Chapter 3: Economic System

The fundamental economic questions

- “What resources to produce?”-first basic economic question

- “What quantity to produce the resources?”-second basic economic question

- Decided quantity is based on the concept of opportunity cost

- As more of good A is produced, the lesser good B is to be produced

- “Who gets the resources and how much?”-third basic economic question

Economic Systems

3 ways to address the economic question

- Government commands

- Capitalism

- A blend of government commands and capitalism

Command economy: Economy dominated by the government- they decide what gets produced, in what quantity, and who is entitled to it.

Disadvantages

- Relies on a quota system and production plans-difficult if millions of products

- Requires strong coordination of the production of various goods and services.

E.g. achieving the production level of crops also needs proper coordination with the quality of land, machinery available, etc.

- Extremely tough task to allocate prices for so many goods and decide who is entitled to them

Advantages:

- Unemployment rates fall

- Prevent class differences by controlling wage rates

- Price control of socially desirable and undesirable goods

Capitalism

- The economic system where supply and demand define the prices

- This supply-demand determines how much is produced

- This supply-demand determines the income of people in an economy and how much do they get from the economy

- The government creates an environment where prices can be determined in a free market

- Consumers decide how much of each product would be produced

- Upon noticing the profit potential, suppliers produce more of product A-hence product B’s quantity is reduced

- The government doesn’t influence prices in capitalist markets-prices and wages are determined in the free market and this helps answer the basic economic question

- The right products are produced in the right quantity-Product A would be produced in a quantity based on only the number of people who demand it-This is known as allocative efficiency

Allocative Efficiency

Free markets are unaffected by third parties who are uninvolved. E.g. Government

The more perfectly competitive a market exists in an economy, the closer the economy is to perfect capitalism

The free market offers 2 main benefits

- Helps answer the basic economic question

- Decentralizes the authority-government doesn’t have to interfere to ensure production

- Thus, when all prices are established in a market, optimal allocation is done to ensure the right resources are deployed and in the accurate quantity- this is allocative efficiency

- Government intervention impacts the invisible hand in the economy but they still have an important role to play in the economy

The Mixed Economy

- Government, in a capitalist economy, usually interferes when free markets themselves fail e.g. USA

- The interference is usually for society’s benefit e.g. educational support in the form of student loans, grants, etc after higher education is completed

- All countries in real-world function using both capitalist and command market-just the domination varies on this scale

- The USA is closer to a capitalist economy than a command whereas Cuba is the opposite, being closer to the command economy

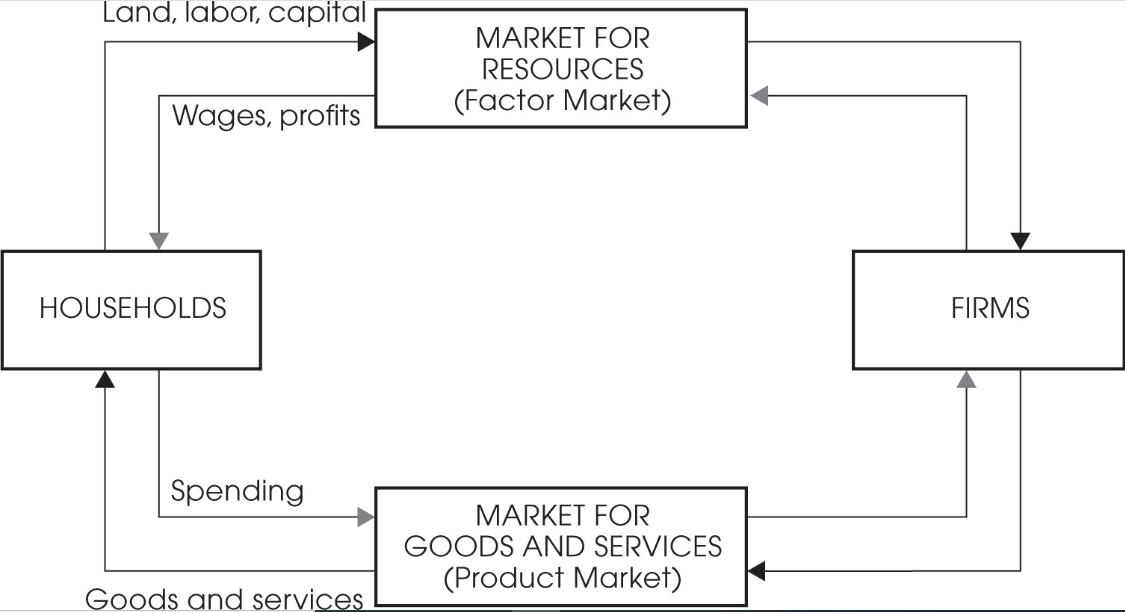

The Circular Flow Diagram

- In capitalist economies, most resources are owned by individuals, and households-government owns small shares too

- Resources are transferred from households to firms and in return receive wages and profits

- The resources are sold so that firms may produce goods and services

- This exchange of money for resources is known as the “market for resources.”

- Households spend their wages and profit to purchase the goods and services that the firms supply

- This exchange of income for goods and services is known as the “market for goods and services”

- The diagram represents how institutions are tied up in a capitalist economy

- The diagram can be further expanded to include banks and government