introduction to accounting

1/196

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

197 Terms

fundamental qualitative characteristics

relevance: if it has

predictive value

confirmatory value

→ must also cross threshold of materiality

faithful representation

completeness

neutrality

freedom from error

difference between management and financial accounting

management: for internal users, managers making decisions

unregulated, forward looking, tailored to need

financial: for external users, shareholders, lenders regulators

regulated, historical, standardised

four enhancing qualitative characteristics

comparability

verifiability

timeliness

understandability

sole proprietorship

owned by one individual, often small eg. driving instructors

+easy to set up and dissolve

+no legal obligation to disclose to external users other than tax authorities

-unlimited liability

partnership

owned by two or more individuals, eg. dentists/lawyers

+shared ownership and burden

+specialisation opportunities

-limited individual decision-making

-usually unlimited liability

limited liability

owned by one or more individuals, eg. loyds bank plc

+limited liability

+more financing opportunities than sole proprietorships and partnerships

-regulations

statement of financial position

provides a ‘snapshot’ of financial position at a point in time

income statement

measures financial performance of a business over a period

statement of cash flows

summaries the inflows and outflows of cash and cash equivalents for a business over a period

assets

resources held by the company, is an economic resource under the control of the business , measured in money

liabilities

what the company owes to parties apart from the owner(s), claim of other parties

equity

what is left for the owner(s) after liabilities are settled, owner’s residual claim

the accounting equation

assets = equity + liabilities

current assets

short-term held assets which meet any of the following:

held for sale/consumption during normal operating cycle/ 12 months after date of the relevant SoFP

eg. cash & cash equivalents, inventories, trade receivables, prepaid expenses

non current assets

long term assets held for continuing use, fixed (tangible or intangible)

claim

an obligation to provide cash or some form of benefit to an outside party. two types:

equity

liabilities

current liabilities

amounts due for settlement in the short term (12 months or normal operating cycle)

accrued expenses

trade payables

eg. bank overdrafts

bank loan to be repaid in 12 months

non-current liabilities

amounts due that do not meet the definition of current liabilities (eg. long term loans over 1 year)

long-term bank loans

loan notes/ bonds/ debentures

5 accounting conventions

business entity: business ≠ owner(s). they are separate economic units - regardless of legal form

historic cost: records assets as acquisition cost. reliable, but may not reflect current market value

prudence: be cautious. don’t overstate or understate the financial position

going concern: assume the business will continue operating into the foreseeable future → ‘exit’ values have limited relevance and historic costs can continue to be used as a valuation basis

dual aspect: every transaction affects at least 2 accounts (has 2 effects) and both need recirding if the entity uses a double entry system- this is what keeps the SoFP in balance

difference between business entity and limited liability

entity is an accounting concept ; limited liability is a legal status of the owners

standard layout of SoFP

non-current assets + current assets = total assets

equity + non current liabilities + current liabilities = total equity and liabilities

4 key profit formulas

profit = revenue - expenses

gross profit = sales - CoS

CoS = opening inventory + purchases - closing inventory

operating profit = gross profit - operating expenses

cost of sales

cost of goods that are sold during the period

some goods bought during the period may remain as inventories at the end of the period

in some businesses, the cost of sales for each individual item is identified at the time of the sale

calculation of cost of sales

cost of sales = opening investments + purchases - closing inventories

accruals convention

revenue is recognised when earned and expenses recognised when incurred regardless of when cash is paid/received

profit = revenue - expenses

cash sale - revenue = cash

revenue increases/ income statement increases (equity up)

trade receivables increase (asset up)

accrued expenses

expenses that are outstanding at the end of the reporting period

recorded as liabilities (usually current0 on the SoFP)

prepaid expenses

expenses that have been paid in advance at the end of the reporting period

recorded as assets (usually current) on the SoFP

non-current assets with finite lives

provides benefits for a limited period due to market changes, wear and tear ect.

