Final Exam 1.1

1/119

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

120 Terms

Opportunity costs reflect

What you give up or lose when you do one thing instead of another

What you get to do or new expenses you pay when you make your selection

Unrecoverable lost costs

Potential gains available if you take the opportunity

What you give up or lose when you do one thing instead of another

If my willingness to pay is $10 and the price of coffee I plan to buy is $3, then

I am willing to spend no more than $7 to buy the coffee

I am indifferent between buying coffee and finding $7 on the ground

If I find $5 on the ground and am so happy I forget all about the coffee, I know my willingness to pay was higher than $15.

None of these.

I am indifferent between buying coffee and finding $7 on the ground

Which of the following is an application of the marginal principle?

You consider the total cost and benefit of buying meals for the week

You compare your willingness to pay for pizza to the price of one additional slice

You consider the lost ability to buy a burger when you purchase pizza instead.

You consider whether to purchase one additional pizza slice

You consider whether to purchase one additional pizza slice

A person should always buy more pizza as long as

The total benefit from buying pizza is equal to the total cost of buying pizza.

The marginal benefit is at least as big as the marginal cost

The opportunity cost of buying pizza is increasing

There are no serious sunk costs to worry about

The marginal benefit is at least as big as the marginal cost

When the Xbox X was released at $499 and sold out immediately on the Microsoft website, while simultaneously being listed for sale at $1200 on eBay and Wal-Mart’s Marketplace, we conclude

The $499 is a below equilibrium price

The Xbox X is an elastic good

The $499 is an equilibrium price

The $499 is an above equilibrium price

A typical buyer has a willingness to pay of $499

The $499 is a below equilibrium price

What is the total expenditure if you purchase 3 sliced of pizza for $5 each?

$5

$10

$15

$20

None of these are correct

$15

If demand is given by P=10 - Q and currently the price is $2, find the Quantity demanded

8

7

6

5

10

None of these

8

Suppose demand is given by P=10-Q and supply by P=2+Q, but then there’s an increase in the number of buyers. After this happens we know:

The new equilibrium price is some P* < 6

The new equilibrium price is some P* > 6

The new equilibrium price is P* = 5

Demand is elastic

The new equilibrium price is some P > 6*

If Caramel and apples are complements but people also use apples to make pies, we expect

The cross price elasticity of the quantity demanded of Apples to the price of caramel is less in absolute value than the cross price elasticity of the quantity of caramel to the price of apples.

The cross price elasticity of the quantity demanded of Apples to the price of caramel is greater in absolute value than the cross price elasticity of the quantity of caramel to the price of apples.

The cross price elasticity of the quantity demanded of Apples to the price of caramel is equal in absolute value to the cross price elasticity of the quantity of caramel to the price of apples.

Demand for apples is elastic

The cross price elasticity of the quantity demanded of Apples to the price of caramel is less in absolute value than the cross price elasticity of the quantity of caramel to the price of apples.

If demand for Detroit Lions tickets increased by 40% over the last year and supply increased by 10% due to Ford Field renovations, we can conclude

Equilibrium price rises, and equilibrium quantity rises

Equilibrium price could rise or fall, but equilibrium quantity rises

Equilibrium price falls, but equilibrium quantity could rise or fall

Demand is inelastic

Supply is elastic

Equilibrium price rises, and equilibrium quantity rises

If the price of Red Wings tickets increases by 15% and the team sells 5% fewer tickets we know that

Equilibrium price rises, equilibrium quantity falls

Equilibrium price falls, equilibrium quantity rises

E = 1/3 in absolute value

E = 3 in absolute value

E = 15%

E = 1/3 in absolute value

If income falls by 10% and quantity demanded rises by 20% for some good, we know that good

Is inferior

Is normal

Is a complement

Has elastic demand

None of these.

Is inferior

Taco King charges the same price of everything on the menu: $5 for a taco, burrito, or nachos. You buy the burrito and think if you had not purchased the burrito you could have purchased the taco. The opportunity cost of the burrito is:

$5

Your forgone enjoyment of the taco

$5 and your forgone enjoyment of the taco

$5 and your forgone enjoyment of the taco and nachos

None of these.

