Chapter 7: Inventory and Cost of Goods Sold

Objective 7.1: Describe the issues in managing different types of inventory

Types of Inventory

- Merchandise inventory consists of products that are @@already made@@. Merchandisers then sell these finished goods to their customers.

- Manufacturers have @@three types of inventory@@: raw materials, work in process, and finished goods.

- These three types of inventory represent the manufacturing process.

- Raw materials are materials that are waiting to be processed, such as plastic, steel, and fabric.

- Work in Process goods are not up for sale yet, but are in the process of getting to that stage.

- Finished goods are the inventory that are completed and ready to be sold to customers.

- Raw materials are used to create the goods that are in the process of being manufactured, which results in the completed products

- Consignment inventory are any products being held by a company so they do not claim ownership over the owners’ product. In the case the inventory is difficult to sell, the ownership is not under them.

- Goods in transit are goods being transported to the location of the buyer, whether this is someones front door or a store getting ready to sell those items (Walmart).

Inventory Management Decisions

- Inventory managers must:

- Ensure there is enough inventory to meet demand.

- Ensure the quality of the product is satisfactory.

- Minimize costs of acquiring, transporting, and storing inventory.

Objective 7.2: Explain how to report inventory and cost of goods sold.

Balance Sheet and Income Statement Reporting

- Inventory is reported on the Balance Sheet as a current asset because it will be sold to generate cash within a year.

- When inventory is sold, the cost moves from the Inventory account (balance sheet) and becomes Cost of Goods Sold expense (income statement).

- ==Equation to calculate gross profit:==

- Net Sales - Cost of Goods Sold = Gross Profit

Cost of Goods Sold Equation

- The Cost of Goods Sold equation changes depending if it’s for periodic or perpetual updating of inventory.

- Periodic Updating is used for small businesses (mom and pop shops).

- ==It uses the Cost of Goods Equation, which is:==

- Beginning Inventory + Purchases - Ending Inventory = Cost of Goods Sold

- Perpetual Updating is used for bigger companies (Walmart).

