Chapter 6: Demand, Supply, Market Equilibrium, and Welfare Analysis

Demand

- Simple concept- people purchase less when prices are high and vice versa

Law of Demand

- Ceteris paribus means holding everything else constant

- There is an inverse relationship between quantity demanded and prices

| ]]Price per cup($)]] | ]]Quantity Demanded]] |

|---|---|

| .25 | 120 |

| .50 | 100 |

| .75 | 80 |

| 1.00 | 60 |

| 1.25 | 40 |

- For simplification of the demand model, we assume all other things as constant

Reasons for the Law of Demand (why people buy less when price increases)

- Income effect: when prices are low, people are easily able to afford it since their budget would allow it

Imagine having a budget of $10, and you are able to buy a limited quantity of apples

Now if your income increases, your budget increases by more than 10, which allows you to buy more of the apples

- Substitution effect: when products price increase, they tend to increase in relative to other products

2 products exist in the market A and B, where B is a substitute product for A

If product A were to become expensive, product B would most likely be cheaper than A

Due to the existence of substitutes, customers immediately leave product A for B

- Diminishing marginal utility: As more units of a product are consumed, the satisfaction/utility it provides tends to decline

- Apple users would purchase at maximum, a limited phones-they wouldn’t purchase a new iPhone every month since that extra phone would offer them no utility or not as much

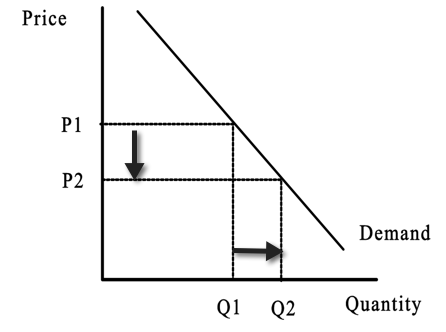

Quantity Demanded vs. Change in Demand

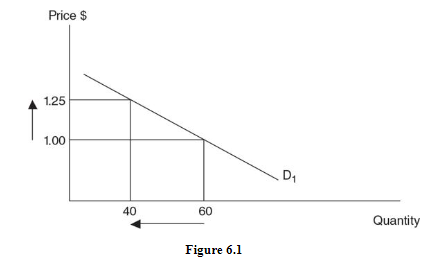

- Change is the quantity demanded only occurs due to change in price of a product

- If product X would become expensive (1.00 to 1.25), the quantity demanded would fall (60 to 40)

- Change in demand occurs when the entire demand curve shifts upwards or downwards due to specific factors

- Change in demand occurs irrespective of price changes of the product

Determinants of Demand

- Consumer income

- Price of substitutes

- The price of a complementary good

- Consumer tastes and preferences

- Consumer expectations about future prices

- Number of buyers in the market

1. Consumer income

- Goods are usually categorized into 2 types, inferior and normal

- Demand tends to decline (shift downwards) for inferior goods with an increase in consumer income

- Demand for normal goods increases (shifts upwards) with an increase in consumer income

- A good example of this would be how college students purchase used furniture (higher demand) at the beginning of their semesters

- The same students however go for the purchase of new furniture once they graduate/ or are employed

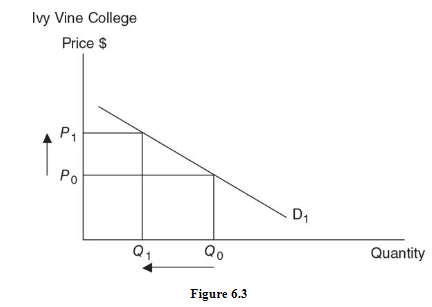

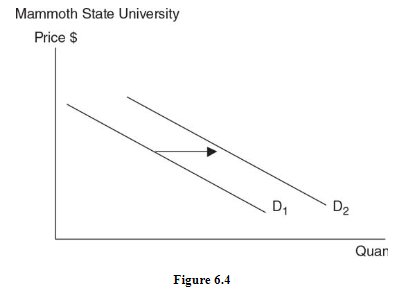

2. Price of substitute goods

- Substitutes goods are products that a consumer can use as alternates to satisfy the same essential function, yielding the same degree of happiness (utility)

