AP Microeconomics Unit Review

==Unit 1== ==: Introduction to Economics==

@@1.1 : Scarcity@@

- Economics : study of scarcity and choice

- Individual choice : given scarcity, individuals make decisions about what to do and not to do

- Scarcity : unlimited wants, limited resources (example : land)

- Positive statement : true statement (what is)

- Normative statement : opinionated statement (what should be)

@@1.2: Resource Allocation and Economic Systems@@

- Market economy : individual producers and consumers decide what/how/and for whom to produce (limited government intervention)

- Command economy : publicly owned, a central authority will make decisions for production and consumption (has government intervention)

- Property rights : establish ownership and grants individuals the right to trade goods/services with each other

- Resources : anything that can be used to produce something else

- Factors of production :

- land (natural resources),

- labor (the effort of workers),

- capital (all manufactured resources),

- entrepreneurship (risk taking, innovation, and organization)

- Opportunity cost : value of the next-best alternative that you give up to make another choice

- Microeconomics : individuals/households/firms making decisions and how those decisions interact (ex : college vs. a job)

- Macroeconomics : behavior of the economy as a whole (ex: employment)

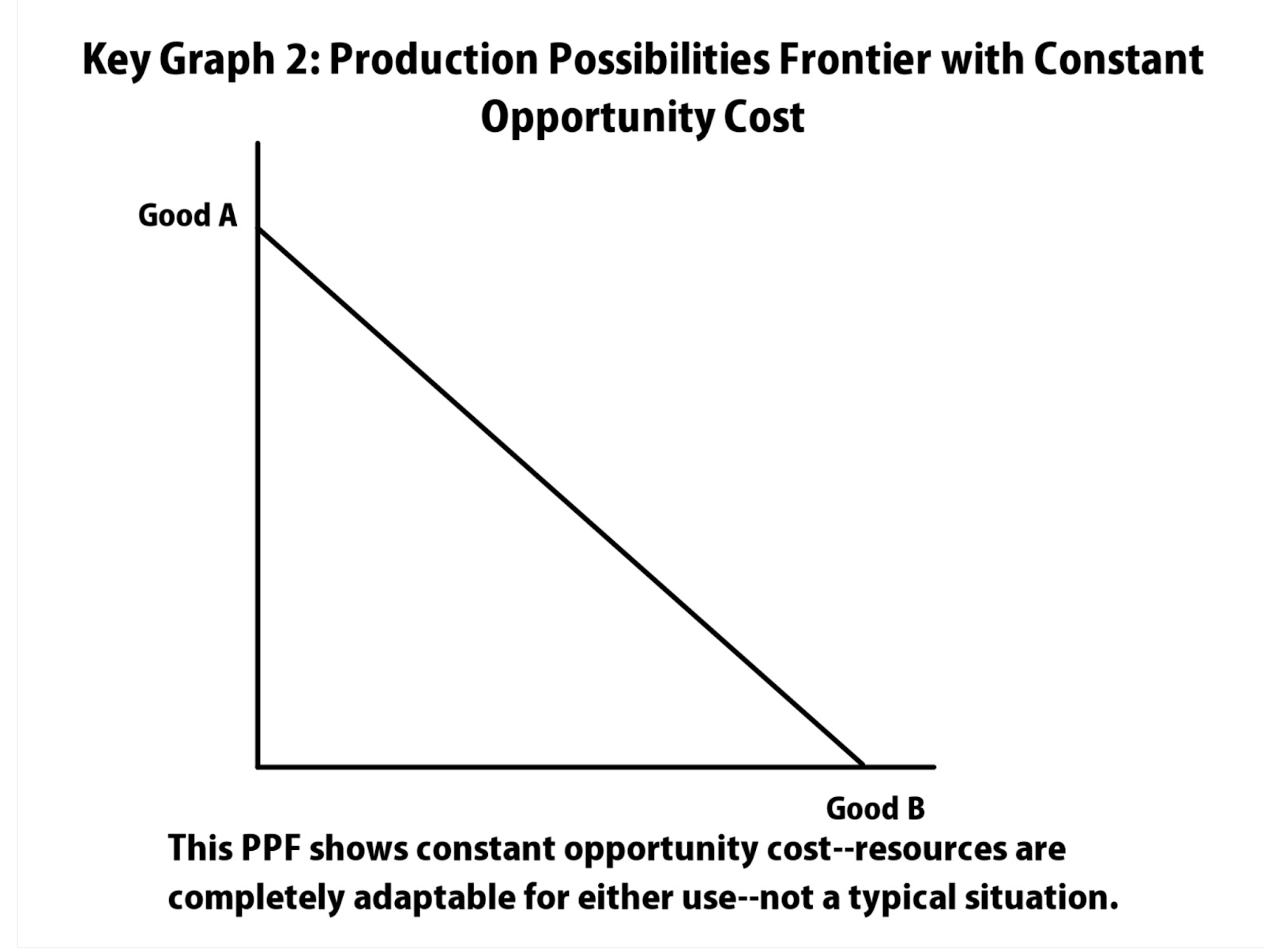

@@1.3: Production Possibilities Curve@@

- Production possibilities curve (PPC) : illustrates the trade-offs that faces an economy, compares only two goods

- Trade-offs : giving up something for something else

- If the PPC is linear, it has a constant opportunity cost, if it is curved, it has increasing opportunity costs

- Economic growth : a sustained rise in aggregate output and an increase in standard of living (causes are developments in technology, or an increase in resources)

- Productive efficiency : lowest cost possible on the PPC

- Allocative efficiency : the economy allocates resources so consumers are well off as possible, producing what is demanded

- \

@@1.4: Comparative Advantage and Trade@@

- Trade : people split up the work, and provide each other with a good in return for another

- Comparative advantage : lower opportunity cost in the production of a good (you cannot have a comparative advantage in both goods)

- Absolute advantage : higher output

@@1.5: Cost-Benefit Analysis@@

- Terms of Trade : the rate at which one good can be exchanged for another (if the price of a good obtained from trade is less than the opportunity cost of producing it, trade is beneficial)

- Capital goods: goods that make consumer goods (ex. machinery)

- Consumer goods : goods that are consumed (ex. food)

@@1.6: Marginal Analysis and Consumer Choice@@

- Utility : the measure of personal satisfaction (util is a unit of utility)

- Marginal utility : the change in total utility by consumer one additional unit of that good/service

- Principle of diminishing marginal utility : additional units of a good/service add less total utility than the previous units do

- Marginal utility per dollar : MUgood/Pgood (marginal utility of one unit of the good / price of one unit of the good)

- Optimal consumption rule : to maximize utility, marginal utility per dollar spend on each good = service in consumption bundle, MUc/Pc = MUt/Pt

==Unit 2== ==: Supply and Demand==

@@2.1: Demand@@

- Demand is downwards sloping

- Law of demand : As price increases, demand decreases, and as price decreases, demand increases

- Movement along the curve : change in price

- Shifters of demand :

- Tastes,

- related goods (substitutes + complements),

- income (normal + inferior goods),

- (# of) buyers,

- expectation of future prices

- (TRIBE)

- Substitution effect : as the price of a good increases, consumers substitute the good with another that is cheaper

- Substitutes : good/service that can be used in place of another, when price of one increases, consumers will buy more of the other (ex. coffee and tea)

- Complements : goods/services that are consumed together (ex. hamburgers and buns)

- Income effect : as income increases, people will buy more of normal goods, and less of inferior goods

- Normal good : increase in demand when consumer’s income increases (ex. oreos)

- Inferior good : increase in demand when consumer’s income decreases (ex. off brand oreos)

