Macro Unit 1

1.1 Scarcity

Scarcity - we have unlimited wants but limited resources

Opportunity Cost

Explicit costs - out of pocket expense

ex) money payments or exchange of items of value

Implicit costs - value of resources that could be used elsewhere

ex) resource allocations not item exchange

Positive vs Normative Statements

Positive - based on facts. Avoids value judgements (what is)

Normative - Include value judgements (what ought to be)

5 Economic Assumptions

Society has limited wants and limited resources. (scarcity)

Due to scarcity, choices may be made. Every choice has a cost. (a trade-off)

Everyone’s goal is to make choices that maximize their satisfaction. Everyone acts in their own “self-interest”.

Everyone makes decisions by comparing the marginal cost and marginal benefits of every choice.

Real-life situations can be explained and analyzed through simplified models and graphs.

Marginal Analysis

Marginal = additional

Marginal analysis (aka thinking on the margin) making decisions based on increments

Point: You will continue to do something as long as the marginal benefit is greater than the marginal cost.

Trade offs vs. Opportunity Cost

ALL decisions involve trade-offs

Trade-offs - all the alternatives that we give up when we make a choice

ex: Going to the movies

Opportunity cost - most desirable alternative given up when you make a choice

Economic Terminology

Utility - satisfaction

Marginal - additional

Allocate - distribute

Price vs. Cost

Price - amount buyer (or consumer) pays

Cost - amount seller pays to produce a good

Investment - the money spent by BUSINESSES to improve their production

ex: 1 million dollar new factory

Consumer goods - created for direct consumption

Capital goods - created for indirect consumption

Goods used to make consumer goods

Four Factors of Production

Land - all natural resources that are used to make goods and services

Labor - any effort a person devotes to a task for which that person is paid

Capital

Physical capital - any human made resource that is used to create other goods or services

Human capital - any skills or knowledge gained by a worker through education and experience

Entrepreneurship - ambitious leaders that combine the other factors of production to create goods and services

Profit = revenue - costs

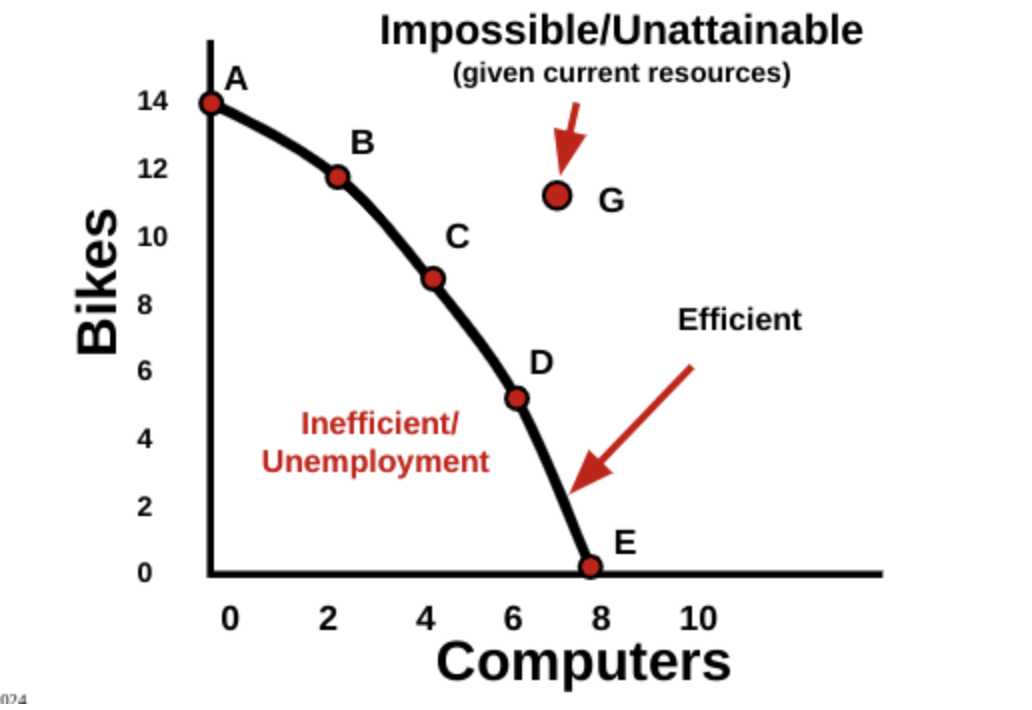

1.2 Opportunity Cost and the PPC

Product possibilities curve (PPC) or frontier, is a model that shows alternative ways that an economy can use its scarce resources

This model demonstrates scarcity, trade-offs, opportunity costs, and efficiency

4 Key Assumptions