AP Microeconomics - Unit 3 Notes

Unit 3 Microeconomics

3.1 The Production Function

3.2 Short-Run Production Costs

3.3 Long-Run Production Costs

3.4 Types of profit

3.5 Profit maximization

3.6 Firm's short-run decision to produce and long-run decisions to enter or exit markets

3.7 Perfect competition

Some info/photos taken from Jacob Clifford and ReviewEcon on youtube.

3.1 - The Production Function

The Production Function - The relationship between the quantity of inputs used and quantity of outputs

Fixed Inputs

Cannot [easily] change during a period of time

Generally land in short-term runs. Should be at least 1 in short-term

Variable inputs

Can change over a period of time

During long runs, all inputs are variable

In, short-run, ex: land

Short-Run

at least one fixed input

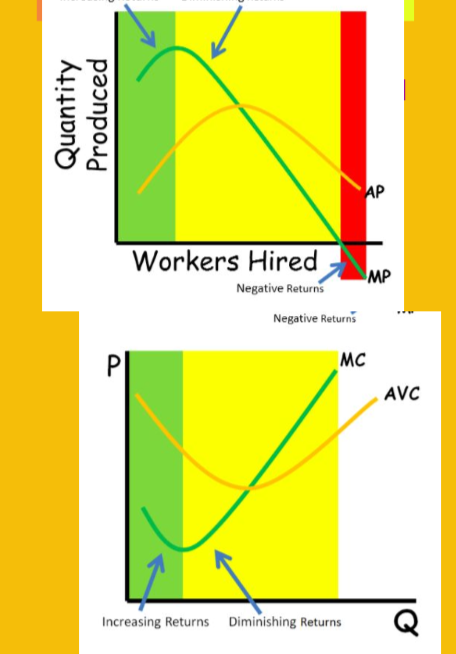

Law of diminishing marginal returns applies

Long-Run

All inputs are variable

Law of diminishing marginal returns does not apply due to variable inputs

(△ = change in)

Total Product (TP) - The total quantity of output produced by a firm given a fixed input.

TP=Sum(MP)

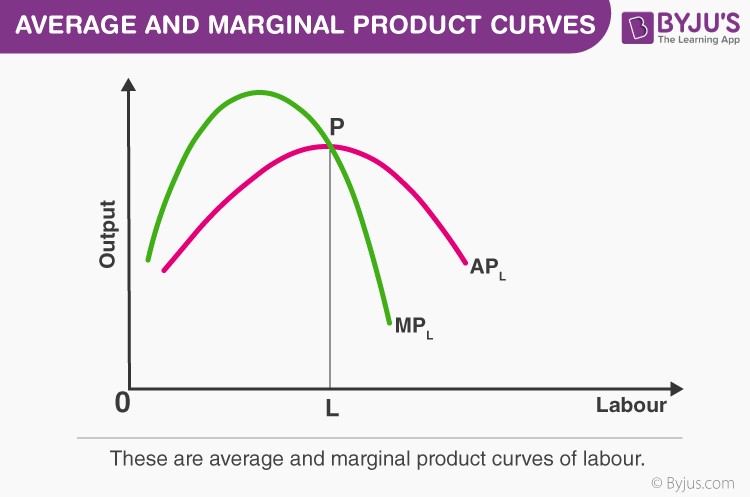

Average Product (AP) - The total quantity of output produced per unit of labor

AP - TP/L

Marginal Product - extra output created by adding an additional worker

△TP/ △L

The Law of Diminishing Marginal Utility - As a person consumes more of a good, they get less pleasure out of additional units. Related to Consumer behavior.

The Law of Diminishing Marginal Returns - Eventually, when there is a fixed amount of land/capital, adding another worker decreases utility. (Things get too crowded!) Related to producer behavior. Sets in whenever marginal product begins to decrease

There is an initial increase in marginal product due to specialization

3.2 - Short-Run Production Costs

Producers want to maximize profits, pi=profits in economics

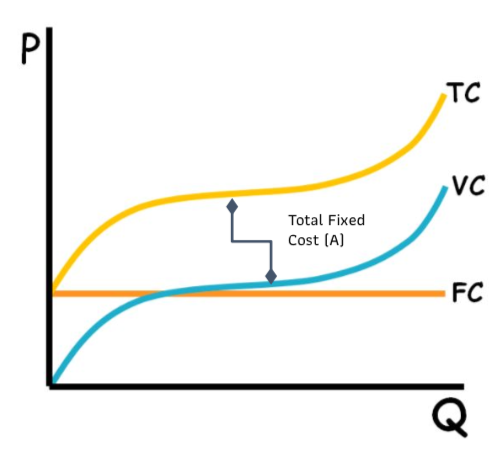

Fixed costs (fc) - costs that cannot be change

Variable costs (vc) - costs that can be changed

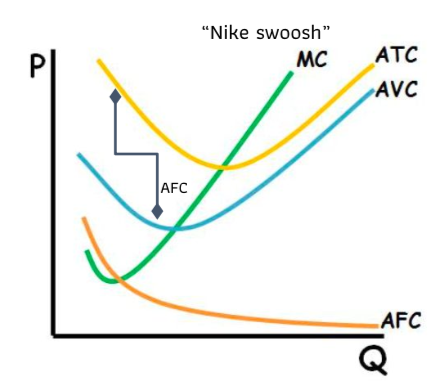

Marginal cost (mc) - the addition cost of staying open one more hour (Stores) or producing one more product

