Industrial Topic 5 + CS

1/32

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

33 Terms

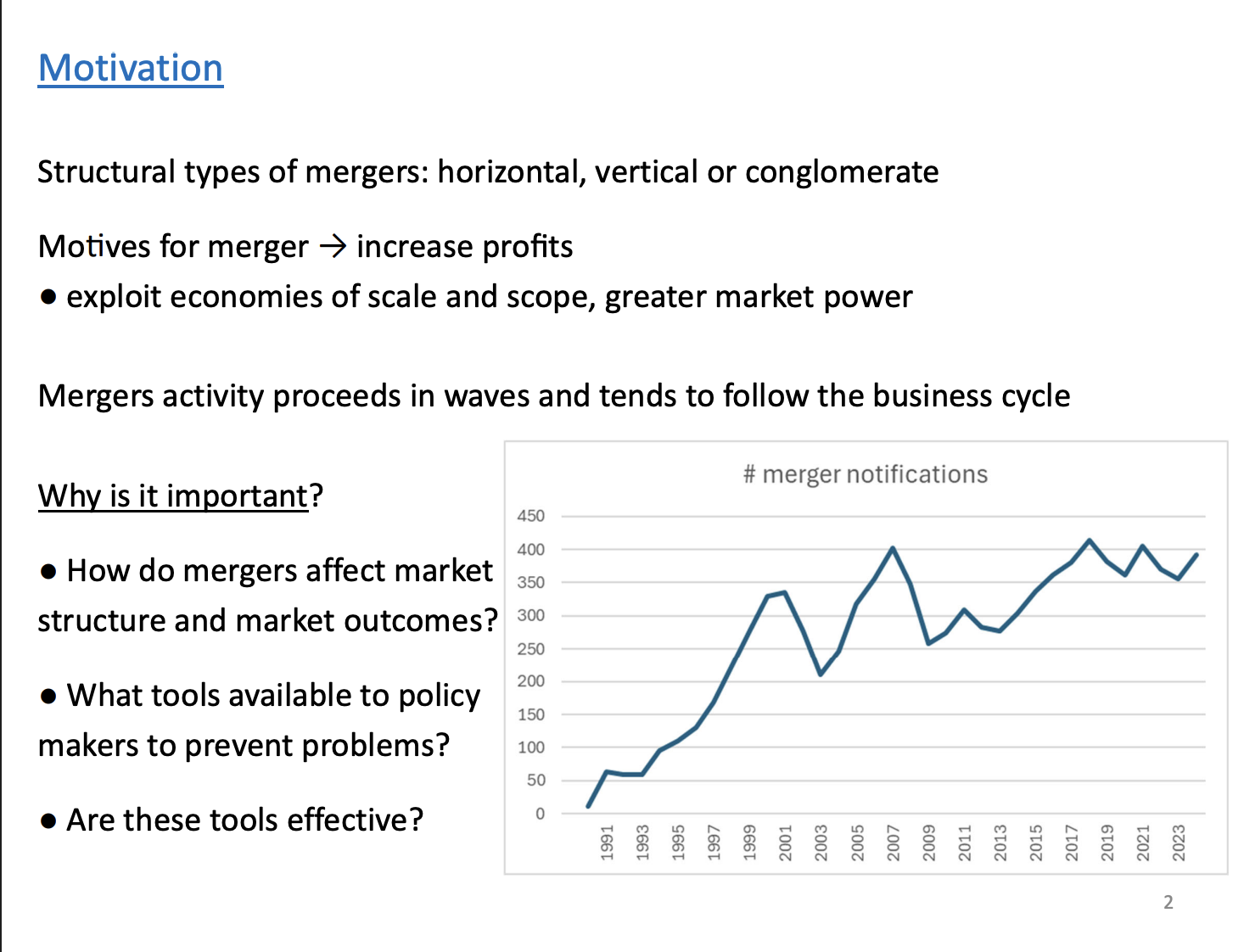

What are the types of mergers, what are the motives, why are they important to follow

Horizontal - same stage of the production process, example Asda and Sainsbury, both operate in the retail sector - would be competitors

Vertical merger, different stages of the production process, example Sainsbury and a cheese producer. Manufacturing stage to retail stage of the production process

Conglomerate - firms offer complementary products and combine together not competitors, example of this Sainsbury and Argos. Not considered competitors, grocery section vs mix retailors. Producing various products They complement each other, Argos had a good online presence. Allowed Sainsbury to sell online

Motivations - look to merger to increase profits. One is through economic of scale, lowering average costs and raising profits. Another way, increase concentration in the market, provides the merger entity with higher market power and increase profits.

Merger activity, follows the business cycle. Was no merger control at the European level before 1990. Increased up to the dot com bubble, then the financial crisis. Then austerity for a period in the teens. Covid from 2020. Mergers tends to happen when the economy is doing well. Effect of covid was much smaller than the financial crisis, during covid times we might've thought that during downturns of the economy firms should merger less, but that didn’t really sort of tend to happen, firms didn’t have much choice, merge or go out of business.

Important to study mergers:

Effect market structure, impact market outcomes. Good and bad effects, the good side, if firms are more efficient, lower costs and lower prices. On the other hand, if we reduce the number of firm in a market, market shares increase, market power and higher price for consumers

Policy makers need to decide which mergers will produce good effects and bad effects, if bad they need to intervene and prevent it from occurring.

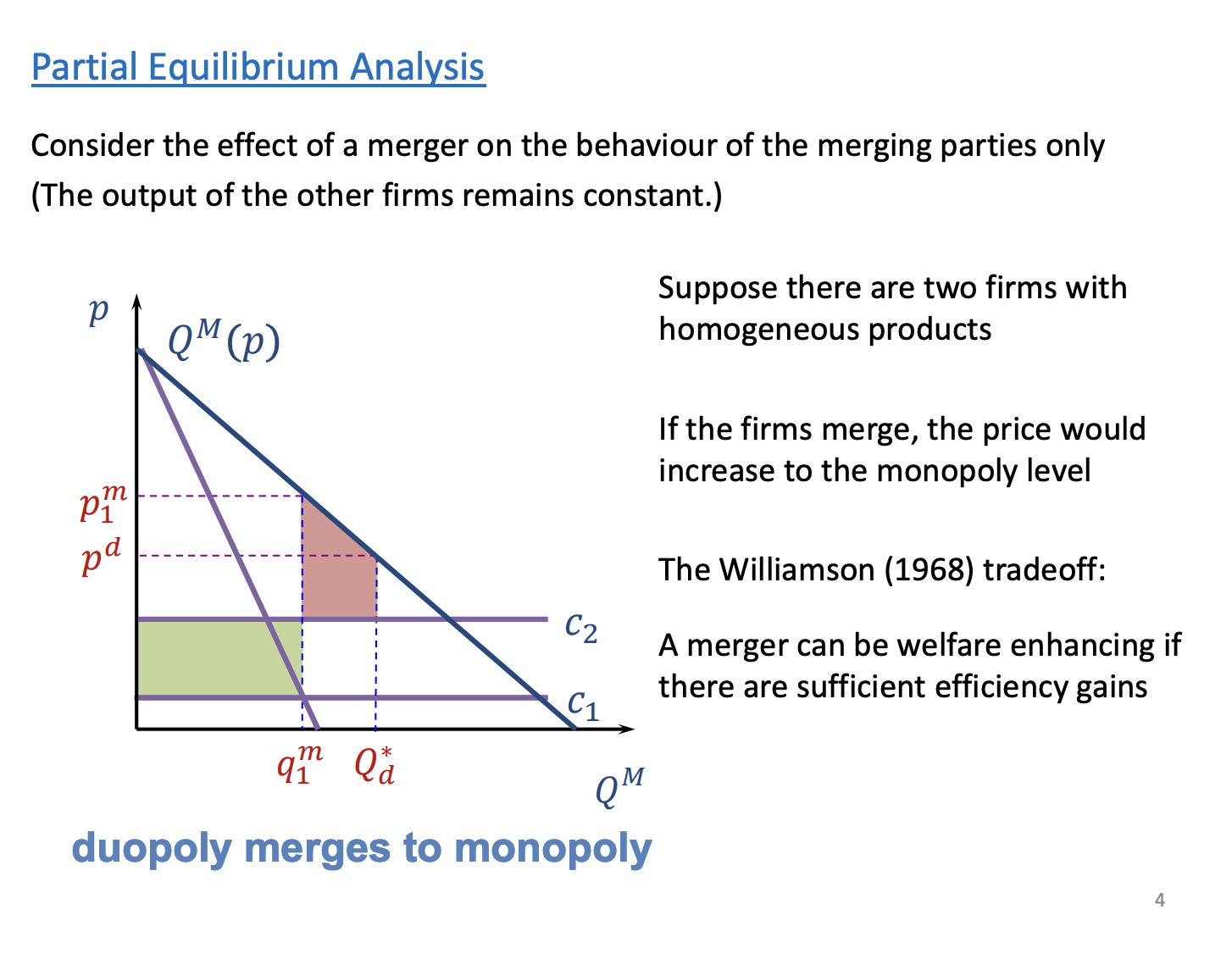

What is the effect of merger behaviour of the merging parties only, draw diagram and what did williamson say about merger and what tyope of wlefare do cma focus on

Basic effects of a merger

Reduce the number of firms in the market, higher concentration, could lead to incentive to prices rises

Reduce the firms costs, provide incentive to lower prices

Trade off between these two effects, firm analysis by Williamson back in 1968

Suppose two firms with homogeneous products and merger to create a monopoly. Simple case to isolate the effects of the insiders of the mergers, no outside effects/responses - other firms in the market. Pd and Qd is the duopoly market structure (pre merger), not a Bertrand's model here as p should equal mc.

Price move from Pd to Pm, and quantity falls. If the reduction in marginal costs is large, there can be welfare gains. Red box is a loss of CS and profits as the price goes up and the quantity falls as less is demanded at higher prices. The green box is the gain in profits from higher prices and lower costs.

If green > red, total welfare will be increase as a result of a merger. Can be welfare enhancing.

Competition agency don’t focus on total welfare, they focus on consumer surplus. In the case above, as price goes up, CS fall, the competition agency would be concerned by this merger. Reason for more focus on CS than total welfare, easier to understand through prices as al they need to find I merger which would increase prices. If they concerned about total welfare they would have to look into more depth, as in the example above prices rise but total welfare also rises so it adds another element of complexity. Just focusing on prices is much easier. Just CS, because consumer are often small, where as the firms are normally huge MNC, look to protect the smaller less powerful consumers.

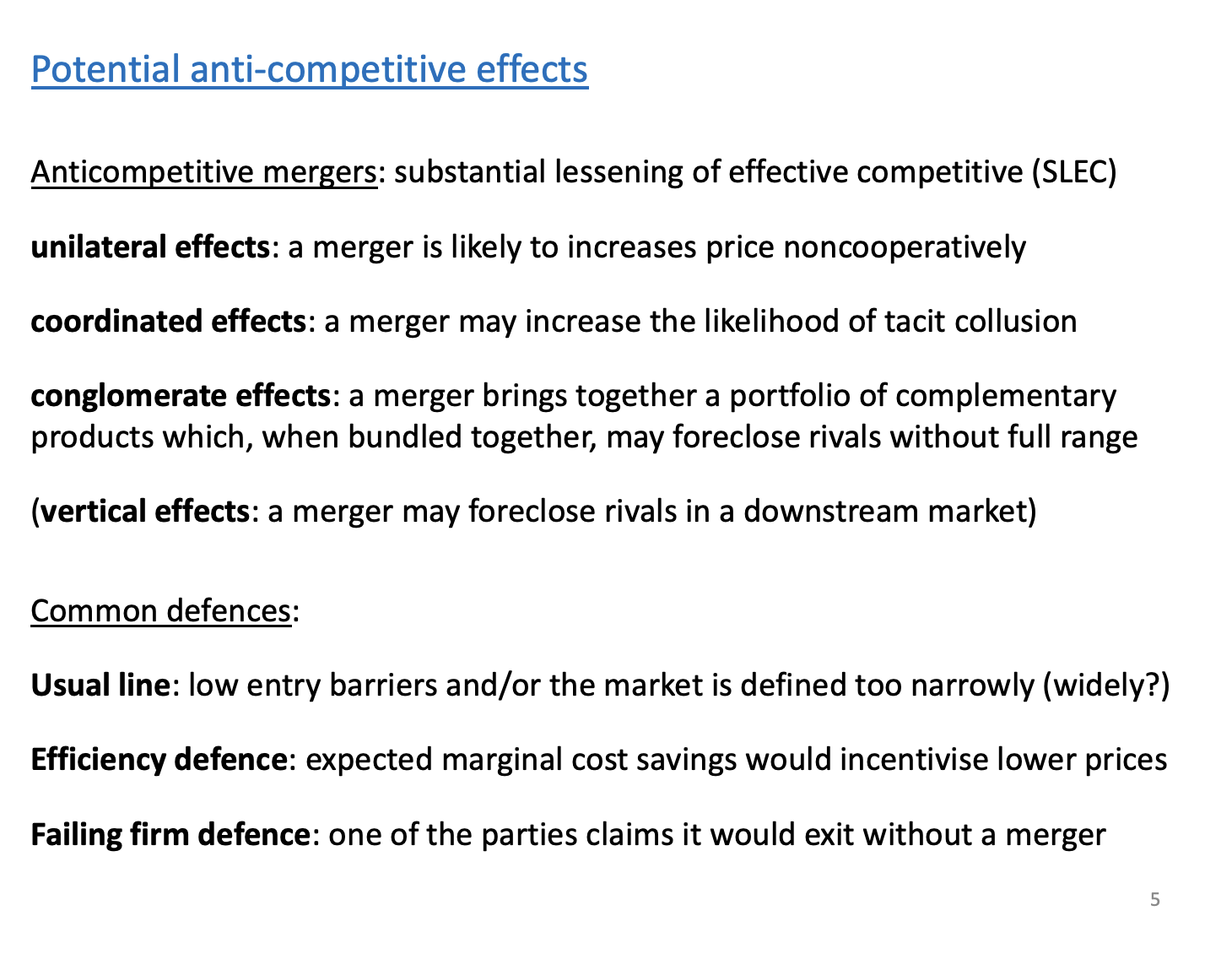

What are the potential anti competitive effects (3) and the common defences (3)

Other effects.

