Chapter 33: Interest Rates and Monetary Policy

- Monetary policy - Consists of deliberate changes in the money supply to influence interest rates and thus the total level of spending in the economy

- Interest - The price paid for the use of money

- Demand for money

- Holding money to use to purchase goods + services

- Transactions demand - The demand for money as a medium of exchange

- Level of nominal GDP determines amount of money demanded for transactions

- Money’s function as a store of value

- Asset demand - Holding money as an asset

- Money is the most liquid of all financial assets; it is immediately usable for purchasing other assets when opportunities arise

- Earns very little interest

- Total demand for money - The total amount of money the public wants to hold, both for transactions and as an asset, at each possible interest rate

- Equilibrium interest rate

- Just as in a product market or a resource market, the intersection of demand and supply determines the equilibrium price in the market for money

- Changes in the demand for money, the supply of money, or both can change the equilibrium interest rate

- An increase in the supply of money will lower the equilibrium interest rate; a decrease in the supply of money will raise the equilibrium interest rate

- Interest rates + bond prices

- Inversely related

- When the interest rate increases, bond prices fall; when the interest rate falls, bond prices rise

- Consolidated balance sheet of federal reserve banks

- Assets

- Securities - Government bonds that have been purchased by the Federal Reserve Banks

- Loans to commercial banks

- Liabilities

- Reserves of commercial banks - he Fed requires that the commercial banks hold reserves against their checkable deposits

- Treasury deposits

- Federal Reserve notes outstanding

- Tools of monetary policy

- Open market operations - Buying of government bonds from, or the selling of government bonds to, commercial banks and the general public

- When Federal Reserve Banks purchase securities from commercial banks, they increase the reserves in the banking system, which then increases the lending ability of the commercial banks (and vice versa)

- When the Fed sells government bonds, the additional supply of bonds in the bond market lowers bond prices and raises their interest yields, making government bonds attractive purchases for banks and the public

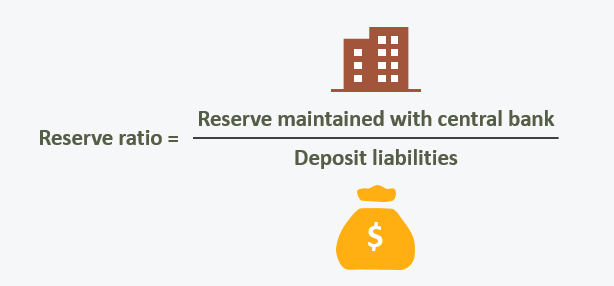

- Reserve ratio - Can be manipulated in order to influence the ability of commercial banks to lend

- Raising the reserve ratio increases the amount of required reserves banks must keep

- As a consequence, either banks lose excess reserves, diminishing their ability to create money by lending, or they find their reserves deficient and are forced to contract checkable deposits and therefore the money supply

- Discount rate - Federal Reserve Banks charge interest on loans they grant to commercial banks

- Borrowing from the Federal Reserve Banks by commercial banks increases the reserves of the commercial banks and enhances their ability to extend credit

- A lowering of the discount rate encourages commercial banks to obtain additional reserves by borrowing from Federal Reserve Banks

- When the commercial banks lend new reserves, the money supply increases

- Term auction facility - The Fed holds two auctions each month at which banks bid for the right to borrow reserves for 28-day periods

- Once they are received, Fed officials arrange them from highest to lowest by interest rate

- Guarantees that the amount of reserves that the Fed wishes to lend will be borrowed

- Targeting the federal funds rate

- Federal funds rate - The rate of interest that banks charge one another on overnight loans made from temporary excess reserves

- Banks with excess reserves desire to lend out their temporary excess reserves overnight to other banks that temporarily need them to meet their reserve requirements

- Directs the Federal Reserve Bank of New York to undertake whatever open-market operations may be necessary to achieve and maintain the targeted rate