- 2 goods would be considered substitutes if an increase in the price of one good causes an increase in demand for the other good

- Assuming 2 institutes only exist in the market: Mammoth State University (MSU) and Ivy Vine College (IVC)

- In an effort to generate more revenue, IVC raises fee per student which in turn leads to counter effects (see below)

- Automatically, IVC faces a decline in demand while MSU faces increase in demand

3. Price of Complementary Goods

- Complementary goods are those which are purchased separately but used together

- The consumer receives more utility from consuming them together than consuming each separately

- The relation here is inverse of that of substitute goods

- If 2 products are complements, an increase in the price of one good causes demand for the other good to decline as well

- A good example would be of tortilla chips and the nacho sauce

- Both products are purchased together, and not individually

4. Tastes and Preferences

- This is the consumer’s taste for a product at any point

- If consumers like a product, the demand curve for that product shifts upwards and vice versa if they dislike it

- A good example is when the trend of vegetarianism hit the public, the consumption of plant-based food drastically increased

5. Future Expectations

- Consumer expectation plays a major role in the determination of the price

- if consumers expect that the price of something would increase in the future, they would buy the product at a larger scale leading to the demand curve shifting upwards

- A good example would be when consumers assume that gasoline prices may raise tomorrow by a certain percentage

- This would result in them filling up more gasoline in the day prior to overcome future trouble

- Demand can also be influenced by future expectations of income changes

6. Number of Buyers

- Increase in the number of buyers leads to an increase in demand (keeping everything else constant)

- This is usually due to demographic changes or increasing availability in more markets

- A good example would be after the abolishment of communism in USSR, many US based companies entered into Russia with their products, hence a new market with new consumer base

Supply

- The market supply shows the quantity a supplier is willing and able to offer at various prices at a given time

Law of Supply

- Law of supply states that when prices increase, the supply increases (while holding everything else constant)

- This proves a direct relationship between price and supply

Behind the scenes of the law of supply

Increasing Marginal Costs

- As suppliers increase the number of units supplied, they face increasing marginal cost

- In conclusion, they would only supply up to the quantity which allows them to at least cover their high marginal cost

The Supply Curve

- The table above is sometime referred to as supply schedule

| ]]Price per cup ($)]] | ]]Quantity supplied]] |

|---|---|

| .25 | 40 |

| .50 | 60 |

| .75 | 80 |

| 1.00 | 100 |

| 1.25 | 120 |

Quantity Supplied Versus Supply

- Change is the quantity supplied only occurs due to a change in the price of a product, holding all other factors constant

- Change in supply occurs when the entire supply curve shifts upwards or downwards due to specific factors

- Increase in supply is viewed as a rightward shift in the supply curve and vice versa

- Change in supply occurs irrespective of price changes of the product

Determinants of Supply

- The cost of an input to be used in the production

- Technology and productivity used to produce

- Taxes or subsidies

- Producer expectations about future prices

- The price of other goods that could be produced

- The number of producers in the industry

1. Cost of Inputs

- The cost of production (land, labor, capital) has an inverse impact on the supply

- When the cost of these increases, the supplier decides to produce less of the products since he is unable to afford the production cost

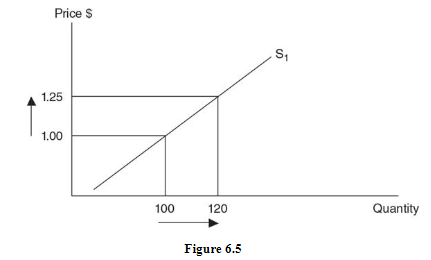

2. Technology or Productivity

- Newer technology causes the cost of production (reduces the marginal cost) to decline and helps improve the efficiency of the supplier

- This allows the supplier to produce more, shifting the supply curve outwards(towards the right)