Anti competitive effects of mergers, in terms of laws, substantial lessening of competitive (in the European level). Anti competitive effects fall into the four cases.

Unilateral - firms have unilateral incentive to increase prices post merger, duopoly to monopoly.

Coordination effects - increases the likelihood of collusion post merger, can occur as collusion is more likely to occur when symmetric and lower no. of firms in the market. From 3 firms 20 30 50 to 2 firms 50 50. Market structure more symmetric and less firms, increases the likelihood.

Conglomerate - complementary products join together, provide the merged entity with a large product range to bundle together to such a large extent to exclude rivals from the market.

Vertical effects - next week

Common defences against competition agency

Low barriers - other firms will enter the market and reduce market shares. Market is defined too narrowly, that’s sort of increasing the firms markets share and overstating the dominance it has.

Efficiency - create efficiencies so large that even if they have market power the prices will go down, can occur in the Williamson example if MC fall by a huge proportion.

Falling firm - will lead to market power, but the firm we are merging with will go out of business and we will get the power anyways. Will gain some efficiencies.

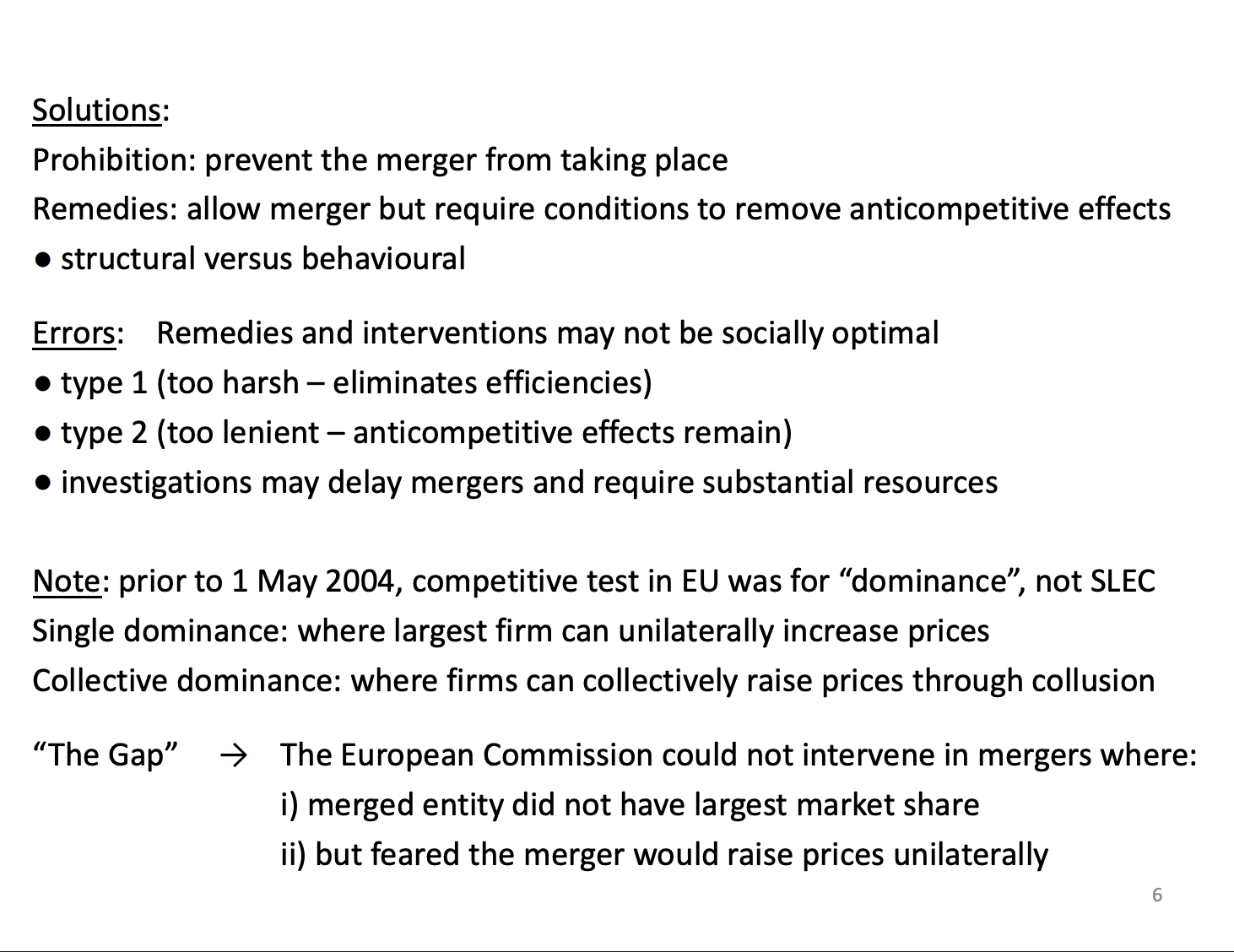

What are the solutions (2) and what errors can arise (2) and what issue did the EU have with merger prior to 2004

Prohibition - Stop merging from happening at all, Asda x Sainsbury merger is an example. Very blunt as most mergers are multi markets and could be gains in other markets which are stopped. More elegant solution is remedies.

Remedies - allowing mergers to go through under some conditions, like sell of assets in problematic markets. Allowing the merger to go through will prevent the problems and allow efficiencies to occur.

Remedies can have errors as well. Type 1 and Type 2.

Been a change in how we look at mergers, change happened in 2004, afterwards we follow the US approach which we looked for unilateral effects and coordinated effects. Pre 2004 had similar concepts which caused problems.

We had Single dominance in place for unilateral effects and collective dominance which is similar to coordinated effects. Had this problem where single dominance only allowed competition agency to intervene if it was the largest entity in the market was merging, other entities the agency couldn't intervene.

Unilateral effects doesn’t have these restrictions, wider and less restrictive. If they are the second largest entity, they can still intervene.

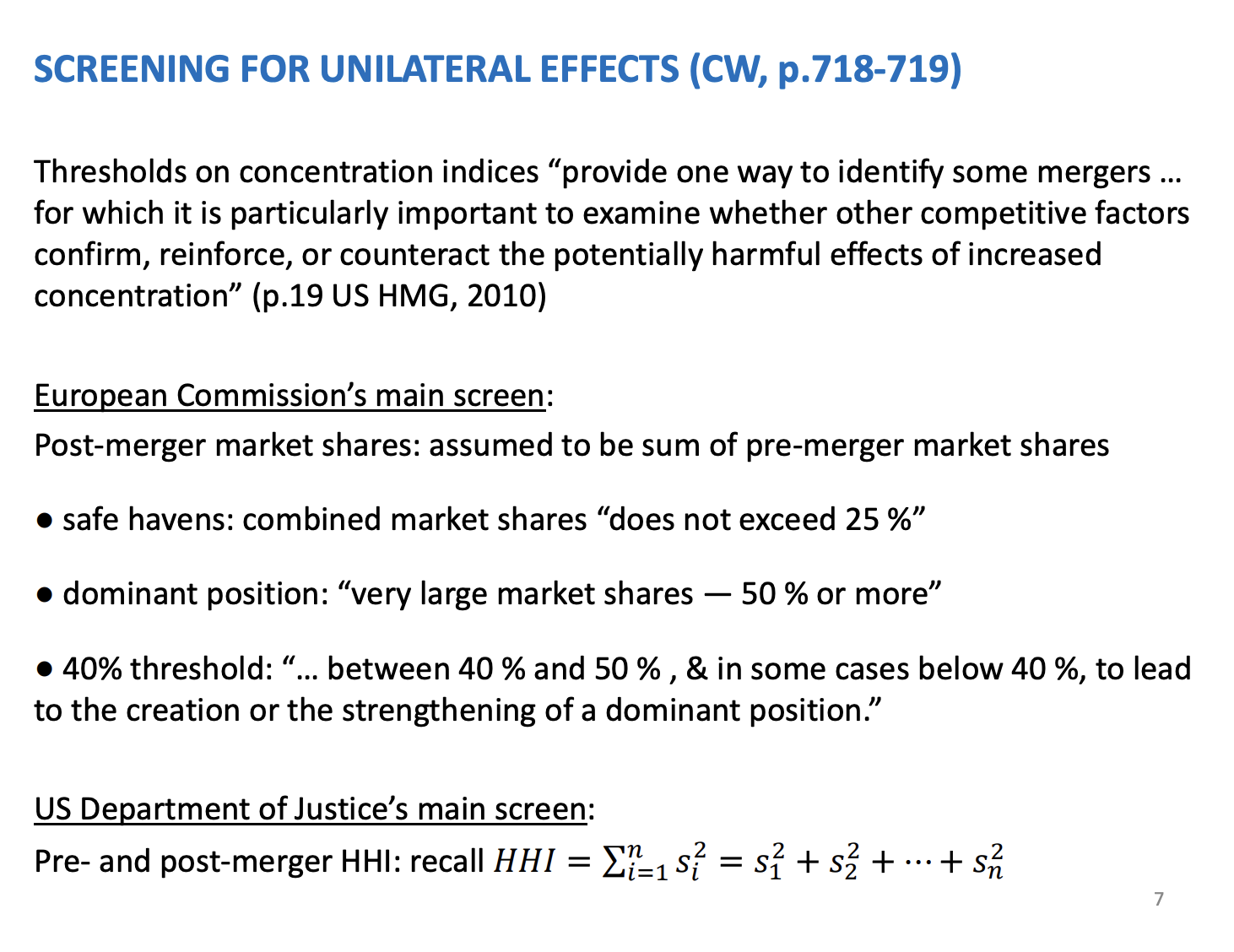

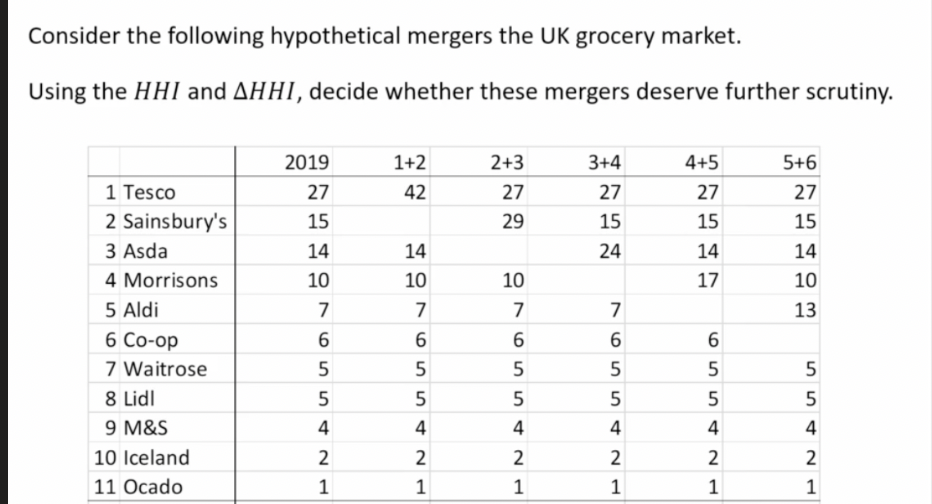

Screening for unilateral effects, EU (3) and US (1)

Simple techniques used to assess mergers.

Worek under strict time constraint, when deciding to allow a merger or not. Two phrase bargaining process. Competitive agency has 6 week after being noticed about the merger to decide if they are happy or not. If not, the firm has a chance to offer remedies. If that doesn’t work they can go through to a 6 month period to resolve issues which is called phrase 2. At the end of this phrase two it will either go through or be prevented.

In this time constraint, the agency need to allocate its resource very effectively to parts which need more understanding. Spilt into three sections of a multi market merger.

