Chapter 3: The Income Statement

Objective 3.1: Describe common operating transactions and select appropriate income statement account titles.

Operating Activities

- Operating activities occur routinely and are necessary for running a business. They often have a shorter duration of effect.

- Operating activities ^^produce expenses and revenues^^ for a company.

- Examples include:

- Selling a good or service

- Buying a good or service

- Cash payments

- Receiving cash

- The transactions between a company and a customer when selling goods or services is called the operating cycle.

- ^^The order of the operating cycle is^^:

- Buying goods and services

- Paying cash to suppliers and/or employees

- Selling goods and services

- Receiving money from customers

- The journal entries for this cycle would be structured like:

- Buying goods and services

| Account Name 1 | Account Name 2 | Debit | Credit |

|---|---|---|---|

| Supplies | | |\n| | Accounts Payable | | |

- Paying suppliers and/or employees

| Account Name 1 | Account Name 2 | Debit | Credit |

|---|---|---|---|

| Liability | | |\n| | Cash | | |

- Selling goods and services

| Account Name 1 | Account Name 2 | Debit | Credit |

|---|---|---|---|

| Account Receivable | | |\n| | Revenue | | |

- Receiving cash from customers

| Account Name 1 | Account Name 2 | Debit | Credit |

|---|---|---|---|

| Cash | | |\n| | Accounts Receivable | | |

The Income Statement

- The Income Statement vs the Balance Sheet

- Income Statements show the activities over a period of time (month ended, year ended)

- The accounts under an Income Statement are ^^temporary^^.

- Balance Sheets records assets, liabilities, and stockholders’ equity at specific point in time (like a snapshot)

- Accounts under the Balance Sheet are ^^permanent^^.

- Under the Income Statement, you will find:

- Revenues

- Expenses

- Net Income or Loss

- Revenues are the amount of ^^money generated^^ from selling goods or services. They are recorded when earned (doing the sale or service). Just because they are reported, does not mean they have gotten paid yet.

- Expenses are ^^costs incurred^^ from business operations. They are reported when resources are used, like supplies, land, buildings, etc.

- Net Income or Loss measures the company’s success

- To have Net Income, revenues must be greater than expenses.

- Net Income INCREASES stockholders’ equity.

- To get Net Loss, expenses are higher than revenues.

- Net Loss DECREASES stockholders’ equity.

- @@Equation to calculate net income or loss:@@

- Revenues - Expenses = Net Income or Loss

- The Income Statement uses the Time Period Assumption - Dividing the company’s long life into shorter chunks of time such as months, quarters, and years.

Cash Basis Accounting

- Cash basis accounting records revenues when cash is received and expenses when cash is paid.

- ^^Cash may not be received when something is paid “on account” or by credit^^.

- When cash is paid but not received, expenses are recorded and it creates an inaccurate representation of the company.

- When cash is received but not paid, revenues are recorded and it looks good for the company.

Objective 3.2: Explain and apply the revenue and expense recognition principles.

Accrual Basis Accounting

- In Accrual Basis Accounting, revenues are recorded when earned and expenses are recorded in the same period as correlated revenues (regardless of cash received or payment)

- Accounting standards:

- GAAP - Generally Accepted Accounting Principles

- IFRS - International Financial Reporting Standard

- Both GAAP and IFRS use accrual accounting for external reporting of income.

- The two basic accounting principles associated with accrual accounting are the revenue recognition principle and the expense cognition principle.

Revenue Recognition Principle

- The Revenue Recognition Principle says that revenues are acknowledged when the good or service is provided to the customer and not when cash is received.

- ^^Three scenarios can apply to revenues^^.

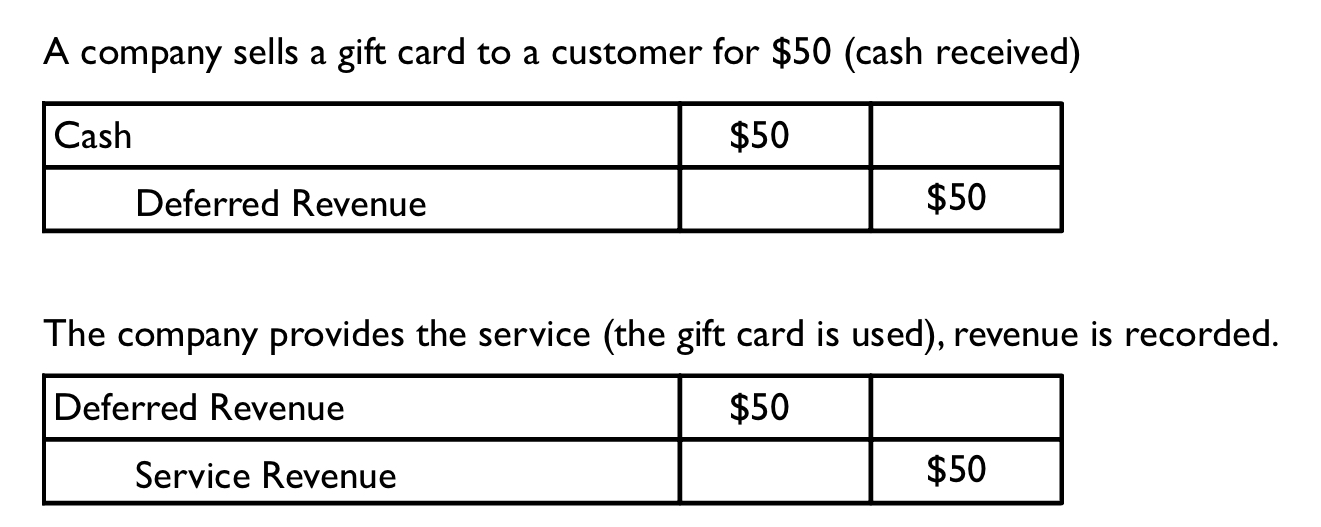

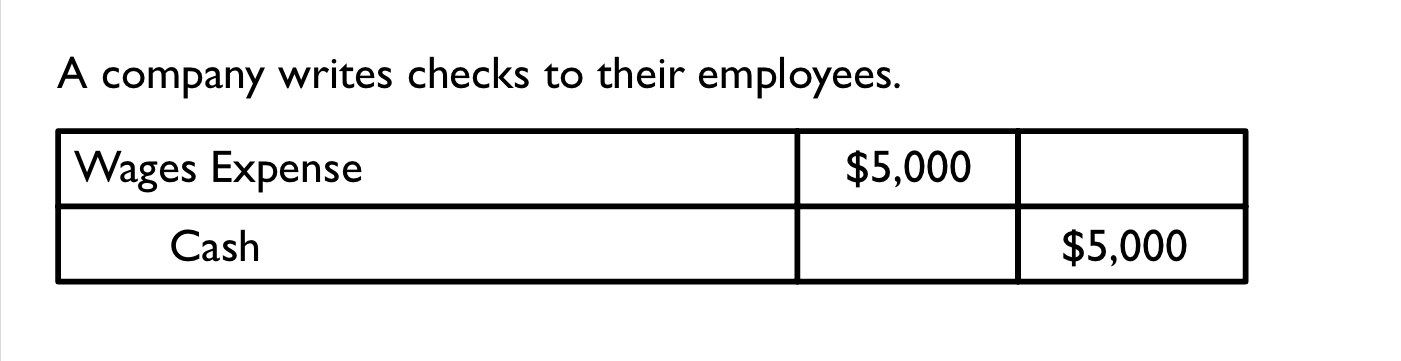

- Scenario 1: Cash is received before a sale or service.