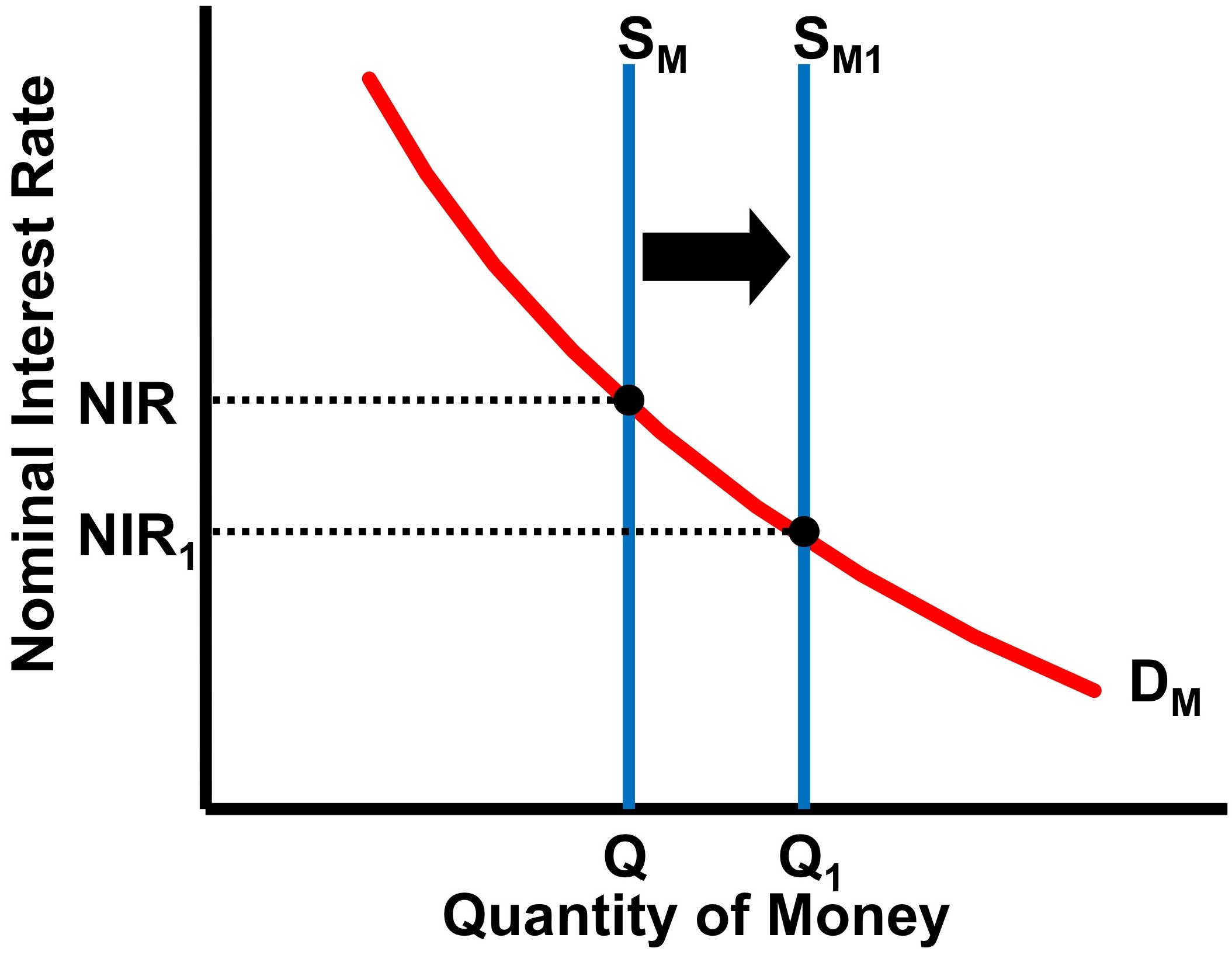

- Expansionary monetary policy - Lower the interest rate to bolster borrowing and spending, which will increase aggregate demand and expand real output

- The supply of Federal funds increases, lowering the Federal funds rate to the new targeted rate

- A multiple expansion of the nation’s money supply occurs

- Prime interest rate - The benchmark interest rate used by banks as a reference point for a wide range of interest rates charged on loans to businesses and individuals

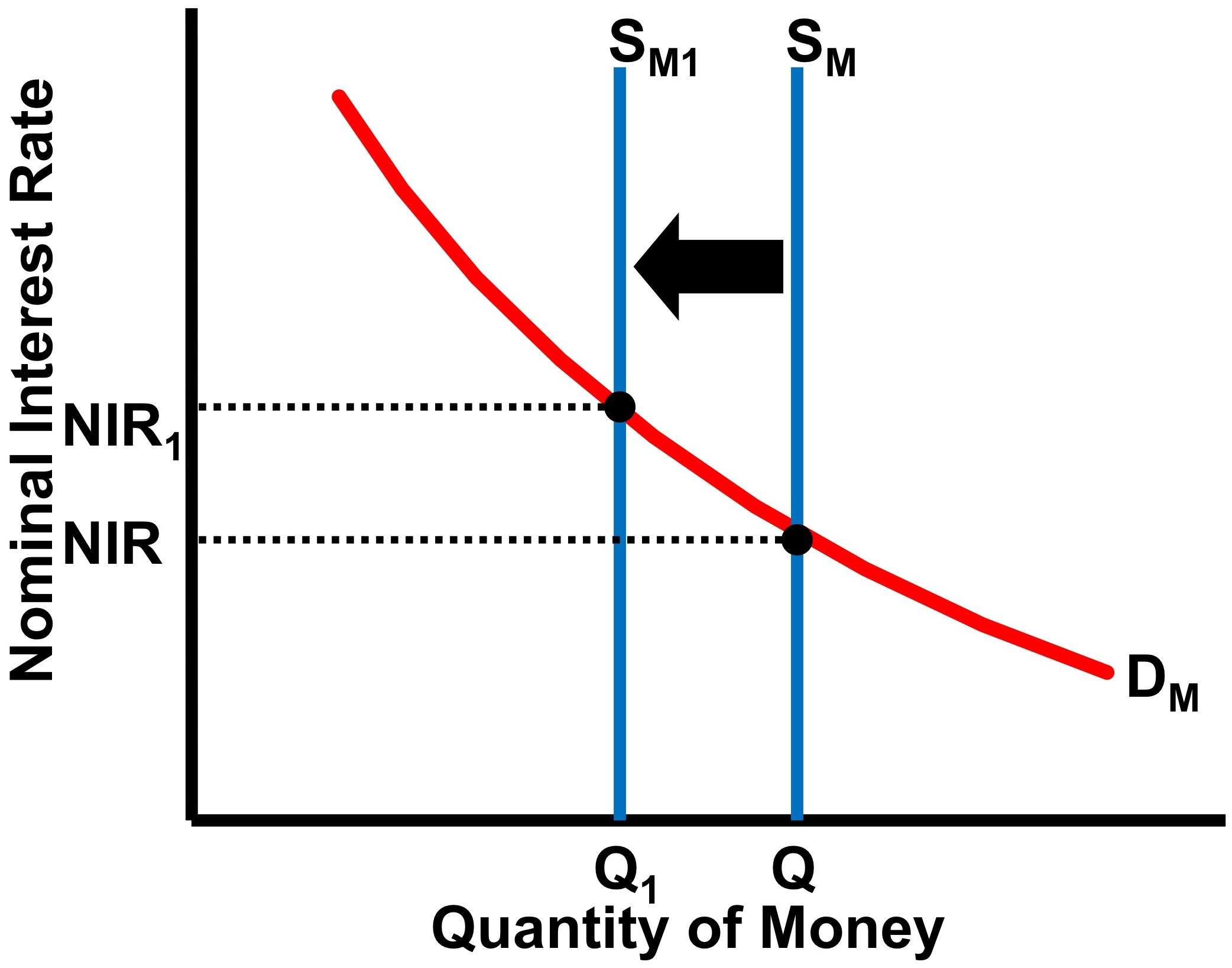

- Restrictive monetary policy - Increase the interest rate in order to reduce borrowing and spending, which will curtail the expansion of aggregate demand and hold down price-level increases

- The supply of Federal funds decreases, raising the Federal funds rate to the new targeted rate

- A multiple contraction of the nation’s money supply occurs

- Taylor rule - Assumes that the Fed has a 2 percent “target rate of inflation” that it is willing to tolerate

- For each 1 percent increase of real GDP above potential GDP, the Fed should raise the real Federal funds rate by ½ percentage point

- For each 1 percent increase in the inflation rate above its 2 percent target rate, the Fed should raise the real Federal funds rate by ½ percentage point

- Cause-effect chain

- The money supply is shown as a vertical line representing some fixed amount of money determined by the Fed

- Changes in the interest rate mainly affect the investment component of total spending, although they also affect spending on durable consumer goods (such as autos) that are purchased on credit

- Effects of an expansionary monetary policy

- Increase in excess reserves in the commercial banking system and a decline in the Federal funds rate

- An increase in the money supply will lower the interest rate, increasing investment, aggregate demand, and equilibrium GDP

- Effects of a restrictive monetary policy

- Banks will need to reduce their checkable deposits by refraining from issuing new loans as old loans are paid back

- The higher interest rate will discourage investment, lowering aggregate demand and restraining demand-pull inflation

- Monetary policy: Evaluation + issues

- Faster + more flexible than fiscal policy

- Don’t need to worry about political pressures

- Problems + complications of monetary policy

- Hindered by lags because normal monthly variations in economic activity and the price level mean that the Fed may not be able to quickly recognize when the economy is truly starting to recede or when inflation is really starting to rise

- Cyclical asymmetry

- Monetary policy may be highly effective in slowing expansions and controlling inflation but less reliable in pushing the economy from severe recession