Markets which are fine

Markets which are bad and need to intervene

Market we need to invest our time in to see if they are good or bad

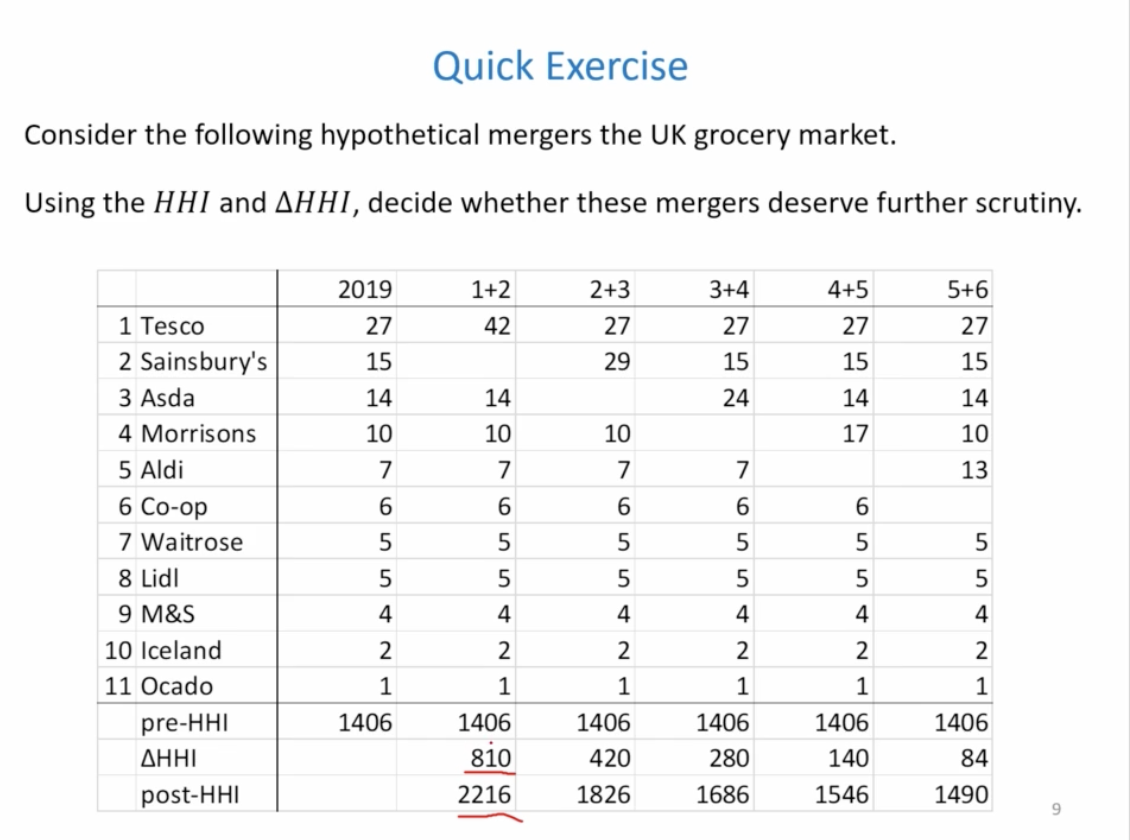

Simple technique to decide where they fall. Use concentration indices.

EU

Use market shares to understand when a merger is likely to be problematic.

Take market share pre merger, then add them together and assume this is the market share of the merged firm, if combined and less than 25 its fine. If >50, very concerned. 40 - 50% is the grey area, will be allocating the most resources to as it is the grey area to see whether it is good or bad.

US

HHI is used. Sum of market shares squared. They calculate the HHI, pre and post mergers. Simple trick

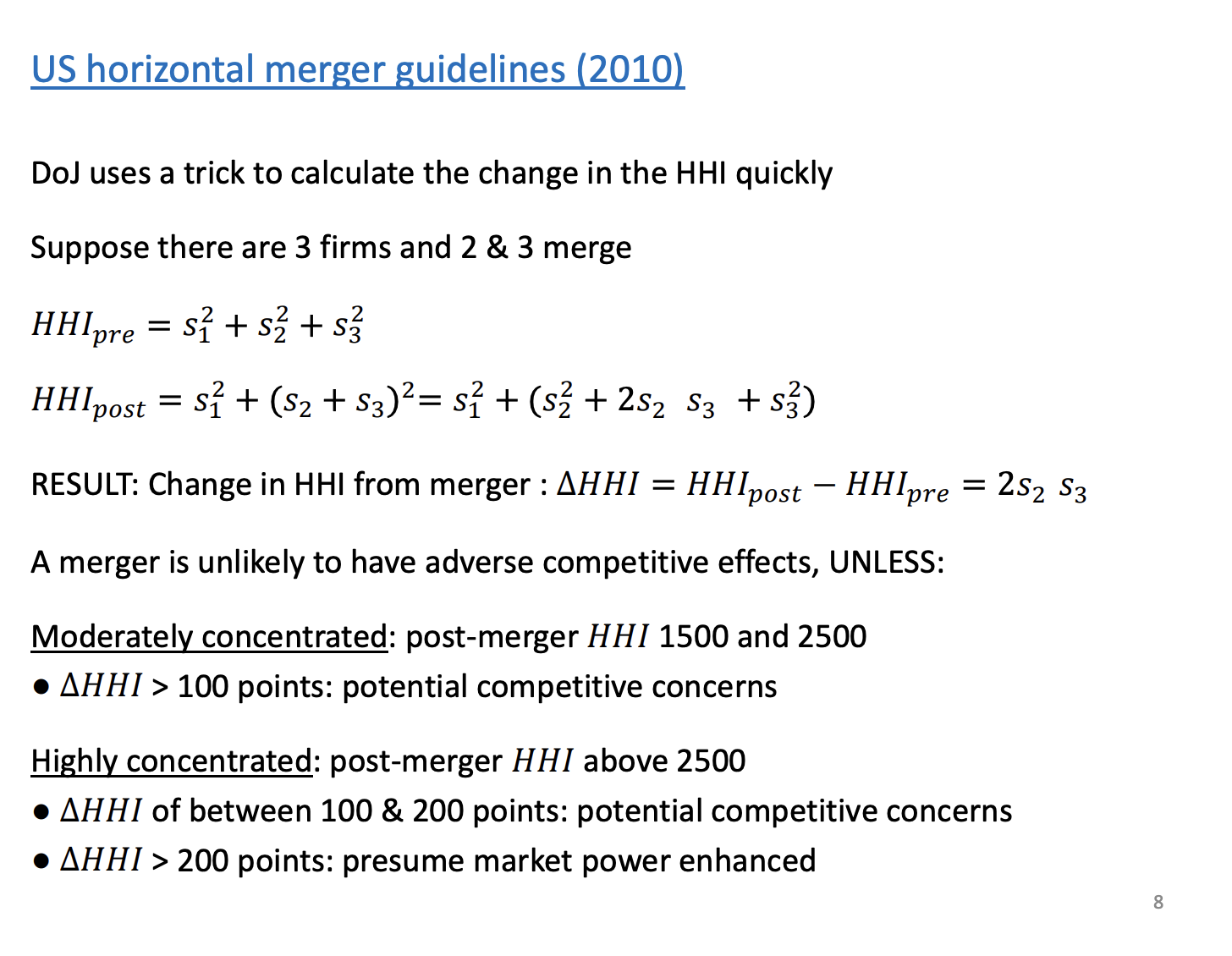

What are the US horizontal merger guidelines

Second and third largest firm combine. Sum of the pre merger shares. The post HHI is the expanded bracket + the biggest firm

The change leaves just the middle of the expanded bracket. CA can calculate how much the HHI is going to change pre and post merger.

Guidelines for the CA

If above 2500 and the change is >200, in the US they presume it is going to be bad

If above 2500 but only a change between 100 and 200, the grey area. If even lower, the CA won't get involved at all.

HHI between 1500 and 2500, and the change is > 100, grey area again.

ANswer

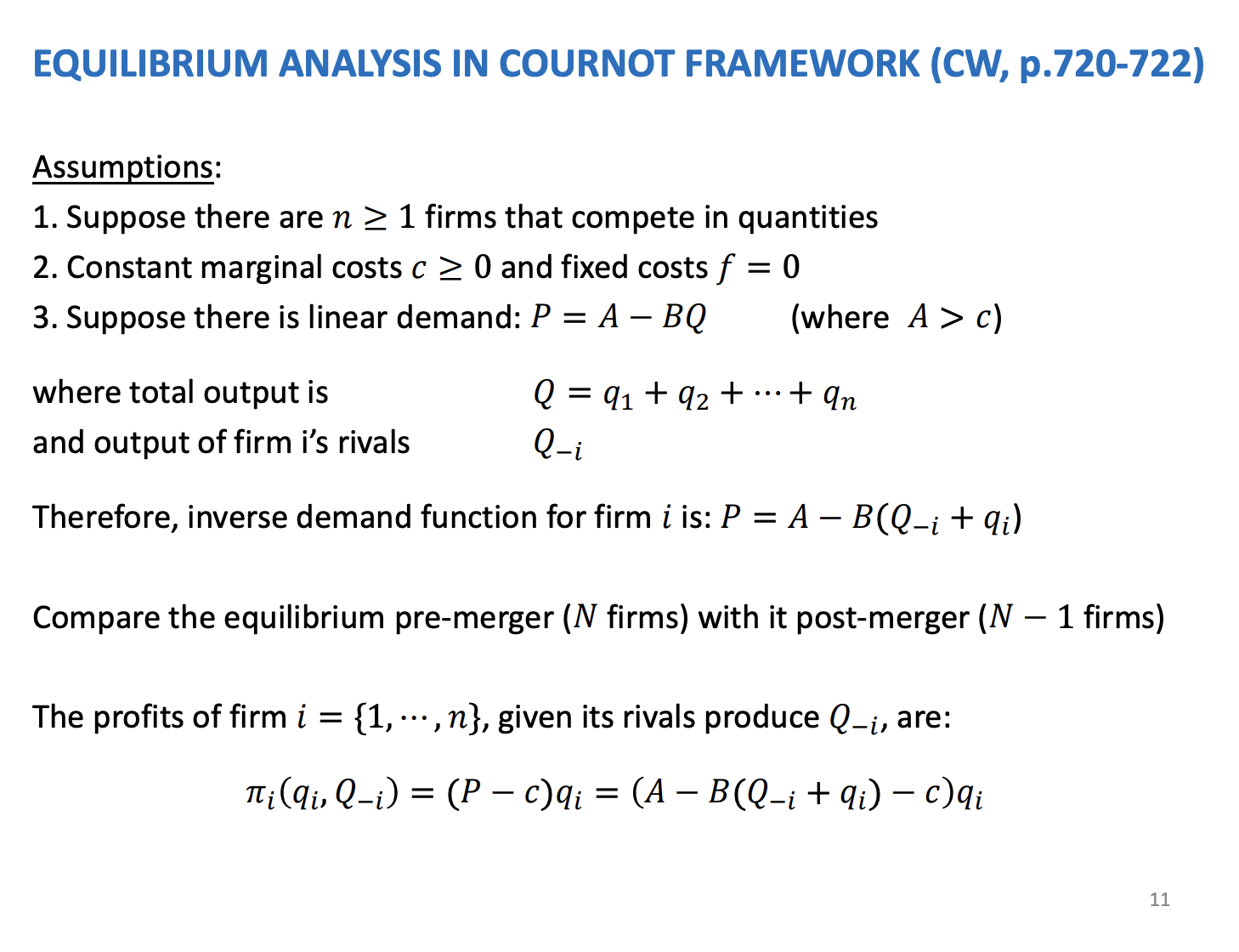

What are the assumptions of equilibrium analysis in the cournot framework? (3) and what is the demand function and the profit function

Equilibrium model which looks at the effects of mergers. Need to look at the strategic interactions of firms outside of the merger. Williamson only looked at insiders as it was only two firms and both combined.

Model first introduced by Farrow and Sharpio back in 1990. First attempt to model mergers through game theory, known as the merger paradox. In the equilibrium the insiders profits reduce as a result of the merger, it’s a paradox as we think they merger to increase profits but in the model the profits fall.

Suppose there is n firms and compete on Q. Allow marginal costs is C and set to 0 and no fixed costs. Assume demand is linear and the inverse demand function is price equal to A - BQ. A is the choke price, if above parameter A nothing is demand, below the price, there is going to be positive demand. Q is total amount being supplied to the market by all firms, sum of all of the firms outputs. B is slope of the demand curve.

Capital Q is the sum of all firms in the market. Sum of the firms rivals outputs is denoted as Q -I and we can sub into the inverse demand function to simply

Continued

Compare equilibrium pre and post by n-1, as there is one less firm in the market. Solve for the Nash equilibrium

Take the firms profit functions, and then maximise them to find the firms best response functions and then from the BR functions we're going to find the Nash equilibriums quantities and the various welfare pre and post merger scenarios.