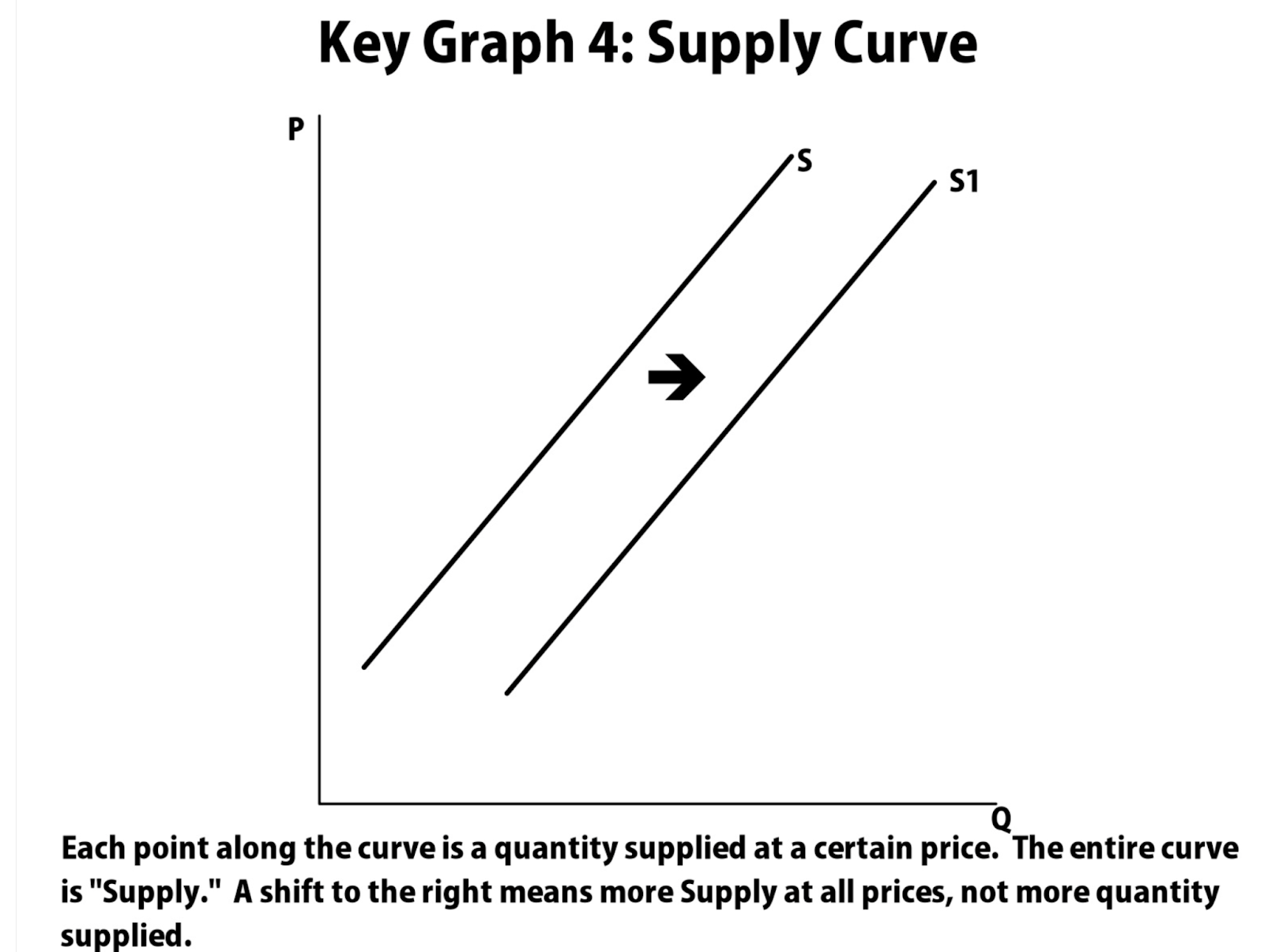

@@2.2 : Supply@@

- Supply is upwards sloping

- Law of supply : as price increases, quantity supplied also increases

- Movement along the curve : change in price

- Shifters of supply :

- input prices,

- (price of) related goods/services,

- (producer) expectations

- , number of producers

- , technology

- (I-RENT)

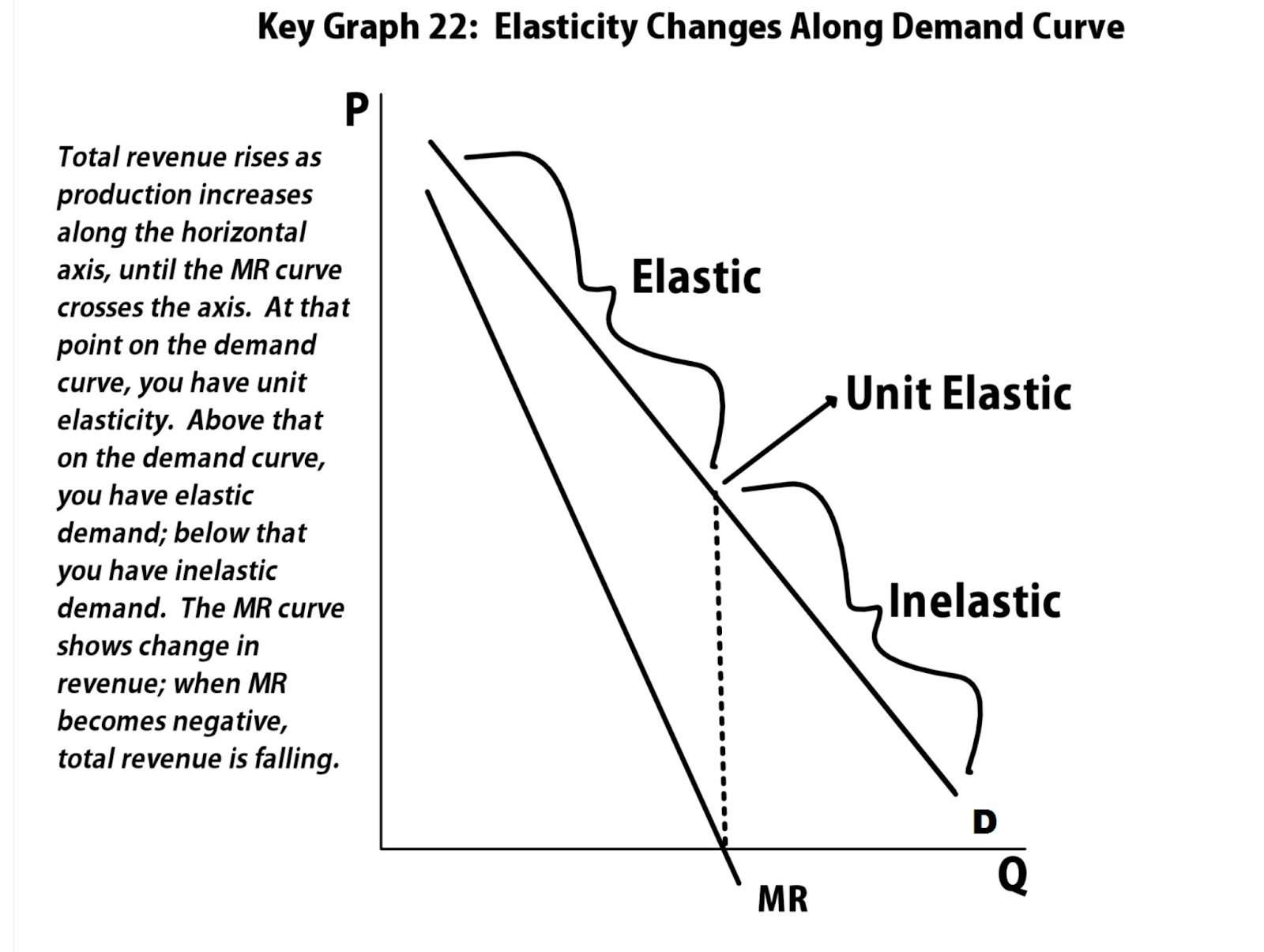

@@2.3: Price Elasticity of Demand@@

- Equation : %∆Qd/%∆P

- 0 = perfectly elastic,

- Midpoint formula : Qd2-Qd1/(Q2d+Qd1)/2 , replace with Qd with price for price

- Inelastic demand : TR correlates direct with price

- Elastic demand = TR correlates inversely with price

@@2.4: Price Elasticity of Supply@@

- Equation : %∆Qs/%∆P

- 0 = perfectly elastic,

- Inelastic : unable to respond to price change

- Elastic : short run

- Extremely elastic : long run

@@2.5: Other Elasticities@@

- Cross price elasticity of demand : %∆Qd of Good A/%∆P of good B

- negative = compliments, positive = substitutes

- Income elasticity of demand : %∆Qd/%∆income

- \ > 1 = income elastic, <1 = income inelastic, negative = inferior, positive = normal

