Chapter 7: Elasticity, Microeconomics Policy, and Consumer Theory

Elasticity of demand (ED)

- It’s a measure of the responsiveness of consumers to change in price

- If a firm increases price of their product, would consumers still buy it?

- If a demand for a product is inelastic, change in price wouldn’t impact the consumers much e.g. cancer medicines

- If the demand for a product is elastic, change in price would impact the quantity purchased of that product

- The following is the formula to calculate the ED

- %change in Qd / %change in Price

- Economists ignore the negative value of PED

- The greater the value, the more sensitive consumers are to a change in the price of good X

- The answer that is received falls under the following ranges, each with their own interpretation

| ]]Type of Elasticity]] | ]]Elasticity value]] |

|---|---|

| Perfectly inelastic | 0 |

| Relatively Inelastic | <1 |

| Unit elastic | 1 |

| Relatively elastic | >1 |

| Perfectly elastic | Infinity |

Example

- Suppose the price of designer blue jeans increases from $100 to $120 and the quantity demanded decreases from 10 to 9

- First, calculate the percentage change for both price and quantity demanded: ($120 – $100)/$100 = 0.2= 20% increase in price

- (9 – 10)/10 = –0.1 = 10% decrease in the quantity demanded.

- Ed = (–10%)/(20%) = 0.5

- The price elasticity is relatively inelastic

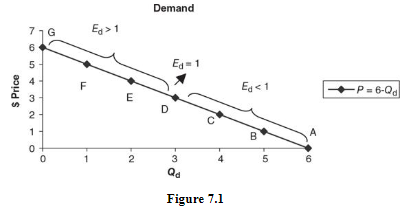

Elasticity on the demand curve

The midpoint formula

- (Change in Qd/Change in Price) x (Average price/ Average quantity)

Example

- Initial price of a hypothetical product is $16, and 20 units are demanded

- The price rises to $20, quantity demanded falls to 10 units.

- The average price between these two points is $18, and the average quantity is 15 units

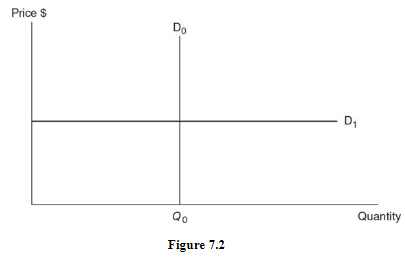

Special cases

- The following is a perfectly inelastic demand curve (D0)

- No substitutes

- Vertical demand curve tells us that no matter what percentage increase, or decrease, in price, the quantity demanded remains the same

- Ed = 0

- The following is a perfectly elastic demand curve (D1)

- Many substitutes

- Horizontal demand curve tells us that even the smallest percentage change in price causes an infinite change in the quantity demanded

- Ed = infinite

Determinants of elasticity

- Number of Good Substitutes

- Proportion of Income

- Time

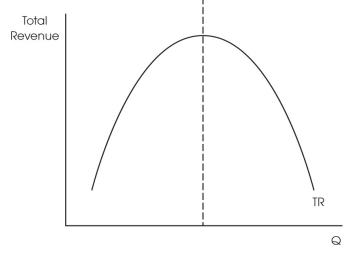

Total revenue test to determine elasticity

- Total revenue is price x quantity

- The answer falls under the following categories, each with its own interpretation

| ]]Type of Elasticity]] | ]]Relationship between Price and total revenue (TR)]] |

|---|---|

| Relatively elastic | inverse relation |

| Relatively inelastic | direct relation |

| Unit elastic | TR doesn’t change when P changes |

- If price increases but total revenue decreases, the demand for the product is relatively elastic

- If price increases and total revenue also increases, the demand for the product is relatively inelastic

- If price changes but total revenue stays same, the demand for the product is unit elastic