ANswer

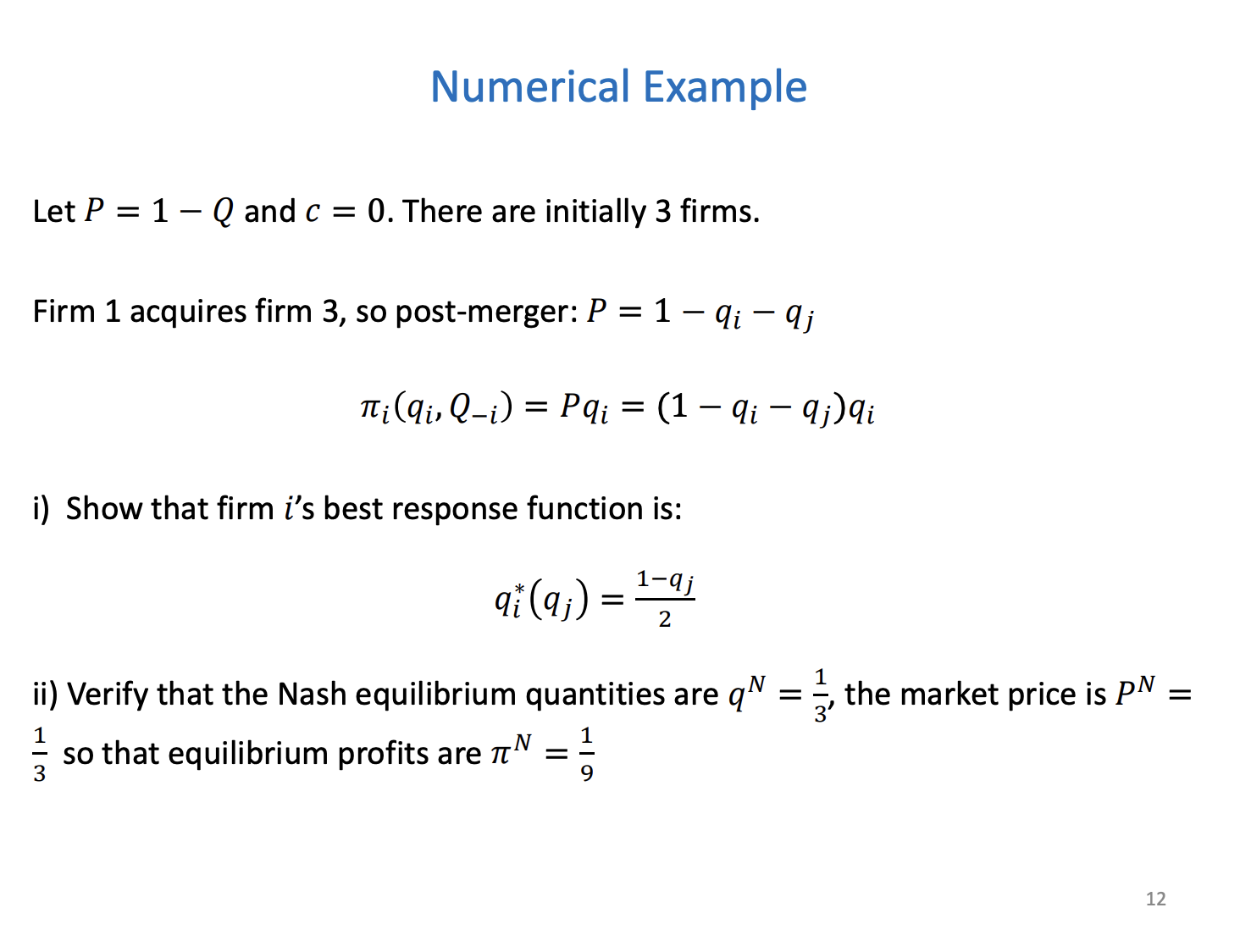

Add numerical example in

Merger leads to a reduction in Q, Prices go up, a unilateral effects . Concentration increases and no efficiency gains as MC = 0.

Profits go up from 1/16 to 1/9, the outside firm 2 its profits are going up as a result of the merger. To work out the profits of firm 1 and firm 3, post merger they get 1/9, pre merger would get 1/8. So this shows us the merger paradox. As a result of the merger, the profits have gone down from merging.

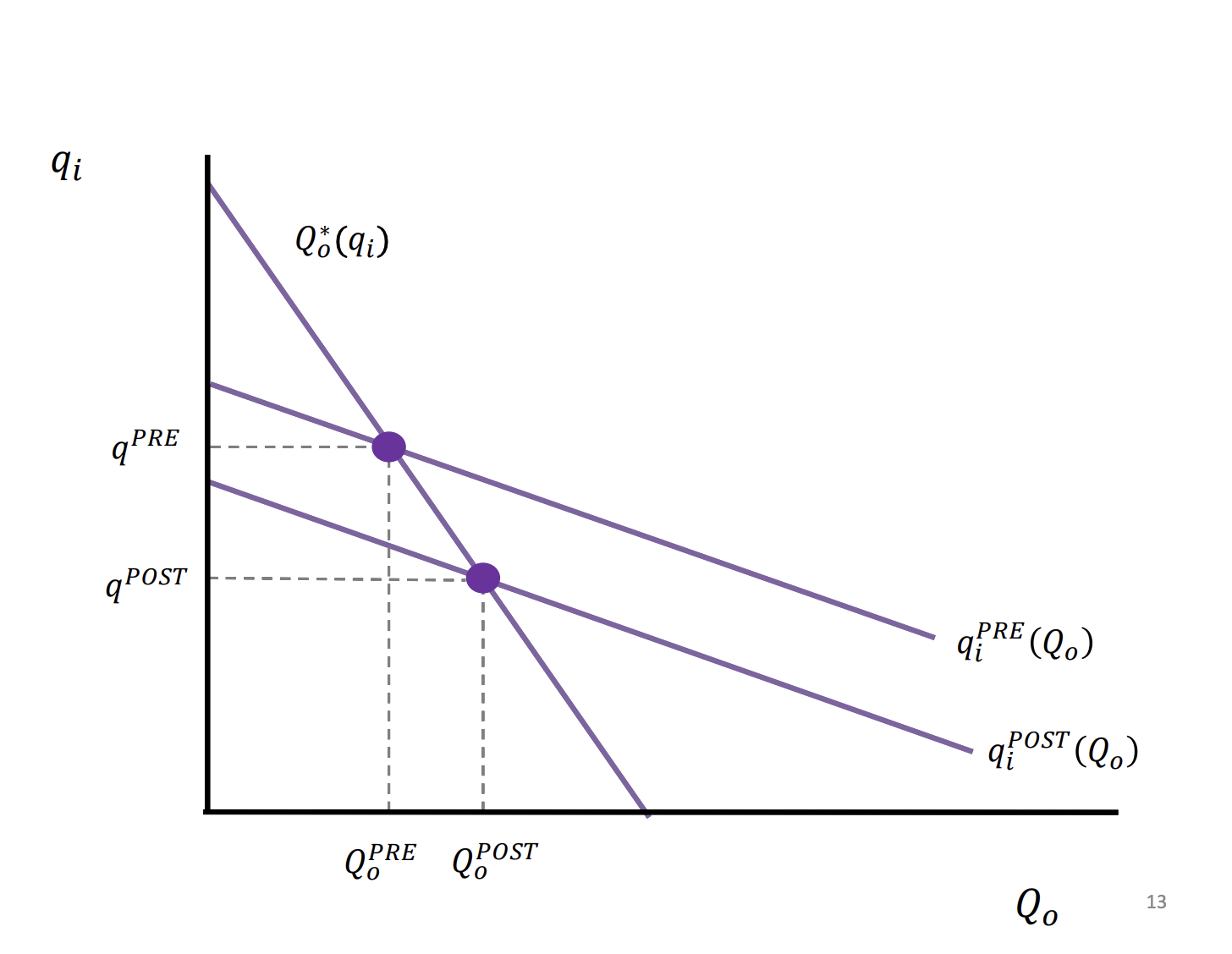

What are the BR function diagram look like

Qi represents the quantity of the insiders, x axis is the quantity of the outsiders.

Insiders firm 1 and 3 and outsides firm 2. Q*0 (qi) is the outsides best response function. Any output of the insiders, shows the outputs of the outsiders that would maximise the outsiders firms profit. Qipre(Q0) - sum of the insiders best response function pre merger, collectively would produce q given the output of the outsider.

Nash equilibrium post merger, is the purple intercept of post and the outsider BR curve

The merging firms are gaining market share and exploiting the market power by reducing how much they produce and increase the prices, higher profits. The merger paradox is caused by the outsider responding by producing more. So they produce more, the prices aren't going up as much as the insiders want and this causes the merger paradox

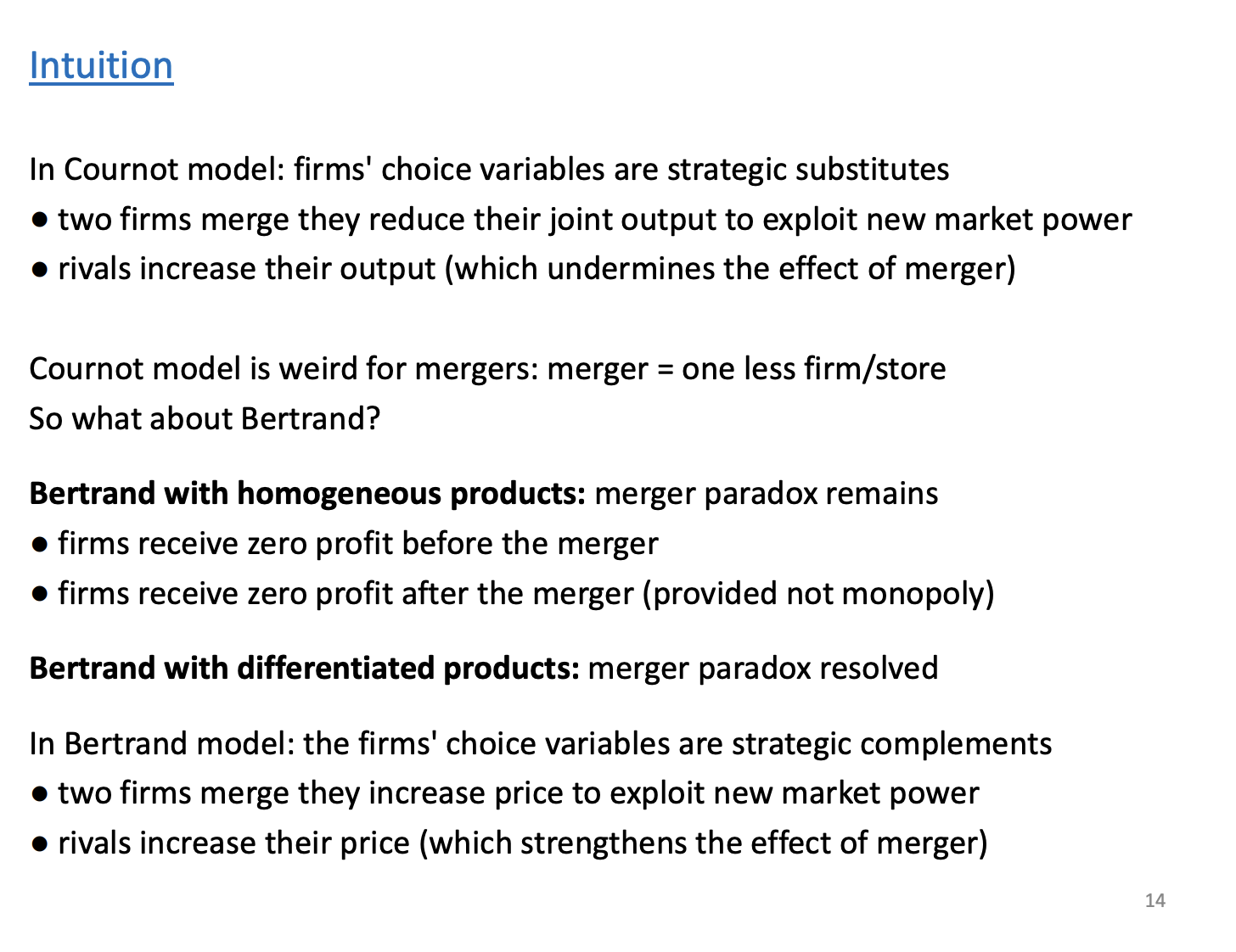

Intutition of the Cournot model (2), Bertrand model and then with differentiated products

It is inconsistent with reality, so its telling us the insiders profits will go down. As economistic we tend to think that firms should be maximising profits so according to this theory firms shouldn't merge.

Problem with assumptions in the model

The way be have modelled the merger, modelled by a reduced in firms. In reality if you acquire a firm you will receive its assets, stores or production process. Effect the market structure and effect the outcome in the market. Here we have been modelling the merger by assuming firm one acquires firm 3 its takes the competitor out. We are comparing a symmetric situation pre and post merger and this is counter to our example before when summing the market share together

More contemporary models of mergers actually model the assets that change hands within there mergers and since the assets change hands that can lead to a different sort of competitive environment post merger and that change the outcomes. Modelling more generally this will over come the merger paradox.