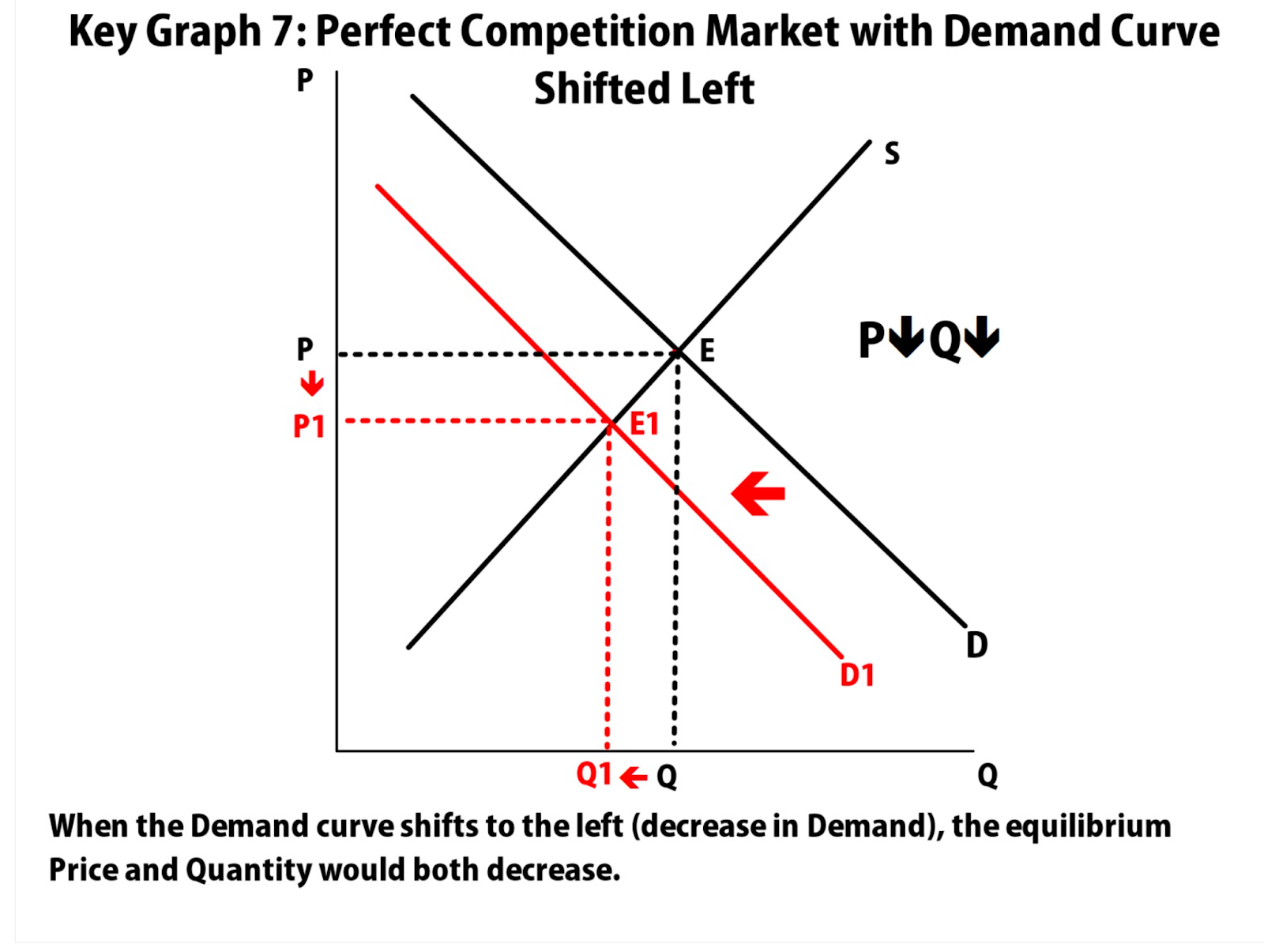

@@2.6: Market Equilibrium and Consumer and Producer Surplus@@

- Equilibrium : occurs when no one is better off doing something else

- Equilibrium = Qs=Qd

- Price below the equilibrium is shortage

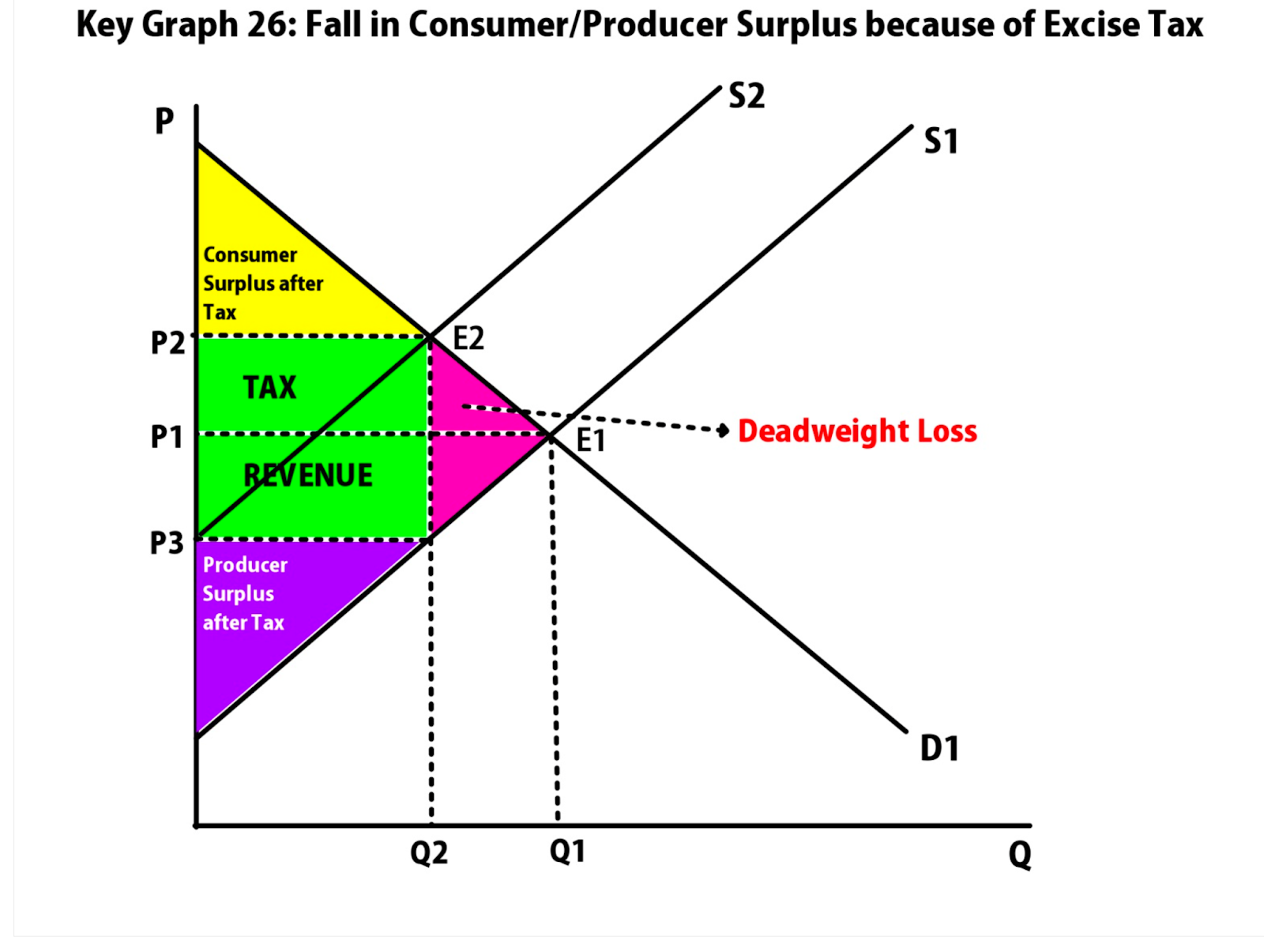

- Consumer surplus : price consumers are willing to pay - actual price

- Producer surplus : actual price -price the producer is willing to sell for

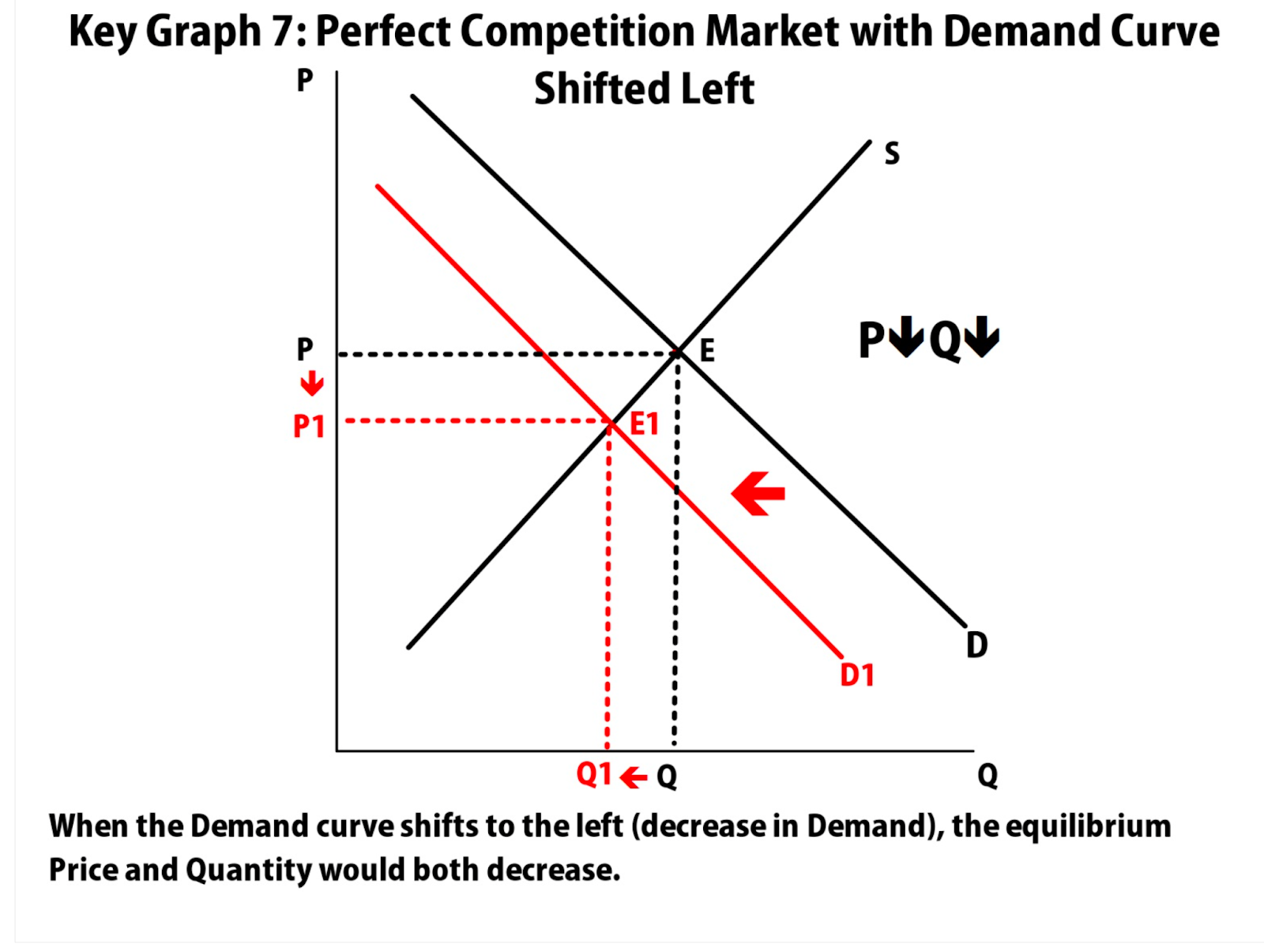

