CH 7: Futures and Options on Foreign Exchange

Future Contracts: Preliminaries

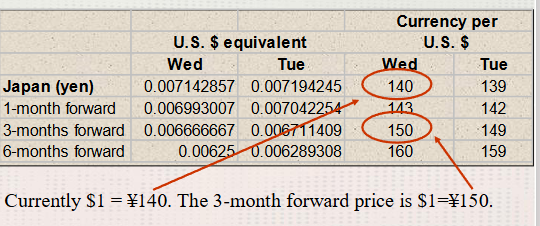

A forward contract is a vehicle for buying or selling a stated amount of foreign exchange at a stated price per unit at a specific time in the future.

Both forward and futures contracts are classified as derivative or contingent claim securities because their values are derived from or contingent upon the value of the underlying security.

A futures contract is like a forward contract: It specifies that a certain currency will be exchanged for another at a specified time in the future at prices specified today.

A future contract is different from a forward contract: Futures are standardized contracts trading on organized exchanges with daily resettlement through a clearinghouse.

Standardizing Features:

Contract Size - specifying the amount of the underlying foreign currency.

Delivery Month - maturity

Daily resettlement

An initial performance bond (Margin) must be deposited into a collateral account to establish a futures position. Either cash or treasury bills may be used to meet the performance bond requirement.

the performance bond put up by the contract holder can be viewes as “Good-Faith” money.

If the investors performance bond account falls below a maintenance performance bond level (Approx. 90% of the initial performance bond), additional funds must be deposited into the account to bring it back to the initial performance bond level, to keep position open.

An investor who suffers a liquidity crunch and cannot deposit addition funds will have their position liquidated.

The major difference between a forward contract and a futures contract is the way the underlying asset is prices for future purchase/sale. Forwards contract states a price for the future transaction, and the profits/losses are realized all at once at maturity. By contrast, a futures contract is settled up or market to market, daily at the settlement price.

Marking-to-market feature of futures markets means that market participants realize their profits or suffer their losses on a day to day basis rather than all at once at maturity.

A higher settlement price means the futures price of the underlying asset has increased in value.

The seller of the futures contract (Short positions) will have his performance bond account increased (or decreased) by the amount the longs performance account is decreased (or increased). Therefore, Futures trading between the long and short is a zero-sum game; the sum of the long and short’s daily settlement is zero.

In SUM, a futures contract is comparable in some aspects to a new forward contract on the underlying asset at the new settlement price with a one day shorter maturity. Because of the daily marking to market, the futures price will converge through time to the spot price on the last day of trading.

Differences between Futures and Forward Contracts

Trading Location:

Futures: Traded competitively on organized exchanges

Forward: Traded OTC via a network of dealers

Contractual Size:

Futures: Standardized amount of the underlying asset

Forward: Tailor made to the needs of the participant.

Settlement:

Futures : Daily settlement, or marking to market, done by the futures clearinghouse through the participants performance bond account.

Forward: Participant buys or sells the contractual amount of the underlying asset from the bank at maturity at the forward (Contractual) price.

Expiration date:

Futures: Standardized delivery dates

Forward: Tailor made delivery the meets the needs of the investor.

Delivery:

Futures: Delivery of the underlying asset is seldom made. Usually a reversing trade is transacted to exit the market.

Forward: Delivery of the underlying asset is commonly made.

Trading Costs:

Futures: Bid-ask spread plus brokers commission

forward: Bid-ask spread plus indirect bank charges via compensating balance requirements.

Two types of market participants are necessary:

Speculators attempt to profit from a change in the futures price. To do this, the speculator will take a long or short position in a futures contract depending upon expectations of future price movement.

Hedgers want to avoid price variation by locking in a purchase price of the underlying asset through a long position in the futures contract or a sales price through a short position. Passes off the risk of price variation to the speculator, who is more willing to bear this risk.

Both forward and future markets are very liquid.

A reverse trade can be made in either market that will close out or neutralize a position.