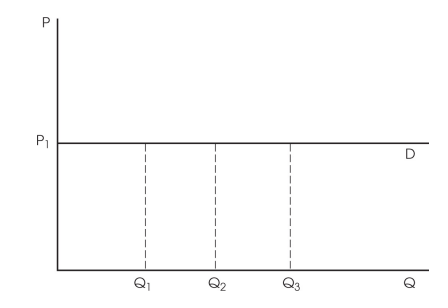

Perfect elasticity

- If the demand is perfectly elastic, the price elasticity is infinity

- Any price above P1 and the demand falls to zero

- Any price that’s exactly P1, the demand could keep increasing (buyers would buy as much quantity as possible)

- Any price below P1 and the quantity demanded becomes infinite

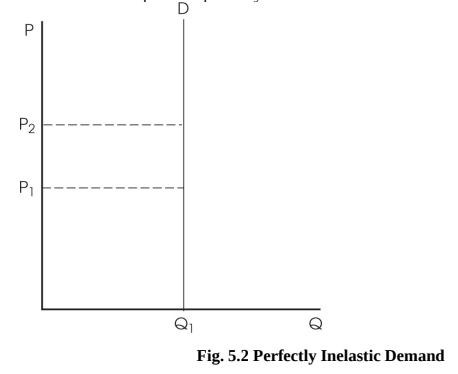

Perfect inelasticity

- If the demand is perfectly inelastic, the price elasticity of demand is zero

- As the price keeps on changing, the quantity demanded stays same

- A good example of this would be life-saving drugs

- Prices could increase by a big margin but quantity demanded wouldn’t change still

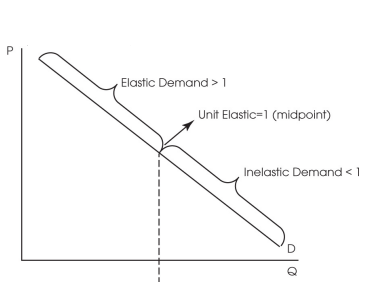

Elasticity along a linear demand curve

- The demand curve is elastic towards the top, unit elastic at the midpoint and inelastic towards the bottom

- As the prices decrease in the elastic range, the total revenue eventually increases

- As the prices decrease in the inelastic range, the total revenue actually decreases

- Monopolies (a type of market structure) prefer producing in the elastic range because that’s also where the revenue is maximized

Income Elasticity of demand

- This measure how the demand for a product changes with respect to change in their income

- % change in quantity demanded/ %change in consumers income

- Calculations of this help determine whether the product is inferior or normal good

- Inferior good: as income increases, demand for the product decreases

- Normal good: as income increases, demand for the product increases

Three Questions to Determine Demand Elasticity

1. Necessity of the product

- If the product is a necessity, such as life-saving drugs, prices could increase but people would still purchase it

- Products which are wants, such as cars, demand would be price elastic

2. Could the purchase be delayed

- The longer the time consumers have the product as a choice, the more elastic the product demand tends to be

- If the choice time is limited, the product demand tends to be inelastic

- A good example would be emergency supplies

- Since the decision time is limited, demand tends to be inelastic

3. Does the purchase require a larger budget range?

- If the product forms a large proportion of someone’s budget, demand tends to be elastic

- An increase in the price of luxury products would result to consumers stopping their purchase for the time being

- On the contrary, products that don’t form a large proportion of someone’s budget such as match sticks, are inelastic in nature (purchased even if prices increases)

Cross-price elasticity of demand

- This measures how a demand for a product changes with respect to price changes

- Calculations of this help determine whether the product is a complement or substitute

- % change quantity demanded for product X/ % change in price of product Y

- If the result is positive, the product is substitute

- If the result is negative, the product is complement

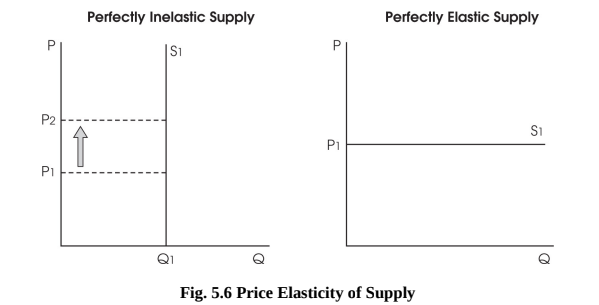

Price Elasticity of supply

- This measures the change in supply that takes place with respect to changes in price

