Causes of Shift in Supply Demand Curves (AP)

Aggregate Demand

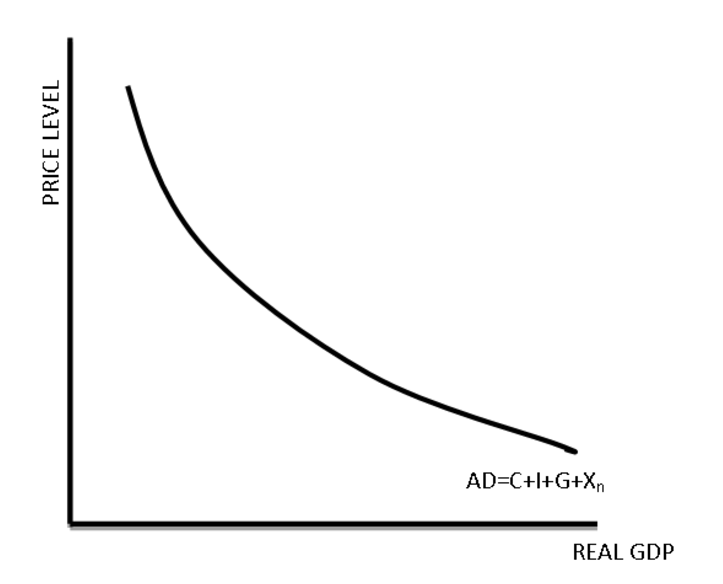

Definition: Measures the total value of all goods and services produced in an economy, expressed as AD=C+I+G+XnAD = C + I + G + XnAD=C+I+G+Xn (consumption, investment, government spending, and net exports).

Relationship with GDP: AD is equivalent to real GDP in the long run.

Curve: Downward sloping, as price levels rise, AD decreases due to:

Wealth Effect: Higher prices reduce purchasing power, lowering demand.

Savings & Interest Rate Effect: Higher prices reduce savings, raising interest rates, which discourages investment and consumption.

Exchange Rate Effect: Higher prices make imports cheaper and exports more expensive, reducing net exports.

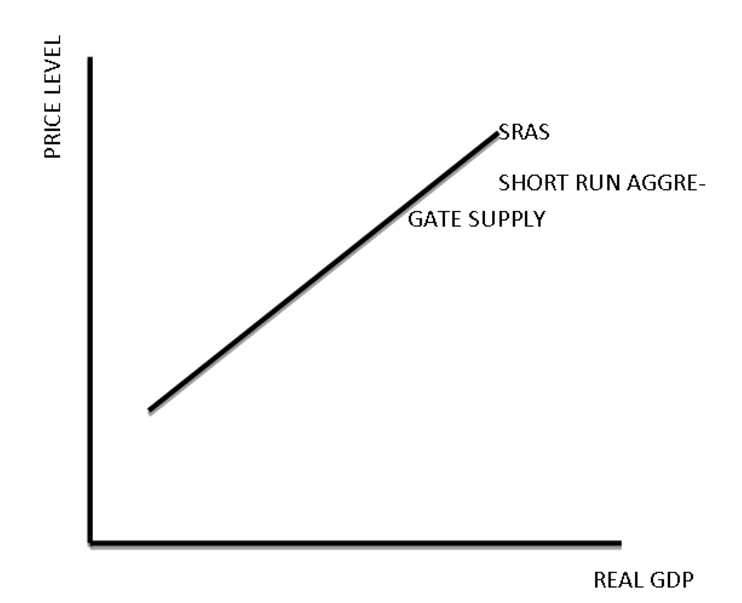

Definition: Total goods and services producers supply at a given price level.

Curve Representation:

Short-Run Aggregate Supply (SRAS):

Upward sloping; higher prices lead to increased production.

"Sticky" resource prices prevent immediate adjustments.

Real GDP may not reach full employment levels.

Long-Run Aggregate Supply (LRAS):

Vertical curve; unaffected by price levels.

Real GDP equals potential GDP.

Determined by:

Labor availability

Capital stock

Technology levels

Key Factor: Time impacts the flexibility of resource prices and production capacity.

Changes in price levels, holding other things constant (ceteris paribus), causes movements along both aggregate demand and aggregate supply curves. However, other factors can shift aggregate demand and aggregate supply curves.