amount used up is referred to as depreciation for tangible non-current assets and amortisation for intangible ones

carrying amount (aka net book value) is cost accumulated depreciation (amortisation)

non-current assets with indefinite lives

provides continuous benefits without a foreseeable time limit, not subject to depreciation/ amortisation

two methods of depreciation

straight line method and reducing balance method

straight line method

use when economic benefits are consumed evenly over time (eg. buildings)

annual depreciation expense = [ cost(fair value) - estimated residual value]/estimated useful life

cost - accumulated depreciation = carrying amount

reducing balance method

use when economic benefits consumed decline over time (eg. cars)

annual depreciation expense = carrying amount x depreciation rate

disposal (and equation)

when an asset is sold, we need to calculate the gain/loss on disposal

gain(loss) on disposal = sale proceeds - carrying amount

statement of comprehensive income

extends the conventional income statement to include other comprehensive income (OCI): unrealised gains and some unrealised losses that affect equity

unrealised gain(loss)

refers to an increase(decrease) in the value of an asset/ investment that has not been sold eg. property revaluation gain

impact of bad debts (such as credit sales) on financial statements

where is is reasonably certain the customer won’t pay, the amount owed is considered an irrecoverable debt(bad debt) and written off

where it is doubtful a customer will pay, an allowance for trade receivables expense should be created

when you make a prepayment:

cash goes down (asset down)

prepayment goes up (asset up)

control over an asset

the entity has the ability to direct use of the asset and obtain the economic benefits from it

→ ownership is not necessary for a resource to be classified as an asset

business entity convention

establishes a clear separation between a business and its owners for accounting purposes

accurate assessment of financial performance easier to compare financial data with other entities personal tax vs. corporate tax

applies to limited companies, sole proprietorships and partnerships

general ledgers

record transactions in general ledgers, which includes different accounts

trial balance

general trial balance (i.e summary of account balances) from general ledger

double-entry bookkeeping

each transaction is recorded in account

an account (T-account) is a record of transactions relating to an item of asset, claim, revenue or expense

trial balance

shows the balances on each account at a date, making cure total debits=total credits

providing some assurance that the accounts have been recorded correctly when the totals agree

trade receivables equation

beg. trade receivables + credit sales - receipts from credit customers - bad debts written off = end. trade receivables

net trade receivables = gross trade receivables - allowance for trade receivables

trade payables equation

beg. trade payables + credit purchases - payments to credit suppliers = end. trade payables

ordinary shares (or equities)

represent basic units of ownership of a company

ordinary shareholders

may receive a dividend (if they’re given) only after claims of lenders and preference are satisfied, have voting rights, face limited downside risk but unlimited upside potential

issue price

the price at which shares are initially offered to investors

nominal (par) value

total nominal value of shares issued by the company

issue share capital

total nominal value of shares issued by the company

share premium

additional amount paid by shareholders over the nominal value of shares

statement of changes in equity

provides details on changes in a company’s equity (share capital and reserves) over a specific period

retained earnings equation

beg. retained earnings + profit for the year - dividends declared = end. retained earnings

dividends

distribution of wealth to shareholders, but not an expense (listed as cash distribution not operating expense in income statement)

declaration of dividends

board of directors formally announces the intention to pay dividends at a specific date

statement of cash flows

summarises the inflows and outflows of cash and cash equivalents over a period

key components:

cash flows from operating activities (CFO)

cash flows from investing activities (CFI)

cash flows from financing activities (CFF)

net CFO + net CFF = net increase/(decrease) in cash and cash equivalents

cash flows from operating activities (CFO)

principle revenue - producing activity of the entity

cash flows from investing activities (CFI)

acquisition and disposal of long-term assets and other investments not included in cash equivalents

cash flows from financing activities (CFF)

activities that result in changes in the size and composition of the contributed equity and borrowings of the entity

cash equation

beg. cash + net increase/(decrease) = end. cash

cash flows from operating activities : direct method

major classes of gross receipts and gross cash payments are disclosed

cash flows from operating activities: indirect method

profit/loss adjusted for for the effects of transactions of a non-cash nature, any deferrals or accruals of past or future operating cash receipts/payments , and items of income or expense associated with investing or financing cash flows

profitability

measuring how successful a business is in creating wealth for its owners

return on capital employed (ROCE) equation

ROCE=(operating profit)/(equity+non-current liabilities) * 100%

gross profit margin equation

GPM= gross profit/ sales * 100%

operating profit margin (OPM) equation

OPM= operating profit/ sales * 100%

net profit margin equation

NPM = profit for the year/ sales * 100%

efficiency

measuring how efficient a business is in using resources (eg. inventory or employees)