Your forgone enjoyment of the taco

Researchers find a new strain of olives that is resistant to pesticides and drought while yielding more olive oil. Holding all else constant this will:

Shift the supply curve for olive oil leftward

Increase the quantity supplied of olive oil

Decrease the quantity supplied of olive oil

Shift the supply curve for olive oil rightward

Shift the supply curve for olive oil rightward

Following the rational rule, maximum economic surplus occurs when

Total benefits equal total costs

Total benefits exceed total costs

Marginal benefits equal marginal costs

Marginal benefits exceed marginal costs

Marginal benefits equal marginal costs

If income rises by 20% and the quantity demanded of the item rises by 10%, the income elasticity of demand for the good is:

2

-2

1/2

-1/2

1/2

If two goods are complements their cross price elasticity is:

Positive

Positive but almost equal to zero

Equal to zero

Negative

Negative

The price elasticity of demand measures how responsive:

Buyers are to quantity changes

Buyers are to price changes

Buyers are to income changes

Sellers are to quantity changes

Two of the above

Buyers are to price changes

Kevin goes to a local coffee shop and orders a medium latte. He is willing to pay $6 and the price is actually $2. The cost to the coffee shop to produce the latte is $1. How much economic surplus does the coffee shop receive when Kevin buys the latte?

$6

$4

$2

$1

$1

Surpluses always occur

At the equilibrium price

At prices below the equilibrium price

At price above the equilibrium price

When the quantity demanded exceeds the quantity supplied

At price above the equilibrium price

Which is most likely to have a vertical supply curve?

Pepper

Olive oil

Prescription drugs

Sculptures by Michelangelo

Sculptures by Michelangelo

A meat processing plant produces both steak and ground beef. What effect would a rising market price for steak have on the supply for ground beef?

The quantity of ground beef supplied will increase

The supply of ground beef will increase

The supply of ground beef will decrease

The supply of steak will decrease

The supply of ground beef will decrease

It is certain that the equilibrium quantity will fall when the supply curve:

And the demand curve both shift to the right

Shifts to the right and the demand curve shifts to the left

And the demand curve both shift to the left

Shifts to the left and the demand curve shifts to the right.

And the demand curve both shift to the left

Butter producers know the price elasticity of demand for butter is 0.2. If they want to increase the amount sold by 4%, the will have to lower price by:

0.1%

1%

4%

20%

20%

The Taco King franchise installs touch-screen kiosks for customers to place orders. This enables the restaurant to employ fewer cashiers to take orders but it must hire a skilled technician to maintain the new kiosks. These changes suggest:

Cashiers and kiosks are substitutes, and skilled technicians and kiosks are complements

Cashiers and kiosks are complements, and skilled technicians and kiosk are substitutes

Skilled workers, such as technicians, are cheaper than unskilled workers such as cashiers

Kiosks are a substitute for both skilled and unskilled workers

Cashiers and kiosks are substitutes, and skilled technicians and kiosks are complements

Shelby consumes 100% more pencils when the price of pens rises by 50%. For Shelby, pencils and pens are (blank) and the cross price elasticity of demand is (blank)

Complements, 0.5

Substitutes, -0.5

Complements, 2

Substitutes, 2

Substitutes, 2

The marginal benefit from an additional workers is

The additional benefit from hiring one more worker

The total benefit from all workers hired

Always equal to the benefit from the first worker hired

Always equal to the cost of hiring the additional worker

The additional benefit from hiring one more worker

An increase in the price of shoes would probably result in (blank) in the demand for shoe laces

A decrease

An increase

No change

Random fluctuation

A decrease

In the early 1990’s Canadian fashion model Linda Evangelista famously said, ``We don’t wake up for less than $10,000 a day’’ and later Vince Vaughn in Mr & Mrs. Smith (2005) says ``I don’t get out of bed for less than half a million dollars.’’ Both phrases best exemplify:

Sunk costs

The cost benefit principle

The marginal principle

The interdependence principle

The opportunity cost principle

The opportunity cost principle

Last year, the equilibrium price for a movie ticket was $12 and the equilibrium quantity sold was 5,000 tickets per week. This year, the equilibrium price remained $12, however the equilibrium quantity fell to 4,000 tickets per week. Which of the following could correctly explain this phenomenon? Assume that movie tickets are a normal good, streaming subscriptions are a substitute for movie tickets, popcorn is a complement to movie tickets, and labor is an input into movie-theater operations.

Consumer incomes decreased, and theater wages decreased.

The price of streaming subscriptions increased, and the supply of movie tickets is perfectly elastic.

Theater wages increased, and demand for movie tickets is perfectly inelastic.

A news report highlighted health concerns about crowded theaters, and there was a decrease in the number of movie theaters.

The price of popcorn increased, and the supply of movie tickets is perfectly inelastic.

A news report highlighted health concerns about crowded theaters, and there was a decrease in the number of movie theaters.

Suppose that the supply of Wolverine/Winged Helmet-edition sneakers is perfectly elastic. If these sneakers suddenly become extremely fashionable so that more consumers want to buy them, what happens to their equilibrium price and quantity?

