Chapter 5: Basic Economic Concepts

5.1 Scarcity

Scarcity: occurs because unlimited desire for goods and services exceeds limited ability to produce them due to constraints on time and resources

Resources

- Also sometimes called inputs or factors of production

- Examples

- Capital (physical capital): manufactured goods that can be used in the production process

- Ex) Tools, machinery, equipment

- Labor: physical and mental effort of people

- Includes human capital: knowledge and skill acquired through training and experience

- Entrepreneurship: ability to identify opportunities and organize production, and willingness to accept risk to pursue rewards

- Natural resources: refers to any productive resource existing in nature

- Ex) Wild plants, wind, water

- Acronym: Crazy Leopards Envy Narwhals → Capital, Labor, Entrepreneurship, Natural resources/land

- Energy and technology are considered to be byproducts

- Production models often just includes labor and capital

5.2 Resource Allocation and Economic Systems

- Economics: study of how societies allocate scarce resources among competing ends

- Positive economics: describes the way things are

- Ex) “The unemployment rate hit a three-year high”

- Normative economics: way things should be

- Ex) “The Fed should lower the federal funds rate”

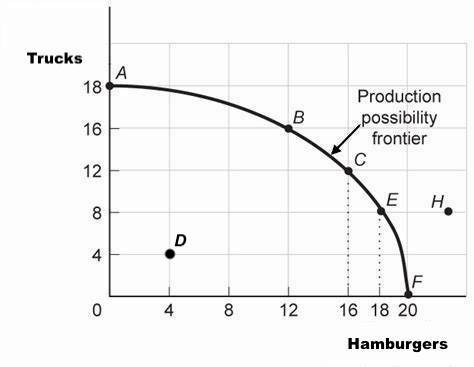

5.3 The Production Possibilities Curve

- Opportunity cost: value of the best alternative sacrificed compared to what actually takes place

- Ex) Opportunity cost of studying is losing sleep

- Production-possibilities frontier: illustrates the opportunity cost of making one good rather than another one

- Abbreviated as PPF

- Frontier: curve that represents all of the combinations that could be produced using available resources

- If a point is outside the frontier, the good cannot be produced since it needs more resources than the economy has

- If a point is inside the frontier, it can be obtained but is inefficient

- Efficiency: all of the resources are used productively

- Resources are wasted

- Can determine opportunity cost from PPF

- Greater absolute value of slope = greater opportunity cost

- Consumer goods: products for sale in a retail or consumer market used directly by consumers

- Capital goods: things purchased to produce other goods

5.4 Comparative Advantage and Gains From Trade

- Specialization

- More efficient → increases productivity

- Division of labor: allows people to develop expertise in certain tasks, where practice improves performance

- Absolute advantage: when a country can produce a good using fewer resources per unit of output compared to another country

- Comparative advantage: when a country can produce a good at a lower opportunity cost compared to another country

- Consumption possibilities frontier

- With trade, countries can have a consumption possibilities frontier that exceeds its own production possibilities frontier

- Slope is determined by terms of trade

5.5 Cost-Benefit Analysis

Business project factors

- Cost of implementing project

- Resulting benefits

Cost-benefit analysis: comparing value of cost vs. benefits

5.6 Marginal Analysis and Consumer Choice

- Distributive efficiency (efficiency in exchange): those who place the highest relative value on goods should receive them

- Ex) Auctions

- Achieved when marginal rate of substitution is equal for every consumer

- Marginal rate of substitution: ratio of marginal utility for two goods