Shifts Aggregate Demand

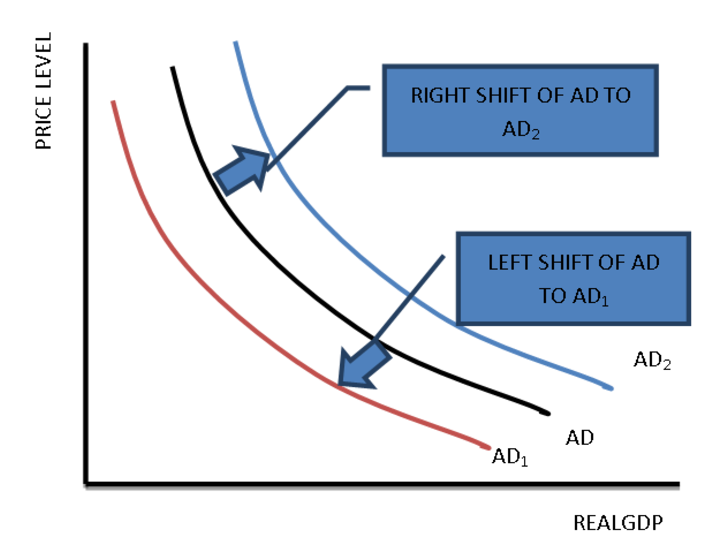

Shifts in aggregate demand occur due to changes in its main components: consumption (C), investment (I), government spending (G), and net exports (Xn). These shifts alter the total demand for goods and services within the economy, leading to a rightward or leftward movement of the aggregate demand curve. For visual representations or further details, refer to the original source.

1. Expectations

Positive Expectations:

Anticipation of higher inflation, future income, or profits increases consumer spending and investments.

This drives up real GDP, shifting the aggregate demand curve rightward (AD2).

Negative Expectations:

Recession fears cause reduced consumer and business spending.

Real GDP decreases, shifting the aggregate demand curve leftward (AD1).

2. Government Fiscal and Monetary Policy

Fiscal Policy:

Tax Reductions or Increased Spending:

Increases consumer wealth and investments, driving real GDP up.

Shifts aggregate demand rightward (AD2).

Higher Taxes or Reduced Spending:

Decreases consumer wealth, contracting real GDP.

Shifts aggregate demand leftward (AD1).

Monetary Policy:

Higher Interest Rates:

Strengthens the dollar, raises the cost of local goods, and lowers investment and consumer spending.

Shifts aggregate demand leftward (AD1).

3. Changes in Foreign Trade

Increased Net Exports:

Boosts aggregate demand, shifting the curve rightward (AD2).

Decreased Net Exports:

Occurs due to:

Preference for foreign goods over local products.

Strengthened dollar reducing export competitiveness.

Faster U.S. GDP growth compared to other nations, strengthening the dollar and lowering net exports.

Shifts aggregate demand leftward (AD1).

4. Changes in Productivity

Improved Productivity:

Enhanced production efficiency through better management or technology.

Boosts investments and exports, shifting aggregate demand rightward (AD2).

Shifts Aggregate Supply

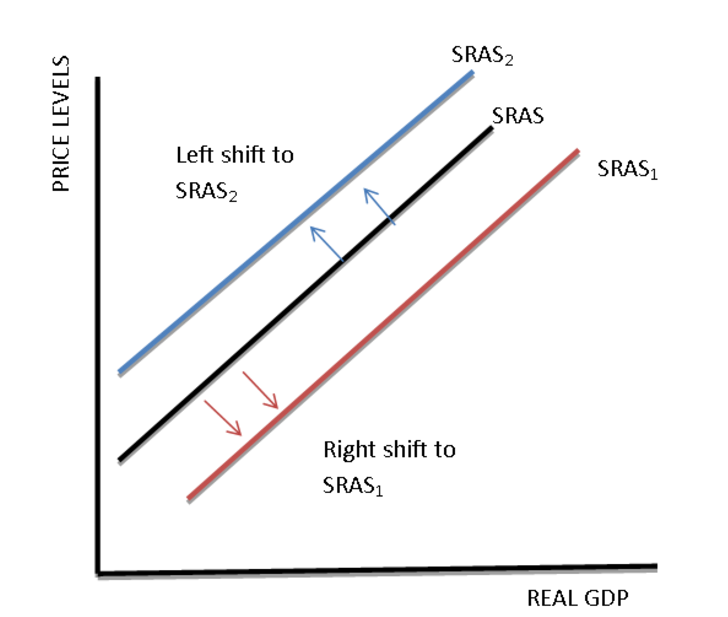

Shifts in the short-run aggregate supply (SRAS) curve are influenced by:

Inflationary Expectations: Expected price level changes can impact costs and supply decisions.