- ==It uses the Ending Inventory equation, which is:==

- Beginning Inventory + Purchases - Cost of Goods Sold = Ending Inventory

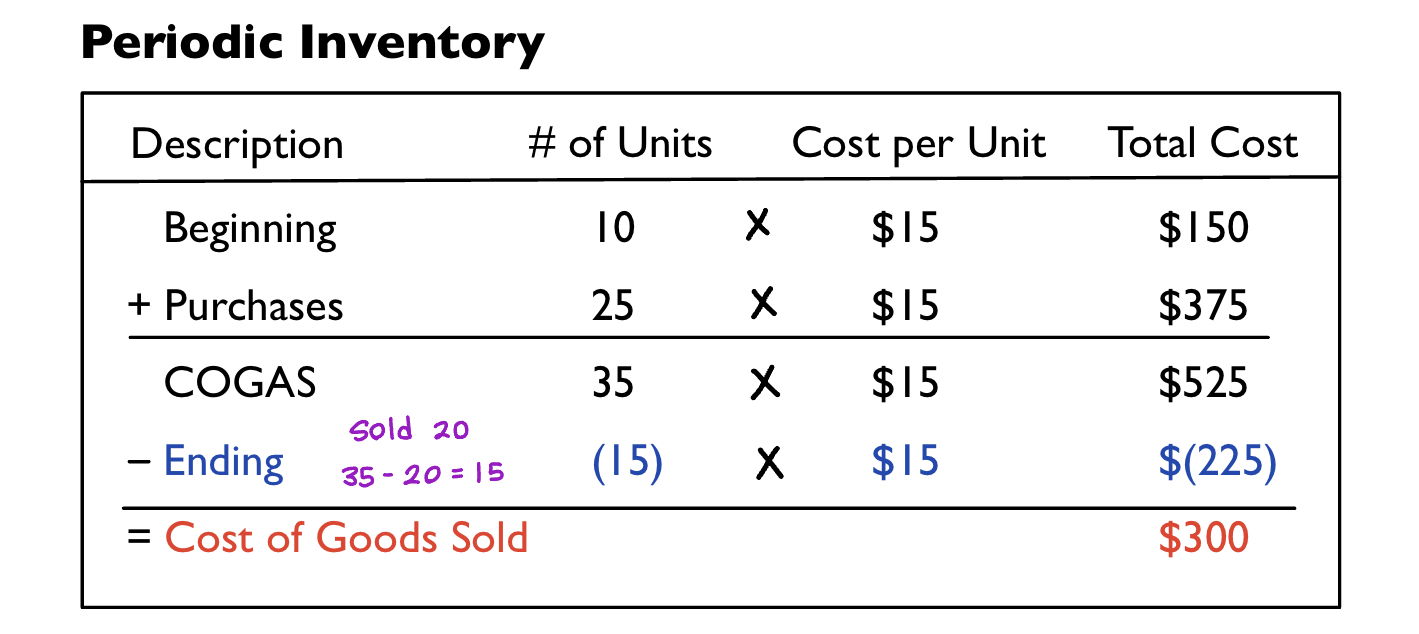

- Example (periodic): A company has 10 units in their beginning inventory that each cost $15. The company then purchases 25 units that cost $15 each. Its has 15 units in ending inventory. (COGAS = Cost of Goods Available for Sale)

- Periodic Steps

- Step 1: Multiply number of units and cost per unit to find the total cost of beginning inventory and purchases.

- 10 x $15 = $150

- 25 x $15 = $375

- Step 2: Add the number of units for beginning inventory and purchases to find COGAS units and total cost.

- 10 + 25 = 35 units

- $150 + $375 = $525

- Step 3: We are told that ending inventory is 15.

- Step 4: Multiply ending inventory units by cost per unit to find total cost.

- 15 x $15 = $225

- Step 5: Subtract total cost of ending inventory from COGAS to find the total cost of Cost of Goods Sold.

- $525 - $225

- Cost of Goods Sold = $300

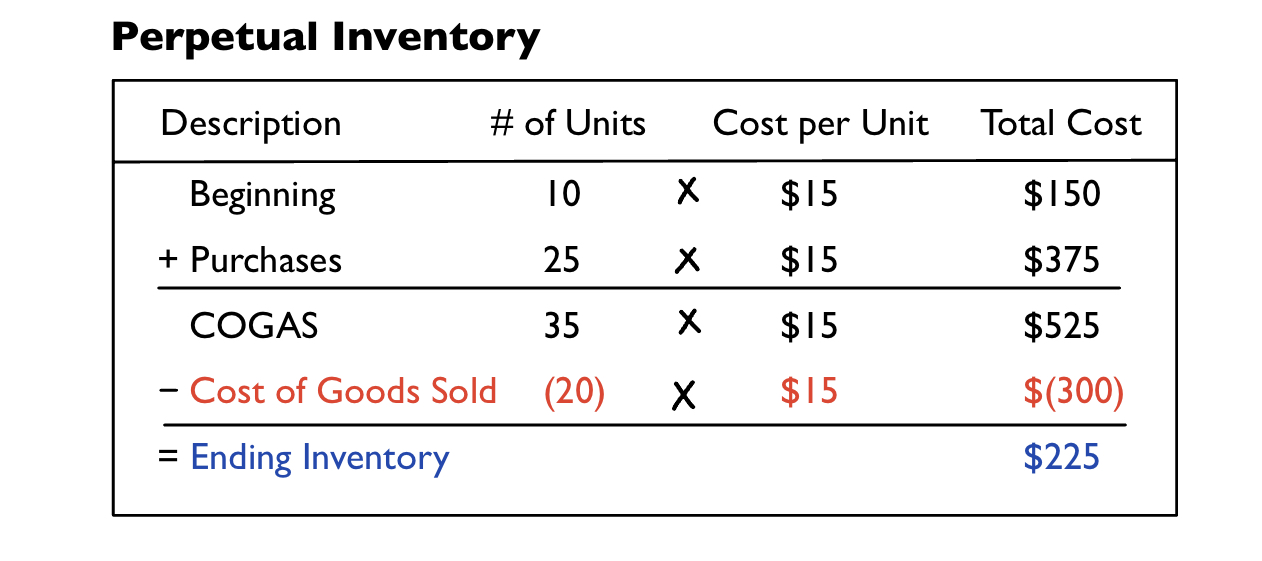

- Example (perpetual): A company has 10 units in their beginning inventory that each cost $15. The company then purchases 25 units that cost $15 each. It then sells 20 units.

