Basic Economics Final

1/127

Earn XP

Description and Tags

Test 1,2,3 + Chapter 16

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

128 Terms

If a market shortage exists

consumers will compete for the product by offering to pay more.

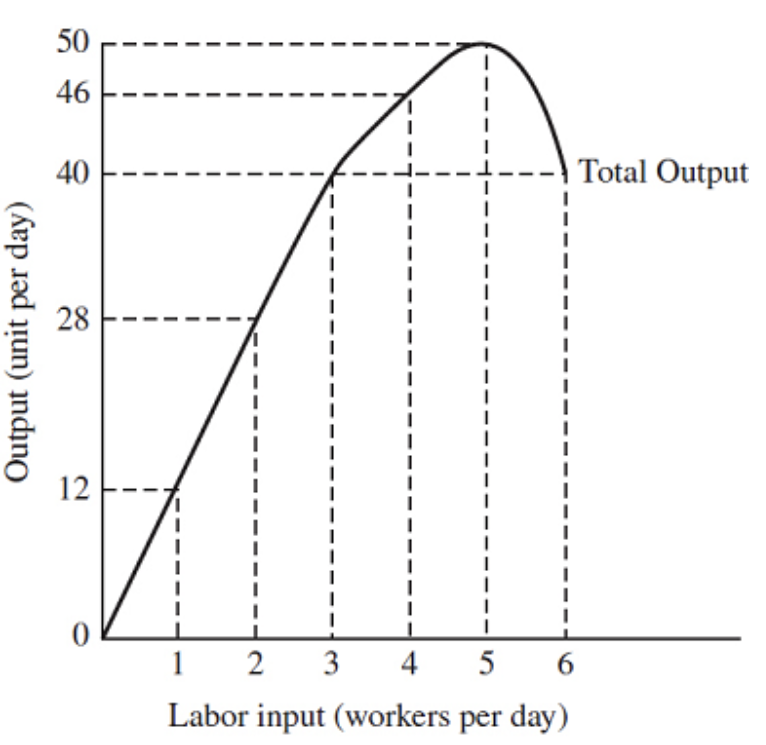

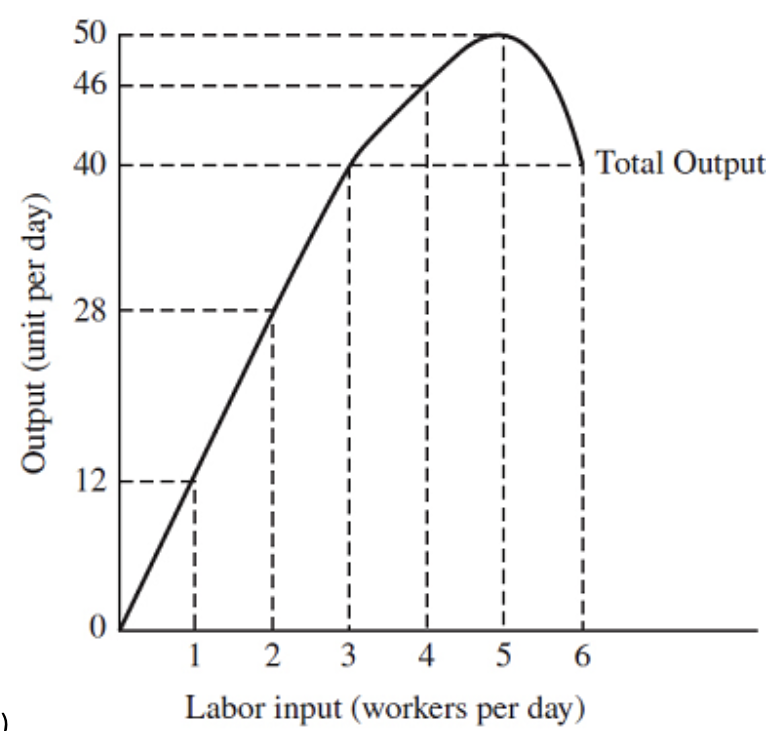

According to the graph, the marginal physical product of the third unit of labor is

12 units per worker

The price of chocolate candy bars rises. This could be due to

a decrease in the number of chocolate candy bar producers.

As output increases, fixed costs

do not change

If demand is elastic, then:

Quantity demanded is very responsive to changes in price.

Which of the following is associated with microeconomics?

An increase in sales for a chain of pet supply stores

The law of demand states that:

Price and quantity demanded are inversely related.

Which of the following is a determinant of supply?

prices of the factors of production

In a market, the equilibrium price is determined by

the interaction of both demand and supply.

Which of the following is NOT a factor of production?

The money hidden in an old basement.

Economic profit equals

total revenue minus explicit and implicit costs

Nominal GDP measures the

value of output produced in current prices.

An increase in the supply of frozen yogurt will take place when

the cost of producing frozen yogurt decreases.

Which of the following is included in investment, according to economists?

production of plant and machinery

Consumer goods

account for over two-thirds of total U.S. output

Opportunity cost may be defined as the

value of the most desired goods or services that are forgone in order to obtain something else.

Sociopsychiatric explanations of consumer demand for a good or service include the:

Desire for ego and status

The response of quantity demanded to price changes is shown by:

The price elasticity of demand

Which of the following will NOT cause a shift in the demand curve for a good?

the price of the good itself

In economic theory, utility refers to the:

Satisfaction obtained from a good or service.

According to the law of demand, a change in _______ causes a movement along the demand curve.

the price of the good

Explicit costs

are the sum of actual monetary payments made for resources used to produce a good

A market

is any place (physical or digital) where goods are bought and sold.

Marginal physical product is

the additional output from using one more unit of labor.

GDP can be found by

adding the monetary value of all final goods and services produced during a given period of time.

During the long run

the firm can build or lease any size factory

When income increases, the demand for most products

Increases and the demand curve shifts to the right.

Economic cost is

the value of all resources, both explicit and implicit, used to produce a good or service.

According to the graph, the diminishing marginal returns first occur with the

third worker

Market participants include

consumers, business firms, governments, and foreigners.

Marginal cost

may initially decline and then increase as more output is produced.

Economic growth always takes the form of

an expansion of production possibilities.

The primary concern of economics is the study of

how best to allocate scarce resources among competing uses.

Total revenue is:

The price of a product times the quantity sold in a given time period.

The price of a good or service

serves as the essential signal of the market mechanism.

Which of the following is a goal of businesses?

to maximize profits given resource constraints

In attempting to answer the WHAT question, a society seeks to

produce the optimal mix of output.

Market demand represents the:

Sum of all individual demands for a product at each possible price.

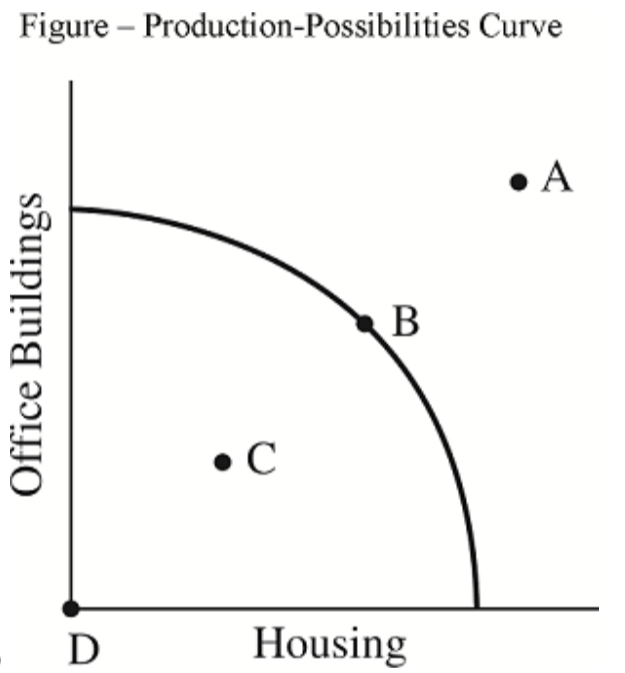

Society is employing some of the available technology but not all of it. Select the appropriate point that could represent this situation.

C

The general shape of the average total cost curve is

u-shaped

If society lacks enough resources to satisfy all the desired uses of the resources, this is known as

scarcity

Government services

include federal, state, and local government purchases of goods and services.

Which of the following statements is consistent with central planning?

Government planners play the dominant role in deciding how resources are allocated.

Marginal utility refers to the:

Additional utility from consuming the last unit of a good or service.

In economic theory, total utility refers to:

The amount of utility obtained from the consumption of a certain amount of a good or service.

Market structure is determined by

the number and relative size of firms in a specific market.

An individual competitive firm

produces a small proportion of output relative to the market.

Which of the following is an example of perfect competition?

Many small firms all produce the same good.

