Ch.11 Understanding Accounting

~11.1 - Accounting + acc. Info~

- Accounting: system for collecting and communicating financial information

- measures business performance and translates findings into information for management decisions

- Bookkeeping: records of taxes paid, income received, and expenses incurred

- Users of accounting information are numerous:

- Business managers use acc. info to set goals, develop plans, and set budgets

- employees and unions use accounting info to get paid and to plan for receive benefits like health care

- investors and creditors: estimate returns to shareholders and to determine tax liabilities of individuals and businesses, ensure amounts are paid on time

- Controller/Chief accounting officer: manages firm’s accounting activities by ensuring that AIS provides reports and statements needed for planning/decision making/other management activities

~Financial vs Managerial accouting~

- can be distinguished by users they serve: those outside the company and those within

~financial accounting~

- accounting system: process in which interested groups are kept informed about financial condition of a firm

- concerned with external users of info like consumer groups, unions, shareholders, and government agencies

- companies prepare + publish income statements and balance sheets at regular intervals

- all documents focus on activities of company as a whole, rather than on individual departments or divisions

~managerial accounting~

- internal procedures that alert managers to problems and aid them in planning and decision making

- serves internal users

- managers at all levels need info to make decisions for their department/ monitor current projects/ plan future events

- to set performance goals:

- salespeople: need data on past sales by geographic regions

- purchasing agents: use info on material costs to negotiate terms with suppliers

~Professional Accountants~

- chartered professional accountant: banner (designation) that is being used to unify the accounting profession in Canada

~Chartered Accountants~

- to achieve designation, must have a uni degree, complete an educational program, and pass national exam

- focus on external financial reporting, so certifying the true financial condition of the firm for various interested parties (shareholders, lenders, etc.)

~Certified General accountants~

- to become a CGA

- complete an education program + pass national exam

- must also have an accounting job within a company

- Can audit corporate financial statements in most provinces

- most work in private companies, but there are a few CGA firms

- also, focus on external financial reporting

~Certified Management Accountants~

- to get designation

- must have a uni degree, passed two-part entrance exam, completed strategic leadership program while gaining practical experience in management accounting environment

- work in organizations of all sizes and focus on applying best management practices in all operations of business

- CMAs bring a strong market focus to strategic management and resource deployment

- synthesizing and analyzing financial and non-financial info to help organizations maintain competitive advantage

- emphasize the role of accountants in the planning and overall strategy of the firm in which they work

~Accounting Services~

~Auditing~

- accountants examine the company’s AIS to ensure it follows prescribed accounting rules

- involves examination of receipts such as shipping documents, cancelled cheques, payroll records, and cash receipt record

- may physically check inventories, equipment, or other assets

- at the end of audit, auditor will certify whether clien’’s financial reports comply with accounting rules

~International accounting standards~

- International financial reporting standards: were developed b/c users of financial information want assurances that accounting procedures are comparable from country to country

- aka: GLOBAL GAAP

- used by more than 140 countries

- IASB financial statements require an income statement, balance sheet, and statement of cash flows

~detecting fraud~

- forensic accountants may be used to track down hidden funds in business firms

- look behind the behind the corporate walls instead of accepting financial records at face value

- may be called upon by law enforcement agencies, insurance companies, law firms, and business firms

- fraud examiners interview high-level executives , pursue tips from employees or outsiders, and search through emails looking for supscious words/phrases

~Tax services~

- helping clients with preparing tax returns and tax planning

~management consulting services~

- range from personal financial planning to planning corporate mergers.

- plant layout and design

- marketing studies

- production scheduling

- computer feasibility studies and design implementation of accounting systems

- some CA firms assist in executive recruitment

~PRIVATE ACCOUNTANTS~

- are salaried employees who deal with company’s day-to-day accounting needs

- large businesses employ specialized accountants in areas such as budgets, financial planning, internal auditing, payroll, and taxation

- work of private accountants varies, depending on nature of specific business and activities needed to make business a success