Also the paradox only occurs in the Cournot framework, because the competitors response by doing what the insiders don’t want, if it was a Bertrand's framework what happens here outsider response by how the insiders want them to, what happens is when you're looking at mergers in a differentiated setting, the insiders will respond to their market power by raising their price and outside response by also raising their price. Add to the profits the insiders get

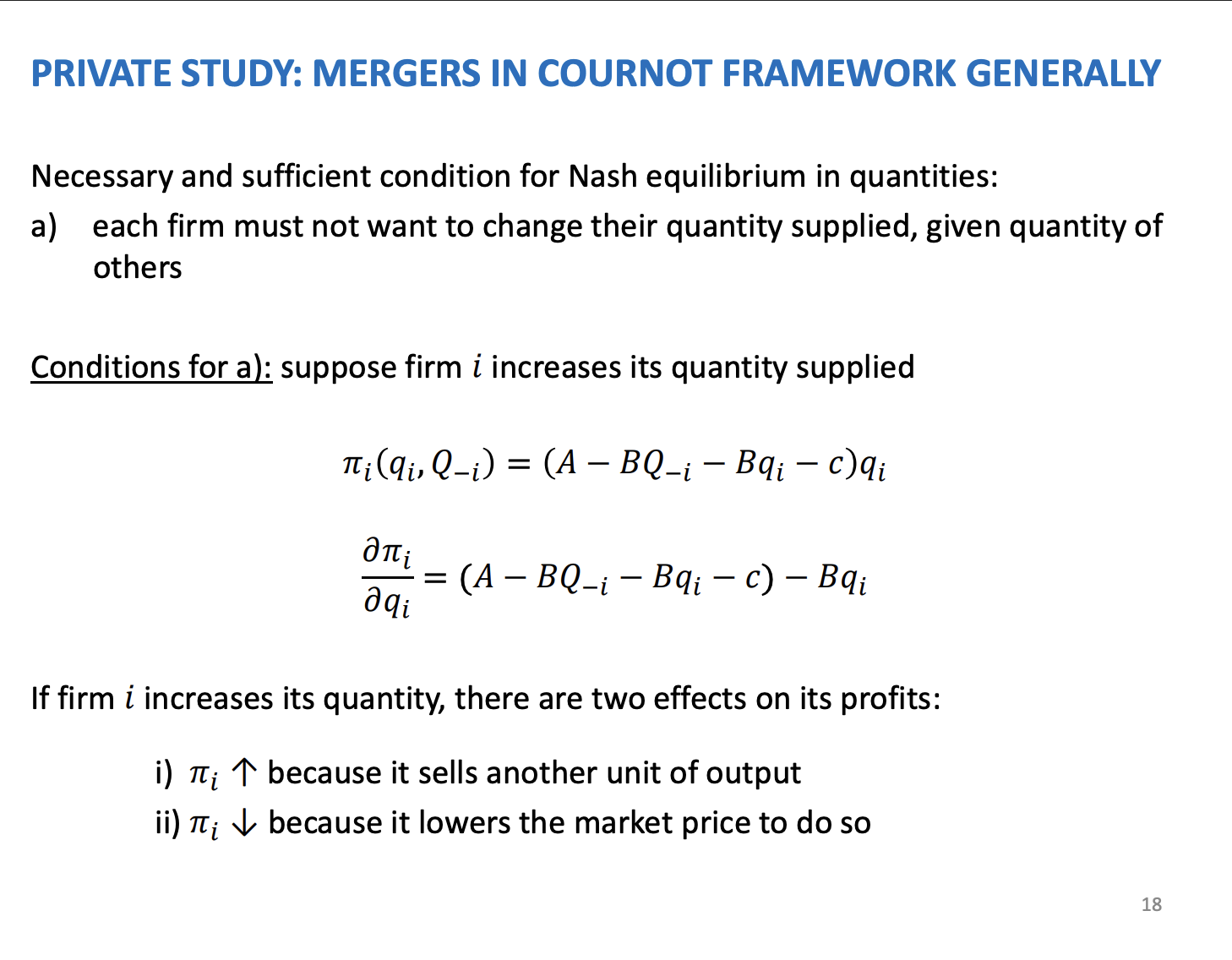

Mergers in the cournot framework, what is the necessary condition for the nash equilibrium to hold, what is the profit function and the diffential of it and what is the two effects

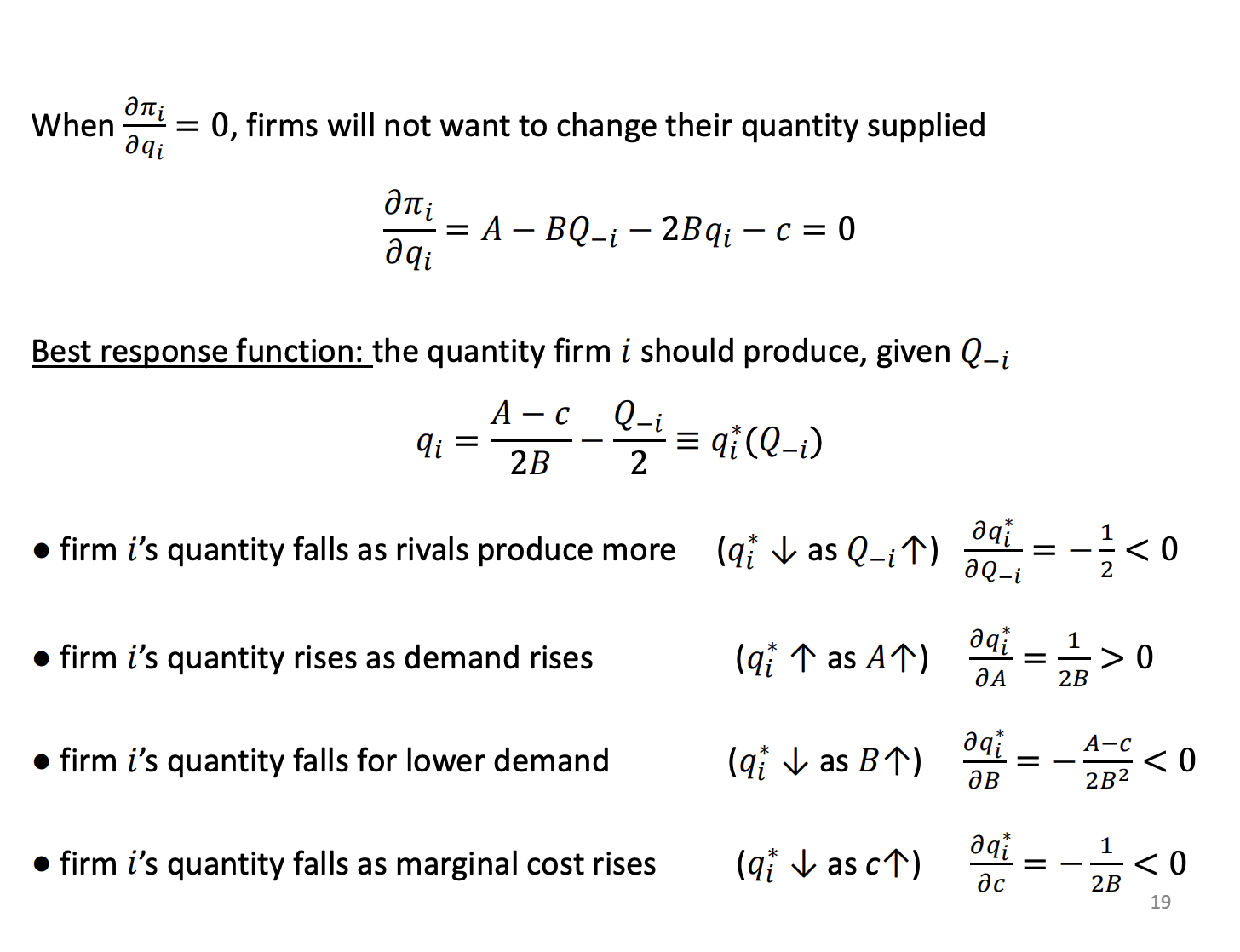

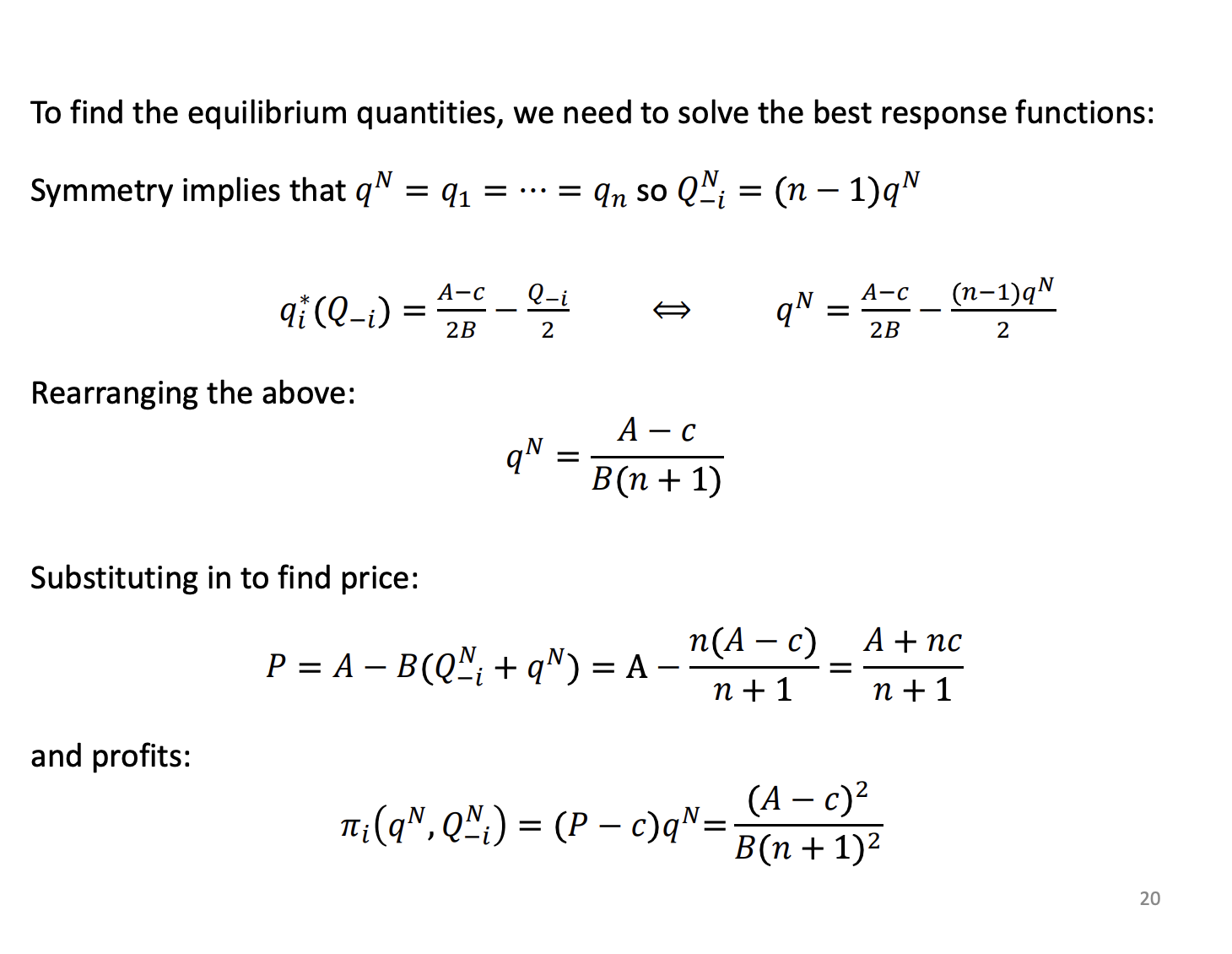

What is the best reponse function in the cournot model, and what does it mean (4)

The Concept: This slide solves the balancing act from Slide 18 to create a "Best response function." This is essentially a cheat sheet formula that tells a firm exactly how much to produce based on what its rivals are doing.

The Rules of the Game: The math proves three logical rules for how a firm should behave:

If rival firms start producing more, our firm should back off and produce less (to avoid crashing the price).

If overall market demand goes up, our firm should produce more.

If manufacturing costs go up, our firm should produce less.

How do you solve the best response functions, to find the rivals output

Now we assume all firms in the market are identical ("Symmetry") and are all using that same "Best response" cheat sheet.

The Math: By mashing all their individual equations together, we find the "Nash Equilibrium"—the final resting state where no firm wants to change what they are doing. The slide provides the final formulas for individual output ($q^N$), the market price ($P$), and individual profit ($\pi_i$) in this perfectly balanced market. This is our "Pre-Merger" baseline.