Labor Force and Capital Availability: Changes in the number of workers or available capital affect production.

Government Actions: Policies such as regulations or taxes (distinct from government spending) can impact costs.

Productivity Changes: Improvements in productivity can increase supply.

Supply Shocks: Unexpected events (e.g., natural disasters) that disrupt production.

Short-Run Aggregate Supply (SRAS) Shifts

Inflationary Expectations:

If firms and workers expect prices to rise, SRAS shifts leftward (SRAS2) as higher expected prices increase production costs.

Labor Force and Capital Stock:

Increased availability of labor and capital enhances production capacity, shifting SRAS rightward (SRAS1).

Government Action:

Restrictive Policies (e.g., taxes, removing subsidies, regulations) shift SRAS leftward (SRAS2).

Supportive Policies (e.g., tax cuts, subsidies, deregulation) shift SRAS rightward (SRAS1).

Positive Institutional and Technological Changes:

Advances in technology or improvements in business practices reduce production costs, shifting SRAS rightward (SRAS2).

Supply Shocks:

Unforeseen events like natural disasters or resource shortages increase costs, shifting SRAS leftward (SRAS1).

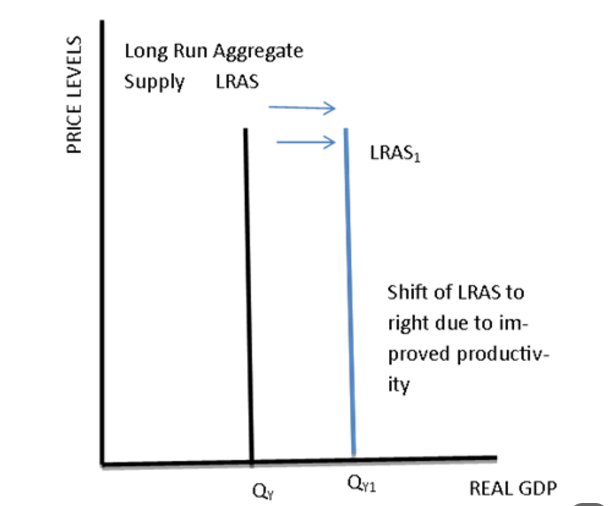

Long-Run Aggregate Supply (LRAS) Shifts

Technological Advancements and Labor Quality improvements increase potential output, shifting LRAS rightward (LRAS1).

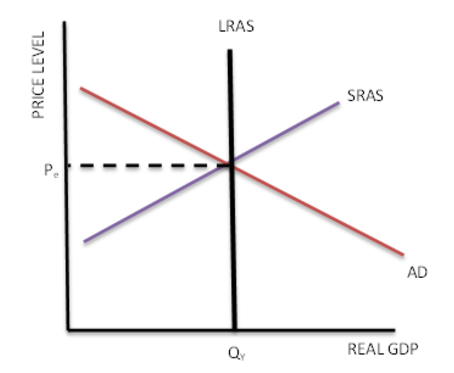

Long-Run Macroeconomic Equilibrium occurs when the AD, SRAS, and LRAS curves meet at the equilibrium price level and full-employment GDP (Pe and QY).

Macroeconomics Schools of Thought

Keynesian Theory

Key Idea: Aggregate demand (AD) is influenced by both private and public sector decisions.

Keynes’ View: Economic output is driven by AD; during recessions, government intervention (fiscal and monetary policy) is necessary to stimulate the economy.

Sticky Prices and Wages: Prices and wages do not adjust quickly in the short run due to fixed contracts.

Classical Theory

Key Idea: The economy is self-regulating and can reach potential GDP/full employment naturally.

Self-Adjusting Mechanisms: Economic downturns are brief, with prices, wages, and interest rates being flexible.

Say’s Law: Supply creates its own demand; the income generated by producing GDP is sufficient to buy that GDP.

Importance of AD and AS

AD and AS curves are fundamental to understanding macroeconomics, influencing taxation, international trade, and government policy.

Governments use these concepts to influence investments, interest rates, and consumer spending, ensuring economic stability.

Example:

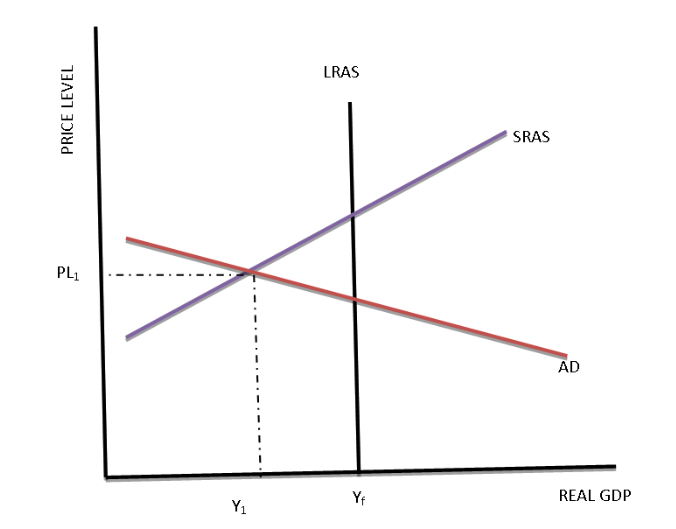

Graph Instructions for U.S. Economy Below Potential GDP

(a) Label the following curves:

Long-Run Aggregate Supply (LRAS): Vertical line at Yf (full employment GDP).

Short-Run Aggregate Supply (SRAS): Upward sloping curve.

Aggregate Demand (AD): Downward sloping curve.

Identify equilibrium:

Equilibrium Output (Y1): Point where AD and SRAS intersect.

Equilibrium Price Level (PL1): Corresponding price level at intersection of AD and SRAS.

Full-Employment GDP (Yf): Vertical LRAS at potential GDP, to the right of Y1 (indicating underperformance).

(b) Federal Reserve's Target for Federal Funds Rate

The Federal Reserve should target a lower federal funds rate.

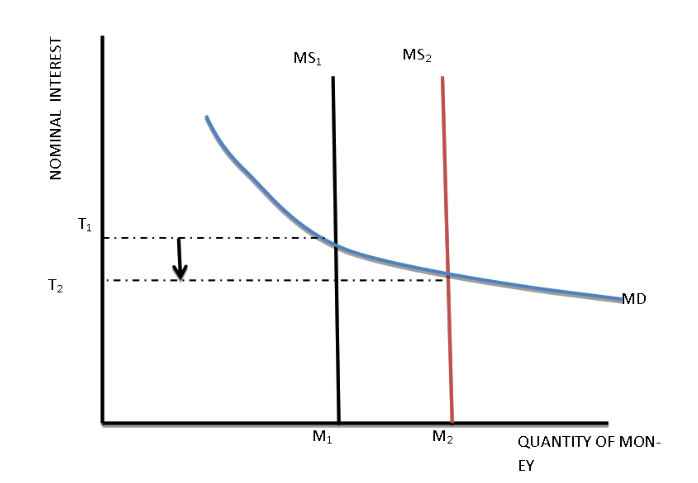

(c) Justification and Money Market Graph

Justification: A lower federal funds rate reduces borrowing costs for banks and consumers, which encourages more spending and investment. This increase in aggregate demand helps to move the economy closer to full employment (Yf).

Money Market Graph:

Money Supply Curve (MS) shifts rightward to MS2.

Nominal interest rate decreases, which stimulates borrowing and spending.

The new equilibrium is at a lower interest rate, which boosts economic activity.

(d) Fiscal Policy and Government Spending

(i) Least Required Change in Government Spending:

The minimum change in government spending is calculated using the government spending multiplier.

Formula: Recessionary gap ÷ Government spending multiplier = $300 billion ÷ 5 = $60 billion.

This means the government needs to increase spending by $60 billion to close the recessionary gap.

(ii) Impact of Changing Taxes:

The least required adjustment in taxes will be larger than the required adjustment in government spending.

Explanation: The tax multiplier is smaller than the spending multiplier. For tax changes, a portion of increased income is saved rather than spent, reducing the overall impact.

Tax multiplier:

Thus, tax adjustments are less effective.

(e) Effect of Easing Income Tax Rates

(i) Effect on Aggregate Demand:

Lowering income taxes increases disposable income, which boosts consumption and investment, raising aggregate demand.

(ii) Effect on Aggregate Supply:

Possible outcomes:

No change in LRAS: Lower taxes may stimulate consumption and investment, but no change in input levels.

Increase in LRAS: Low taxes may increase savings and investment in physical capital, improving productivity.

Decrease in LRAS: Potential for crowding out, where tax cuts reduce government revenue, limiting public investment and reducing LRAS.