While futures contracts are useful for speculation and hedging, their standardized delivery dates are unlikely to correspond to the actual future dates when foreign exchange transactions will transpire.

In futures market, a clearinghouse serves as the third party to all transactions. Facilitates active secondary market because the buyer and seller do not have to evaluate one another’s creditworthiness. The clearinghouse liability is limited because a contract holders position is marked to market daily. Clearinghouse maintains the futures performance bond accounts for the clearing members (Individual brokers).

Frequently, a futures exchange may have a daily price limit on the futures price.

Currency Futures Markets

The Chicago Mercantile Exchange (CME) is by far the largest.

Basic Currency Futures Relationships

Open interest refers to the number of short or long contracts outstanding for a particular delivery month in the derivative markets. A good proxy for demand for a contract.

Some refer to open interest as the depth of the market. The breadth of the market would be how many different contracts (expiry month, currency) are outstanding.

Options Contracts: Preliminaries

An Option is a contract giving the owner the right, but not the obligation, to buy or sell a given quantity of an asset at a specified price at some time in the future. Like a future or forward contract, an option is derivative or contingent claim, security.

The buyer of an option is referred to as the long and the seller is referred to as the writer of the option, or the short.

Because the option owner (buyer) does not have to exercise the option if it is not advantageous for them, the option has a price (Premium). Writer receives premium.

There are two types of options, American and European.

A European option can be exercised only at the maturity or expiration date of the contract.

American option can be exercised at any time during the contract.

Currency Options - Preliminaries

An option gives the holder the right, but not the obligation, to buy or sell a given quantity of an asset in the future, at prices agreed upon today.

An option is a derivative, or contingent claim, security.

Options on currency futures behave similarly to options on the physical currency since the futures price converges to the spot price as the futures contract nears maturity.

Calls Vs Puts

Call options gives the holder the right, but not the obligation, to buy a given quantity of some asset at some time in the future, at prices agreed upon today.

Put options gives the holder the right, but not the obligation, to sell a given quantity of some asset at some time in the future, at prices agreed upon today.

European vs. American options

Euro options can only be exercised on the expiration date.

American options can be exercised at any time up to and including the expiration date.

Since the option to exercise early on American options makes it worth more than Euro.

In the money - The exercise price is less than the spot price of the underlying asset.

At the money - The exercise price is equal to the spot price of the underlying asset,

Out of the money - The exercise price is more than the spot price of the underlying asset.

Intrinsic Value - The difference between the exercise price of the option and the spot price of the underlying asset.

Speculative Value - The difference between the option premium and the intrinsic value of the option.

Currency Options Pricing Relationships at Expiry

At expiration, a European option and an American option (not previously exercised), both with the same exercise price, will have the same terminal value.

Currency options are an option on a currency futures contract.

Exercise of a currency futures option results in a long futures position for the holder of a call or the writer of a put.

Exercise of a currency futures option results in a short futures position for the seller of a call or the buyer of a put.

If the futures position is not offset prior to its expiration, foreign currency will change hands.

The difference between the option premium and the options intrinsic value is nonnegative and is sometimes referred to as the options time value.

Summary

Derivatives value is “derived” or contingent on an underlying asset, like stocks or bonds. Futures, options, or forward contracts are derivatives.

Forward and futures contracts serve similar purposes but forwards have custom contracts sizes and maturities, futures contracts are standardized and exchange traded.

Futures contracts are marked to market daily.

A futures market requires hedgers and speculators to operate efficiently

Options on spot foreign exchange are traded on the Philadelphia exchange, options on currency futures on the CME.

The interest parity relationship is used to price currency futures and forward contracts.

Forward, Futures, and options contracts are derivative, or contingent claim securities. That is, their value is derived or contingent upon the value of the asset that underlies these securities.

The CME Group is the largest currency futures exchange.

Exchange traded options with standardized features are traded on two exchanges. Options on spot foreign exchange are traded at the NASDAQ, options on currency futures are traded at the CME.