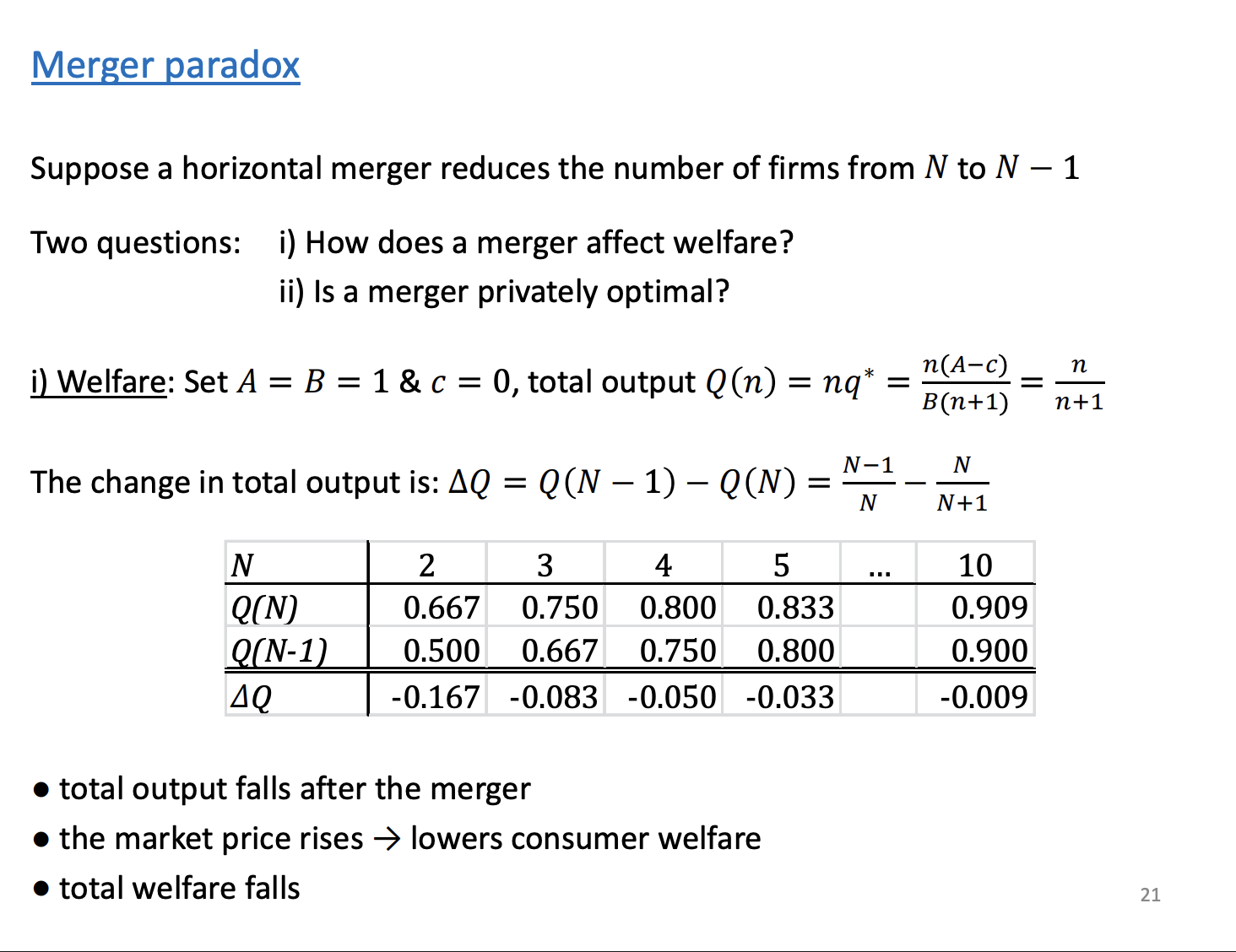

What is the merger paradox, what two questions are initially asked and what are the three effects

The Concept: The main event! We now imagine a market with $N$ firms, and two of them merge, reducing the total number of competitors to $N-1$. To make the math visible, the slide sets demand and costs to simple numbers (1 and 0).

The Result: The table compares the total amount of goods produced before and after the merger. It shows that when firms merge, total market output falls.

The Harm: Because there is less product available, the market price rises. This harms consumers, meaning total economic welfare drops

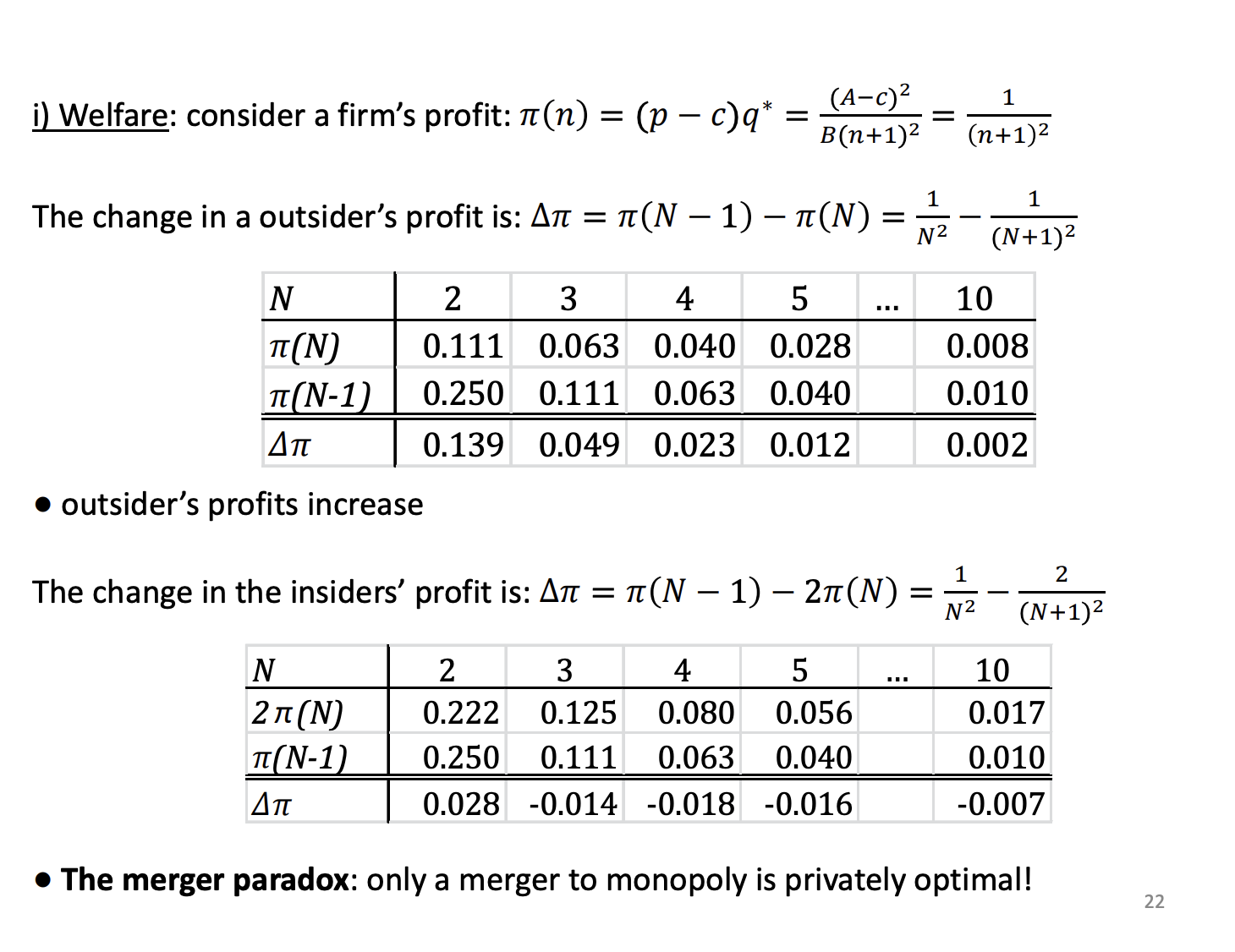

What happens to profits and welfare in the merger paradox and what is the resulting outcome

The Concept: This is the punchline. Since prices went up, someone must be making more money. But who?

The Outsiders (Top Table): The firms that did not merge see what is happening. The merging firms reduced output to drive up prices, so the outsiders happily swoop in to sell more at that new, higher price. Their profits increase dramatically.

The Insiders (Bottom Table): This table compares what the two merging firms made combined before the merger vs. what they make as a single merged entity.

The Paradox: Look at the negative numbers in the $\Delta\pi$ row. Unless the merger creates a total monopoly (going from 2 firms to 1), the merging firms actually lose money by merging! They take the financial hit of cutting production to raise the market price, but their un-merged rivals end up reaping all the rewards.

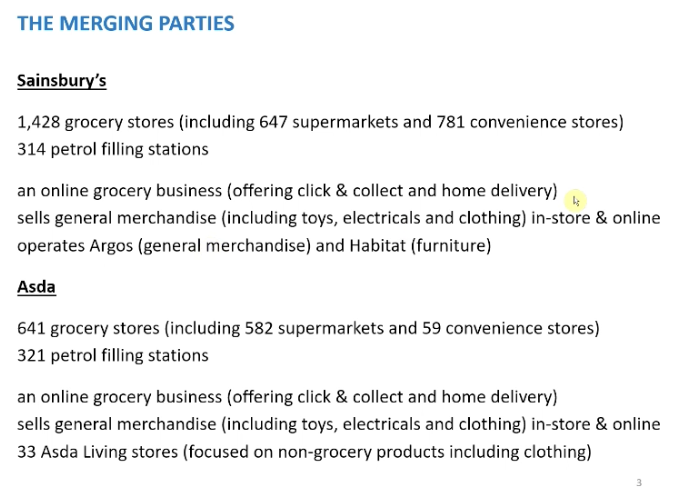

What are the two merging parities, number fo stores, pretol, markets, where were they mainly located

THE OVERVIEW OF THE MERGER AND looking at the parties involved. Bring together the second and third largest supermarket brand, but the competition agency were much wider as they were involved in a wider range of other activity, convenience stores, fuel are a few examples

Grocery - the number of stores, Sainsbury was much larger than Asda at the time of the merger. Sainsbury only had a small number more super stores, Sainsbury had many more convenience stores. Sainsbury more active in convenience store market than Asda. Main difference were locations, Sainsbury mainly located in the south, Asda more in the north of England. Sainsbury considered a place with high quality than Asda

Petrol - involved in supplying fuel, very similar. Asda slightly higher, normally located at the larger stores.

Online - both had online grocery service

General merchandise - both in store and online

Other - operate in other markets, like Argos and habitat. Asda involved in similar operations through their living stores, non grocery products

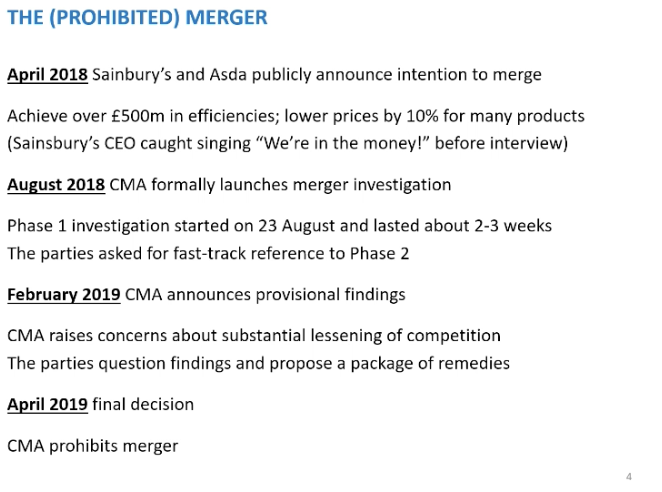

Key dates in the merger (2,1,2,1)

April 2018,, both publicly announced their intension to merge. From the outset you could tell people where sceptical. Sainsbury CEO was saw singing were in the money before a interview. Merging parties keen to emphasize the benefits of the merger, 50m pounds of efficiencies and lower prices of many products by 10%.

CMA launch investigation in Aug 2018, delay of a few month before the CMA start investigation for Sainsbury and Asda to get their houses in order (shareholders). Merger producers starts a two phrase process.

Phase 1 - quick look at the merger and decides if there are going to be problem from the merger, normally 6 weeks, competition aspects of the merger. If they can't resolve competitive issues in phase one, merger goes to phase two

Phase 2 - much long investigation into the merger and last up to 6 months.

Merging parities knew there would be some competition issues so they ask to be fast tracked to phase 2

Feb 2019 - End of phase two, raised concerns about lessening of competition with many aspects of the merger.

Allows parities to respond and propose remedies to overcome the CMA concerns and questioned the findings

April 2019: CMA agreed that the efficiencies were from doing more analysis were greater than they first expected. Admitted some of the problems that the merger could create would be unlikely to materialise, but some major problems were still there

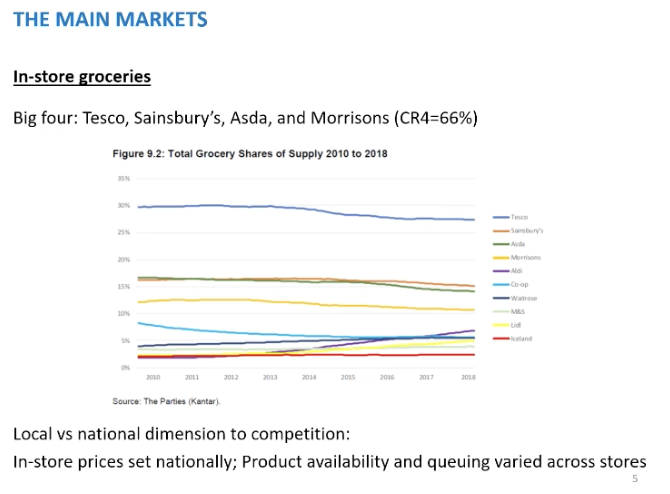

The instore groceries market

In store - going to the store to buy groceries. Market share over time

The big four - Tesco's (1st, 27%), Sainsbury (2nd, 15%), Asda (3rd,14%) and Morrisons (4th, 11%) in 2018

Merger would create the largest firm in the market, 15+14=29 %, just bigger than Tesco's.

Aldi and Lidi market share going up over time, the way we buy groceries changed over time from 2008, weekly shop to buying little and often.

From 2008, competition happening nationally vs locally. Competition commission argued completion between the supermarkets happen at the local level, supermarkets argued that it was at the national level. 2018 CMA much more willing to accept the national argument. This occurred as price were set nationally, same prices in England and Scotland. CMA did mention their was local dimension to competition as well, price might've been the same but the products differed across the store - impact the quality the consumer would experience

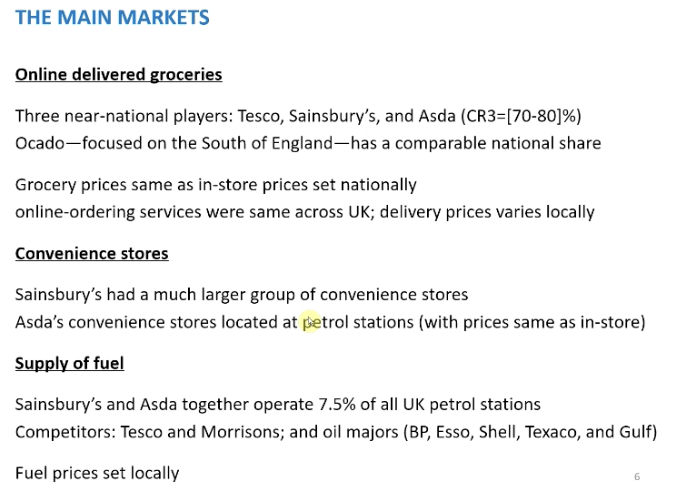

What were the other main markets

Another main market the CMA analysed, was the online delivered market. Structured in a very different way, only three near national players. Morrisons wasn't a player. Market share of around 70-80%. Tesco's is twice the size of Sainsbury and Asda. The only other competitor is Ocado, but only operated in the south.