- Flow production techniques, where similar products are produced in one go are preferred by suppliers as the marginal cost is reduced and supply can be increased

3. Taxes and Subsidies

- Taxes are added up to the unit cost of production, thus making it more expensive

- Due to this, heavily taxed products are produced in less quantity by suppliers(supply curve shifts towards the left)

- Subsidies are the opposite of taxes and help reduce price per unit

- This allows suppliers to produce more of the product(supply curve shifts towards right)

4. Price Expectations

- Producers’ willingness to supply depends greatly on future prices as well

- If a juice producer assumes that heat waves tomorrow would reduce the number of people coming out of their houses, he would hold back some of his supply

- If the same producer is aware that a marathon would be taking place on a particular date, he would supply more on that particular day at an inflated price

5. Price of Other Outputs

- Suppliers can use the same resources for production of 2 goods

- If the demand for let’s say milkshake rises, the supplier would reduce his supply of ice cream and shift towards selling more of milkshake

6. Number of Suppliers

- As the number of sellers increases in the market, the supply automatically increases

- This allows consumers more choices at a lower price due to an increase in competition

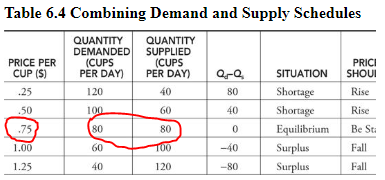

Market Equilibrium

- Consumers prefer lower prices whereas suppliers prefer higher prices

- Market is in a state of equilibrium when the quantity supplied equals the quantity demanded at a given price

- It is where the price expected by consumers is equal to the price required by suppliers

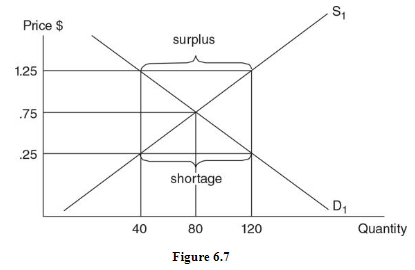

| Price per cup ($) | Quantity demanded | Quantity supplied | Qd-Qs | Situation | Price should |

|---|---|---|---|---|---|

| .25 | 120 | 40 | 80 | Shortage | rise |

| .50 | 100 | 60 | 40 | shortage | rise |

| {{.75{{ | {{80{{ | {{80{{ | 0 | equilibrim | Same |

| 1.00 | 60 | 100 | -40 | surplus | fall |

| 1.25 | 40 | 120 | -80 | surplus | fall |

Shortage

- A shortage exists at a market price when the quantity demanded exceeds the quantity supplied

- At prices of 25 cents and 50 cents per cup, you can see the shortage in the figure above

- Suppliers don’t prefer lower prices and therefore decrease their quantity supplied.

- At prices below 75 cents per cup, lemonade buyers and sellers are in a state of disequilibrium

- With a shortage in the market, consumers become willing to pay slightly more which in turn allows suppliers to produce more

- Hence the shortage is eliminated at a price of 75 cents per cup

Surplus

- A surplus exists at a market price when the quantity supplied exceeds the quantity demanded

- At prices of $1 and $1.25 per cup, you can see the surplus in the figure above

- Consumers don’t wish to purchase more lemonade but suppliers are willing to supply more

- Hence the market is in disequilibrium state

- To overcome this, suppliers begin offering discounted prices which helps them overcome the problem

- Hence the surplus would be eliminated at a price of 75 cents per cup

- {{Note: Shortages and surpluses are relatively short-lived in a free market as prices rise or fall until the quantity demanded again equals the quantity supplied{{

