Chapter 5: Elasticity

- Elasticity helps us assess how responsive consumers or suppliers are to changes in the prices of goods or services.

- ^^Elasticity is a measure of responsiveness between any two variables.^^

- In the demand model, the price elasticity of demand measures how responsive quantity demanded is to a change in a good's price.

- In the supply model, the price elasticity of supply measures how responsive quantity supplied is to a change in a good's price.

- The price elasticity of demand measures how quantity demanded responds to changes in price, but uses percentage changes rather than raw numerical changes.

- Percentage changes provide a consistent measure that we can compare across different variables such as price and quantity.

- Economists categorize the price elasticity of demand into two broad categories to describe the different levels of consumer responsiveness to changes in goods' prices: elastic demand and inelastic demand.

- Elastic demand is when a given percent change in the price of a good causes a larger percent change in the quantity demanded of the good.

- When consumers have elastic demand for a good, they are relatively responsive to changes in that good's price, so that a given percent change in the good's price causes a larger percent change in the good's quantity demanded.

- Inelastic demand is when a given percent change in the price of a good causes a smaller percent change in the quantity demanded of the good.

- When consumers have inelastic demand for a good, they are relatively unresponsive to changes in that good's price.

- Within the elastic and inelastic categories of elasticity are three important subcategories that represent the special cases of consumer responsiveness to price changes: perfectly inelastic demand, perfectly elastic demand, and unit elastic demand.

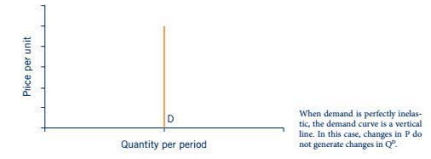

- Perfectly inelastic demand is the extreme subcategory of inelastic demand that describes the situation where quantity demanded does not change in response to a price change.

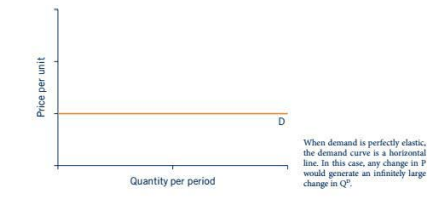

- Perfectly elastic demand is the extreme subcategory of elastic demand that describes the situation where quantity demanded changes by an infinite amount in response to a price change.

- Unit elastic demand is when a given percent change in the price of a good causes an equal size percent change in the quantity of the good demanded.

- The elasticity coefficient is the percent change in quantity demanded divided by the percentage change in price.

- When demand is elastic, the absolute value of the numerator of the elasticity coefficient will be greater than the absolute value of the denominator of the elasticity coefficient.

- When the numerator of a fraction is greater than the denominator of a fraction, the fraction's value is greater than 1.

- Correspondingly, when demand is elastic, the absolute value of the elasticity coefficient is greater than 1.

- When demand is inelastic, the absolute value of the elasticity coefficient is less than 1 because the numerator of E will be smaller than the denominator of E.

- Total revenue (TR) is the amount of money earned when a supplier sells a given quantity of a good. Total revenue is equal to the price of the good multiplied by the quantity of the good sold.

- When demand is inelastic, an increase in price causes an increase in total revenue.

- When demand is elastic, a decrease in price causes an increase in total revenue, while an increase in price causes a decrease in total revenue.

- There are four factors that impact the price elasticity of demand:

1)The Availability of Substitutes

2)Luxury versus Necessity Goods

3)The length of Time Available to Adjust to a Price Change

4)The Portion of Income Spent on the Good

- When demand is perfectly inelastic, at each of the possible prices quantity demanded is constant and unchanging.

- At the other extreme, when demand is perfectly elastic, price does not change, and demand is represented by a horizontal line.

- There is a relationship between the slope of a demand curve and the price elasticity of demand.

- For a given change in price, a steeper demand curve reflects more inelastic demand than a flatter demand curve.

- The quantity demanded is more responsive along the flat demand curve than on the steep demand curve, which means that demand is more elastic on the flat demand curve than on the steep demand curve.

- As a general rule, for the same price change, steeper demand curves reflect more inelastic demand, while flatter demand curves reflect more elastic demand.

- At the extremes, the steepest possible demand curve is vertical and reflects perfectly inelastic demand.

- Although there is a relationship between the price elasticity of demand and the slope of the demand curve, we cannot conclude that steep curves always represent inelastic demand and flat curves always represent elastic demand.