The equilibrium quantity will increase and the impact on equilibrium price is ambiguous.

Both the equilibrium price and the equilibrium quantity increase.

The equilibrium price increases, but the equilibrium quantity is unchanged.

The equilibrium quantity increases, but the equilibrium price is unchanged.

Both the equilibrium price and the equilibrium quantity are unchanged.

The equilibrium quantity increases, but the equilibrium price is unchanged.

Which of the following would NOT shift the demand curve for movie theater tickets?

A report by a national health organization warns that prolonged sitting in movie theaters increases the risk of back problems.

An increase in wages paid to movie theater employees.

An increase in the price of streaming services, which are substitutes for movie theater attendance.

A decrease in the price of streaming services, which are substitutes for movie theater attendance.

An increase in wages paid to movie theater employees.

Suppose the market for ride-share trips in a city is currently in equilibrium at a price of $18 per trip and a quantity transacted of 2.0 million trips per year. If the following events occurred, what impact would they have on the equilibrium price and quantity in the market for ride-share trips? Assume that ride-share trips and taxi rides are substitutes in consumption.

I. A city regulation increases licensing fees for taxi companies, raising the cost of providing taxi rides.

II.A new driver-routing algorithm reduces the per-trip operating cost for ride-share companies

III. A major employer announces a return-to-office policy, increasing the number of commuters.

Equilibrium price will rise for certain and equilibrium quantity will rise for certain.

Equilibrium price will rise for certain and the impact on equilibrium quantity is unknown.

Equilibrium price will fall for certain and the impact on equilibrium quantity is unknown.

Equilibrium quantity will rise for certain and the impact on equilibrium price is unknown.

Equilibrium quantity will fall for certain and the impact on equilibrium price is unknown.

Equilibrium quantity will rise for certain and the impact on equilibrium price is unknown.

Which of the following will NOT cause the supply curve for video game consoles to shift?

An increase in the current market price of video game consoles.

A decrease in the cost of microchips used in console production.

A decrease in the expected future price of video game consoles.

A technological improvement in manufacturing that allows consoles to be assembled more quickly.

All of the above will cause the supply curve to shift.

Increase in current market price

A decrease in supply means

There is a smaller quantity supplied at any given price

The cost of inputs and other production costs evidently have fallen

The quantity demanded must rise

The market price must fall to reach the new equilibrium

There is a smaller quantity supplied at any given price

Suppose you observe that both the equilibrium price and equilibrium quantity of electric scooters in a city have fallen. Holding all else constant, which of the following could be consistent with this observation? Assume that electric scooters are a normal good, ride-share trips are a substitute for electric scooter rentals, and charging stations are a complement to electric scooters.

I. Consumers have experienced an increase in income and there is an increase in the number of scooter rental companies.

II. The price of ride-share trips has risen and the price of charging services has fallen.

III. New research reports that frequent scooter use significantly increases injury risk.

IV. The number of scooter rental companies has declined and the price of ride-share trips has declined.

I and III only

III and IV only

I, II, and III only

IV only

I, II, III, and IV

III and IV only

In a particular year, a major concert tour experienced a sharp reduction in available tickets due to unexpected venue closures. As ticket availability fell, the price of tickets rose substantially, leading to a lower quantity of tickets sold, reflecting a movement along the demand curve. In the year before the closures, total revenue from ticket sales was $620 million. In the year of the closures, total revenue rose to $700 million. It must be the case, therefore, that demand for concert tickets was elastic over the relevant portion of the demand curve.

True

False

False

Supply curves are upward sloping because:

I. Eventually output involves diminishing marginal product

II. Consumers follow the rational rule for buyers

III. Input costs rise as additional units are produced

I only

II only

III only

I and II only.

I and III only.

I and III only

Suppose that the initial equilibrium price of monthly streaming subscriptions is $12 per month. If the price of cable television subscriptions (considered a substitute by consumers) increases, what happens in the market for streaming subscriptions?

There will now be a shortage of streaming subscriptions at $12 per month. As a result, the price will rise leading to a decrease in quantity demanded and an increase in quantity supplied.

There will now be a shortage of streaming subscriptions at $12 per month. As a result, the price will fall leading to an increase in quantity demanded and a decrease in quantity supplied

There will now be a surplus of streaming subscriptions at $12 per month. As a result, the price will fall leading to an increase in quantity demanded and a decrease in quantity supplied.

There will now be a surplus of streaming subscriptions at $12 per month. As a result, the price will rise leading to a decrease in quantity demanded and an increase in quantity supplied.

More than one of the above are true.

There will now be a shortage of streaming subscriptions at $12 per month. As a result, the price will rise leading to a decrease in quantity demanded and an increase in quantity supplied.

