Adjustments, Financial Statements, & the Quality of Earnings

Creation of Financial Statements:

During the Accounting Period:

Analyze business transactions

Record transactions using journal entries

Aggregate journal entries

End of the Accounting Period:

Prepare the (unadjusted) trial balance

Make adjusting entries (record & post)

Prepare financial statements

Close temporary accounts

“Regular” Journal Entry:

Recorded in the normal course of daily business transactions

May or may not involve cash (ie selling goods to customers for cash, buying inventory on account)

May or may not involve recording Revenue or Expenses

Adjusted Journal Entry (AJEs):

Recorded at the end of the accounting period

Never involves cash

Always involves Revenue or Expenses

Necessary because:

Timing differences between Revenues being earned vs receipt of cash

Timing differences between Expenses being incurred vs exchange of cash

Expenses that are difficult or inefficient to recognize on a daily basis (ie depreciation expense)

Types of Adjusting Entries:

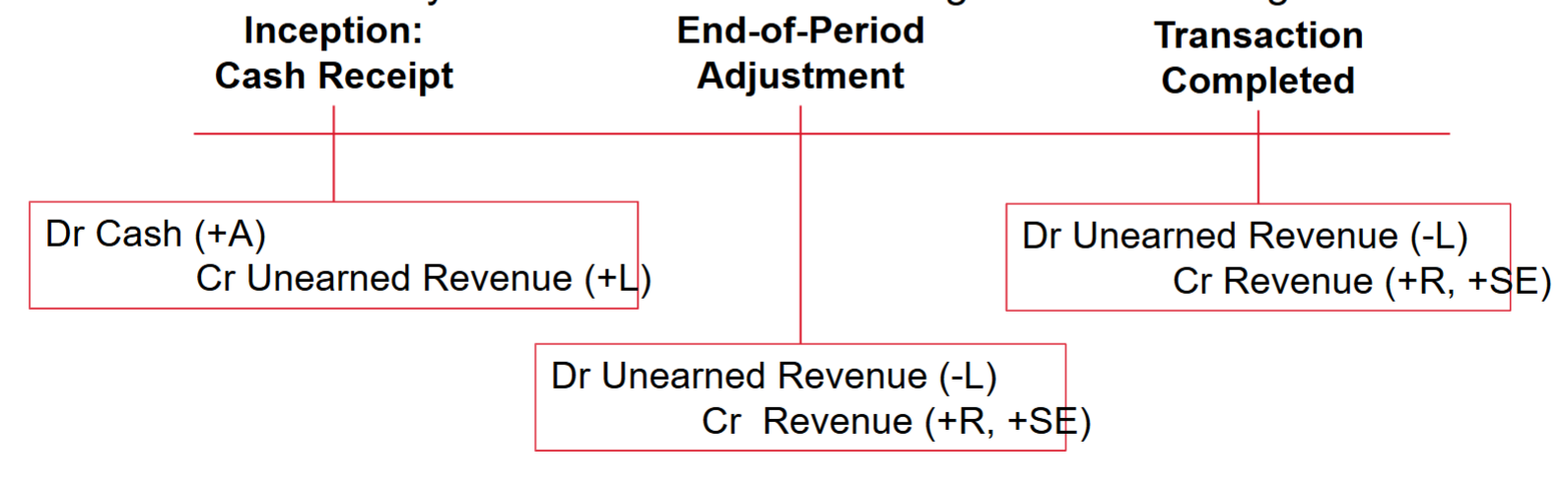

Deferred Revenue:

Revenue after cash

Inception: A liability (ie promise from future services) was recorded at the time cash was received

Adjustment: Liability is reduced to recognize revenue earned

Conclusion: Liability is eliminated & remaining revenue is recognized

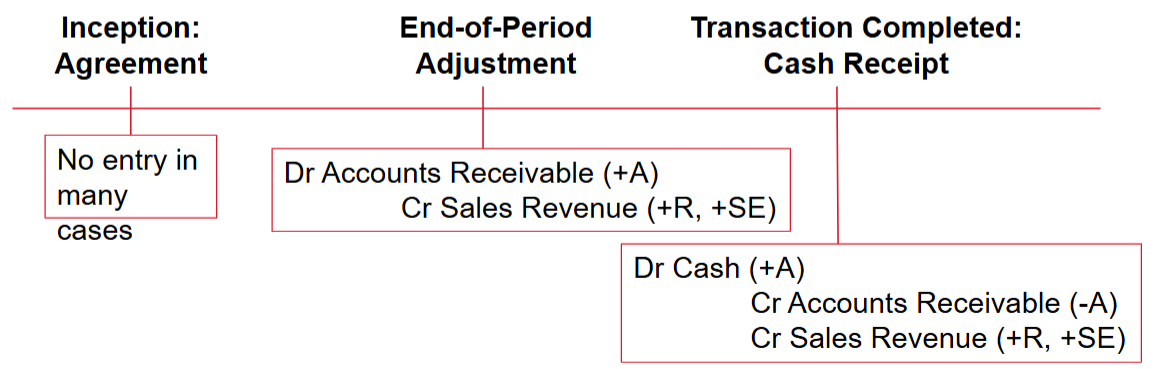

Accrued Revenue:

Revenue before cash

Inception: Reaches an agreement for future services; no transaction in most cases

Adjustment: Revenue earned for services performed; receivable is increased

Conclusion: Cash receipt recorded, receivable eliminated, & remaining revenue recognized (if any)

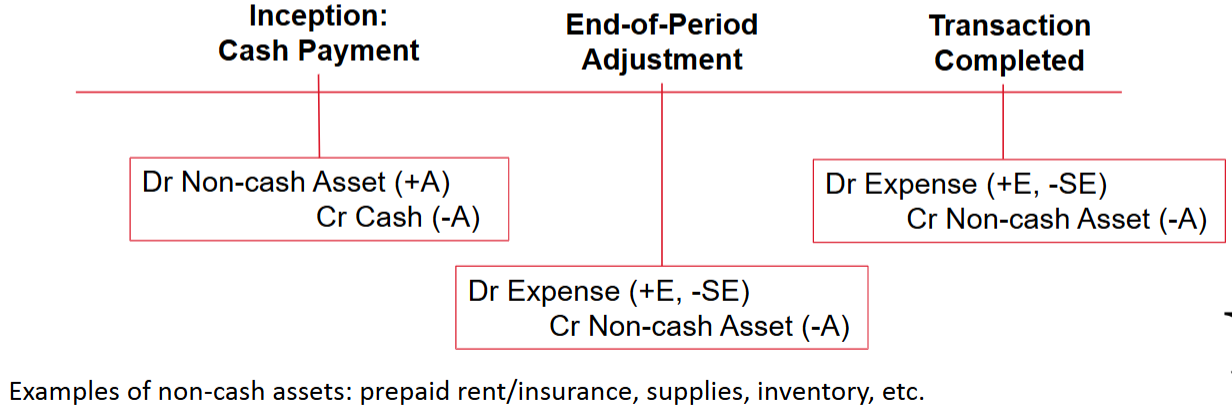

Deferred Expense:

Expenses after cash

Inception: An asset was acquired at the time cash was paid

Adjustment: Asset is used; asset balance reduced to recognize expense incurred

Conclusion: Asset is eliminated & remaining expense is recognized

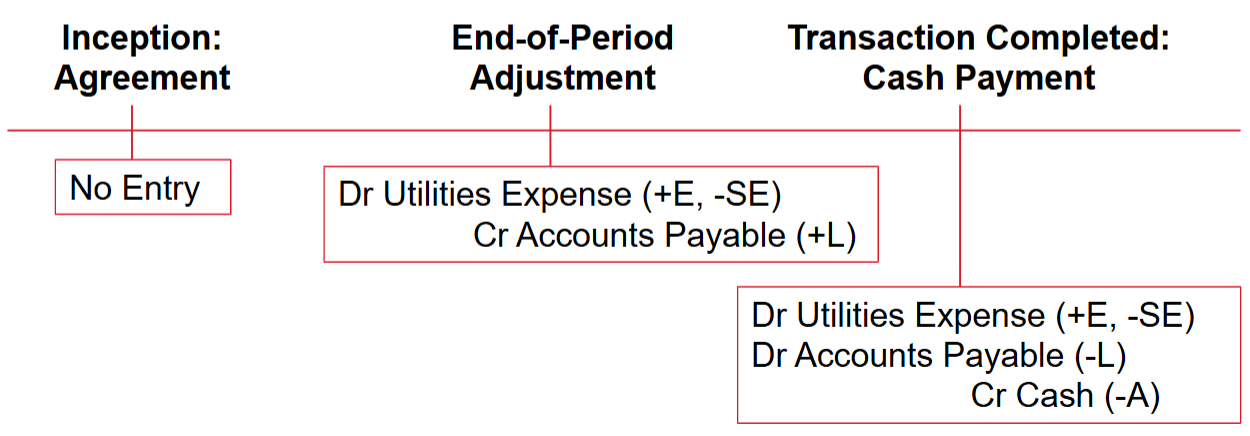

Accrued Expense:

Expenses before cash

Inception: Reaches an agreement for future services; no transaction

Adjustment: Expense incurred for services received; payable is increased

Conclusion: Cash payment made, payable eliminated, remaining expense recognized (if any)

Closing the Books:

The balance sheet provides a snapshot of a company’s resources & sources at a given date

These balances carry forward from period to period

Balance sheet accounts are permanent accounts

The income statement provides a report of performance over a period

These account balances need to be reset at zero each period so current period income is not included in future income

Income statement accounts are temporary accounts

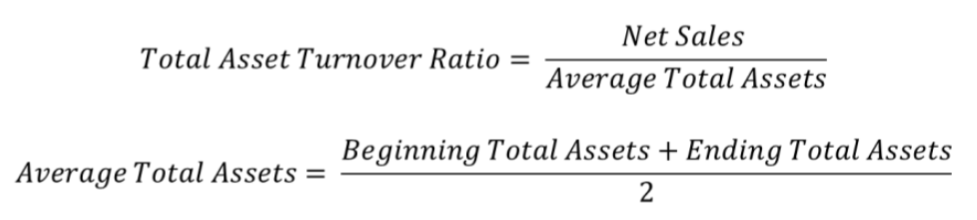

Total Asset Turnover Ratio: