Investments Test #2

1/34

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

35 Terms

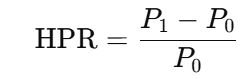

How to find annual return with holding return/period

Portfolio return given weight and return

What is the expected risk regarding CAL?

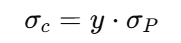

Op = standard deviation

y= weight in the risky portfolio

What are the 3 variables for HPR?

Price Paid

Price Received

Income

HPR

HPRs do not include compounding, and HPRs of two investments are directly comparable when their holding periods are identical.

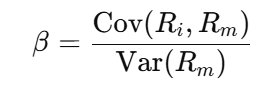

How to find beta given covariance and excess returns

Beta when given weights and betas

Neglected firm effect

stocks of companies that receive little analyst coverage tend to earn higher returns than well-followed companies.

January effect

a market anomaly where stock prices—especially small-cap stocks—tend to rise more in January than in other months

covariance

A measure of comovement between a pair of risky assets, measured on a scale ranging from negative to positive infinity, is called

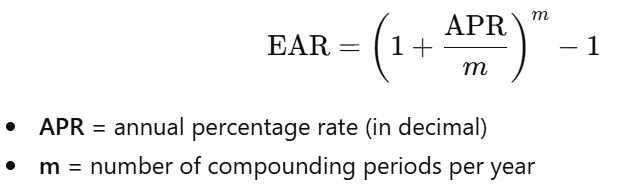

EAR

Return difference and whether it is undervalued, overvalued, or properly valued

subtract given expected return - calculated return

Calculate total return for following months

How to determine if a stock dominates

Higher return + lower risk → dominates

Same return + lower risk → dominates

Higher return + same risk → dominates

Nonstationary beta problem

The beta estimated today differing from the estimation a year from now refers to which problem

Market index bias

The presence of which of these makes it imperative that beta comparison among individual companies reflect identical and appropriate market benchmarks?

when a stock’s beta (or performance) depends on which market index you use as the benchmark.

Time interval bias

happens when a stock’s beta (or risk estimates) change depending on the data frequency used

An adjusted closing price is adjusted for the effects of

dividends paid and stock splits.

The anticipated rate of return when either the beta is 0 or the market rate of return is equal to the risk-free rate is called

alpha

What are the stock's deviations from an expected 4-Factor model return if the realized return is 1%?

Step 1: plug in all #s into CAPM equation

Step 2: Convert to total expected return

R=Rf+(R−Rf)

Step 3: Compute deviation

Deviation (or realized alpha)=Realized Return−Expected Return (from model)

Paco currently has a portfolio with an expected return of 10.25% and a standard deviation of 13.75%. He is wondering if he should reallocate 50% of his current portfolio to an asset class that has an expected return of 15% and a standard deviation of 12%. The correlation between his current portfolio and the other asset class is 0.8. What would be Paco's new return, and by how much would it increase or decrease?

E(Rp) = weight * expected return

subtract new expected return from expected return

Which return/standard deviation could be most stale?

includes outdated, abnormal data that no longer reflects current performance.

What are arithmetic averages better for?

for estimating next-period expected return

What is geometric averages good for?

for measuring actual performance (accounts for compounding); performance evaluation

When should you use population σ or sample σ?

Historical returns are sample (N-1)

Population only for probabilistic scenarios where all outcomes and probabilities are explicitly enumerated (N)

How to solve a multi period HPR problem

Income yield

Income/Price paid

capital gains yield

= (P₁ − P₀) ÷ P₀

Expected return, Required return, and Realized return

Expected: probability weighted forward looking estimate (before the fact)

Required: minimum return investor demands given the risk (before the fact); depends on risk aversion and systematic risk

Realized return: actual return earned - calculated after the fact

Total return

income + capital appreciation

HPR return

total return (income + price change) / beginning price

How to find EAR from APR

Strong, Semi-strong, Weak form

Strong: Current prices reflect all public information and non-public information. All trading rules are pointless

Asset allocation and portfolio construction

Semi-strong: Current prices reflect all public information. All trading rules based on public information are ineffective.

Fundamental analysis with private information, asset allocation and portfolio construction

Weak: Current prices reflect all public information. All trading rules based on public information are ineffective.

Fundamental analysis, asset allocation and portfolio construction

Data snooping

you search through a dataset until you find patterns that look significant—but are actually just random noise

EMH Paradox

Markets are only efficient because people try to beat them—but if everyone believed markets were perfectly efficient, no one would try, and markets would become inefficient.