If Anna is willing to pay up to $15 for Betty’s Pokemon trading card, but buys it from Betty for $7, the economic surplus to Anna as a buyer is (blank). Then if Anna sells the card to Charlie for $20 Anna’s economic surplus as a seller is (blank). Betty’s economic surplus as a seller is (blank).

$15, $7, and $20

$8, $7, and $5

$8, $7, and $15

$8, $13, and unknown.

$8, $5, and unknown.

$8, $13, and unknown

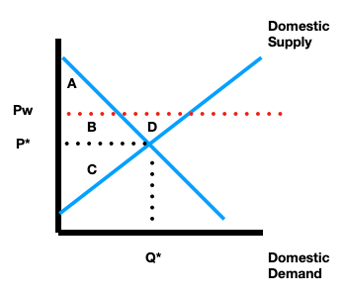

1. If the world price is above the domestic price, the quantity actually traded domestically is Qd. If the world price is below domestic price the quantity actually traded domestically is Qs.

A. True

B. False

True

2. In a market with free trade where the world price is below the domestic price, we can say that domestic buyers compete with foreign buyers at Pw

A. True

B. False

True

3. On graph “B” is transfer from consumers to producers as a result of trade; “D” is new economic value created from transactions between domestic seller and foreign buyer

A. True

B. False

True

4. In a market with free trade where the world price is above the domestic price, we can say that domestic producers compete with foreign producers for domestic buyers’ business

A. True

B. False

True

When there’s free trade and the domestic country is an exporter for some product we can identify new economic value created from transaction between domestic buyer and foreign producer. This is what is meant by the statement ``winners win more than losers lose’’

A. True

B. False

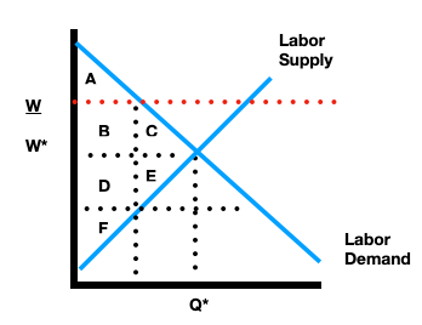

Refer to the labor market appearing in the graph below:

True

In this market we can best describe area C as capturing:

A. Deadweight loss attributed to the forgone ability of firms to hire workers at the new wage.

B. Deadweight loss attributed to the forgone ability of workers to find jobs at the new wage.

C. Consumer surplus to firms

D. Producer surplus to firms

Deadweight loss attributed to the forgone ability of firms to hire workers at the new wage.

Consider an economy with two traders, Vermont and Idaho who both can produce maple syrup and potatoes. It takes Vermont 3 hours to produce 1 shipment of maple syrup and 12 hours to produce 1 shipment of potatoes. It takes Idaho 5 hours to produce 1 shipment of maple syrup and 10 hours to produce 1 shipment of potatoes. On the basis of these data we can conclude:

A. Vermont holds an absolute advantage in both goods

B. Idaho holds an absolute advantage in both goods

C. Vermont holds a comparative advantage in potatoes.

D. Vermont holds a comparative advantage in maple syrup.

Vermont holds a comparative advantage in maple syrup.

Suppose an economy chooses between producing semiconductor chips and coffee. Using the production possibilities frontier model, technological change that improves the production efficiency of semiconductor chips creates a situation where:

A. The economy can produce more semiconductor chips

B. The economy produces more coffee

C. Any efficient combination where the country produces both semiconductors and coffee prior to the technology change becomes inefficient after the technology change.

D. All of these are correct.

E. None of these are correct.

All these are correct

If the goal is to maximize efficiency, which of the following ought to be the basis for trade?

A. Tariffs

B. Absolute advantage

C. Comparative advantage

D. Scarcity

Comparative advantage

One of the primary purposes of studying consumer surplus, producer surplus, and deadweight loss is:

A. An alternative to assessing opportunity costs

B. A different version of the rational rule

C. A better way to understand comparative advantage

D. Analyzing how price & policy changes affect market participants (buyers & sellers) differently.

E. None of these.

Analyzing how price & policy changes affect market participants (buyers & sellers) differently.

A price ceiling of $10 placed above the market equilibrium price of $8 will have the effect of

A. Not disrupting the market equilibrium unless something else causes a change in demand or supply or both

B. Creating a shortage as the quantity demanded will exceed the quantity supplied at the new price

C. Creating a surplus as the quantity supplied will exceed the quantity demanded at the new price

D. Introduce an incentive for consumers to obtain the good from outside the main market, which is how underground economies are formed.