Which list has market structures in the correct order from the most to the least market power?

monopoly, oligopoly, monopolistic competition, perfect competition

A perfectly competitive firm currently sells 30,000 cartons of eggs at $1.25 each. If the firm wants to sell one more carton of eggs, the firm

should price the carton at $1.25.

From the firm perspective, the price of a good multiplied by the quantity sold equals

total revenue.

If marginal cost equals price, then _________ is at a maximum.

profit

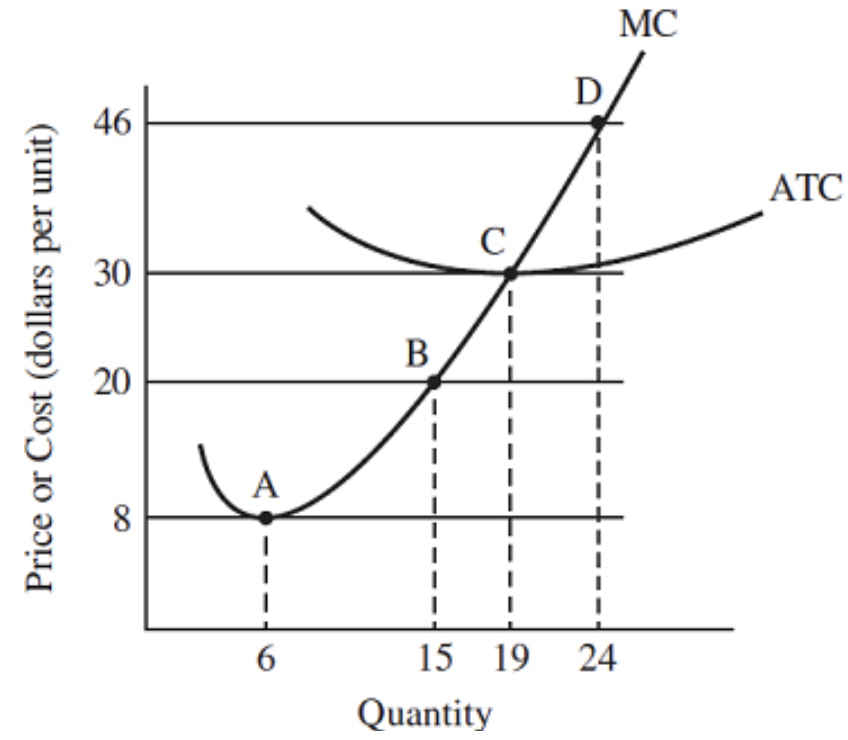

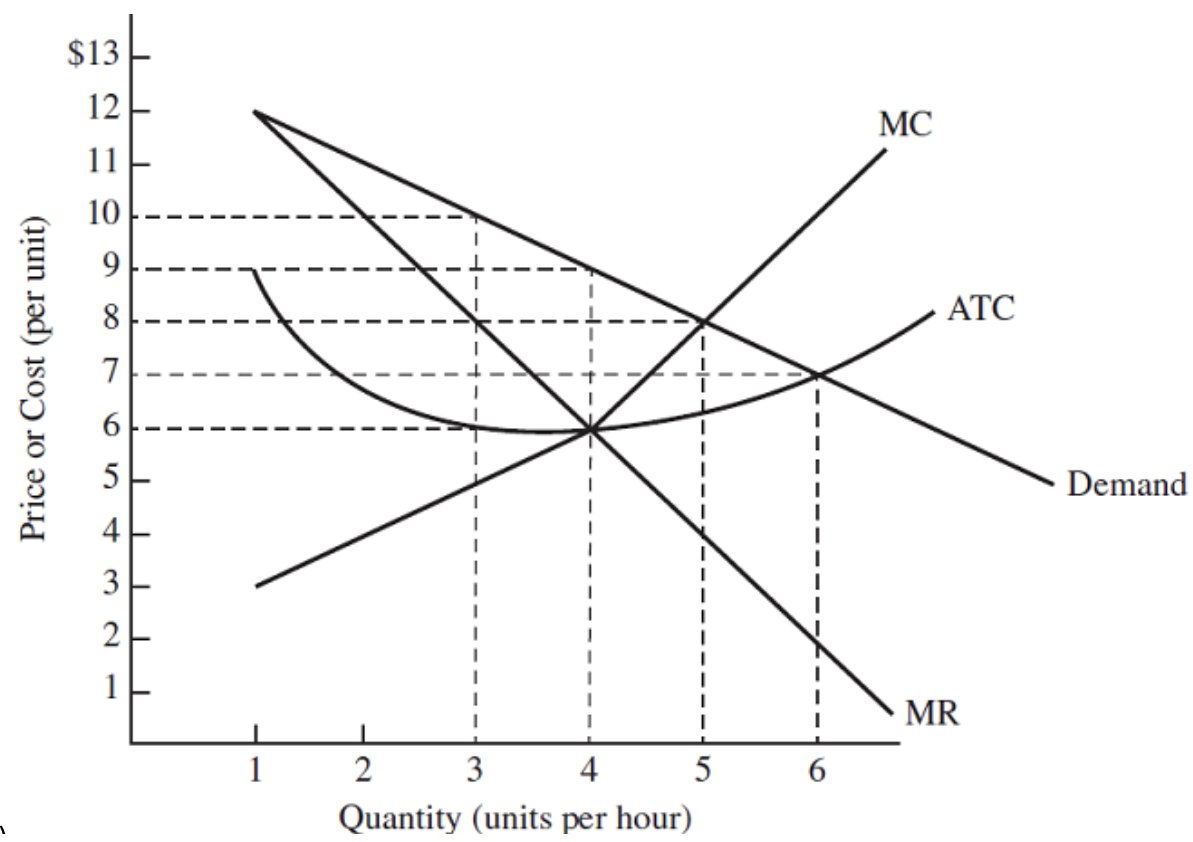

Refer to the graph. If the market price is $46 for this perfectly competitive firm

there will be economic profits.

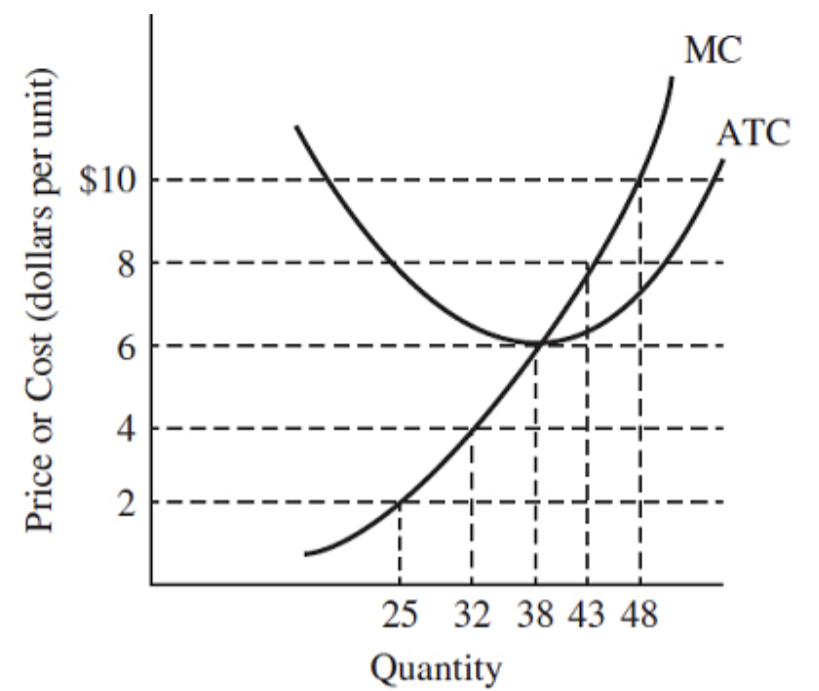

Refer to the figure. If price is $4, the profit-maximizing rate of output for this perfectly competitive firm is

32 units.

When firms exit an industry, price _________ and industry output _________.

increases; decreases

Which of the following firms is likely to have the greatest market power?

the sole producer of the latest computer microchip technology

The demand curve for an individual monopolist

is the same as the market demand curve.

Which of the following might be used to protect a monopoly from competition?

a patent

If the entire output of a market is produced by a single seller, the firm

is a monopoly.

Which of the following is not true for a monopoly?

It is a price taker.

The change in total revenue that results from a one-unit increase in quantity sold is

marginal revenue.

The marginal revenue of a monopolist is

less than price because to sell more output the firm must reduce the price on all units sold.