Total cost (tc): fixed + variable costs

Equations

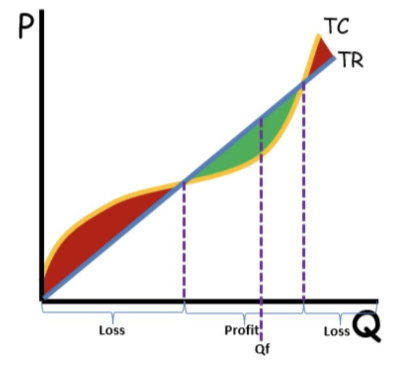

Total revenue - total costs = total revenue

Total costs = tvc + tfc

Average total cost = avc + atc, or tc/q

Marginal cost (MC) = ΔTC/ΔQ

Where marginal costs begin to increase is where the Law of Diminishing Marginal Returns comes into effect for costs.

The Marginal Product Curve is a mirror of the Marginal Cost Curve.

When the marginal product is increasing, marginal cost is falling, and vice versa. (due to specialization)

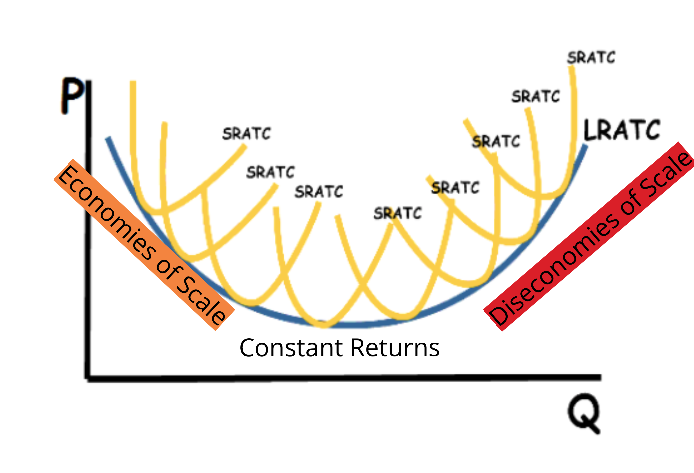

3.3 - Long-Run Production Costs

The long-run average total cost curve (LRATC curve) is the summation of all the short-run ATCs a firm could produce under different firm sizes. It is used to determine how large a firm should optimally be.

Economies of Scale: Downward sloping LRATC, higher quantities have a lower average cost

Doubling inputs triples outputs

Constant returns to scale: LRATC is flat

Doubling inputs doubles outputs

Diseconomies of scale: Upward sloping LRATC

Doubling inputs less than doubles output

the firm is too large and is hard to manage

Efficient scale - The point of lowest possible output at which a firm can minimize long-run average costs and operate efficiently. Occurs at the center or constant returns to scale

3.5 - Profit Maximization

Accounting Profit - Total revenue minus explicit costs only, used by accountants.

Economic Profit - Total revenue minus total costs (both implicit and explicit)

Normal Profit - When Economic Profit = 0, Accounting Profit = Opportunity Costs

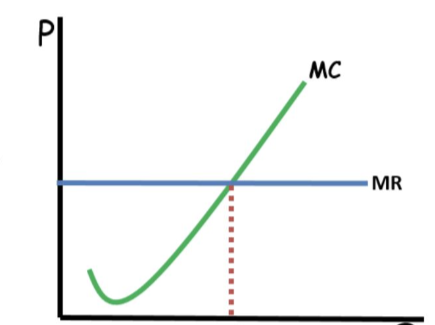

If MC > MR, produce less.

If MC < MR, produce more

If MC = MR is perfect profit maximization, it is the profiting maximizing point

3.6 - Firm’s Short-Run and Long-Run Decisions

Short Run:

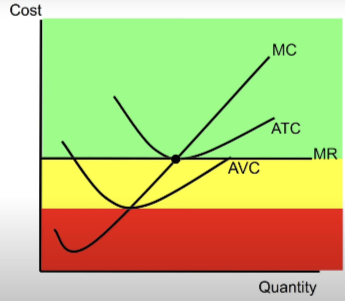

When a business shuts down it still has to pay fixed costs.

Compare: TR/TVC or P/AVC

In the Short Run, a firm will choose to shut-down when the price of the good falls below the average variable cost. (P<AVC)

A firm will choose to operate as long as the price is equal to or greater than the AVC. (P>AVG)

A firm will still stay open when price falls below total costs or fixed costs to minimize loss. (P<ATC)

3.7 Perfect Competition in the Short Run

THIS IS COVERED IN UNIT 4 NOTES, BECAUSE IT FITS BETTER WITH UNIT 4. LINK HERE