average inventories turnover period equation

average inventories held/ cost of sales * 365 days

average settlement period for trade receivables

average trade receivables/ credit sales * 365 days

average settlement period for trade payables equation

average trade payables/ credit purchases * 365 days

sales revenue to capital employed (SRCE)

sales/ (equity + non-current liabilities)

sales revenue per employee

sales/ number of employees

liquidity

measuring a business’s ability to meet maturing obligations using liquid resources

current ratio equation

current assets/ current liabilities

quick ratio (aka ‘acid test ratio’) equation

(current assets-inventories)/ current liabilities

financial gearing

measuring the extent to which loan finance is employed and the consequent effect on the level of risk borne by a business

gearing ration equation

non-current liabilities/ (equity + non-current liabilities) *100%

investment

helping shareholders assess the returns on their investment

dividend payout ratio equation

dividends announced for the year/ (profit for the year-preference dividends) *100%

dividend cover ratio equation

1/ dividend payout ratio

dividend yield equation

dividend per share/ market price per share * 100%

earnings per share (EPS)

(profit for the year- preference dividends)/ number of ordinary shares in issue

price/earnings (p/e) ratio

market price share/ earnings per share

depreciation

non-current asset decreasing in value

why we do management accounting?

strategies/ long-range plans- helps companies plan future

resource allocation, pricing- methods of costing/ pricing strategies

planning and control- revises budget compared to actual output and revises previous budget

performance measurement, staff evaluation

functions of management accounting:

helping manager of company make better decisions about the business in terms of operation

→decision making

cost

a resource sacrificed or forgone to achieve a specific objective

eg. resources such as labour, raw materials, time

in the context of decision making, managers need to know costs for:

controlling (regards the past):

measuring/ evaluating performance

forecasting (regards the past):

budgeting/ planning

operational decisions vs. one off decisions

operational:

pricing

output levels

profit shares

bonuses for employees- related to performance measurement

one off decisions:

accept/ reject project

price for one off contract

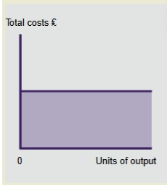

fixed cost

independent of the level of activity

remains constant regardless of change in production/ sales volume

such as rent and salary

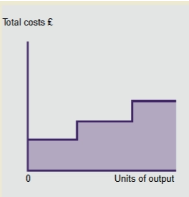

stepped costs

an extension of fixed cost, where cost is fixed up until a certain level of activity

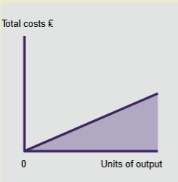

variable costs

varies with the level of activity

fluctuate in direct proportion to changes in production levels or sales volume

such as raw material

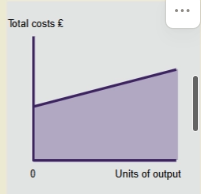

semi-fixed (semi-variable cost)

consists of both fixed and variable cost, components where overall cost increases, only due to the variable element

break-even point

company is not losing money at this level of output, yet profit is not made yet

number of units required to cover the cost

why is breakeven analysis useful?

how many products they need to sell to ensure a profit

whether a product is worth selling or is too risky

the amount of revenue the business will make at each level of output

whether costs need to be reduced to lower the BEP

quick and easy to analyse

break even analysis limitations

ignores behaviour outside range of analysis

assumes constant variable cost per unit

assumes constant selling price per unit

must be single product or constant product mix

assumes no change in efficiency or productivity of workers

assumes volume is the only factor affecting costs (eg. weather effects)

formula for break even point (remember)

b* = fixed cost/ (sales revenue per unit - variable cost per unit)

BEP = FC/ contribution per unit

→ the denominator leads to the notion of contribution which is valuable in making short term decisions

contribution equation

contribution = sales revenue - variable cost

= price minus variable/marginal costs

contribution per unit = (revenue - variable costs) / units

→ positive contribution is good

margin of safety and equation

the planned volume of output/ salles lies above the breakeven point, which can also be used as a partial measure of risk

→ how much production can decrease before the starts losing money

margin of safety = t - b = target output - breakeven point