- Time is key factor when looking at supply elasticity

- The longer the firms have time to adjust, the more elastic the supply (difficult to adjust in the short term hence the inelasticity)

- In the longer run, market supply is usually perfectly elastic

- % change in quantity supplied / % change in price

- If the demand curve is perfectly elastic, there wouldn’t be any consumer surplus

- If the supply curve is perfectly elastic, there wouldn’t be any producer surplus

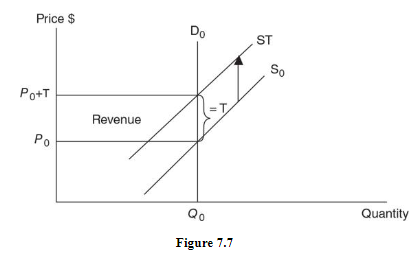

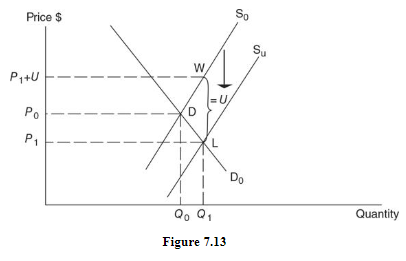

Excise taxes

- Per-unit tax on production

- Firm responds as if the marginal cost of producing each unit has risen by the amount of the tax

- Results in a vertical shift in the supply curve by the amount of the tax

Reason for taxes are:

- Increase revenue collected by the government

- To decrease consumption of a good that might be harmful to some members of society

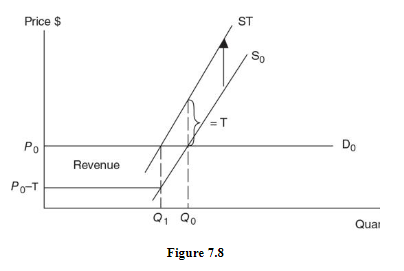

Demand Is Perfectly Inelastic

- Assume the following demand is of tobacco

- If a per-unit tax of T is imposed on the producers of cigarettes, the supply curve shifts upward by T

- Since quantity remained constant, the tax did nothing to decrease the harmful effects of smoking in society

- Only increased tax revenues for the government

- The entire tax was paid by consumers in the form of a new price exactly equal to the old price plus the tax.

Demand is perfectly elastic

- Assume the following demand is of tobacco

- The per-unit tax of T shifts the supply curve upward by T

- Because the price of a pack of cigarettes did not increase after the tax, it was not the consumers who paid more

- Producer pays the entire share of the tax when demand is perfectly elastic

- Compared to the perfectly inelastic scenario, the government collected much fewer tax revenue dollars

- Maximum decrease in harmful cigarette consumption is a definite plus

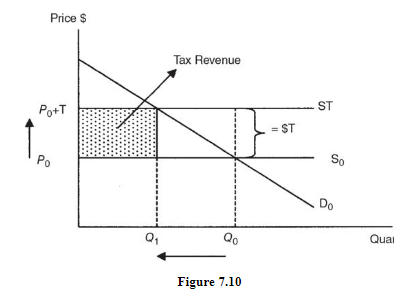

The Role the Supply Curve Plays in the Impact of an Excise Tax

- A perfectly elastic, or horizontal, supply curve tells us that even a very small change in the price will cause an infinitely large change in the quantity supplied

- The new equilibrium price is exactly T higher than the old price P0, so consumers pay the entire burden of the tax

- The equilibrium quantity decreases from Q0 to Q1, and the government collects tax revenue equal to T × Q1.

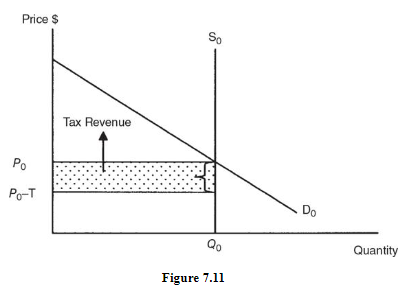

- A perfectly inelastic, or vertical, supply curve illustrates the special case where any change in the price creates absolutely no change in the quantity supplied

- At the equilibrium quantity Q0, suppliers would like to charge a higher price than P0, but any price above P0 creates a surplus, and this surplus will clear only at the equilibrium price P0.