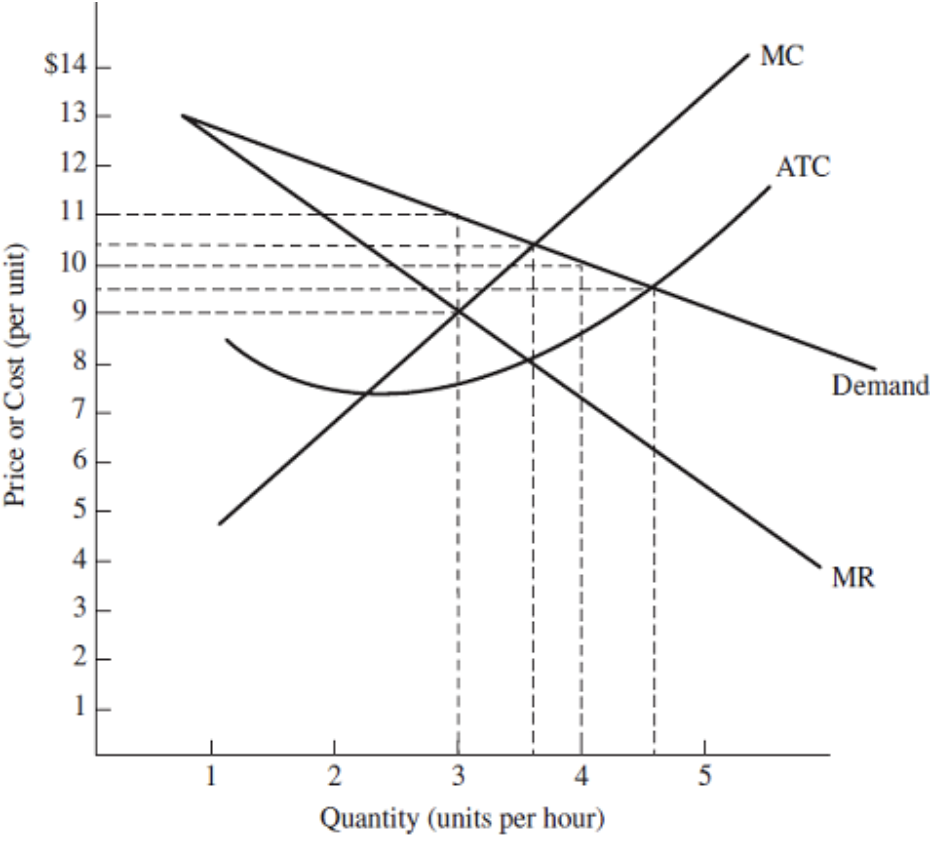

Refer to the figure. The price charged by this profit-maximizing monopolist is

$11 per unit.

Refer to the figure. The profit-maximizing rate of output for this monopolist is

4 units per hour.

In the figure, at the profit-maximizing level of output for a monopolist, marginal cost is

$6 per hour.

The labor-supply curve depicts the quantity of _________ at alternative _________.

labor supplied; wage rates

The quantity of labor supplied

increases as the wage rate increases.

The opportunity cost of working is the

value of leisure time that must be given up.

Generally, as the number of hours worked increases, the marginal utility of leisure time tends to

increase.

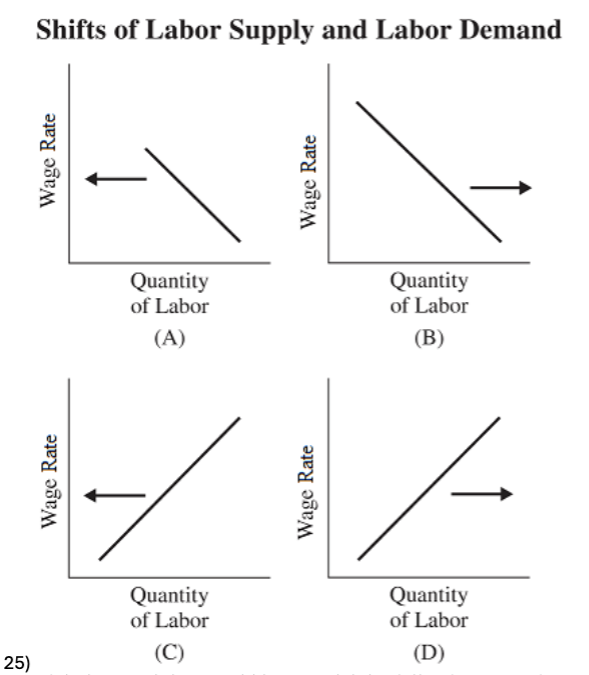

Pick the panel that would best model the following scenario: A significant number of immigrants enter the labor market.

D

If market prices and sales are used to signal desired output, then the optimal mix of output would be determined by

the market mechanism.