- Step 1: Multiply number of units and cost per unit to find the total cost of beginning inventory and purchases.

- 10 x $15 = $150

- 25 x $15 = $375

- Step 2: Add the number of units for beginning inventory and purchases to find COGAS units and total cost.

- 10 + 25 = 35 units

- $150 + $375 = $525

- Step 3: We are told that cost of goods sold is 20

- Step 4: Multiply cost of goods sold units by cost per unit to find total cost.

- 20 x $15 = $300

- Step 5: Subtract total cost of cost of goods sold from COGAS to find the total cost of ending inventory.

- $525 - $300

- Ending inventory = $225

Objective 7.3: Compute costs using four inventory costing methods.

Inventory Costing Methods

- The four inventory costing methods tell us the @@value of what was sold and what should be in Cost of Goods expense@@.

- All methods are accepted by the Generally Accepted Accounting Principles (GAAP).

- Specific identification

- Individually identifies and records the cost of each item sold as Cost of Goods Sold.

- The cost of each item must be tracked.

- This method is best used for luxury items (Cars, Jewelry)

- The last three are not based on physical flow of goods, but based on Cost Flows Assumptions, which are assumptions accountants make about the flow of inventory costs.

- First in, first out (FIFO) - Inventory goes out (sold) in the order the goods are received.

- Last in, last out (LIFO) - The last goods received are the first to be sold.

- Weighted average - The average for Cost of Goods Available for Sale is used for each good sold and for the goods that are still in inventory.

- Equation to calculate weighted average cost:

- Cost of Goods Available for Sale/Number of Units Available for Sale = Cost per unit

- Apply the average to what was sold and what was not sold (sales and ending inventory).

- ==Equation to calculate total cost:==

- Number of units x Cost per units = Total cost

- After sales are made, calculate ending inventory by subtracting sales from beginning inventory.

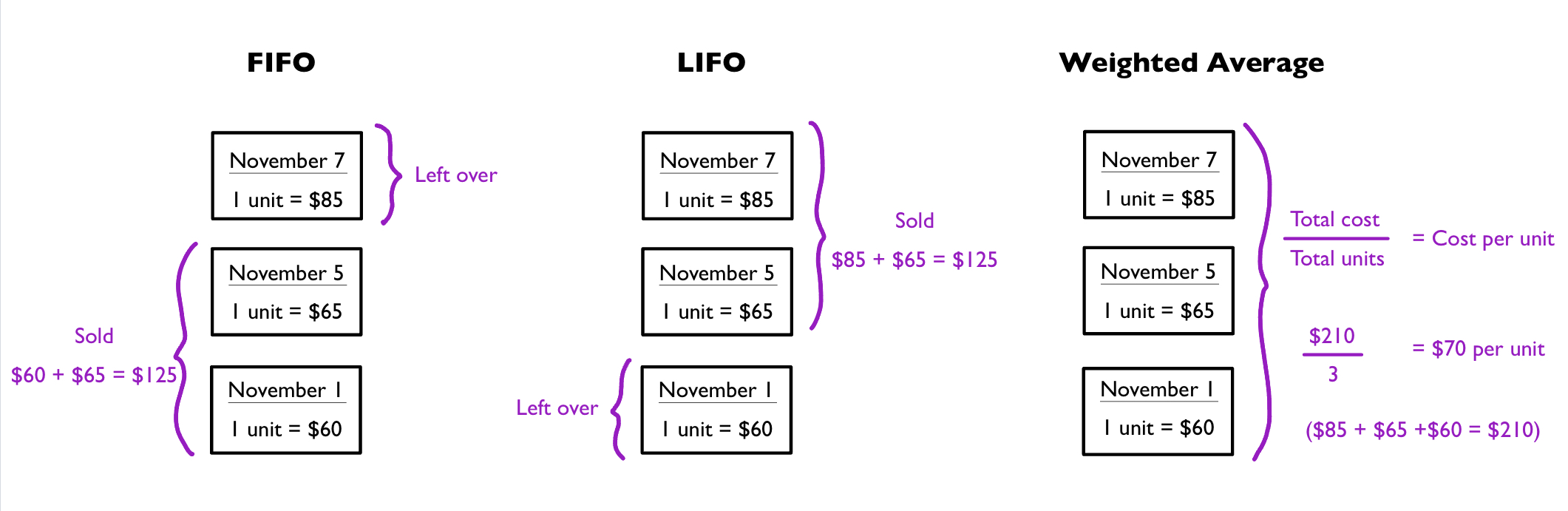

- Example: Using the following table of information, we will apply it using the specific identification method, FIFO method, LIFO method, and weighted average.