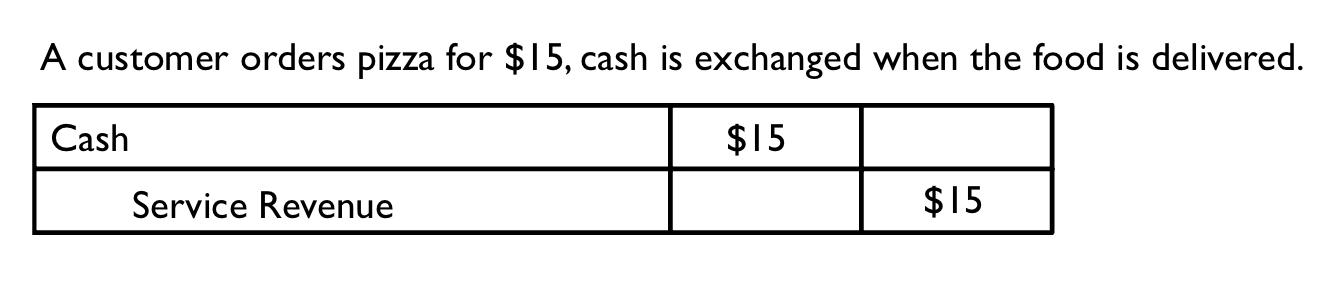

- Scenario 2: Cash comes in with the sale or service.

- The cash and revenue are reported at the same time.

- ONE journal entry: An asset is debited (cash) and revenue is credited at the same time.

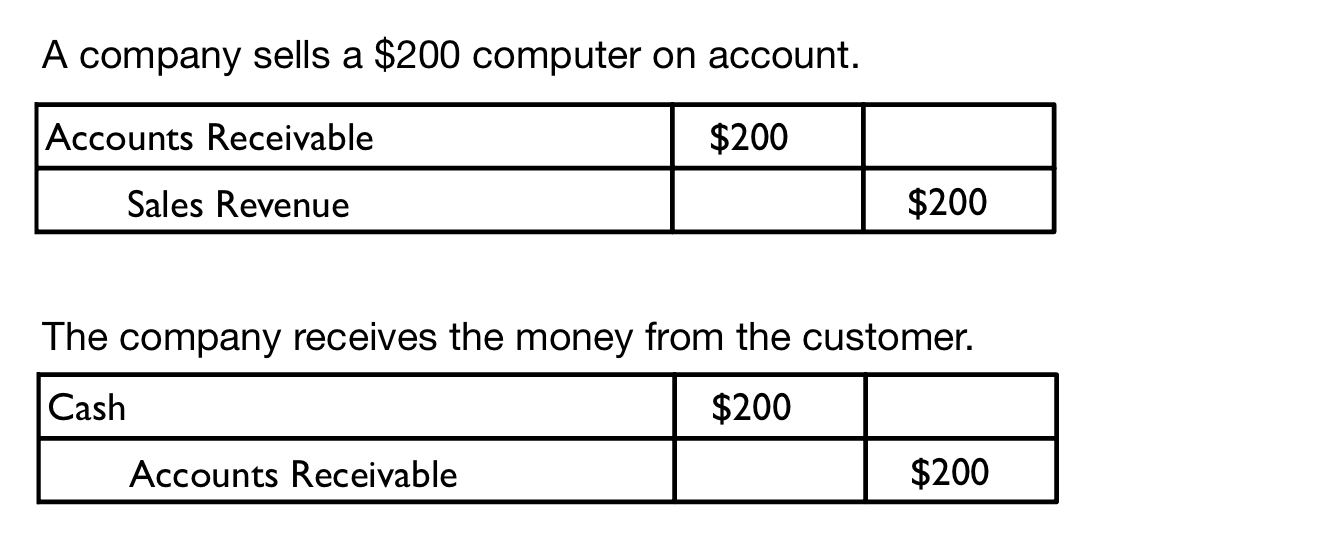

- Scenario 3: The sale or service happens first and cash comes after.

- Sale/service is provided, so an asset is debited (accounts receivable) and revenue is credited.

- Cash is received, so an asset is debited (cash) and an asset is credited (accounts receivable).

- Deferred Revenue is a liability on the Balance Sheet. It means you ^^promise to provide a sale or service^^.

- The term “on account” means you bought a good or service without cash and ^^will owe cash to the company in the future^^.

- Accounts Receivable is the right to collect cash from a customer who paid “on account”. It is an asset on the Balance Sheet.

Expense Recognition Principle

- The Expense Recognition Principle (aka “matching”) means expenses are recorded in the same period as revenues.

- An expense is recorded when an asset is used.

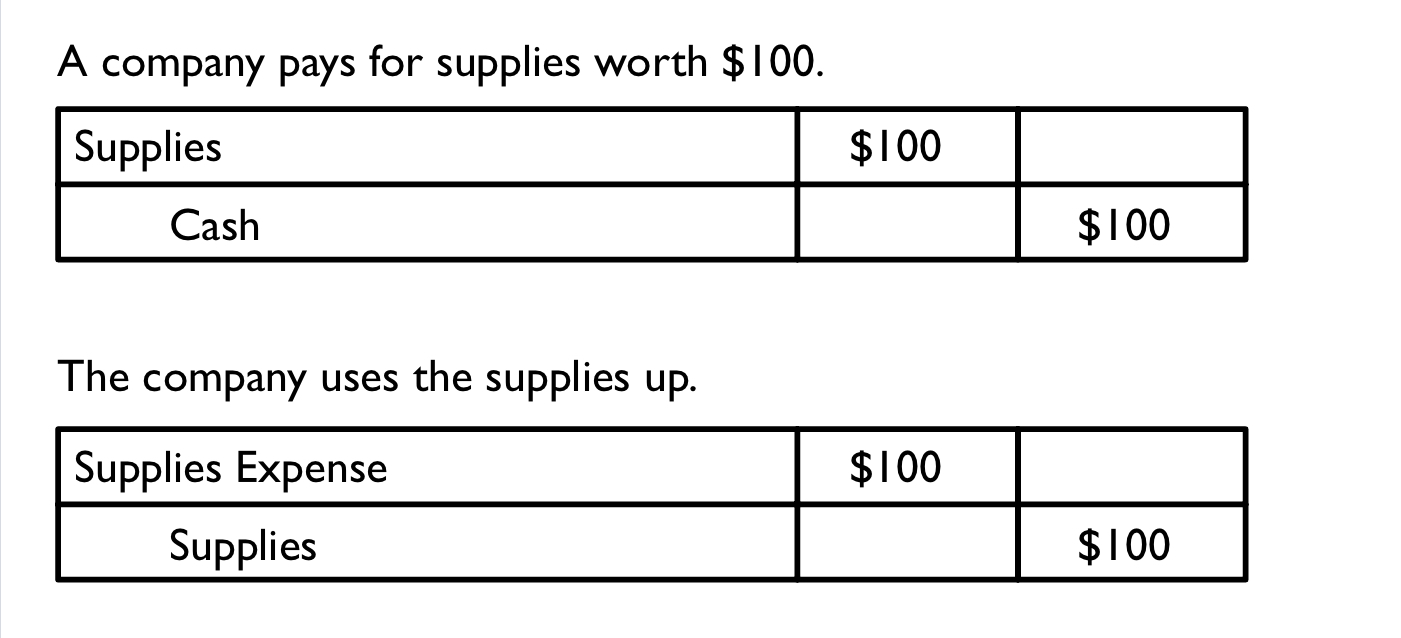

- ^^Three scenarios can apply to expenses^^.

- When paying for supplies, an asset is debited and an asset is credited.

- When the supplies are used up, an expense is credited and an asset is credited.

- This can apply to supplies, equipment, prepaid rent, etc.

Scenario 1: Cash is paid before the expense

Scenario 1: Cash is paid and expense is reported in the same period

- ^^Only one journal entry^^: An expense is debited and an asset is credited.

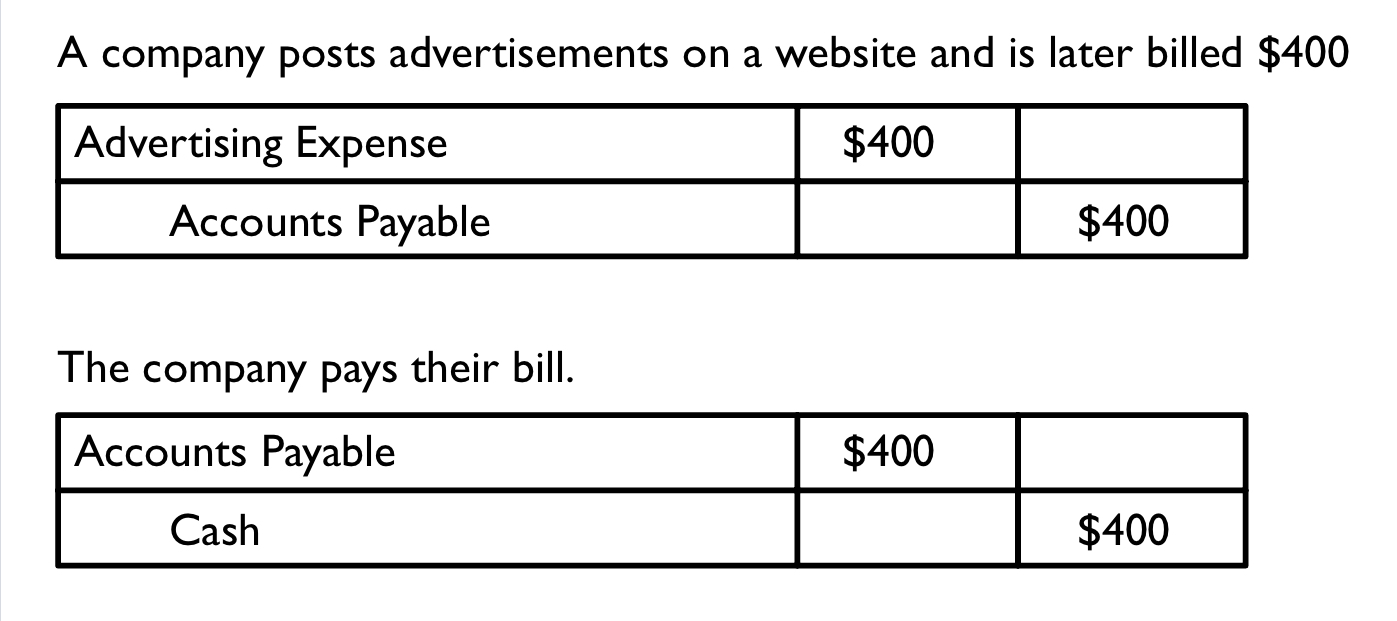

Scenario 3: Cash comes after the expense is reported

- When services are used up, an expense is debited and a liability is credited (Accounts Payable).

- When you pay cash for the service used up, the liability is debited (Accounts Payable) and the asset is credited (cash)

- Accounts Payable - A promise to pay in the future.

Objective 3.3: Analyze, record, and summarize the effects of operating transactions using the accounting equation, journal entries, and T-accounts.

The Expanded Accounting Equation

- Basic accounting equation: Assets = Liabilities + Stockholders’ Equity.

- The Expanded Accounting Equation breaks down the contents of Stockholders’ Equity.

- Stockholders’ Equity consists of Common Stock and Retained Earnings.

- ^^Retained Earnings has two subcategories^^:

- Revenues

- They have a normal credit balance (right side of T-account).

- Increases Net Income.

- Increases Retained Earnings.

- Expenses

- Expenses have a normal debit balance (left side of T-account).

- Decreases Net Income.

- Decreases Retained Earnings.

Totaling T-Accounts

- Each individual T-account must have an ending balance.

- T-accounts for assets, liabilities, and stockholders’ equity are totaled.

Objective 3.4: Prepare an unadjusted trial balance.

Unadjusted Trial Balance

- An adjusted trial balance makes sure debits equal credits after finding the ending balances for each account. Adjustments are made if needed.

- The totals for accounts with normal debit balances are found in the left column and the totals for accounts with a normal credit balance are found in the right column.

Objective 3.5: Evaluate net profit margin, but beware of Income Statement limitations.

Net Profit Margin

- The Net Profit Margin is the profit made from revenues.

- @@Equation to calculate net profit:@@

Income Statement Limitations

- ^^Three misconceptions about the Income Statement^^:

- Net Income is NOT the cash generated by the business.

- Net Income does NOT report the change in the company’s value during the period. When assets increase and decrease during a period of time, this is not reflected in Net Income.

- Net Income is NOT exact, it is an estimate.