Chapter 14-16

AGGREGATE DEMAND (Chapter 14):

AD = total spending on goods + services in a period of time at a given price level

on a graph = Price level v real GDP

lower average price level = high average demand

Long Run Aggregate Demand (LRAD):

AD = C + I + G + (X - M)

C -> consumption

durable vs non-durable goods

I -> investments (producers)

replacement investment vs induced investment

G -> government

X -> exports

M -> imports

Non-price determinants of Consumption:

Income taxes

higher income = higher consumption

higher income tax = lower consumption (less disposable income)

Wealth

change in house prices / value of stocks and shares -> higher = higher consumption

Interest Rates

higher interest rates = less borrowing -> lower consumption

lower interest rates = higher consumption (ceteris paribus)

Consumer confidence / expectations of future

optimistic = higher consumption

consumer confidence index

higher future prices = higher consumption (vice versa)

Debt

easy to borrow money + low interest = higher debt willingness + consumption

hard to borrow money + high interest = lower debt willingness + consumption

acronym: TWICED

Non-price determinants of Investments:

Interest rates

higher interest rate = lower investments

Business confidence

optimistic about future = higher investments

Technology

increase in tech = higher investments

Business taxes

higher taxes = reduced post-tax profits = lower investments

Corporate indebtedness

easy to borrow money + low interest = higher debt willingness + investment

hard to borrow money + high interest = lower debt willingness + investment

acronym: IB-TBC

Non-price determinants of Government Spending:

economic + political priorities

commitment to support industry = higher spending

correct market failure = higher spending

Non-price determinants of Net exports:

change in imports

higher domestic income = higher imports

higher exchange rate = higher imports

lower restrictions on trade = higher imports

lower inflation rates of foreign partners = higher imports

change in exports

increased foreign incomes = higher exports

higher exchange rate of currency = lower exports

lower restrictions on trade = higher exports

higher inflation rate = lower exports

AGGREGATE SUPPLY (Chapter 15):

AS = total amount of goods + services produced by all industries at every given price level

Short Run Aggregate Supply (SRAS):

short run = period of time where FoP do not change

wage / price of labour = fixed

decrease in cost = higher supply

positive relationship between price level and real GDP

Non-price determinants of SRAS:

Cost + availability of resources

wage rates (increase in wages = increase in cost of FoP -> lower AS)

cost of raw materials (higher costs = lower AS)

dependent on how widely used the material is

price of imports (increase in price = higher cost of production -> lower AS)

Government intervention

subsidies (increased subsidies = higher AS)

taxes (increased taxes = lower AS)

regulations (more regulations = lower AS)

Supply shocks

natural disasters

wars / conflicts

Long Run Aggregate Supply (LRAS):

two schools of thought -> Keynesian vs neo-classical

Neo-classical:

efficiency of market

minimal gov intervention

belief in invisible hand

LRAS = perfectly inelastic

full employment level

independent of price level

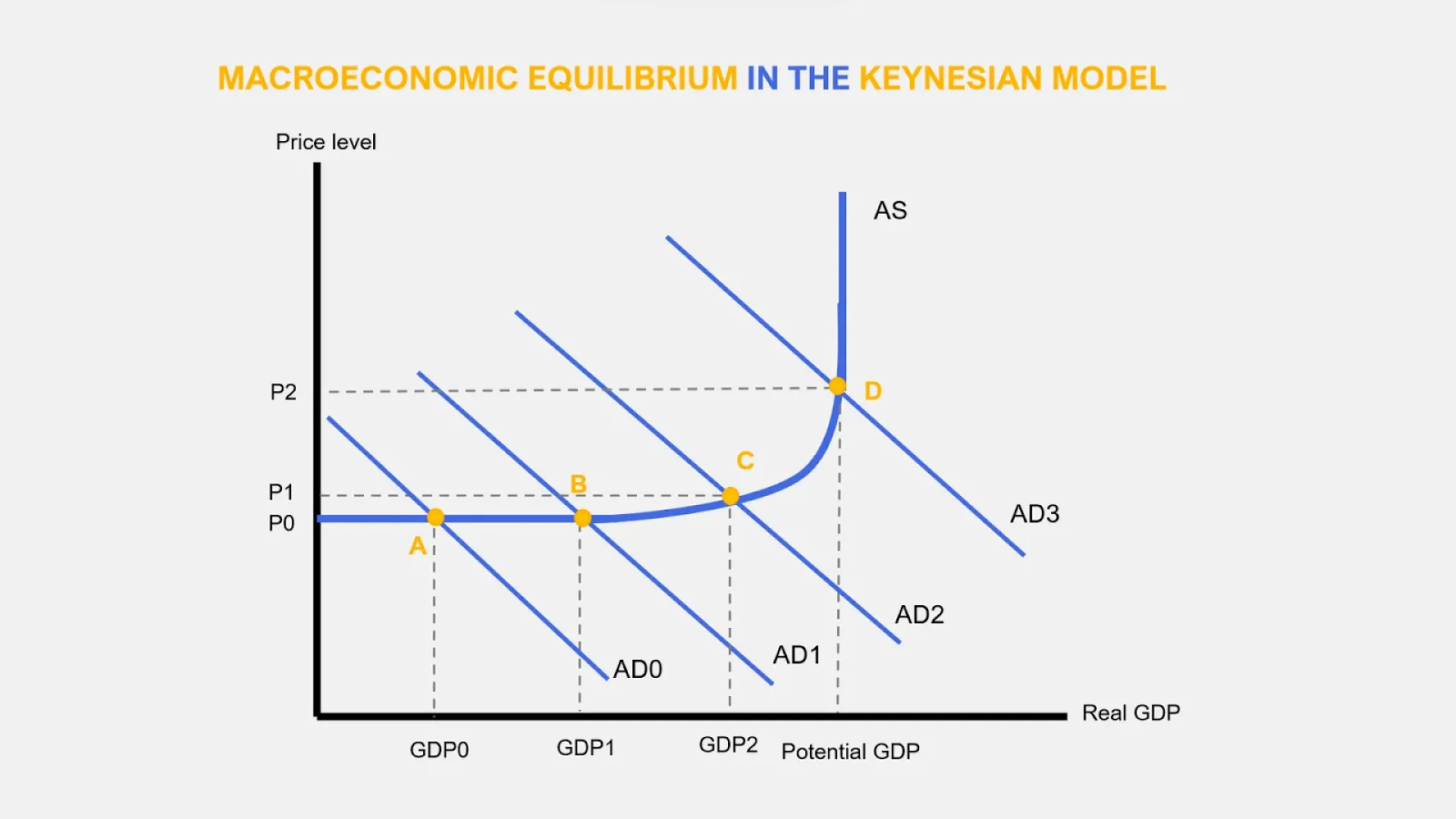

Keynesian view:

1: AS is perfectly elastic

spare capacity

increase output without high costs

2: approaching potential output

use up spare capacity

FoP more scarce

FoP cost more

rising price levels

3: full capacity

impossible to increase output

AS perfectly inelastic

Non-price determinants:

Change in quantity or quantities of FoPs

Technological improvements

Increase in efficiency

Changes in institutions

Factors influencing quality / quantity of FoPs:

MACROECONOMIC EQUILIBRIUM (Chapter 16):

Short run equilibrium

when AD meets SRAS (AD = SRAS)

no incentive for producers to increase output or prices

no inflationary / deflationary pressure

Long run equilibrium

Neo-classical:

AD = LRAS

economy always moves towards LRE without gov intervention

changes to AD only on price level

Recessionary / Deflationary Gap

equilibrium level of real output is less than potential output as result of decrease in AD (assumption = temporary)

Inflationary Gap

equilibrium level of real output is more than potential output as result of increase in AD (assumption = temporary)

Growth / decrease of supply:

Long Run Equilibrium:

short run = inflationary and recessionary gaps exists

long run = equilibrium point must return to LRAS (full employment)

Keynesian:

economy may be in LRE at levels of output below full employment

LRE depends on AD level

AS = perfectly elastic -> spare capacity + unused FoP

equilibrium below full employment level

first shift -> no change in price, only change in output

second shift -> slight inflationary pressure, increased price + output

third shift -> purely inflationary shift, only change in price, no change in output