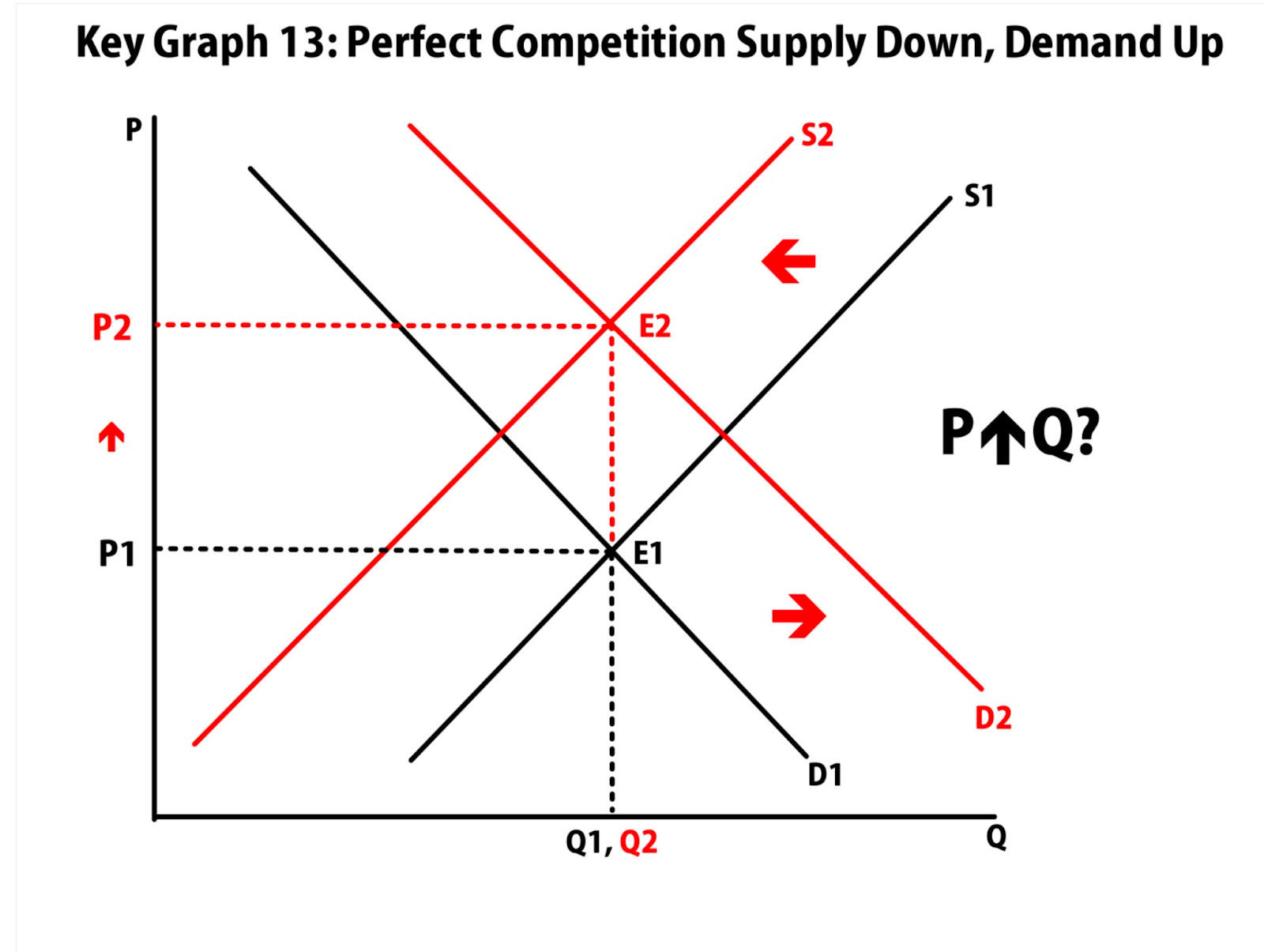

- Demand increase : price and quantity increase

- Demand decrease : price and quantity decrease

- Supply increase : price decreases, quantity increases

- Supply decrease : price increases, quantity decreases

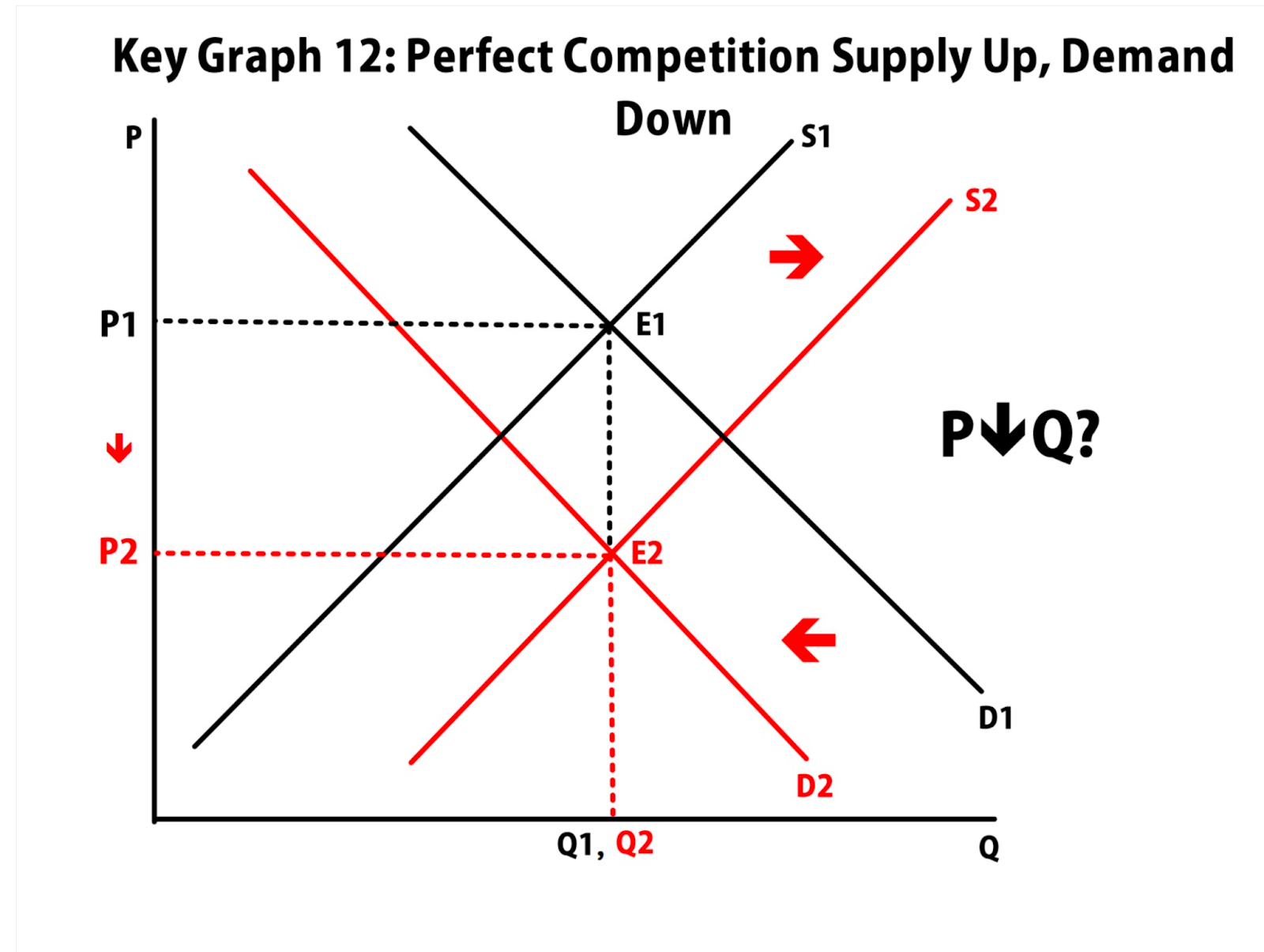

- Double shift : either price or quantity will be unknown

- Deadweight loss (DWL) : transactions that should occur, but don’t because of government intervention (calculate the area = triangle formula, ½(base x height)