E. None of these.

Not disrupting the market equilibrium unless something else causes a change in demand or supply or both

A price floor $200 when the equilibrium price is $150 will have the effect of

A. Creating a shortage in the market as the quantity demanded will exceed the quantity supplied

B. Creating a surplus in the market as the quantity supplied will exceed the quantity demanded

C. Have no impact on the market

D. Causing an increase in supply

E. None of these.

Creating a surplus in the market as the quantity supplied will exceed the quantity demanded.

If you want to argue that raising the minimum wage will cause a relatively small change in the total number of workers employed, it will help your argument if:

A. Demand is relatively elastic

B. Supply is relatively elastic

C. Demand is relatively inelastic

D. Supply is relatively inelastic

E. None of these.

Demand is relativelty inelastic

Consider the market for chocolate chip cookies near campus which we can assume has standard negatively sloped demand and positively sloped supply. Suppose the current equilibrium price is $5 per cookie with quantity of 500 per day. If the city imposes a per-unit tax of $1 per cookie we know:

A. The new equilibrium price will be $6, but the quantity will remain at 500

B. The new equilibrium price will be $6, and the quantity will be something less than 500

C. The new equilibrium price will rise, but stay below $6 and the quantity will fall

D. The new equilibrium price will rise, but stay below $6 and the quantity will be 500.

E. None of these.

The new equilibrium price will rise, but stay below $6 and the quantity will fall

Consider the market for chocolate chip cookies near campus which we can assume has standard negatively sloped demand and positively sloped supply. Suppose the current equilibrium price is $5 per cookie with quantity of 500 per day. If the city imposes a per-unit tax of $1 per cookie we know:

A. At the new equilibrium quantity the vertical distance between demand and supply curves will be exactly $1

B. At the new equilibrium quantity, the vertical distance between the demand and supply curves will be less than $1.

C. At the new equilibrium quantity, the vertical distance between the demand and supply curves will be greater than $1.

D. None of these.

At the new equilibrium quantity the vertical distance between demand and supply curves will be exactly $1

If an economist is interested in understanding how an increase in minimum wage affects welfare of workers they would compare:

A. Changes in the wage in the original equilibrium versus with the price control.

B. Change in total producer surplus of workers including those who are still employed and those who lose their job

C. Change in total consumer surplus of workers including those who are still employed and those who lose their job

D. The total number of unemployed workers before and after the policy change.

E. None of these.

Change in total producer surplus of workers including those who are still employed and those who lose their job

If you want to argue that creating a rent control will prevent people from finding apartments to rent, it will help your argument if:

A. Demand is relatively elastic

B. Supply is relatively elastic

C. Demand is relatively inelastic

D. Supply is relatively inelastic

E. None of these.

Supply is relatively elastic

If we are interested in studying tax incidence, we need to pay attention to:

A. The statutory burden of the tax: whether the tax is on buyers or on sellers

B. The relative elasticity of demand and supply, regardless of the statutory burden

C. Whether the tax is legal according to the Supreme Court.

D. Whether it is buyers or sellers who actually send money to the government.

E. None of these.

The relative elasticity of demand and supply, regardless of the statutory burden

Why might a production possibilities frontier be drawn as a straight line with a constant slope?

A. In order to indicate an increasing opportunity cost of obtaining more of one good in terms to the other

B. Because not all inputs are equally suited to production of both goods

C. In order to indicate that there is a constant opportunity cost of obtaining more of one good in terms of the other.

D. In order to indicate decreasing opportunity cost of obtaining more of one good in terms to the other

E. None of these.

In order to indicate that there is a constant opportunity cost of obtaining more of one good in terms of the other.

If California can produce 1,000 tons of raisins or 250 tons of green chiles, and New Mexico can produce 200 tons of raisins or 800 tons of green chiles, then:

A. California holds an absolute advantage in producing both goods

B. New Mexico holds an absolute advantage in producing both goods

C. California and New Mexico cannot gain from specialization and trade because they have the same opportunity costs

D. They can gain through trade if California specializes in chiles and New Mexico specializes in raisins

E. They can gain through trade if California specializes in raisins and New Mexico specializes in chiles

They can gain through trade if California specializes in raisins and New Mexico specializes in chiles

The production possibilities frontier model is used to demonstrate:

A. The maximal quantities of two goods that an economy can potentially produce

B. The maximal quantities of two goods that an economy can potentially consume without trade

C. The maximal quantities of two goods that an individual consumer can obtain

D. Both A and B are correct

E. None of these.

Both A and B are correct

Comparative advantage is defined as:

A. The condition where a trader is able to produce more efficiently than another trader

B. The condition where a trader is able to produce using fewer resources than another trader

C. The consideration where a trader is able to produce something at a lower opportunity cost than another trader

D. The situation where there are no idle or unused inputs in a production process for a particular trader

E. None of these.

The consideration where a trader is able to produce something at a lower opportunity cost than another trader

Consumer surplus represents

A. Economic value that accrues to sellers through market transactions

B. Economic value that accrues to buyers through market transactions

C. The total economic value created through market transactions.

D. The opportunity cost of market activity

Economic value that accrues to buyers through market transactions

Producer surplus represents

A. Economic value that accrues to sellers through market transactions

B. Economic value that accrues to buyers through market transactions

C. The total economic value created through market transactions

D. The opportunity cost of market activity

Economic value that accrues to sellers through market transactions

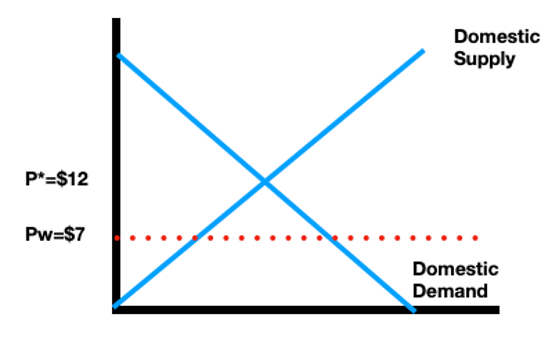

Consider the graph:

This is a situation where:

A. The domestic country can efficiently import this good

B. The domestic country can efficiently export this good

C. A tariff that adds $10 to the price at which consumers can purchase imports will reduce domestic producer surplus

D. A tariff that adds $3 to the price at which consumers can purchase imports will increase domestic consumer surplus

The domestic country can efficiently import this good

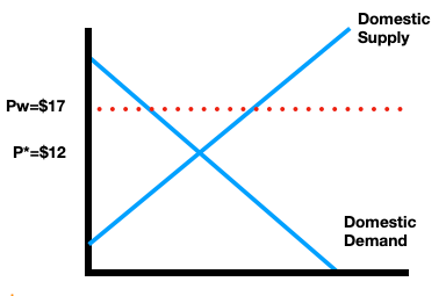

Consider the graph:

This is a situation where:

A. The domestic country can efficiently import this good

B. The domestic country can efficiently export this good

C. A tariff that adds $10 to the price at which consumers can purchase imports will reduce domestic producer surplus

D. A tariff that adds $3 to the price at which consumers can purchase imports will increase domestic consumer surplus

The domestic country can efficiently export this good

In class Ben gave the example of arriving at an empty Lake Michigan beach with no entrance fee only to discover the swarms of flies that were evidently keeping people away as these raised the costs to sitting on the beach (in a way that could be counted in $$$). We can best classify the beach under these circumstances as:

A. A common resource: consumption is rival due to congestion, but non-excludable because everyone can use the beach

B. A private good: consumption is rival due to congestion, and excludable in the sense that it’s limited to whoever will tolerate the flies

C. A club good: consumption is non-rival because the beach is empty, but excludable in the sense that it’s limited to whoever will tolerate the flies

D. A public good: consumption is non-rival because the beach is empty, but non-excludable because everyone can use the beach

A club good: consumption is non-rival because the beach is empty, but excludable in the sense that it’s limited to whoever will tolerate the flies

In class Ben gave the example of arriving at an empty Lake Michigan beach with no entrance fee only to discover the swarms of flies that were evidently keeping people away as these raised the costs to sitting on the beach (in a way that could be counted in $$$). Suppose all the flies leave as Ben arrives. (Hooray!) We can best classify the beach under these new circumstances as:

A. A common resource: consumption is rival due to congestion, but non-excludable because everyone can use the beach

B. A private good: consumption is rival due to congestion, and excludable in the sense that it’s limited to whoever will tolerate the flies

C. A club good: consumption is non-rival because the beach is empty, but excludable in the sense that it’s limited to whoever will tolerate the flies

D. A public good: consumption is non-rival because the beach is empty, but non-excludable because everyone can use the beach.

A public good: consumption is non-rival because the beach is empty, but non-excludable because everyone can use the beach.

Economists would most likely consider the Zach Bryan concert at Michigan Stadium (or the upcoming one at Memorial Stadium in Lincoln, NE) as:

A. A public good

B. A common resource

C. A club good

D. A private good

A club good

Economists would most likely consider a ticket corresponding to a single seat at the Zach Bryan concert at Michigan Stadium (or the upcoming one at Memorial Stadium in Lincoln, NE) as:

A. A public good

B. A common resource

C. A club good

D. A private good

A private good

Suppose the market equilibrium is $10 and then there’s a non-binding price ceiling at $12. Now circumstances change to that there’s an increase in demand coupled with a decrease in supply. Assume demand increases more than supply in creating the new equilibrium price which is now $13. What do we know is true about the resulting outcome in the market?