| Date | Description | Cost |

|---|---|---|

| November 1 (first in) | Purchased 1 Unit | $60 |

| November 5 | Purchased 1 Unit | $65 |

| November 7 (last in) | Purchased 1 Unit | $85 |

| November 10 | Sold 2 Units | $115 per unit |

Specific Identification

- The cost of each item sold is recorded as part of Cost of Goods Sold.

- Example: Units from from November 1 and November 7 are sold.

- $60 + $85 = $145

- $145 is reported as Cost of Goods Sold

- The unit from November 5th that was not sold remains in Inventory ($65).

FIFO (First in, first out)

- We are selling 2 units.

- The first unit purchased was on November 1st, so we sell that first.

- The second unit we would sell would be from November 5th.

- Add those units together: $60 + $65 = $125 (Cost of Goods Sold)

LIFO (Last in, first out)

- We are selling 2 units.

- The last unit purchased was on November 7th, so we selling that first.

- The second unit we would sell would be from November 5th.

- Add those units together: $85 + $65 = $125

Weighted Average

- We use the equation (total cost/total units) = Cost per unit.

- Add the cost of each unit together to find total cost: $85 + $65 + $60 = $210

- We have a total of 3 units.

- Divide total cost by total units: 210/3 = $70 per unit

Financial Statement Effects

- The inventory costing methods split cost of goods available for sale between ending Inventory and Cost of Goods Sold differently.

- Cost that goes into Inventory will not go into Cost of Goods Sold.

- The method that results in the highest cost in Inventory will have the lowest cost in Cost of Goods Sold.

- The method that results in the highest cost in Cost of Goods Sold will have the lowest cost in Inventory.

- @@Costs rising and falling have different financial effects@@

- Rising costs = larger inventory and smaller cost of goods sold.

- Falling costs = smaller inventory and larger costs of goods.

Tax Implications and Cash Flows Effects

- Using a method that results in lower inventory and higher cost of goods sold is beneficial because of lower income tax.

- A company may only switch from one method to another if it improves the accuracy of the company’s financial results.

- Methods can also be used for specific types of inventory, but must be consistent with how the method is used.

- The LIFO conformity rule says the method used for the company’s income tax return must also be used for the financial statement.

Objective 7.4: Report inventory at the lower of cost or market/net realizable value.

Lower of Cost or Market/Net Realizable Value

- The value of inventory may be lower than the cost of the inventory because…

- It is replaced by similar goods and a lower cost

- The goods are outdated or damaged.

- As required by the GAAP, @@there is a rule for reporting inventory at the lower cost or market (LCM)/net realizable value (NRV)@@.

- If the inventory value has fallen below its cost, it must be marked down to the lower value.

- Market value is a replacement cost.

- Net realizable value is the inventory value to be realized when sold.

Objective 7.5: Evaluate inventory management by computing and interpreting the inventory turnover ratio.

Inventory Turnover

- Inventory balance can be good or bad. When you have a lot of inventory for sale, you will make good profit. When inventory builds up because of lack of sales, thats bad.

- Inventory turnover is the cycle of an increasing balance when a company buys goods and a decreasing balance when a company sells goods.

- To evaluate change in inventory, we use inventory turnover analysis.

- An inventory turnover ratio shows how many times inventory is bought and sold. A higher ratio indicates inventory is bought and sold quickly.

- ==Equation to calculate the inventory turnover ratio:==

- Cost of Goods Sold/Average Inventory

- The higher the better.

Days to Sell

- “Days to Sell” focuses on the length of time it takes to sell inventory.

- ==Equation to calculate days to sell:==

- 365/Inventory Turnover Ratio

- A higher number represents a longer amount of time to sell goods.

Example of Inventory Turnover and Days to Sell

- The chart shows the Cost of Goods Sold (COGS) and Inventory of a company from two different years.

- Using this information, it is plugged into the inventory turnover equation.

- The inventory turnover ratio is then plugged into the days to sell equation to get the final answer.