Changes in Demand

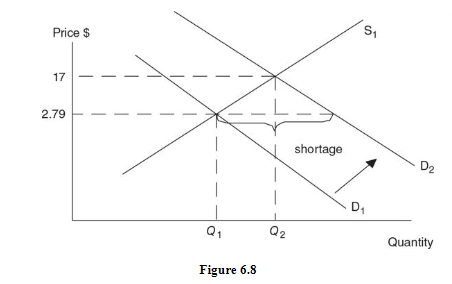

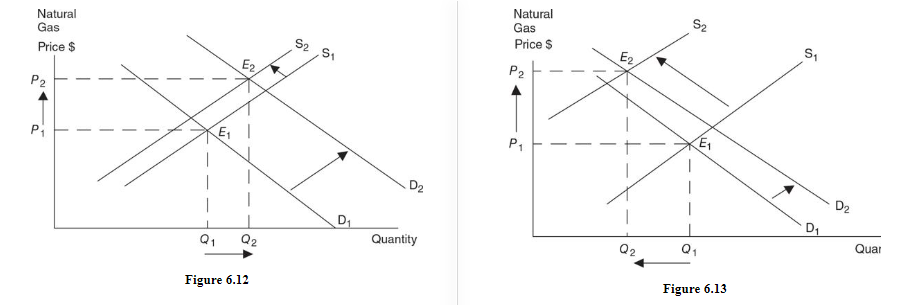

Increase in Demand

- As demand increases from D1 to D2 but supply stays constant, a shortage is created in the market

- Take an example the government suddenly announces that gasoline prices would drop greatly

- This would result in huge influx of demand, giving limited time for suppliers to cope with

- This creates shortage in the market with high gasoline demand but not enough supplied

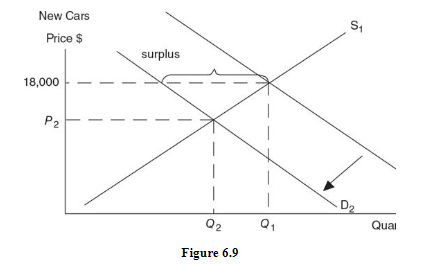

Decrease in Demand

- As demand decreases from D1 to D2 but supply stays constant, a surplus is created in the market

- Take an example that fruit prices hike up greatly in an economy

- This would drop the quantity demanded for the fruits greatly, rendering most of the fruit stored to be useless

- This creates excess in the market with great quantity of fruits supplied but not enough demand

- When demand increases, equilibrium price and quantity both increase

- When demand decreases, equilibrium price and quantity both decrease

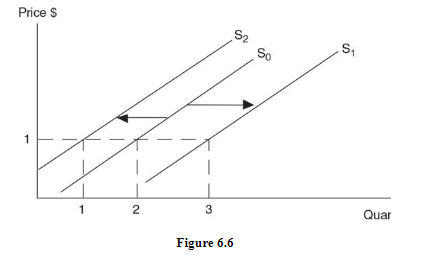

Changes in Supply

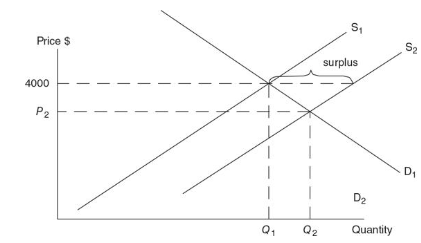

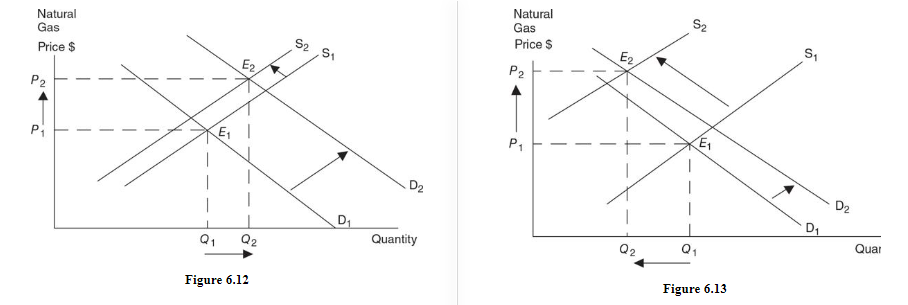

Increase in Supply

- Advancements in computer technology and production methods increases supply greatly

