Micro and Macro Unit 1

1.1

Scarcity - we have unlimited wants but limited resources

Opportunity Cost

Explicit costs - out of pocket expense

ex) money payments or exchange of items of value

Implicit costs - value of resources that could be used elsewhere

ex) resource allocations not item exchange

Positive vs Normative Statements

Positive - based on facts. Avoids value judgements (what is)

Normative - Include value judgements (what ought to be)

5 Economic Assumptions

Society has limited wants and limited resources. (scarcity)

Due to scarcity, choices may be made. Every choice has a cost. (a trade-off)

Everyone’s goal is to make choices that maximize their satisfaction. Everyone acts in their own “self-interest”.

Everyone makes decisions by comparing the marginal cost and marginal benefits of every choice.

Real-life situations can be explained and analyzed through simplified models and graphs.

1.2

Economic Systems

Command (centrally planned) Economy

In a command economy, the government makes all decisions regarding the production and distribution of goods and services, aiming to allocate resources according to a central plan.

Free Market Economy

Little government involvement in the economy. Individuals own resources and answer the three economic questions. The opportunity to make profit gives people incentive to produce quality items efficiently.

Mixed Economy

A system with free markets but also some government intervention.

Private sector - part of economy that is run by individuals and businesses.

Public sector - part of the economy that is controlled by the government,

Factor Payments - payments for the factors of production, namely; rent, wages, interest, and profit.

Economic Freedom: Producers and Consumers are free to participate in voluntary trade; the government has little involvement in the economy; Examples: you are free to open your own business, shop where you want, and own private property.

Economic Efficiency: Involves producing the socially desirable level of output and producing it at the lowest cost possible because resources are scarce and must be used wisely in an attempt to satisfy unlimited wants

Economic Security: Provides safety nets to care for individuals in the event of economic catastrophes and hardships. Examples include unemployment insurance, welfare, and food stamps.

Economic Equity: Members of the society have equal opportunities to be successful. Examples include non-discrimination laws for employment and education.

Economic Growth: Innovation is encouraged and leads to economic growth, which in turn results in an increase in the standard of living and quality of life for citizens. Examples include incentives to businesses (subsidies, etc), changes in tax codes (fiscal policy), and changes in money supply to influence interest rates (monetary policy).

Price Stability: Maintaining steady economic growth so prices do not drastically fluctuate. Examples include laws to prevent price gouging in times of disaster, maintaining appropriate fiscal and monetary policy to allow for restrained growth, and the use of price controls.

1.3

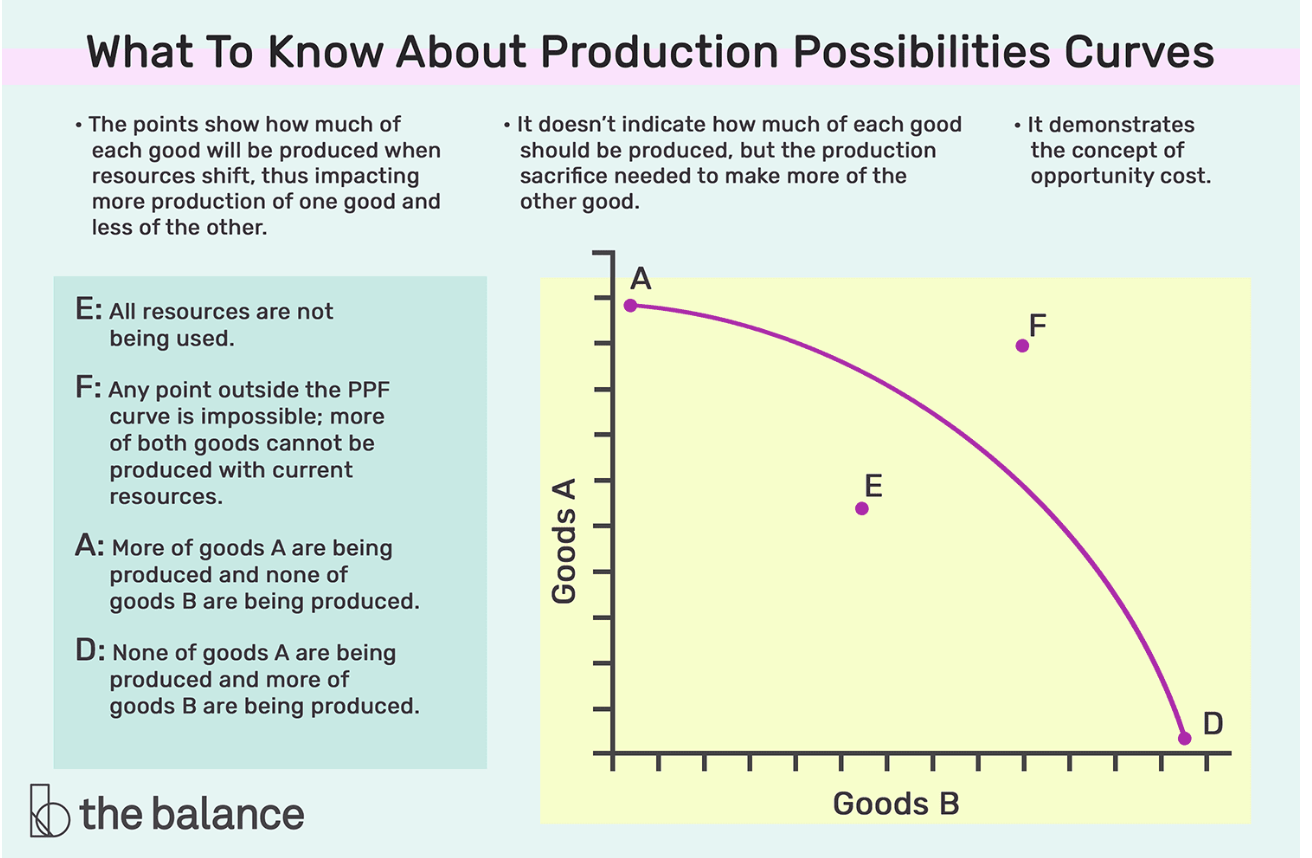

Production Possibilities Curve (PPC)

A PPC is a model that shows alternative ways that an economy can use it’s scarce resources.

Law of Increasing Opportunity Costs- concept that as you continue to increase production of one good, the opportunity cost of producing that next unit increases. This comes about as you reallocate resources to produce one good that was better suited to produce the original good.

1.4

Absolute advantage - The producer that can produce the most output OR requires the least amount of inputs (resources).

Comparative advantage - The producer with the lowest opportunity cost

Ex: Ronald has a comparative advantage in burgers because he has the lowest per unit opportunity cost.

Output questions -the amount of inputs, are the same for both countries. Only the output of each country is different.

Ex: Using the same amount of workers, the US can produce 10 planes and China can produce 3 planes.

Input Questions - The amount of output, are the same for both countries. Only the inputs for each country are different. (opposite)

OOO - Output is Other goes Over, the law of Comparative Advantages

IOU - Input is Other goes Under, the law of comparative advantage calculation

1.5

Trade-offs - all the alternatives that we give up when we make a choice

Opportunity cost - most desirable alternative given up when you make a choice.

Explicit Costs are the traditional out of pocket costs associated with making a decision

Implicit costs are the opportunity costs of making a decision

1.6

Equilibrium

MU/P = Utils/Dollar

times going | marginal utility | MU/P price = $10 | Marginal utility (go karts) | MU/P price = $5 |

1st | 30 | 3 | 10 | 2 |

2nd | 20 | 2 | 5 | 1 |

3rd | 10 | 1 | 2 | .40 |

4th | 5 | .50 | 1 | .20 |

If you only have $40 what combination of moves and go karts maximizes your utility?

3 movies and 2 go kartsTotal utility from 2 movies and 4 go karts?

7 Total utility = 75 = (30+20+10+10+5)

Utility Maximizing Rule/Consumer Equilibrium

MUx/Px = MUy/Py

Marginal Utility of the first item (x) divided by the price/cost of the first item x = marginal utility of the second item (y) divided by the price/cost of the second item (y)