Chapter 6 - Perfectly competitive supply

Profit-maximizing firms in perfectly competitive markets

Profit: total revenue a firm receives from the sale of its product minus all costs - explicit and implicit - incurred in producing it.

Profit-maximizing firm: firm whose primary goal is to maximize the difference between its total revenues and total costs.

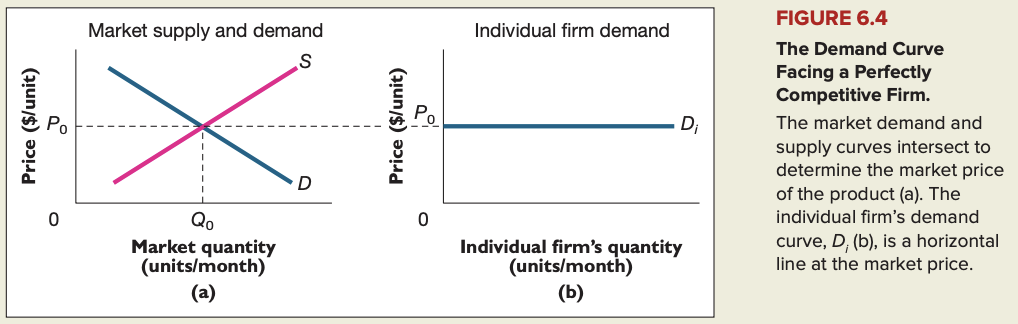

Perfectly competitive market: market in which no individual supplier has significant influence on the market price of the product.

Price taker: firm that has no influence over the price at which it sells its product.

Characteristics of markets that are perfectly competitive:

- All firms sell the same standardized product.

- The market has many buyers and sellers, each of which buys or sells only a small a fraction of the total quantity exchanged.

- Productive resources are mobile.

- Buyers and sellers are well informed.

- That means they are aware of the relevant opportunities available to them.

Imperfectly competitive firm: firm that has at least some control over the market price of its product.

Factor of production: input used in the production of a good/service.

Short run: period of time sufficiently short that at least some of the firm's factors of production are fixed.

Long run: period of time of sufficient length that all the firm's factors of production are variable.

Law of diminishing returns: property of the relationship between the amount of a good/service produced and the amount of a variable factor required to produce it; the law says that when some factors of production are fixed, increased production of the good eventually requires ever-larger in creases in the variable factor.

Fixed factor of production: input whose quantity cannot be altered in the short run.

Variable factor of production: input whose quantity can be altered in the short run.

Fixed cost: sum of all payments made to the firm's fixed factors of production.

Variable cost: sum of all payments made to the firm's variable factors of production.

Total cost: sum of all payments made to the firm's fixed and variable factors of production.

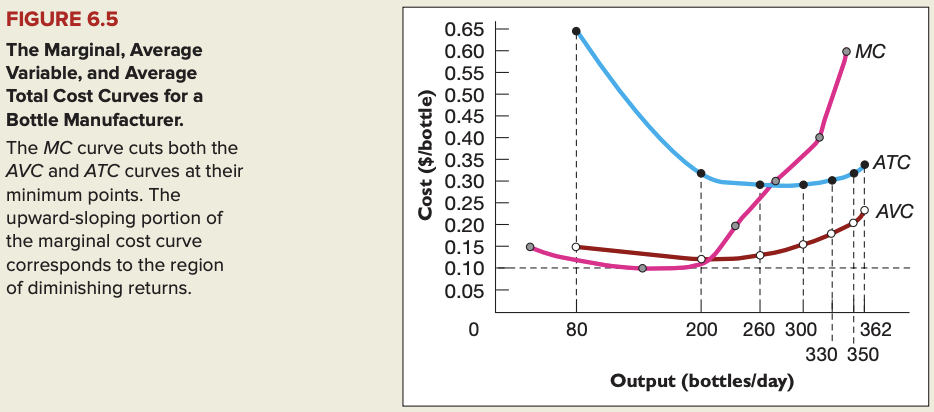

Marginal cost: as output changes from one level to another, the change in total cost divided by the corresponding change in output.

Profit = Total revenue - Total cost

Profit = Total revenue - Variable cost - Fixed cost

Average variable cost (AVC): variable cost divided by total output.

Average total cost (ATC): total cost divided by total output.

Profitable firm: firm whose total revenue exceeds its total cost.

Determinants of supply revisited

- Among the relevant factors causing supply curves to shift are:

- New technologies

- Changes in input prices

- Changes in the number of sellers

- Expectations of future price changes

- Changes in the prices of other products that firms might produce

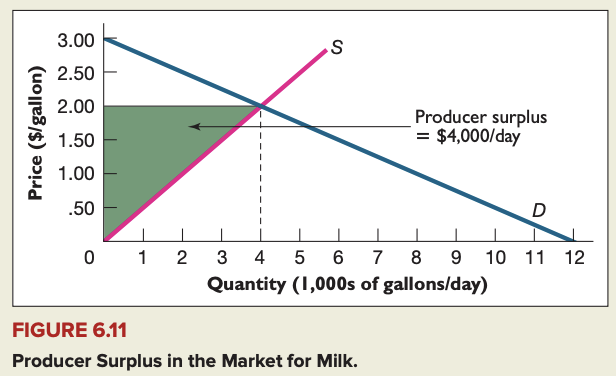

Supply and producer surplus

- Producer surplus: amount by which price exceeds the seller's reservation price.