- At equilibrium price of $4,000, there is now a surplus

- To eliminate the surplus, the market price must fall to P2 and the equilibrium quantity must rise to Q2

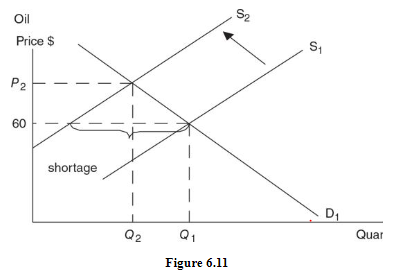

Decrease in Supply

- Assume a decrease in the global supply of oil

- At equilibrium price of $60 per barrel, there is now a shortage of crude oil

- The market eliminates this shortage through higher prices temporarily and the equilibrium quantity of crude oil falls

- When supply increases, equilibrium price decreases and quantity increases

- When supply decreases, equilibrium price increases and quantity decreases

Simultaneous changes in Demand and Supply

- When both demand and supply are changing, one of the equilibrium outcomes (price or quantity) is predictable and one is unpredictable

- Before combining the two shifting curves, predict changes in price and quantity for each shift, by itself

- The variable that is rising in one case and falling in the other case is your ambiguous prediction

Welfare Analysis

- Total Welfare

- Total welfare= consumer surplus + producer surplus

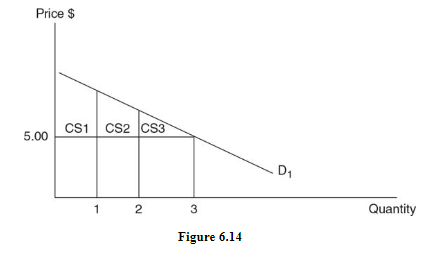

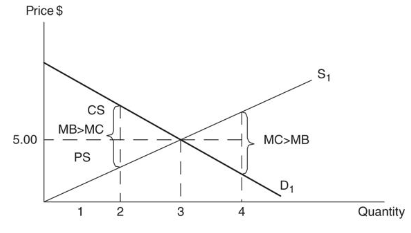

- Consumer Surplus

- consumer surplus, the difference between the price consumers are willing to pay and the price you actually pay for a product

- At a price of $5, three units of the good are purchased.

- First 2 units receive consumer surplus as the price being willingly paid for exceeds $5.

- The third unit pays a price exactly equal to his willingness to pay so he earns no consumer surplus.

- Total consumer surplus is the total amount earned by these three consumer together

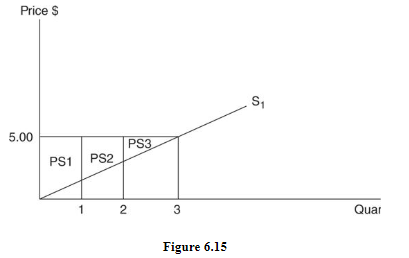

Producer Surplus

- It is the difference between the price received and the marginal cost of producing the good

- The first two units earn producer surplus because $5 is above the marginal cost

- The third unit earns no additional producer surplus, since the marginal cost is exactly equal to the price received by supplier

- Total producer surplus is the total amount earned by these three producers.

- The area under the demand curve and above the market price is equal to total consumer surplus

- The area above the supply curve and below the market price is equal to total producer surplus

- Welfare would be maximized at equilibrium level

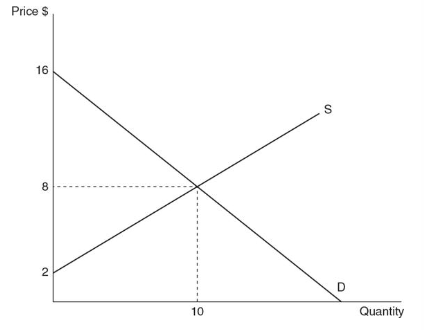

- Use area of triangle (1/2 x base x height) to calculate producer and consumer surplus

- Consumer surplus: ½ x 10 units wide x 8 units long = $40 surplus

- Producer surplus: ½ x 10 units wide x 6 units long = $30 surplus