A. The market started out in equilibrium and after the change will have neither a shortage nor a surplus

B. The market started out with a shortage but now has a surplus

C. The market started out with a surplus but now has a shortage

D. The market started out in equilibrium but now has a shortage

E. The market started out in equilibrium but now has a surplus

The market started out in equilibrium but now has a shortage

The example of a flat user fee that drivers of electric vehicles pay once a year to the state differs from the other examples given an in-class regarding per-unit taxes in that the flat EV fee:

A. Is split evenly between buyers and sellers

B. Is borne by car dealers primarily

C. Is entirely non-distortionary because it’s a lump-sum tax

D. Is not a good revenue generator because EV drivers will drive less

E. None of these.

Is entirely non-distortionary because it’s a lump-sum tax

One reasonable way to evaluate the effectiveness of a minimum wage to benefit workers is to

A. Compare the gains to those who keep their jobs to the losses of those who lose their jobs

B. Compare the gains of those who keep their jobs to the losses of those who were not employed in the first place,

C. Compare the losses of those who lost their jobs to those who are to all of those who are unemployed

D. Consider the equilibrium number of jobs in both cases.

Compare the gains to those who keep their jobs to the losses of those who lose their jobs

The economic burden of a local tax on renting hotel rooms is likely to be born

A. Mostly by consumers of hotel rooms.

B. Mostly by the hotels themselves

C. Mostly by local residents

D. Evenly between consumers and sellers of hotel rooms.

Mostly by the hotels themselves

If the goal of the tax is to generate tax revenue, it should concern policy makers if

A. There is a large amount of dead weight loss

B. There is a small amount of dead weight loss

C. Demand and supply are equally inelastic

D. The good has very few substitutes

There is a large amount of dead weight loss

If the goal of the tax is to change behavior, it most creates the circumstances for success if

A. Demand is quite elastic

B. Demand is quite inelastic

C. There are very few substitutes for the good

D. Deadweight loss is very small

Demand is quite elastic

If there’s a tax on sellers, but demand is more inelastic than supply, we can say for sure.

A. Buyers end up, bearing a larger burden of the tax

B. Sellers end up bearing a larger burden of the tax.

C. The burden of the tax is going be born equally between the two.

D. Deadweight loss is minimized

Buyers end up, bearing a larger burden of the tax

In the case of economic growth, previously efficient bundles

A. Become feasible, but inefficient

B. Become inefficient, but infeasible,

C. Become efficient and feasible

D. Become unattainable except through trade

Become feasible, but inefficient

The economic problem that arises in the presence of a positive externality

A. Is one of underproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external benefits.

B. Is one of overproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external benefits.

C. Is one of underproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external costs.

D. Is one of overproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external costs.

Is one of underproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external benefits.

The economic problem that arises in the presence of a negative externality

A. Is one of underproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external benefits.

B. Is one of overproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external benefits.

C. Is one of underproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external costs.

D. Is one of overproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external costs.

Is one of overproduction: Decision-makers pay attention only to their private benefit compared to their private costs and ignore the additional external costs.

A natural monopoly exists when

a. the good produced by a monopoly is classified as a natural product.

b. the monopoly-level of market power develops naturally due to the company’s high product quality.

c. producing a large output has significantly lower marginal cost than producing a small output.

d. exploitative business tactics are used to force other companies out of the market illegally.

producing a large output has significantly lower marginal cost than producing a small output.

The degree to which a market provides socially optimal outcomes depends on the degree to which it

a. engages in research to develop products to meet needs of customers.

b. differentiates products to satisfy different consumer preferences.

c. focuses on low prices rather than high output.

d. is closer to the competition outcome than market power outcomes.

is closer to the competition outcome than market power outcomes.

When free entry and free exit exist in a market, then in the long run, a seller’s demand curve will:

a. barely touch its average cost curve.

b. be below its average cost curve.

c. be above its average cost curve.

d. cross its average cost curve.

barely touch its average cost curve.

