Week 4 - Sources of value

Major Strategic Investment Decisions

Definition: Large-scale decisions impacting long-term company structure.

Characteristics:

Involves substantial financial investments.

Influences future company dynamics.

Difficult cash flow projections.

Management Involvement: Top-tier management handles these decisions; rarely delegated to junior staff.

Information Dependence: Senior management depends heavily on data from proposers, often presented uncritically.

Risks: Investment proposals often lack thorough discussion of potential risks or alternatives (since presented as sales documents), muddying decision-making.

Behavioural Biases in Investment Decisions

Investment Decision Uncertainty: High uncertainty plays a critical role in forecast reliability.

Bias Awareness: Financial managers must be vigilant of incomplete information that may present a biased perspective.

Key Biases:

Overconfidence Bias: Underestimating project risks due to inflated forecasting confidence.

Optimism Bias: Incorrectly positive outlook on projected cash flows.

Avoiding Forecast Errors

Forecast Limitations: Even unbiased forecasts can include substantial errors, leading to misjudgment of project viability.

Average error will be 0, but you want to accept projects with superior profitability.

Market Value Insight: To avoid being misled by inaccurate forecasts, managers should assess the asset's market value in a competitive market..

Competitive Market Reflections: Understanding why your return exceeds competitors' returns is crucial.

Market Values and Smart Investing

Investment vs. Financing: Profitable investments strategies outperform profitable financing strategies.

Calculating NPVs: NPV calculations are essential yet sometimes flawed due to erroneous cash flow forecasts.

Avoiding Error Dependency: Basing decisions on flawed DCF analyses is risky; start with market asset prices and evaluate their worth in your context.

Competitive Advantage and Positive NPVs

NPV Calculations: Projects gain positive NPVs when they cultivate competitive advantages.

Expected Returns: Under competition, firms generally earn rates aligned with capital costs without competitive advantages. NPV = 0.

Positive NPV only arise when company has a competitive advantage that allow to earn more than the cost of capital.

Economic Rents: Positive NPVs signify the presence of economic rents, meaning actual gains outstrip minimum returns, keep a resource employed in its current use.

Considerations Regarding Rivals

Competitive Surveillance: Speculate on rivals’ responses to your investment strategies, not passively watching.

Marketplace Questions:

Duration of competitive lead over other rivals?

Potential pricing impacts at market saturation, losing competitive lead?

Rivals' possible reactions to my move (cut prices or imitate us)?

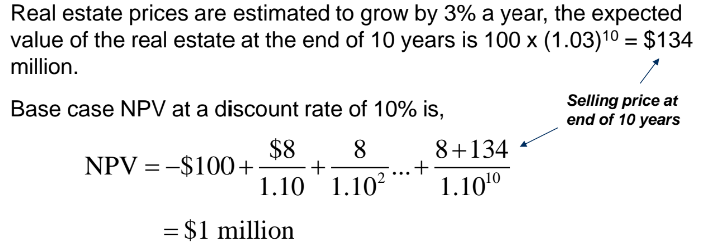

Case Study: Investing in a New Department Store

Investment Outline: Significant cash flow expectations from multiple stores; reliant on real estate pricing.

Financial Evaluations:

Costs, cash flow generation, and projected sales figures impact decisions.

E.g., real estate costs ($100 million) are balanced against after-tax cash flow ($8 million/year).

Ending property value estimations influence NPV projections significantly, e.g. a selling price of 120 could have a negative NPV.

Case Study Implications (Page 11)

Strategic Analysis: A real estate subsidiary and retail operation’s effective rent charge should reflect capacity efficiency.

Market Evaluation: Understanding whether assets are best suited for retail versus alternative usage is critical.

Dynamic Economic Rents: Continuous reassessment to ensure sustained competitive advantage over time.

Case Study: Gold Mining Investments

Project Comparisons: Consideration of initial cost against projected commodity prices and operational costs.

Risk Modeling: Anticipated market price fluctuations and operational viability crucial for making informed investment decisions.

Final Evaluation: Assessing project parameters against current and future market trends to ensure accurate predictive analysis.

Competitive Advantage Translates into Positive NPVs

Financial managers should ask whether an asset is worth the risk associated with its potential return, considering both historical performance and future projections.

Assets are expected to earn their opportunity cost of capital.

If assets earned more, firms would expand or firms outside industry would enter.

A positive NPV is credible only if the company has some special advantage.

Calculation of positive NPV should no the accepted at face value.

Identify the source of economic rent and how long they endure.

Identify competitive advantage and how long will such advantage endure.

Economic Income and Rent

A project’s economic income in any year is equal to the cash flow plus the change in the asset’s present value.

Economic rent is the difference between a project’s economic income and the cost of capital.

Economic rent helps distinguish between good project and good-looking project.

Good projects generate positive economic rent, meaning actual economic income exceed cost of capital.

Positive NPV are projects that earn economic rents.

Lessons from Marvin Enterprises Example (Page 22)

Investment Viability: NPV's integrity hinges on the durability of competitive advantages and market conditions.

Impact Analysis: Understanding how new investments affect overall corporate asset values ensures comprehensive decision making.

Growth Strategy Risks: Emphasizing high-tech investment risks, including technological obsolescence and competitive entry, remains vital.

Collaborative Strategy Overhaul: Continuous evaluation of investment proposals against both internal and competitive markets' realities fosters strategic advantages.