Chapter 12: The Demand for Resources

Significance of resource pricing (determining the prices that should be set for certain resources)

- Money-income determination

- Cost minimization

- Resource allocation

- Policy issues

Marginal productivity theory of resource demand

- Purely competitive product + resource market

- Wage taker in competitive resource market

- Derived demand - Resource demand derived from demand of products that resources used to produce

- Resource indirectly satisfy consumer wants

Marginal revenue product

- Marginal product (MP) - Additional output resulting from using an additional unit of labor

- Diminishing marginal returns begin w/ 1st worker hired

- Marginal revenue product (MRP) - The change in total revenue resulting from the use of each additional unit of a resource

Employing resources

- Marginal resource cost (MRC) - The amount that each additional unit of a resource adds to the firm’s total (resource) cost

- MRP = MRC - It will be profitable for a firm to hire additional units of a resource up to the point at which that resource’s MRP is equal to its MRC

MRP as resource demand schedule

- MRC of labor = Market wage rate

- Hire until market wage rate = MRP

- The MRP schedule constitutes the firm’s demand for labor because each point on this schedule (or curve) indicates the number of workers the firm would hire at each possible wage rate

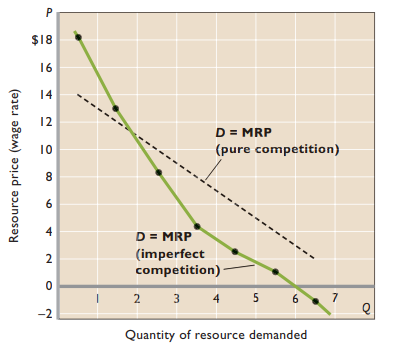

Resource demand under imperfect product market

- Marginal product diminishes and product price falls as output increases → MRP decreases

- Resource demand curve less elastic than that of purely competitive curve

- Doesn’t expand quantity of labor employed as much

- Less responsive to resource price cuts

Market demand for resources

- The total, or market, demand curve for a specific resource shows the various total amounts of the resource that firms will purchase or hire at various resource prices, other things equal

Determinants of resource demand

- Derived from product demand + depends on resource productivity

- Increase in demand for product → Increases demand for resource used in production

- Changes in productivity

- Quantities of other resources

- Technological advance

- Quality of variable resource

- Average level of wages higher in industrially advanced nations

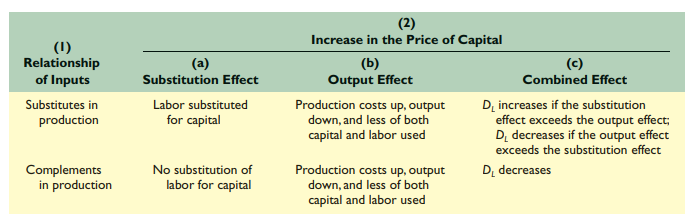

Changes in prices of other resources

- Substitute resources

- Substitution effect - A firm will purchase more of an input whose relative price has declined and, conversely, use less of an input whose relative price has increased

- Output effect - The firm will purchase more of one particular input when the price of the other input falls and less of that particular input when the price of the other input rises

- Net effect - If the substitution effect outweighs the output effect, a decrease in the price of capital decreases the demand for labor. If the output effect exceeds the substitution effect, a decrease in the price of capital increases the demand for labor

- Complementary resources

- An increase in the quantity of one of them used in the production process requires an increase in the amount used of the other as well, and vice versa

- When labor and capital are complementary, a decline in the price of capital increases the demand for labor through the output effect

Occupational employment trends

- Increases in labor demand for certain occupational groups result in increases in their employment; decreases in labor demand result in decreases in their employment

- Demand for service workers increasing rapidly

- Growing demand for health services

- Fast growing occupations related to computers

- More technological change + computerized equipment → Replacing many jobs

Elasticity of resource demand - The sensitivity of resource quantity to changes in resource prices

- Determinants

- Ease of resource substitutability - More easily substituted → More elastic demand

- Elasticity of product demand

- Ratio of resource cost to total cost

Least cost combination of resources - The cost of any output is minimized when the ratios of marginal product to price of the last units of resources used are the same for each resource

- Marginal product of labor / Price of labor = Marginal product of capital / Price of capital

- In achieving the cost-minimizing combination of resources, the producer considers both the marginal-product data and the price (costs) of the various resources

Profit-maximizing rule - When each resource is employed to the point at which its marginal revenue product equals its resource price

- MRP / P = MRP / P = 1

- If a firm is maximizing profit, then it must be using the least-cost combination of inputs to do so

Marginal productivity theory of income distribution - Income is distributed according to contribution to society’s output

- Critics

- Inequality - The distribution of income resulting from payment according to marginal productivity may be highly unequal because productive resources are very unequally distributed in the first place

- Possible market imperfections - The marginal productivity theory of income distribution rests on the assumptions of competitive markets, but not all labor markets are highly competitive