One negative aspect of product differentiation is that it:

a. reduces market demand.

b. makes demand more elastic.

c. reduces consumer choice.

d. adds to costs.

adds to costs

According to the Five Forces framework, which of the following would MOST likely increase competitive pressure in a market?

a. High barriers to entry

b. Few competitors

c. Many firms selling identical goods

d. Strong brand loyalty

Many firms selling identical goods

A company fears that new startups may enter its industry and reduce its profits. This concern relates to which force in the Five Forces framework?

a. Buyer bargaining power

b. Threat of substitutes

c. Threat of new entrants

d. Supplier bargaining power

Threat of new entrants

Which of the following situations BEST illustrates the threat of substitutes?

a. Two gas stations competing on price

b. A new firm entering the same industry

c. A supplier raising input prices

d. Consumers switching from taxis to ride-sharing apps

Consumers switching from taxis to ride-sharing apps

If a firm positions its product very close to its rival’s product, what is the most likely outcome?

a. Increased price competition

b. Higher profit margins

c. Reduced competition

d. Greater product differentiation

Increased price competition

A firm decides to locate its product far from its rival in product space (e.g., very different features). What is the primary benefit of this strategy?

a. Lower production costs

b. Reduced price competition and higher margins

c. Increased number of competitors

d. Greater supply of inputs

Reduced price competition and higher margins

Advertising that increases brand loyalty and makes consumers less sensitive to price will result in:

a. A flatter demand curve

b. A more inelastic (steeper) demand curve

c. A perfectly elastic demand curve

d. A decrease in demand

A more inelastic (steeper) demand curve

Suppose four firms compete in a market and each serves a fraction of the total number of consumers. This best describes:

a. Oligopoly

b. Monopoly

c. Monopolistic Competition

d. Perfect Competition

Oligopoly

Consider a firm that faces demand given by P = 20 – Q, find the profit maximizing price and quantity if this firm has zero marginal costs.

a. P = 20, Q = 0

b. P = 0, Q = 20

c. P = 15, Q = 15

d. P = 10, Q = 10

e. None of these

P = 10, Q = 10

Two neighboring gas stations compete selling at $3.95 per gallon. Another gas station up the road but across a busy intersection wants to determine its pricing policy. This gas station should optimally set:

a. Price = $3.95

b. Price = $3.95 plus whatever seems to be the premium consumers are willing to pay to avoid crossing the intersection to visit a rival gas station

c. Monopoly price based on finding where MR=MC to determine the quantity, then estimating the profit maximizing price based on the firm’s demand curve

d. Marginal cost + discount effect divided by output effect

Price = $3.95 plus whatever seems to be the premium consumers are willing to pay to avoid crossing the intersection to visit a rival gas station

If P = 30 – Q is the monopoly demand curve, what is the marginal revenue curve?

a. MR = 0

b. MR = 30 – Q

c. MR = 15 – Q

d. MR = 15 – (1/2)Q

e. MR = 30 – 2Q

MR = 30 – 2Q

Consider a pretzel cart business where there’s a fixed cost of renting the pretzel cart equal to $1000. The variable cost of selling each pretzel is $1 per pretzel. If the firm sells 10,000 pretzels we know:

a. FC = $1000, VC = $3, TC = $1003, ATC = $1000/3

b. FC = $1000, VC = $10,000, Average Total Cost is $1.10

c. Average fixed cost is $1

d. Average total cost is $2

e. None of these are correct.

FC = $1000, VC = $10,000, Average Total Cost is $1.10

If we conduct a Porter’s Five Forces analysis of Love’s Travel Center, we are most likely conclude that the threat from Tesla building out SuperCharger stations are:

a. Industry rivalry

b. Buyer bargaining power

c. Supplier bargaining power

d. Threat of entrants

e. Threat from substitutes

Threat from substitutes

If the firm is currently producing at a point where MR > 0, we know

a. The firm is operating at the midpoint of its demand curve

b. The firm is operating at a point where demand is inelastic

c. The firm is operating at a point where demand is elastic

d. The firm is unprofitable.

The firm is operating at a point where demand is elastic

If a firm has marginal costs of $1 and operates in a market producing where the market price is $5 and the market quantity is 4, total profits are:

a. Incalculable

b. $16

c. $4

d. $5

e. $20

$16

What type of barrier to entry is best exemplified by a local Bed & Breakfast that lobbies the town council to ban short-term rental units such as AirBnB?

a. Demand side strategy

b. Supply Side Strategy

c. Regulatory strategy

d. Entry deterrence strategy

Regulatory strategy

When firms enter a market, we model the impact on the profitability of any individual firm by

a. Assuming a leftward shift of the supply curve

b. Assuming a leftward shift of the firm’s individual demand curve

c. Assuming a rightward shift of the firm’s individual demand curve

d. Assuming demand becomes perfectly inelastic

e. Assuming supply becomes perfectly inelastic

Assuming a leftward shift of the firm’s individual demand curve