A market failure occurs when

an imperfection in the market mechanism prevents an optimal outcome.

A private good is unique because

nonpayers can be prevented from consuming it.

Which of the following is most likely a private good?

cars

In economics, a public good

cannot be denied to consumers who do not pay.

allows free riders to benefit from the good.

Which of the following is most likely a public good?

a park

The problem with public goods is that those who do not pay receive

the same amount of the good as those who pay.

The free-rider dilemma is associated with

public goods.

The term externalities refers to

all costs and benefits of a market activity borne by a third party.

The study of aggregate economic behavior is referred to as

macroeconomics.

Alternating periods of growth and contraction in real GDP define

the business cycle.

Which of the following is characteristic of a downturn in the business cycle?

higher unemployment rates

As the economy falls from the peak to the trough of the business cycle

cyclical unemployment should increase and real GDP should decline.

Who among the following would be counted as unemployed?

Bob, a college student looking for summer work

Joseph is unemployed. He was working at a thrift shop in Indiana but decided to go back to school full time to become an engineer. He would be classified as

not in the labor force.

The labor force consists of the

members of the population over age 16 who are employed, or who are actively seeking employment.

Which of the following is an example of the income effect during a period of inflation?

Your income is fixed and does not increase even though the price level is rising.

The uncertainty of inflation is likely to affect

production and consumption decisions.

The Consumer Price Index is

a measure of changes in the average price of consumer goods and services.

Which of the following is a measure of overall economic well-being for the United States?

GDP growth

According to Keynes,

government intervention in the economy is necessary at times.

The various quantities of output that all market participants are willing and able to buy at alternative price levels in a given time period is

aggregate demand.

The difference between market demand and aggregate demand is that

aggregate demand applies to all goods and market demand applies to a specific good.

The value of output in constant prices is measured by

real GDP.

The aggregate demand curve is

downward-sloping.

If an economy is experiencing a recession, the Keynesian approach to achieving full employment is to

use tax cuts, more government spending, or both

Monetary theory is referred to as

a demand-side theory.

According to supply-side theories, if producers are less willing and able to supply goods at prevailing prices, then aggregate

supply shifts to the left.

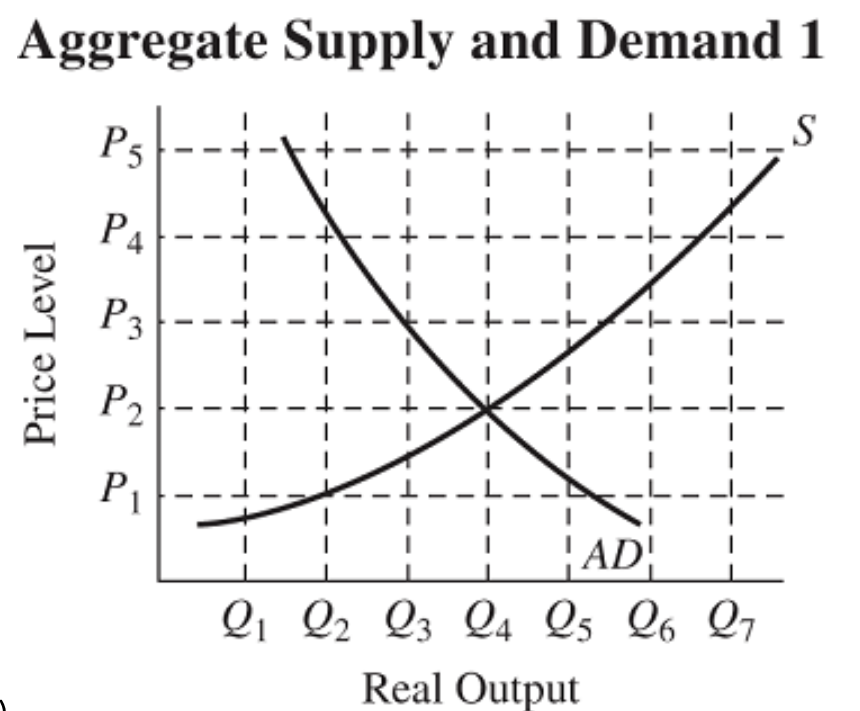

Refer to the figure. Ceteris paribus, if businesses experience higher costs for transporting goods because of an increased price for imported oil, the new equilibrium is likely to occur at

P3 and Q3.

Which of the following relies on government taxes and spending to change macro outcomes?

fiscal policy