Price set at national level, app and websites were consistent across the national level, but the delivery prices varied locally.

Convenience - Sainsbury much larger than Asda. The few that Asda had were located in the petrol stations and located at the larger stores. Prices in convenience stores were at the same level as in store, and those were set at the national level, where Sainsbury they set prices in convenience stores not nationally, local level.

Fuel - together operated just under 10%, competition very much at the local level, as prices set at this level

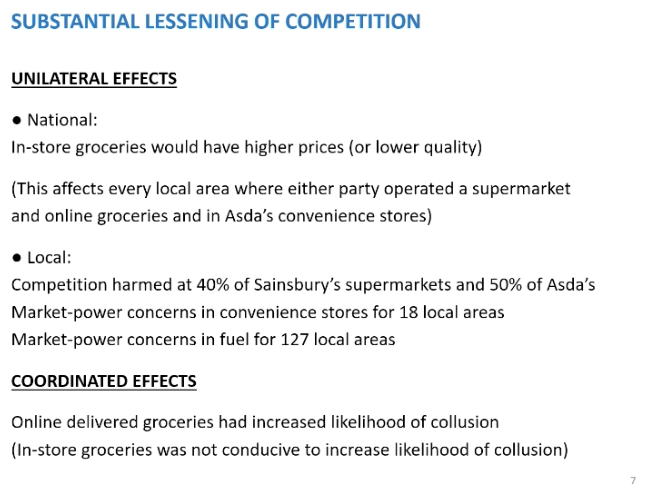

What were the two unilateral effects (national and local) and coordinated effects

CMA found a lessening of competition, both unilateral and coordinated effects.

Unilateral - national level the prices of the groceries in store would be higher as a result of the merger. Every local market would experience higher prices as a result of the merger. This is a complete change to what the CMA though in 2008, where thinking about nation and local competition. Would effect some of the other markets Aswell, online, same as the grocery prices in store.

Local - argued that even if we focused at the local level, competition issues would arise. 40% of Sainsbury and 50% of Asad supermarket stores. Price would be higher in these stores. Smaller number for convenience as Asda didn't have too many

Coordinated - in the online markets, increase chance of tacit collusive. Not the grocery prices but the delivery prices would be higher.

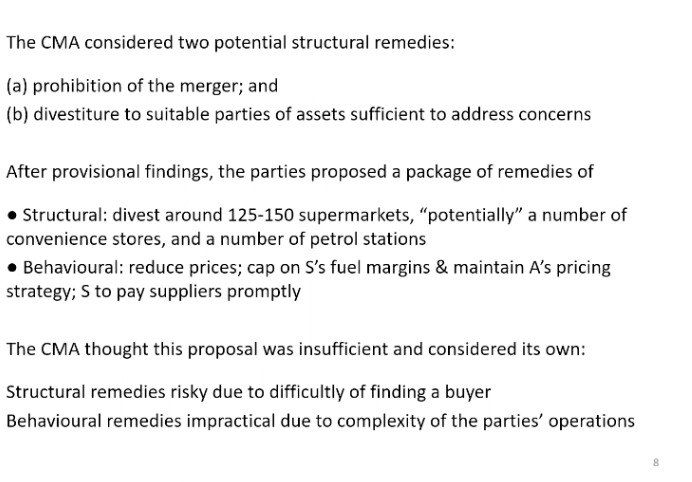

What were the two remedies the CMA proposed and what did the parties propose from this and what did the CMA conclude (structural and behaviour)

Why the CMA went for prohibition rather than remedies. Prohibition is blunt. Remedies much more elegant s it allows the CMA to remove part of the merger which would create problems and keep the parts that lead to efficiencies.

Remedies - can be structural or behavioural. Structure - sell of some of their assets to change the market structure, sell some supermarket. Behavioural merging parties accept some restriction on behaviour to prevent problems with regards to competition, price regulation

CMA did consider remedies. Thought was insufficient. Merger parties said the remedies from the CMA not willing to consider beyond their own. Structural likely to be risky from trying to find a buyer. Buyer could exit the market quickly as unable to produce a viable business.

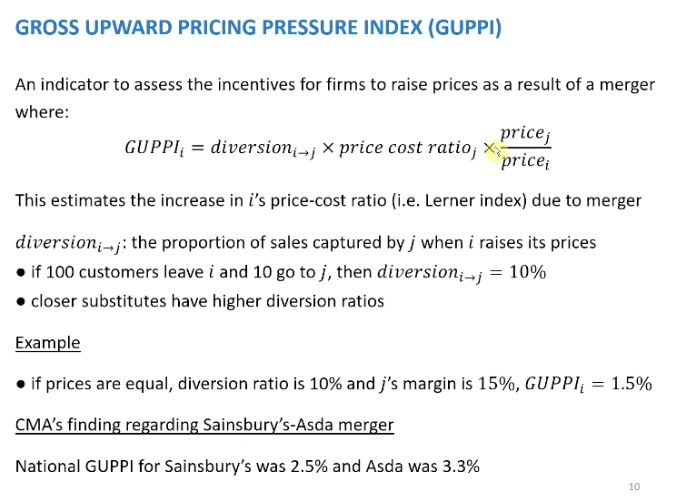

What is the GUPPI used to show, what is the components

CMA analysis of the unilateral effects. Relied on contemporary indicator if firms would raise prices GUPPI. Presents a measure of the market power changing using the Lerner index.

Two firms compete on prices and want to merger. Firm I and firm J. To calculate the GUPPI for firm I. RHS to left, we need prices of firm j and I, relative prices, times by the price cost ratio of firm J and lastly the diversion ratio, diversion ratio is of I to j is the proportion of sales that are captured by firm j when firm I raises it prices.

Price are equal to the relative prices will be equal to 1.

Example - GUPPI 1.5%, this means firm I is how much the firms price costs ratio of firm I increases, 1.5 tells us that the price cost ratio of firm I will increase by 1.5% as a result of the merger between firm I and firm j.

How to calculate the GUPPI

Calculating the GUPPI

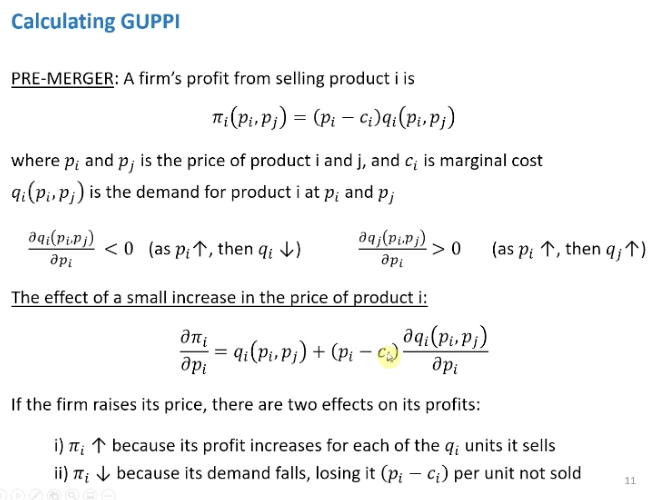

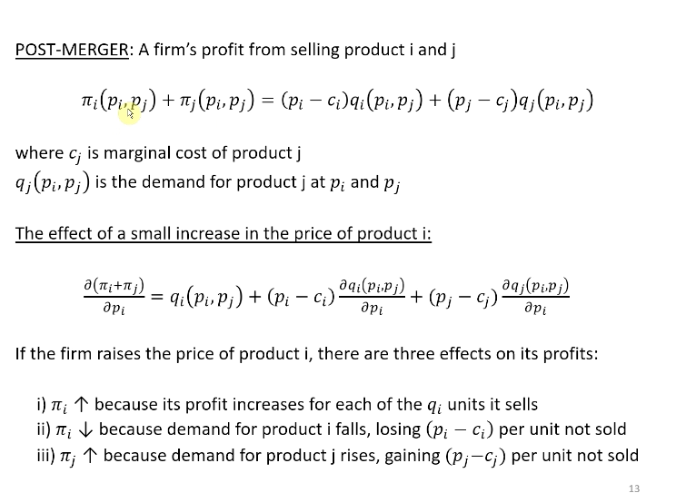

Considered he difference in the Lerner index pre and post merger. Thinking about the firm between firm I and j, compete in prices. Profits prices of firm I minus the marginal cost * the demand of firm I.

Assumptions on demand

Downwards sloping, fir I and j are selling substitutable products so if firm I increase prices the demand of firm j demand will increase.

Pre merger, profit max price is the point where the derivative of the profit function with respect to its price is equal to zero. Differentiation the top function in terms of Pi. Use the product rule.

Two effects from the derivative

Higher profit from each product sold (first term in the equation)

Less sold as demand is downwards sloping

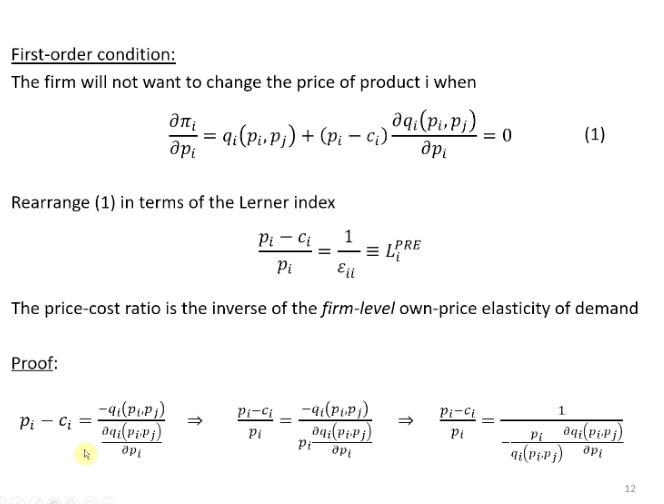

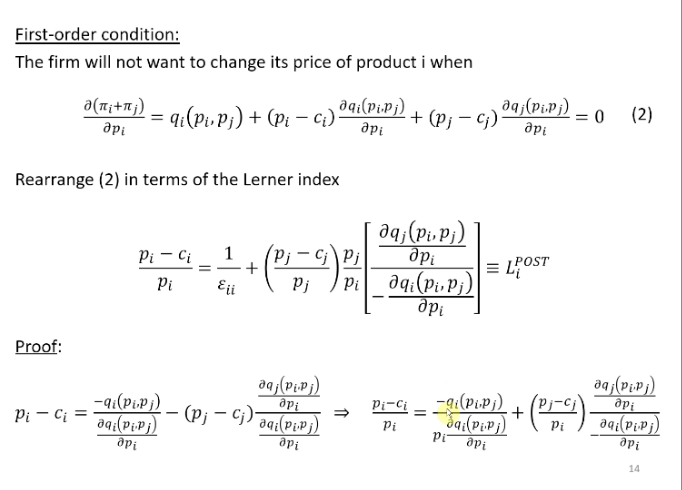

How to rearrange the FOC to the lerner index

Where the derivative is set to zero is the profit max price and can be rearrange to be put into the Lerner index.

Price cost ratio =. 1/ the own firm price elasticity of demand. Very similar to the case of monopoly, where monopoly price cost ratio would be equal to the price elasticity of demand, generalised to oligopoly, this is what you get for the price cost ratio for firm I is equal to the inverse of the firm level own price elasticity of demand

Post merger effects, what is the equation for the profits post merger and the differentiation

Calculate the post merger Lerner index

Firm I and j merge, the price set of the merger entity of product I, it will take account of how the price is going to affect the profits of product j.

Profits from product I and j

The effect of the merger entity profits from the price increase in product I. Differentiation in term of pi, both terms. In the second term pi only comes in to the second term, the demand curve of product J.

Effects

Same first two effects. The new third effect, because the merged entity is setting a higher price for I, the demand for I is going down but the demand for j is going up because j is a substitute, so some of the consumers are substituting away from product I to product j. And so the demand for product j is going up and the profits of the merged entity are going up by the price cost margin of the unit of product j it sells.

How do you re arrnage the post merger effects to get the lerner index

Profit max of product I is given by a driveritative being set to 0 and then if we rearrange to get in terms of the Lerner index. The big horrible term is the GUPPI of firm I, the post Lerner index of firm I is the firm level own elasticity of demand + the GUPPI of firm I.