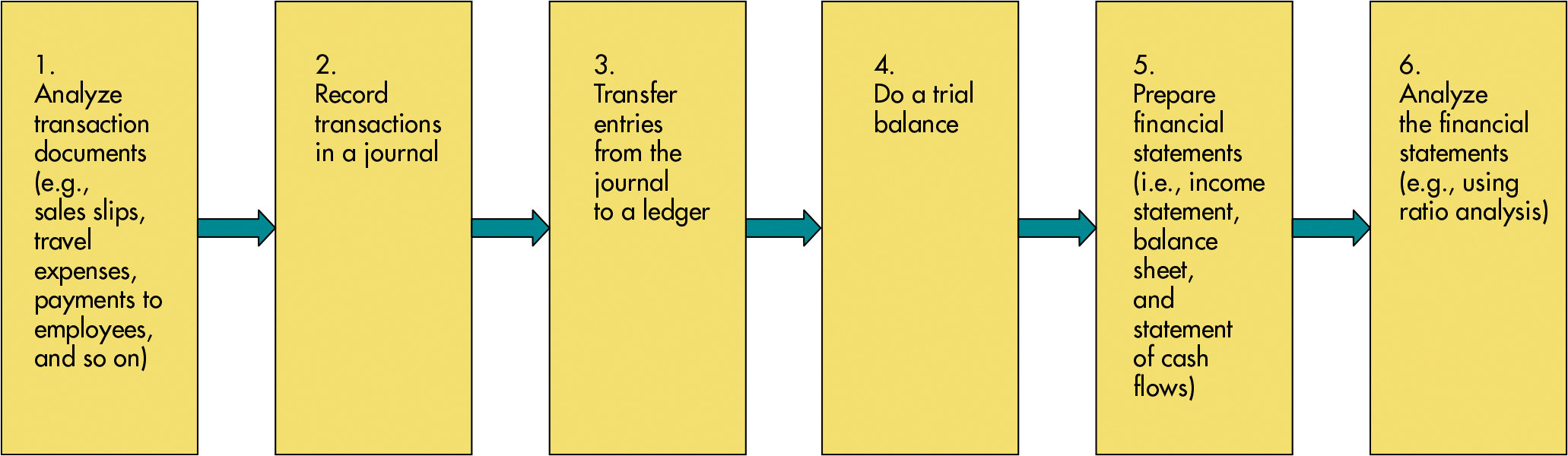

~accouting cycle~

- Private accountants use a six-step process to develop and analyze company’s financial reports

- analyze data generated from company’s regular business operations (sales, income tax payments, etc.)

- transactions are recorded in journal

- then transferred into a ledger (shows increase/decrease in various asset, liability, and equity accounts)

- legder amounts for each account are listed in trial balance (assesses accuracy of cash flows)

- financial statements (balance sheet, income statement, and statement of cash flows) are prepared

- analyzing financial statements

`

`

~11.2 Accounting Equation~

- __ASSETS = LIABILITIES + OWNER’S EQUITY__

- Used to balance the data pertaining financial transactions

~Assets and Liabilities~

- Asset: economic resource that’s expected to benefit firm or individual who owns it

- Liability: debt that the firm owes to an outside party

~Owner’s Equity~

- Owner’s Equity: amount of money received from selling all assets and paying off liabilities

- __ASSETS - LIABILITIES = OWNER’S EQUITY__

- if company’s assets exceed its liabilities, then the owner’s equity is positive

- if company goes out of business, the owner’s will receive some cah after selling assets and paying off liabilities

- if company’s liabilities exceed its assets, owner’s equity is negative

- assets will not be enough to pay off debt

- Consists of two sources of capital:

- Amount owners originally invested

- profits earned by and reinvested in the company

- when company operates profitably, its assets increase faster than liabilities

- owner’s equity will increase if profits are retained in business instead of paid out as dividends to shareholders

- will increase if owners invest more of their own money to increase assets

~11.3 financial statements~

- if business purchases inventory with cash, then cash decreases but inventory increases

- if business purchases inventory on credit, then inventory increases and amounts payable

- since each transaction affects two accounts, DOUBLE ENTRY ACCOUNTING SYSTEMS are used to record the dual effects of financial transactions

- these transactions are reflected in three important FINANCIAL STATEMENTS

- balance sheets

- income statements

- statements of cash flows

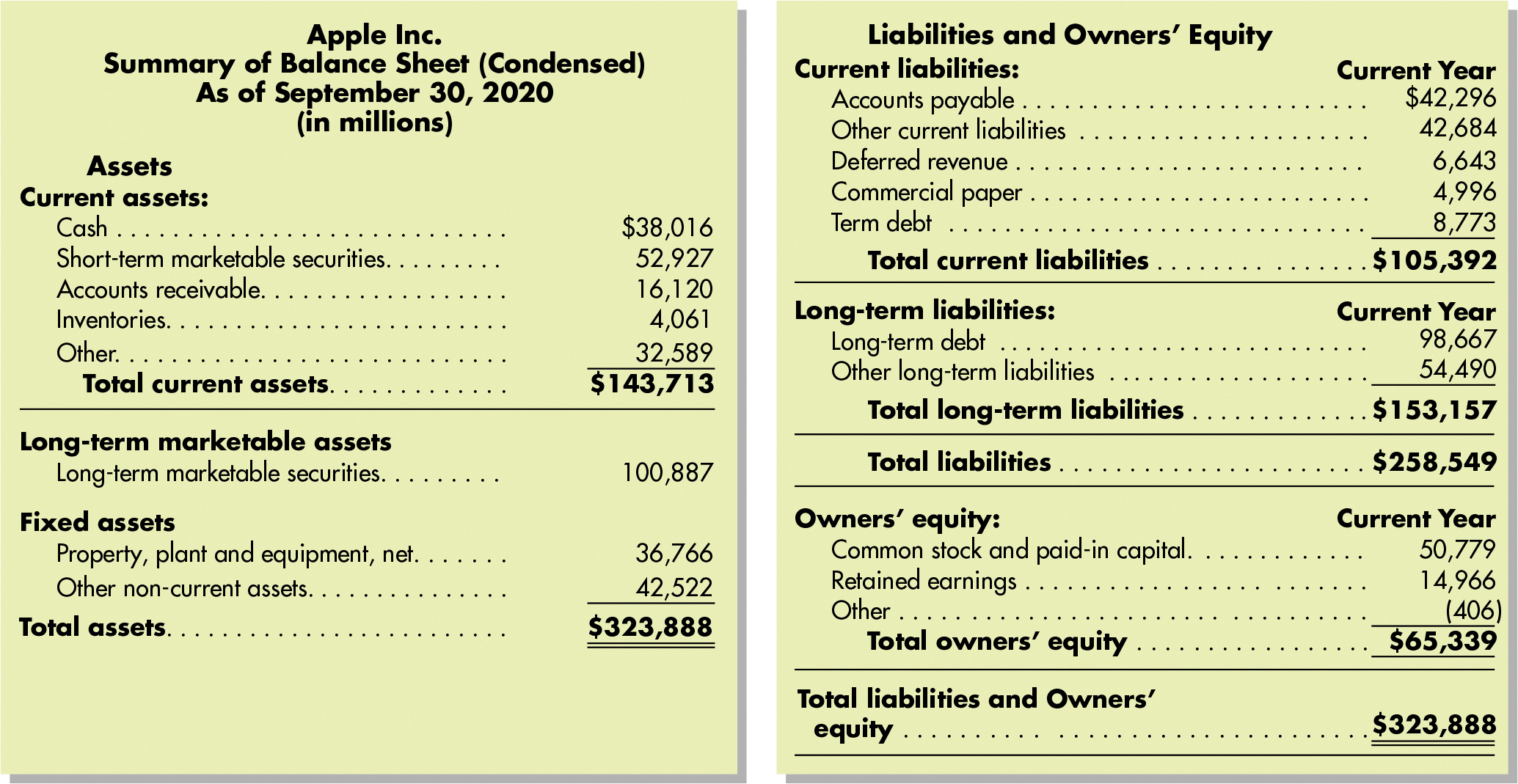

~Balance sheets~

- have detailed info about accounting equation factors: assets, liabilities, and owner’s equity

- shows financial condition at a specific point in time

~assets~

~assets~- three types of assets exist

- current

- fixed

- intangible

~Current assets~

- include cash, money in the bank, and assets that can be converted into cash within a year

- act of converting something into cash is called LIQUIDATING

- assets are listed in order of liquidity

- cash is completely liquid

- Marketable securities: purchased as short-term investments are slightly less liquid but can be sold quickly

- include stocks or bonds of other companies, government securities, and money market certificates

- Non-liquid assets

- Merchandise inventory: is a non-liquid asset, the cost of merchandise that’s been acquired for customers and is still on hand

- Prepaid expenses: supplies on hand and rent paid for the period to come

~Fixed Assets~

- have long-term use or value to the firm (land, buildings, equipment)

- as buildings/equipment become worn out, their value drops/depreciates

- DEPRECIATION: determining an asset’s useful life in years, dividing its worth by that many years, and then subtracting the resulting amount each year

- asset’s remaining value, therefore, decreases each year

~Intangible assets~

- worth is hard to set, intangible assets have monetary value

- usually include cost of obtaining rights or privileges like patents, trademarks, copyright, and franchise fees

- GOODWILL: amount paid for an existing business beyond the value of its other assets

~Liabilities~

- CURRENT LIABILITIES: debts that MUST be paid within a year

- include accounts payable (unpaid bills/wages/taxes)

- LONG-TERM LIABILITIES: debts that are not due for at least one year

- represent borrowed funds on which company must pay interest

~Owners’ Equity~

- RETAINED EARNINGS:

- accumulate when profits, which could have been distributed to shareholders, are kept instead for use by the company

~Income Statements~

- aka “profit-and-loss statement”

- __REVENUES - EXPENSES = PROFIT/LOSS__

- profit or loss (bottom line)

- shows financial results that occurred during a period of time (month, quarter, or year)

- Divided into 3 categories

- REVENUES

- funds that flow into a business from the sale of goods/sevices

- revenue recognition: recording + reporting of revenues in financial statements

- earnings are not reported until reporting cycle has completed

- matching principle: expenses matched with revenues to determine net income for an accounting period

- is important b/c it permits the user of the statement to see how much net gain resulted from assets that had to be given up to generate revenues during period covered in the statement

- COSTS OF GOODS SOLD

- shows the costs of obtaining materials to make products sold during the year

- Gross profit (gross margin): to calculate →

- for companies with low gross margins, it probably has low cost of goods sold but high selling and administrative expenses

- OPERATING EXPENSES

- resources that must flow out of a company for it to earn revenues

- **__selling expenses: __**salaries, delivery costs, + advertising expenses

- general/administrative expenses: management salaries, insurance expenses, + maintenance costs

- operating income: compares gross profit from business operations against operating expenses

- net income:

~STATEMENTS OF CASH FLOWS~

- describes a company’s yearly cash receipts and cash payments

- CASH FLOWS FROM OPERATIONS: concerned with firm’s main operating expenses like cash transactions involved in buying and selling goods/services

- reveals how much of year’s profits result from firm’s main line of business (sales of cars)

- CASH FLOWS FROM INVESTING: net cash used in/provided by investing

- cash receipts + payments from buying/selling stocks, bonds, property, equipment, other productive assets

- CASH FLOWS FROM FINANCING: net cash from all financing activites

- cash inflows from borrowing/issuing stock

- outflows for payment of dividends/repayment of borrowed money

~the budget: an internal financial statement~

- BUDGET: detailed report on estimated receipts and expenditures for a future period

~11.4 analyzing financial statements~

- statements provide data which can be used to compute solvency, profitability, and activity ratios that are useful in analyzing financial health of a company

- ratios are grouped into three major classifications:

- solvency ratios for estimating short-term/long-term risks

- profitability ratios for measuring potential earnings

- activity ratios for evaluating management’s use of assets

~SOLVENCY RATIOS: BORROWER’S ABILITY TO REPAY DEBT~

- measures firm’s ability to meet its debt obligations

~short term solvency ratios~

- measure a company’s liquidity and its ability to pay immediate debts

- current ratio: company’s ability to generate cash to meet obligations by selling inventories and collecting revenues from customers

- calculated by

- the higher the ratio, the lower the risk it represents to investor

~long-term solvency~

- stakeholders are concerned with this

- calculated by

- if debt-to-equity is higher than 1.0, company may be really too much on debt

- sometimes high debt can not only be acceptable, but desirable

- borrowing funds gives firm leverage - ability to make otherwise unaffordable investments

- in leveraged buyouts, firms have sometimes taken on huge debt to get money to buy out other companies

- if owning purchased company generates profits above cost of borrowing purchase price, leveraging makes sense

~PROFITABILITY RATIOS: EARNINGS POWER FOR OWNERS~

- measures firm’s overall financial performance in terms of its likely profits, used by investors to assess their probable returns

~return on equity~

- net income earned by a business for each dollar invested

- calculate:

~return on sales~

- firms want to generate as much profit as they can from each dollar of sales revenue they receive

- calculate:

~earnings per share~

- calculate:

- influences the size of dividend a company can pay its shareholders

- investors use this to figure out whether or not to sell stock

~activity ratios: how efficiently is the firm using its resources~

- measures how efficiently a firm uses its resources; used by investors to assess their probably returns

- important activity ratio: inventory turnover ratio → calculates average number of times that inventory is sold and restocked during the year

- calculation: @@cost of goods sold divided by average inventory (beginning of year + end of year inventory / 2)@@

~11.5 accounting ethics~

- responsibilities as a professional

- serving the public interest

- maintaining integrity

- being objective and independent

- maintaining technical and ethical standards

- professional conduct in providing services