how well they controlled operating expenses for the 21 days of work actually performed, they should look at the difference between Actual Results and the Flexible Budget, which is called the:

Price Variance

A breakdown of the spending variance that measures the difference between the actual price paid for an input and its standard budgeted price.

An unfavorable Price Variance for Direct Materials indicates that the purchasing department:

Quantity Variance (Efficiency Variance)

A breakdown of the spending variance that measures the difference between the actual quantity of an input used in production and the standard quantity that should have been used.

If a factory production team wastes materials due to poorly trained workers or machine malfunctions, which variance will capture this specific issue?