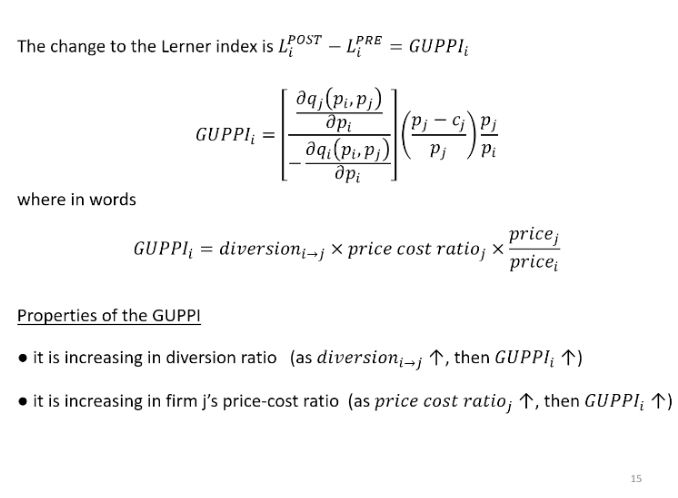

The change in the lerner index is equal to and what are the two properties

Calculate the change in the Lerner index. We get the GUPPI for firm I or product I.

It some of the diversion parameter, as the denominator is telling us the extent to which firm I demand goes down because of an increase in its price and the numerator tells us the extent which firm J demand is going up due to the increase in firms I prices

Doing this calculation, we can now see that the GUPPI firm I is telling us how much the Lerner index is going to change post merger

Properties

Diversion ratio is higher, the GUPPI for firm I is higher. When the price of product I increase and leads greater proportion of demand that will leave product I and join product j this means that there is a greater incentive for the merger entity ti0set higher price for product I. because the firm will loss less from raising the price as the consumers that is loses a lot of them will go to product j and not lose much profit from this

Increasing the price cost ratio of product j all other things being equal, this happens when it increase its price for product I some of the consumers are going to be switching away to product j and so when the price cost ratio for product j is quite high the merged entity is less worried about losing consumer from product I t product j, more willing to set a higher price.

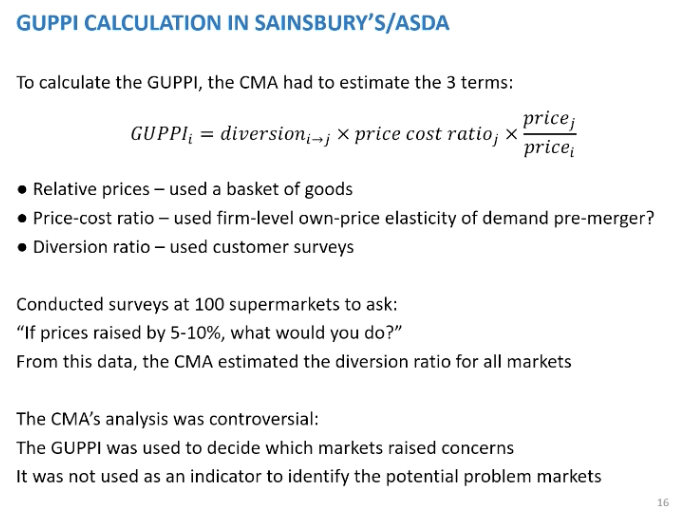

What are the three componets the CMA need, how were the surveys conducted and what was the guppi used for

Calculate the GUPPI in Sainsbury and asada, the CMA had to estimate the three components in the GUPPI. SO with regards to relative prices, they would decided on a representative basket of goods would be and look at the price of that basket. PCR would've done by using level firm own elasticity of demand pre merger, Lerner index. Diversion ratio, CMA did surveys at 100 supermarkets across the country, the question they asked if the prices at this supermarket store increase by 5/10% what would you do. So said we would stay other switch stores. This information would estimate the diversion ratio between Asda and Sainsbury.

CMA looked at no just the national level but also the local level. The CMA analysis was controversial, the GUPPI was used to determine which markets that would cause problems, to just be an indicator of a problem. The merger lectures said the CR used to identify possible problem markets, grey areas. Here the CMA didn’t follow this approach, they set a threshold, if above that GUPPI mark, it was a problematic market. The GUPPI was only based on 100 supermarkets

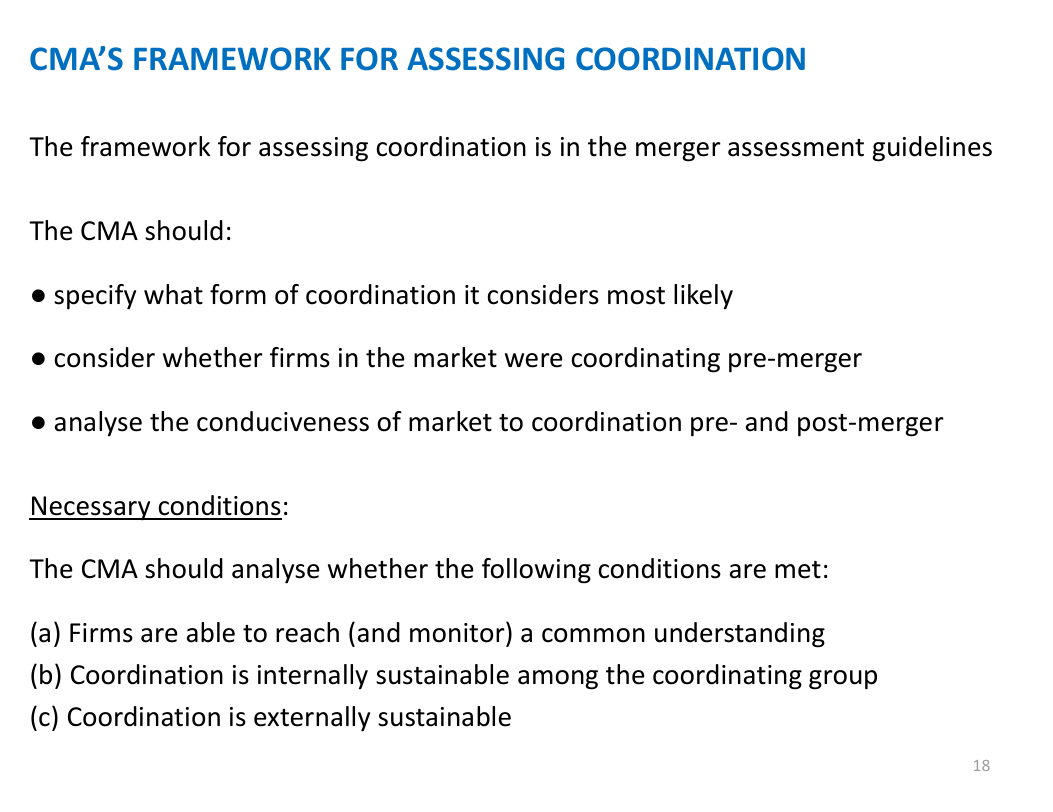

CMA fraemwork for assessing coordinated effects

Coordinated effects from the CMA analysis in Sainsbury and Asda

They arise in a merger, when the merger increased the likelihood of tacit collusion. The CMA needs to a formulaic approach to assessing coordination. The reason for this is because the theory. Of collusion leads the CMA down that route, no sort of easy indicator you an use to get at collusion.

Meger assessment guidelines

Specify who the collusion is likely to be among and what strategic variables and what geographic market and how it will arise

Consider if the firms in the market are coordinating pre merger. Easier to argue that coordinated effects will arise from a merger if collusion is occurring in the market pre merger. Look at pricing alignments, if price go up and own together, or if there has been a cartel in the market

Look if the market is conducive to collusion pre and post merger, do this whether there is collusion pre and post merger \

The last bullet point necessary conditions

(a)

How easy for firms to coordination, and do this by looking if the firms sell differentiated products or not. Easier to reach an agreement if they sell similar products

Number of product the firms sell, more difficult if they sell a large number

Monitor agreements, CMA look for if firms can detect deviations of their rivals, if they cant very difficult to impose a punishment

(b)

Related to the theory of repeated games, if a firm deviates is there's sufficiently harsh response by its rivals that will punishment is deviation, if there is a punishment it will remove its incentive to undertake that deviation

©

Is it externality sustainable, firms outside of the collusive groups that can undermine collusion. For instance, that might be due to entry or because the collusive groups does not encompass all groups in the market. All firms in the market are part of the collusive group is normally the theory

For the CMA to find the merger produces merger effects, they have to argue that, and say this is the form of collusion we have in mind, say whether they think there is collusion or not pre merger, if they argue there isn't collusion pre merger, they need to say why and then if they argue there is going to be collusion pots merger they need to argue what has changed compared to pre merger

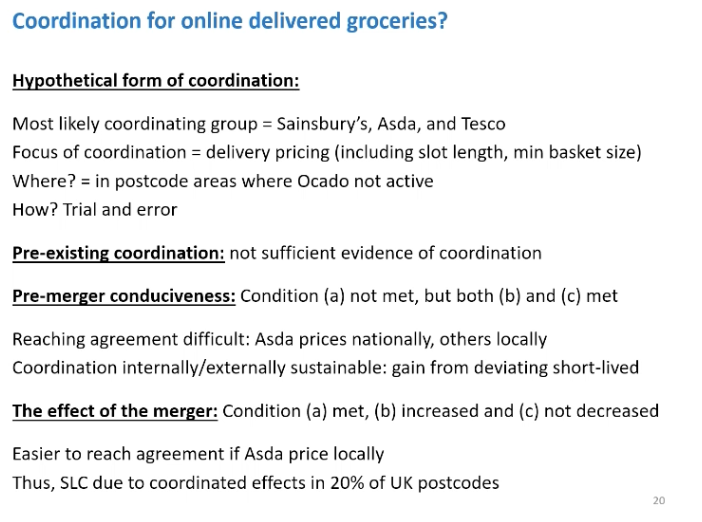

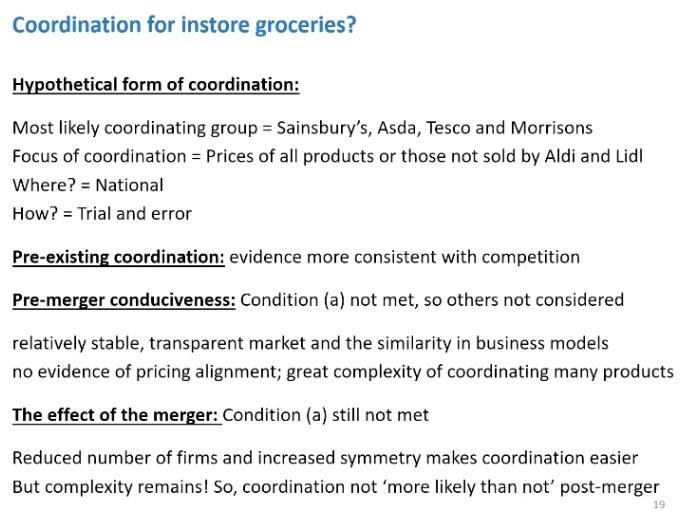

Coordination for instore groceries, coorindating group, focus, location and method

SAINSBURY and ASDA example

Investigated the merger for coordinated effects in the market for instore groceries and for online delivered groceries.

In store

Mostly likely coordinated group according to the CMA was the big four supermarkets and if collusion was going to occur this is the firms it would occur between. CMA on the focus Aldi and Lidl would put competitive pressure on the coordinating group and unable to sustain collusion if the Aldi and Lidl sold those products.

National - prices set nationally

Trail and error - one raise prices, and other would follow. To coordinate in higher prices.

Pre merger effects

Pre no collusion, discussed various points, expend a lot amount of resources monitoring each other and they have stable market shares. Noted there was a cartel in the supermarkets for diary products about 20 years ago. Mentioned the Comp commission found the merger Safeway and Morrisons would create coordinated effects, all of these factored pointed towards there being coordinated effects in these markets.

No evidence of price alignment, also looking to undercut each other

Condition a not met, therefore it was too difficult for this coordinated group to from a collusive agreement so it didn’t need to considered condition b and c

Post merger

Number of firms reduce from 4 to 3. Theory would tell us it would make collusion easier. Would create the largest firm in the market of 29% and be very similar to Tesco's market share of 27%, might be reduced asymmetry and make collusion more simple to sustain. Condition A still not met, and be too difficult o form a collusion agreement post merger, due to selling some many products.

Coordinated for online delivered groceries

Online delivered

CMA said coordinated effects would arise. Morrisons not a big player in the online space. Not just the prices of delivery but the slot length and min basket size for delivery could be effected. Arise in postcodes were there was no competition, Ocado was the fourth players, and only located in the south.

Pre Merger

Looked at internal documents of the firms, suggested the firms were investing a lot of resources looking at rival delivery prices but on the other hand the CM noted that Sainsbury ASDA and Tesco all have different pricing strategies when it comes to delivery prices, also noted no pricing alignment in the market. Looked at the three conditions A, was not met, whether the firms could reach an agreement. CMA came to the conclusion due to the different pricing strategies. Overcoming these differences would be too much to reach an agreement in collusion. Still considered B and C conditions, internally and externally stable. Able to monitor and quick response to deviations. Looking at market where Ocado wasn't operating, no firms likely to influence the agreement.

Post merger

Condition A was now met, would be able to reach an agreement post merger. Collusive arrangement would be easier to sustain internally and it also said the external constraints on the collusive group would no decrease.

The merged entity would follow one price strategy and make it easier for firms to reach an agreement at the local level. Easier to sustain as number of large players decreased. Increase the degree of symmetry as well, as Tesco was twice the size of Sainsbury and Asda.