- \

@@2.7: Market Disequilibrium and Changes in Equilibrium + 2.8: The Effects of Government Intervention in Markets@@

- Shortage : Qs < Qd, price is lower than equilibrium

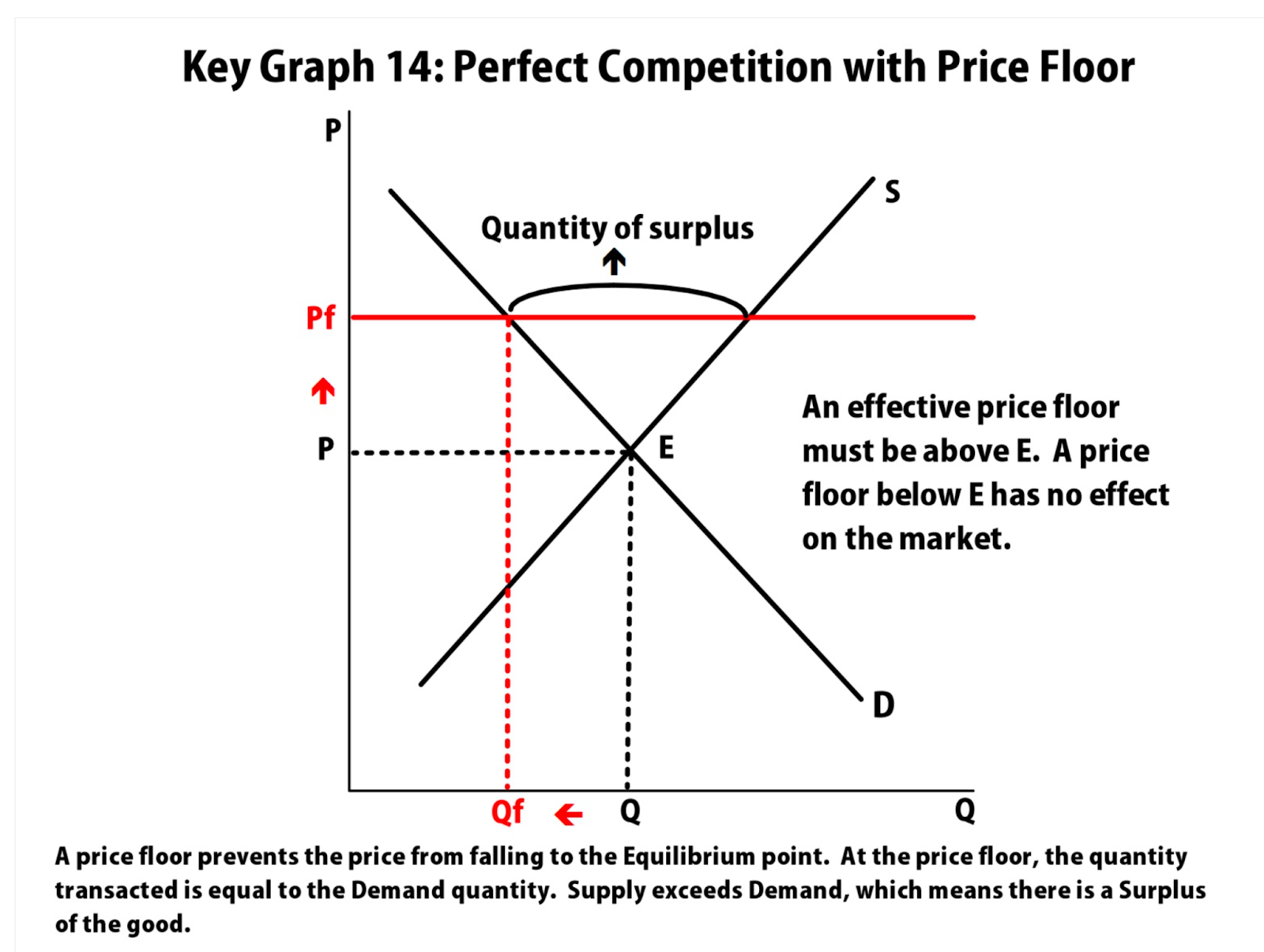

- Surplus : Qs > Qd, price is above equilibrium

- Price floor : minimum price a supplier can charge, price is set above equilibrium (causes shortage)

- Price ceiling : maximum price a supplier can charge, price is set below equilibrium (causes surplus)

- Double shift rule : when supply and demand both shift, either price or quantity will be unknown

- Quota : upper limit of a quantity that can be bought or sold (known as quantity control)

- License : gives an owner the right to supply a good/service

- Demand price : the price at which consumers will demand that quantity

- Supply price : the price at which producers will supply that quantity

- Quota rent : difference between demand price and supply price

@@2.9: International Trade and Public Policy@@

- Tariffs : tax placed on a good that is imported or exported

- Import quota : restriction on the quantity of a good that can be imported

==Unit 3:== ==Production, Cost, and the Perfect Competition Model==

@@3.1: The Production Function@@

- Production function : relation between the quantity of inputs a firm uses and the quantity of output it produces

- Fixed input : an input whose quantity doesn’t change

- Variable input : an input whose quantity can change

- Long run : time period in which all inputs can be variable

- Short run : time period in which at least 1 input is fixed

- Marginal product : change in overall output when input changes

- Marginal product of labor (MPL) : ∆Q/∆L

- Diminishing marginal returns : as input increases, the output of each input will be less than the previous input

- Output : quantity produced

- Rental rate : price of capital

- Capital : goods that are used to produce goods/services

@@3.2: Short-Run Production Costs@@

- Fixed cost : cost that doesn’t change with amount of output produced (ex. oven)

- Variable cost : cost that changes with amount of output produced

- Total cost : fixed cost + variable cost

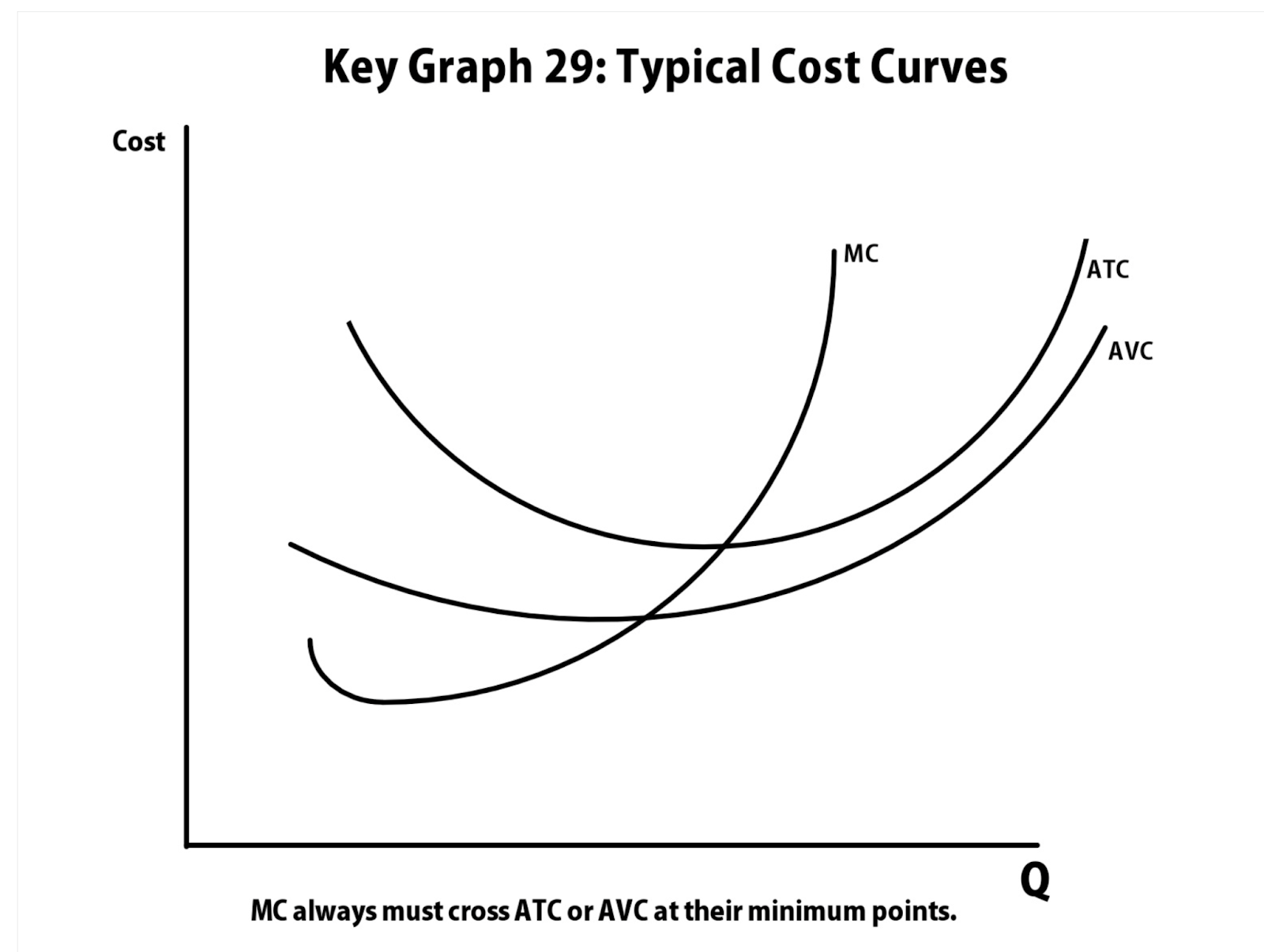

- Marginal cost : cost difference of one additional unit of output (∆TC/∆Q)