- The firms must pay T to the government for each of the Q0 units that are sold and consumers continue to pay the original price of P0

- Producers pay the entire burden of the tax because, after paying the tax, they receive only (P0 – T) on each unit

Price elasticity of supply and tax incidence

| ]]Price elasticity of supply]] | ]]Government revenue]] | ]]Decrease in consumption]] | ]]Incidence of tax paid by consumers]] | ]]Incidence of tax paid by product]] |

|---|---|---|---|---|

| infinity | the least | the most | 100% | 0% |

| >1 | falling | sizeable | >50% | <50% |

| <1 | rising | minimal | <50% | >50% |

| 0 | the most | 0 | 0% | 100% |

- As the price elasticity of demand falls, and the price elasticity of supply rises, the greater the consumer’s share of a per-unit excise tax

- Conversely, as the price elasticity of demand rises and the price elasticity of supply falls, the producer’s share of a per-unit excise tax rises

Loss to society

- There is also a cost to society when an excise tax is imposed on a competitive market

- With the tax, consumers and producers demand and supply 20 fewer units than without the tax

- For these 20 units that go unproduced, the marginal benefit to consumers exceeds the marginal costs to producers

- 20 units go unproduced and unconsumed resulting in an inefficient outcome

- Economists call this area deadweight loss (DWL), or the net benefit sacrificed by society when such a per-unit tax is imposed (triangle labeled DWL)

- Taxes create lost efficiency by moving away from the equilibrium market quantity where MB = MC to society.

- The area of deadweight loss (triangle DWL) increases as the quantity moves further from the competitive market equilibrium quantity

Subsidies

- A per-unit subsidy on good X has the opposite effect of an excise tax

- Firms respond as if the subsidy has lowered the marginal cost of production

- Results in a downward vertical shift in the supply curve for good X

- Assume the graph of the market for public university education

- The subsidy decreases tuition to P1 and increases the number of undergraduate degrees received

- Subsidy distorts the market and creates deadweight loss

- Deadweight loss is the area of the triangle labeled DWL.

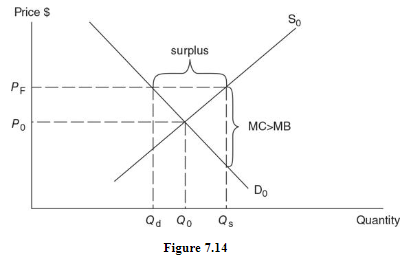

Price Floors

- A price floor is a legal minimum price below which the product cannot be sold

- An ineffective price floor would be a price set below the equilibrium price

- Assume this to be a market for milk

- The resulting surplus of milk is not eliminated through the market

- The government usually agrees, as part of the price floor arrangement, to purchase the surplus milk

- By providing an incentive for producers to produce beyond where MB = MC, the price floor policy causes efficiency to be lost.

- For gallons of milk above Q0, MC > MB; there is an over allocation of resources to milk production

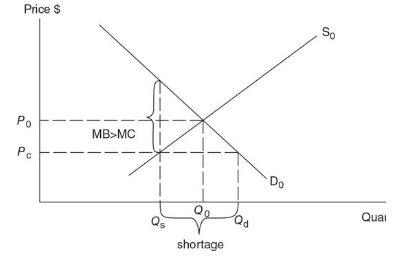

Price Ceilings

- A price ceiling is a legal maximum price above which the product cannot be bought and sold

- An effective price ceiling must be set below the equilibrium price

- Assume this to be a market for rent-controlled households

- This form of price control results in lost efficiency for society

- When suppliers reduce their quantity supplied below the competitive equilibrium quantity, there is a situation where MB > MC, and we see under allocation of resources in the rental apartment market