- Average fixed cost (AFC) : FC/Q

- Average variable cost (AVC) : VC/Q

- Average total cost (ATC) : TC/Q

@@3.3: Long-Run Production Costs@@

- Long run average total cost (LRATC) : same as short run ATC, but bigger

- Economies of scale : LRATC declines as output increases

- Diseconomies of scale : LRATC increaess as output increases

- Constant returns to scale : output increase directly in proportion to an increase in all inputs (ex. input doubles, output also doubles)

@@3.4: Types of Profit@@

- Economic profit : revenue - explicit cost - implicit cost, or accounting profit - implicit cost

- Accounting profit : revenue - explicit cost

- Implicit cost : not an actual cost, a cost that you could’ve been earning (ex. if you own a restaurant, the implicit cost would be the salary you would have earned as being a chef working in a different restaurant)

@@3.5: Profit Maximization@@

- MR = MC

- If you cannot have MR=MC, MR>MC

@@3.6: Firms’ Short-Run Decisions to Produce and Long-Run Decisions to Enter or Exit a Market@@

Short Run:

- Shutdown rule : as long as P > AVC, continue to produce

- If AVC > P : shutdown

- Firms can make profit or losses

Long Run :

- Exit rule : if P < ATC, exit the market

- Firms make normal profit ($0), unless monopoly or oligopoly

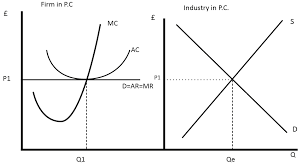

@@3.7: Perfect Competition@@

- Many firms, identical products, low/no barriers to advertisement

- Price takers

- Long run will have normal profit

- Short run can have either profit or loss

==Unit 4:== ==Imperfect Competition==

@@4.1: Introduction to Imperfectly Competitive Markets@@

| Perfect Competition | Monopolistic Competition | Monopoly | Oligopoly | |

|---|---|---|---|---|

| # of firms | Many | Many | 1 | Few |

| Type of product | Standard | Differentiated | Unique | Standard or different |

| Price control | None | Little | Yes | Some |

| Barriers to entry | None | None (few) | High | High |

- Common barriers to entry : control of scarce resources, legal barriers, high startup costs

@@4.2: Monopoly@@

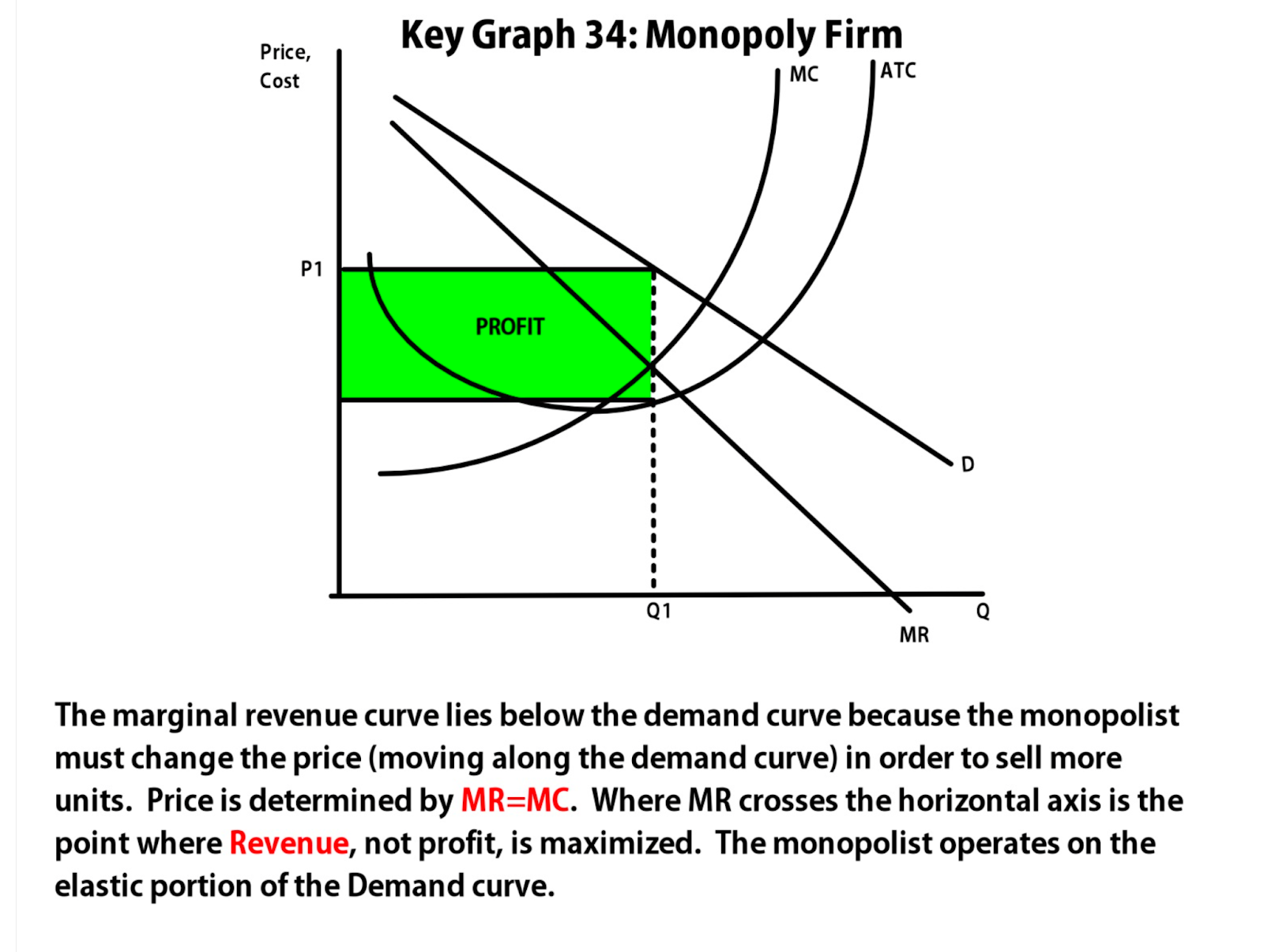

- Only producer of a good, has no close substitutes

- Downwards sloping demand curve

- Quantity is produced : @ MR = MC

- Price is : MR=MC, up to demand

- Supply curve : where MC > AVC

- Allocatively efficient due to them producing at MR=MC

- Productively inefficient because they don’t produce at the minimum of the ATC

- Natural monopoly : has large fixed costs, and long economies of scale, has downward sloping ATC curve

- Natural monopoly production point : MR=MC

- Government will correct by forcing them to set price : @ ATC=D

@@4.3: Price Discrmination@@

- To be able to price discriminate, you need market power

- Imperfect price discrimination : chargine consumers different prices based on the buyer’s willingness to pay

- Perfect price discrimnation : charges all consumers the maximum they are willing to pay, no deadweight loss, produce @ P=MC

- Example : resellers, coupons, bulk buying (costco), etc.