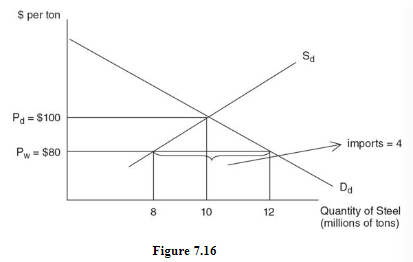

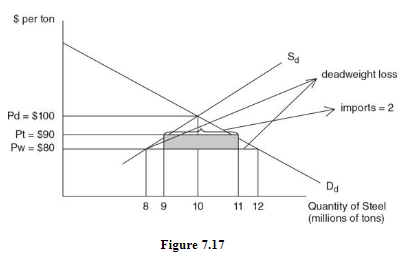

Trade Barriers

1. Tariffs

- Revenue tariff is an excise tax levied on goods that are not produced in the domestic market.

- Protective tariff is an excise tax levied on a good that is produced in the domestic market

Economic effects of the tariff

- Consumers pay higher prices and consume less

- Consumer surplus has been lost

- Domestic producers increase output

- Declining imports

- Tariff revenue

- Inefficiency

- Deadweight loss

2. Quotas

- Import quota is a maximum amount of a good that can be imported into the domestic market

- Both hurt consumers with artificially high prices and lower consumer surplus.

- Both protect inefficient domestic producers at the expense of efficient foreign firms, creating a deadweight loss.

- Both reallocate economic resources toward inefficient producers.

- Tariffs collect revenue for the government, while quotas do not

Consumer Choice

Utility

- People demand things because those things make those people happy

- In economics, we call this happiness utility

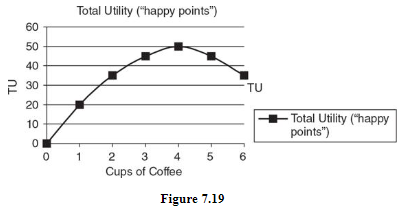

- Consumption of more and more of something is likely to increase our total utility

- It is probably safe to say that the first pint in a week provides more marginal utility than the second, third, or fourth pint

- Total utility (TU) is the total amount of happiness received from the consumption of a certain amount of good.

- Marginal utility (MU) is the additional utility received from the consumption of the next unit of a good

- MU = ∆TU/∆Q

Unconstrained consumer choice

- Total utility initially rises, peaks, and then begins to fall as more coffee is consumed(see fig above)

- Even if the monetary price of good X is zero, the rational consumer stops consuming good X at the point where total utility is maximized.

Diminishing marginal utility

- The law of diminishing marginal utility says that in a given time period, the marginal utility from consumption of one more of that item falls

Constrained utility maximization

- With a fixed daily income and a price that must be paid, this individual is now a constrained utility maximizer

- When required to pay a price, the utility-maximizing consumer stops consuming when MB = P.

- This MB also represents the highest price, or “willingness to pay,” our consumer would be willing to pay for the next cup.

Demand curve revisited

- Law of diminishing marginal utility is the backbone of the law of demand

- Because of diminishing marginal utility, you offer to pay less for additional units

Utility maximizing rule

- Consumers maximize utility when they buy amounts of goods X and Y so that the marginal utility per dollar spent is equal for both goods

- MUx/Px = MUy/Py

- If the consumer has used all income and the above ratios are equal, they are said to be in equilibrium

- It is very important to remember that consuming more of one good causes the marginal utility to fall, but the total utility to rise

- To find the total utility of consuming cups of coffee, sum up the marginal utility of each cup consumed. Do the same for scones to calculate total utility

| ]]Cups of coffee]] | ]]MU of coffee]] | ]]# of Scones]] | ]]MU of Scone]] |

|---|---|---|---|

| 1 | 10 | 1 | 30 |

| 2 | 8 | 2 | 24 |

| 3 | 6 | 3 | 20 |

| 4 | 4 | 4 | 16 |

| 5 | 2 | 5 | 14 |

| 6 | 1 | 6 | 8 |

- MUc/MUs = $2/$4= .5 or

- MUc/MUs = $1/$4 = .25