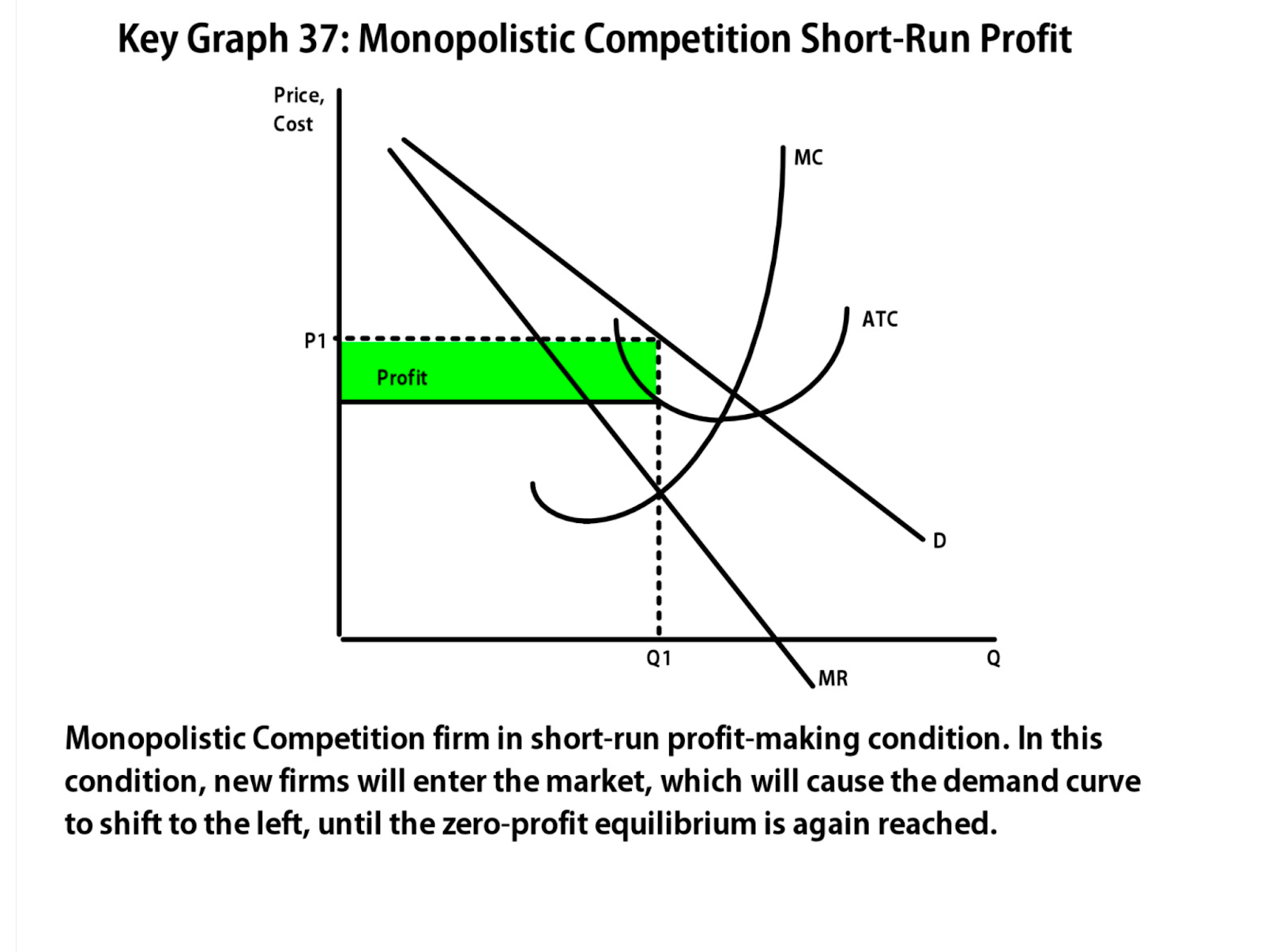

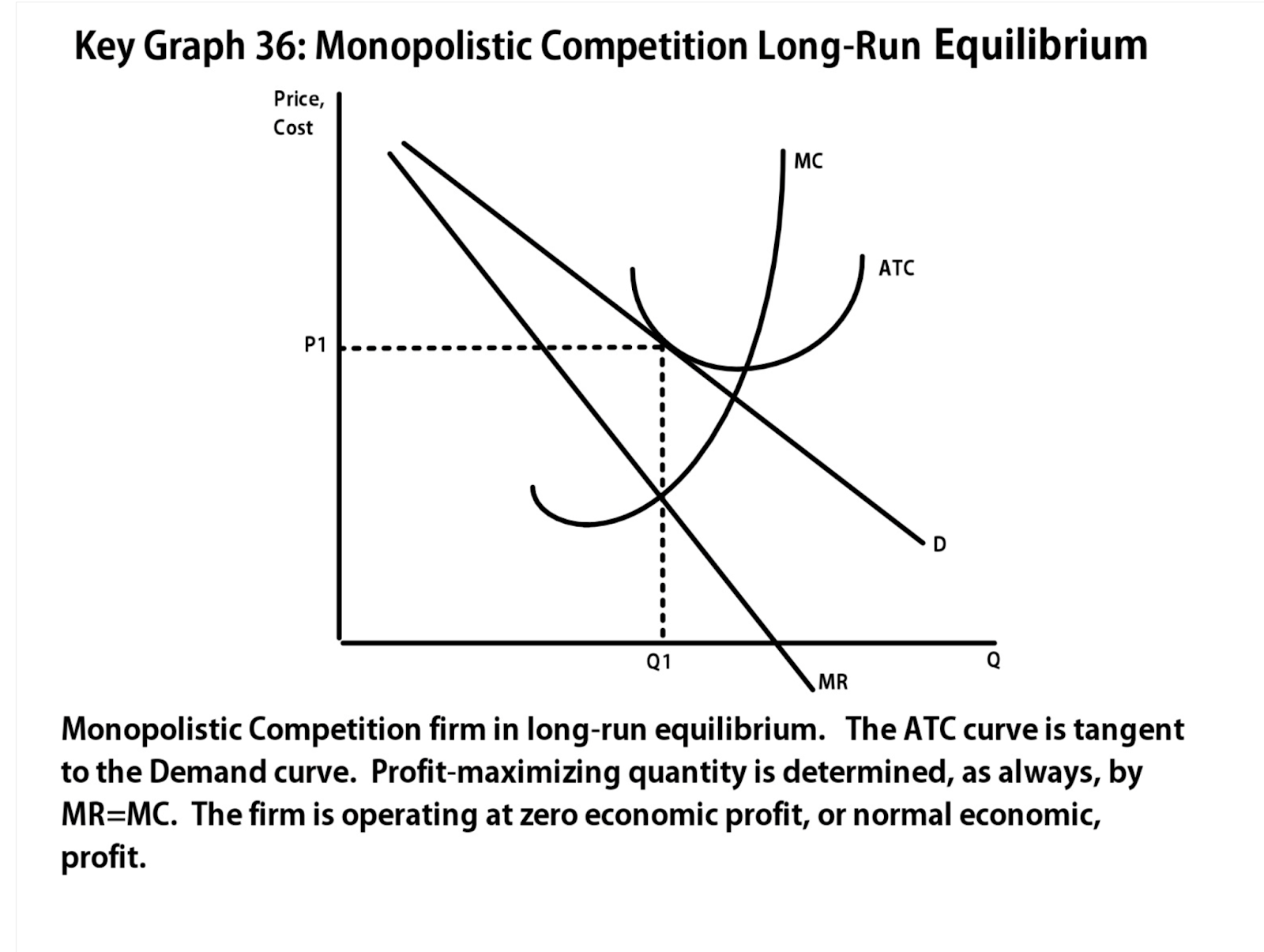

@@4.4: Monopolistic Competition@@

Characteristics

- Combines features of both a monopoly and perfect competition

- Many sellers and differentiated products

- Will use advertising to make demand more inelastic + differentiate product

- Makes profit in short run, normal profit in long run

- Allocatively inefficient (P does not equal MC)

- Productively inefficient (does not produce @ minimum of ATC, until long run)

- Downwards sloping demand curve

- Produce at MR = MC, price is MR = MC up to demand

Long Run

- Normal profit in long run

- Short run profits will attract new firms to join, which decreases the demand until the demand Curve is tangent to ATC, causing normal profits in long run

- In long run, they produce in region where economies of scales exist, because they produce in declining portion of ATC

@@4.5: Oligopoly and Game Theory@@

Oligopoly Characteristics

- Small number of firms, standard or differentiated product

- Interdependent : all the actions that a firm takes will affect the other firms in the oligopoly (if They ask why the market is an oligopoly, say it’s because they’re interdependent)

- Cartels : a group that agrees to control the price and output of a product (often form in oligopoly)

- Collusion : working together to maximize profit

- Graph is almost identical to monopoly (you will never be asked to draw them)

- Also produce same quantity and price of monopoly

Game Theory

- Payoff matrix : represents the payoff to each player to show combinations of given strategies

| Player B | |||

|---|---|---|---|

| Choice 1 | Choice 2 | ||

| Player A | Choice 1 | A1,B1 | A2,B2 |

| Choice 2 | A3,B3 | A4,B4 |

- Dominant strategy : the strategy that has a better payoff regardless of what strategy the opponent chooses

- Nash equilibrium : point where both players can do no better than the other given the choice of their opponent

==Unit 5: Factor Markets==

@@5.1: Introduction of Factor Markets@@

- Derived demand : the demand from a resource is derived by product demand

- Marginal revenue product (MRP) : the additional revenue that is generated by an additional resource/worker

- Marginal factor cost (MFC) : the additional cost of an additional resource/worker

- Least cost rule : marginal product of labor/price of labor = marginal product of capital/price of capital (MPL/PL=MPK/PK)

- Buy more of the one with a higher sum, and less of the one with a smaller sum (to explain, as you increase, diminishing marginal returns kicks in)

@@5.2: Changes in Factor Demand and Factor Supply@@

- Shifters of demand for labor

- Change in demand for the product

- Change in the productivity of the resource

- Change in price of substitutes and complements

- Shifters of supply for labor

- # of qualified workers (ex. immigrants)

- Government regulation

- Leisure (causes supply to shift to left)

@@5.3: Profit-Maximizing Behavior in Perfectly Competitive Factor Markets@@

- Market curve : standard supply and demand curve

- Equilibrium wage in the market : establishes the wage that firms will pay workers

- MRP=MRC!!!!

- will not hire if MRC>MRP

@@5.4: Monopsonistic Markets@@

- Many sellers, one buyer

- Monopsonies pay a lower wage and hire less than perfect competition

- MRP=MFC

- MFC > supply

- example of imperfect competition

==Unit 6: Market Failure and the Role of Government==

@@6.1: Socially Efficient and Inefficient Market Outcomes@@

- Socially efficiency is when resources are allocated effectively

- MSB=MSC !!

- Allocatively Efficient Points

- Perfectly competitive market : S=D, MB=MC

- Perfectly competitive firm : P=MC

- Perfectly competitive labor market : W=MRP (total economic surplus : MSC=MSB)

- Causes of Market Failure

- Market power (imperfectly competitive markets)

- Asymmetric information (lack of info provided by buyers and sellers)

- Positive and negative externalities

- Insufficient production of public goods

- Government policies used to get rid of DWL

- Taxes

- Subsidies

- Reguations

- Public prodivions

- Market failure : exists when firms produce @ MPC=MPC, S=D

- The government tries to get them to produce @ MSC =MSB

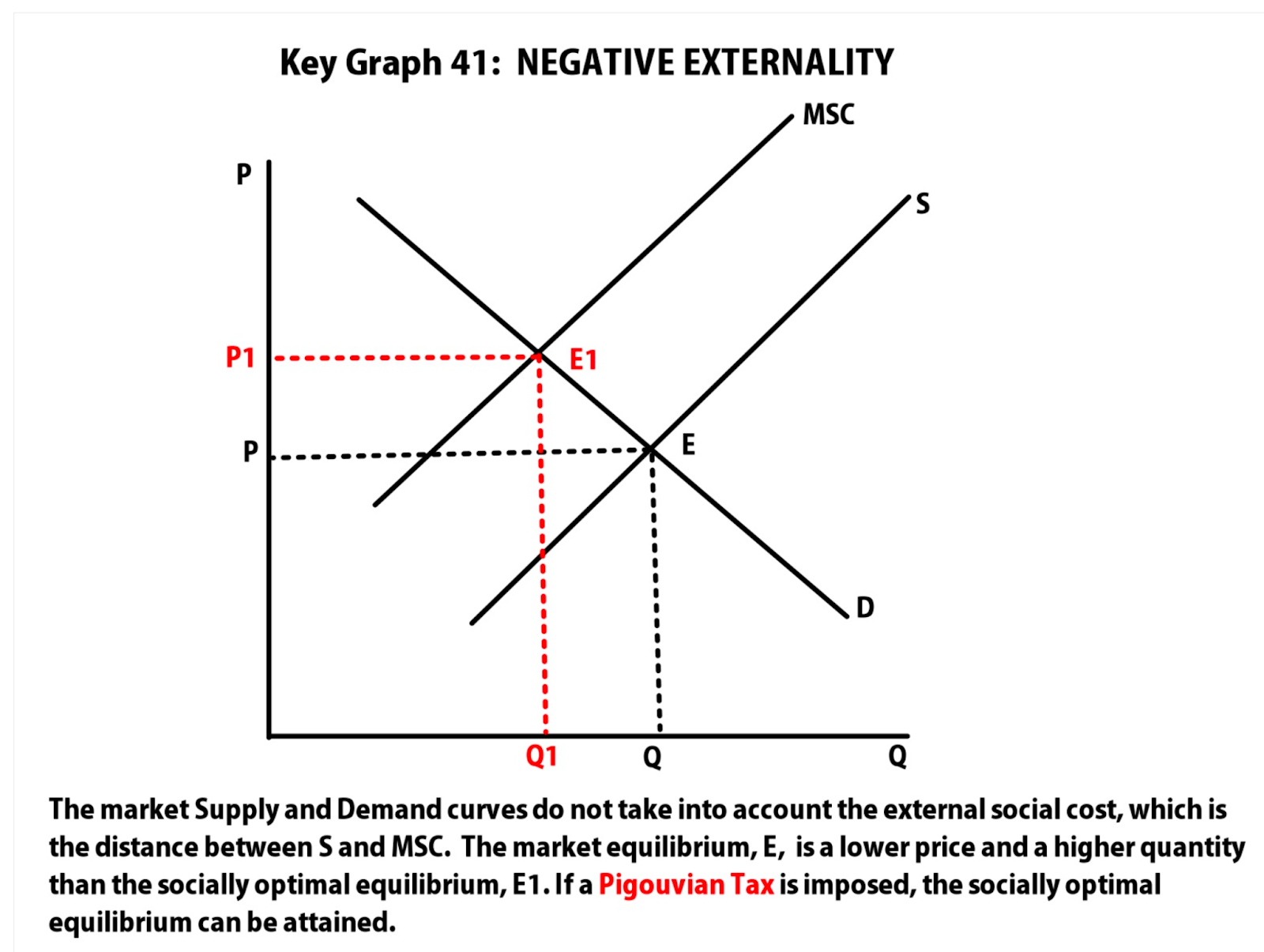

@@6.2: Externalities@@

- Externality : when external cost/benefit is placed on members of society who did not pay for them

- MSB does not equal MSC

- Negative externality : when someone uses a product, it decreases the benefit of others (ex. smoking), MSC > MPC (correct with per unit tax)

- Positive externality : when one uses a product, others benefit (ex. education) MSC < MPC (correct with subsidy)

@@6.3: Public and Private Goods@@

- Rivalrous good : if someone consumers a product, others cannot

- Rivalrous : food, shoes, etc

- Nonrivalrous : national defense, fireworks, etc

- Somewhere in middle : schools, roads, etc

- Excludable good : non payers can be prevented from enjoying the benefits

- Excludable : food, school, etc

- Nonexcludable : national defense, air, etc

- Public goods : underproduced due to freeloader problem

- Examples : national defense, law enforcement, etc

- Freeloader problem : people can enjoy the benefit of a good/service without paying

- Government will provide subsidies to producers

- Private goods : goods produced by private markets, can be excludable

@@6.4: The Effects of Government Intervention in Different Market Structures@@

- Causes of inefficient markets

- Market power

- Externalities

- Nonrival and nonexcludable goods (public goods)

- Forms of government intervention

- Taxes

- Subsidies

- Price floors/ceilings

- Regulation

- Per unit subsidy : gives benefits per unit

- Perfect competition : MC, ATC, AVC decreases, price doesn’t change (price taker)

- Monopolistic competition : MC, ATC, price decreases (price maker @ MR=MC)

- Lump sum subsidy : gives benefit no matter how many units

- Taxes will always shift supply curve to the left in long run, profits decrease

- Per unit tax : increase MC, ATC, and AVC

- Perfect competition : MC, ATC, AVC increases, price doesn’t change (price taker)

- Monopolistic competition : MC, ATC, price increases (price maker @ MR=MC)

- Lump sum tax : only increase ATC

- won’t change output level

- Non price regulation : works like taxes, they ensure competition/environmental protection/health and safety

- Antitrust policy : promote competition and prevents monopolies

- Antitrust laws

- Lawsuits

- Price controls

- Subsidies

- Price ceiling : sets minimum price

- Perfect competition : causes shortage

- Monopolistic competition : becomes MR curve, price and output decreases

- Price floor : sets maximum price

- Perfect competition : leads to surplus

- Monopsony : wages go up and workers go up

6.5: Inequality

- Income distribution : measures % of income that goes to individuals in different percentiles/brackets

- In a system with perfectly equality : everyone would receive equal shares of income

- Income : wages, rent, interest, profit

- Lorenz curve : measures the distribution of income equality (you want to be as close of possible to the perfect equality line as possible)

- Gini coefficient : A/(A+B)

- Closer to 0, more equality

- Closer to 1, the more inequality

- Causes of income inequality

- Supply + demand in labor market

- Human capital

- Discrimination

- Inheritance

- Bargaining power

- Etc

- Policies to address inequality

- Taxes + transfers

- Minimum wage laws

- Anti-poverty program

- Income protection program

- Scholarships

- Taxes :

- Proportional : everyone pays the same percentage of their income (no impact on income distribution)

- Progressive : taxes are higher % on people earning a higher income (reduces income inequality)

- Regressive : taxes are lower % on people earning a higher income (increases income inequality)