Monopolistic Competition and Oligopoly - chapter 15

15.1. Oligopoly and Monopolistic Competition

- Oligopoly: a market with only a few firms that sell a similar good or service

- Firms tend to know their competition and each firm has some price-setting power, but no one has total market control

- monopolistic competition: a market with firms that sell goods and services that are similar, but slightly different

- These firms aren’t necessarily price takers, but they still face competition in the long run

- product differentiation: when goods are close but imperfect substitutes

15.2. Monopolistic Competition in the Short Run

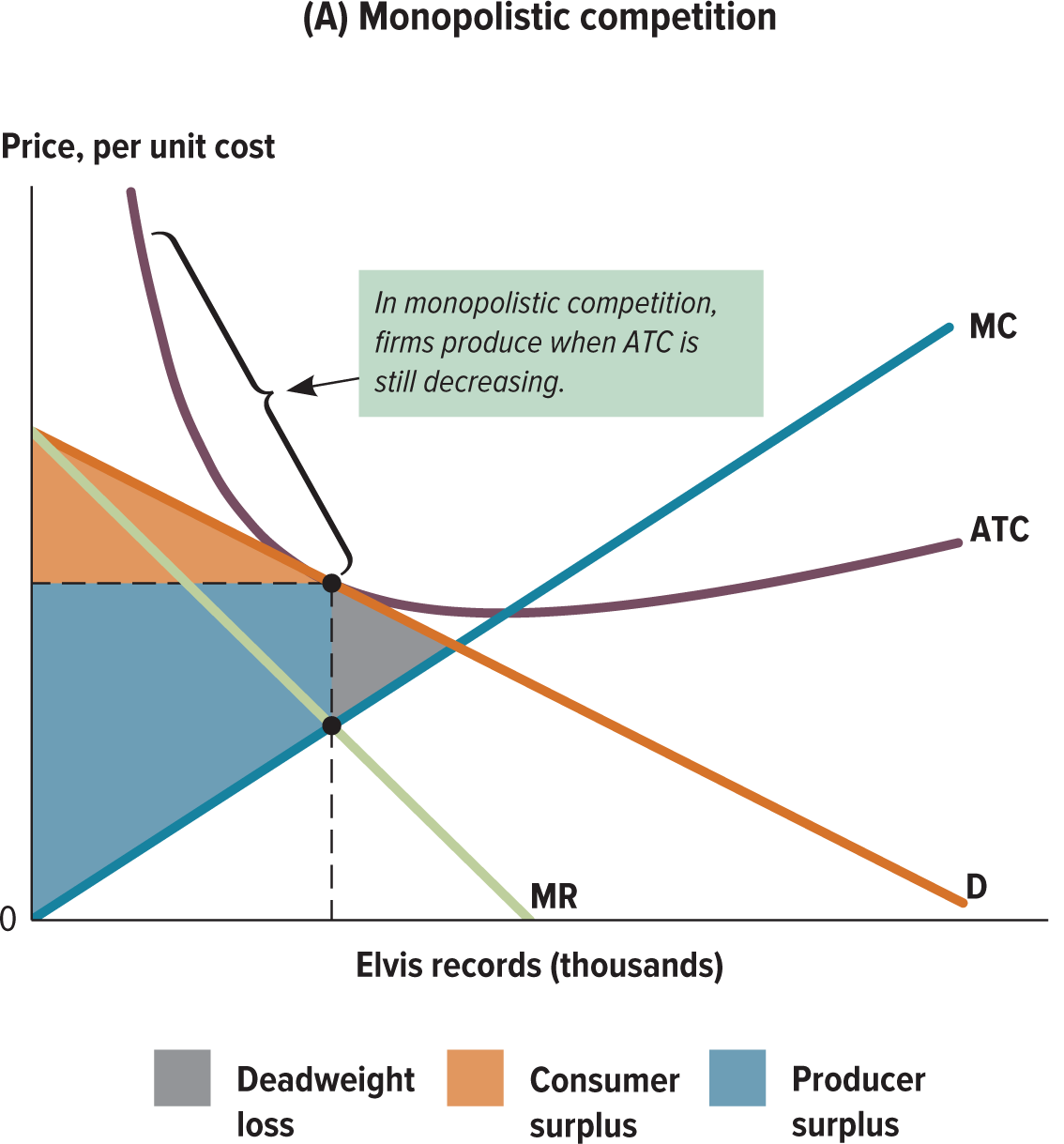

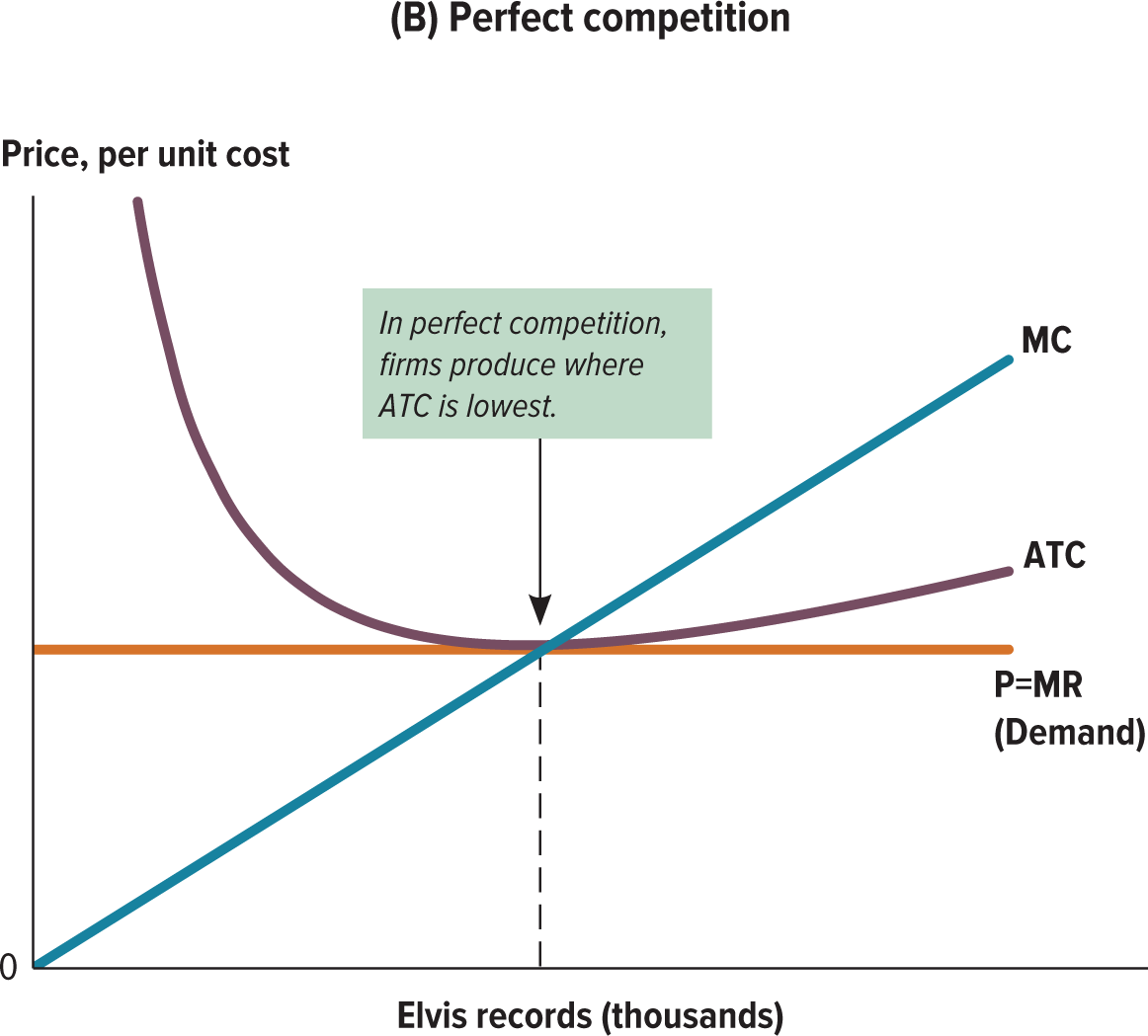

- In the short-run, monopolistically competitive firms behave like monopolists

- They face a downward-sloping demand curve and cannot change the price without causing a change in the quantity consumers demand

- The profit-maximizing production quantity is at the point where the marginal revenue (MR) curve intersects the marginal cost (MC) curve

- The profit-maximizing price is determined by the point on the demand curve that corresponds to this quantity

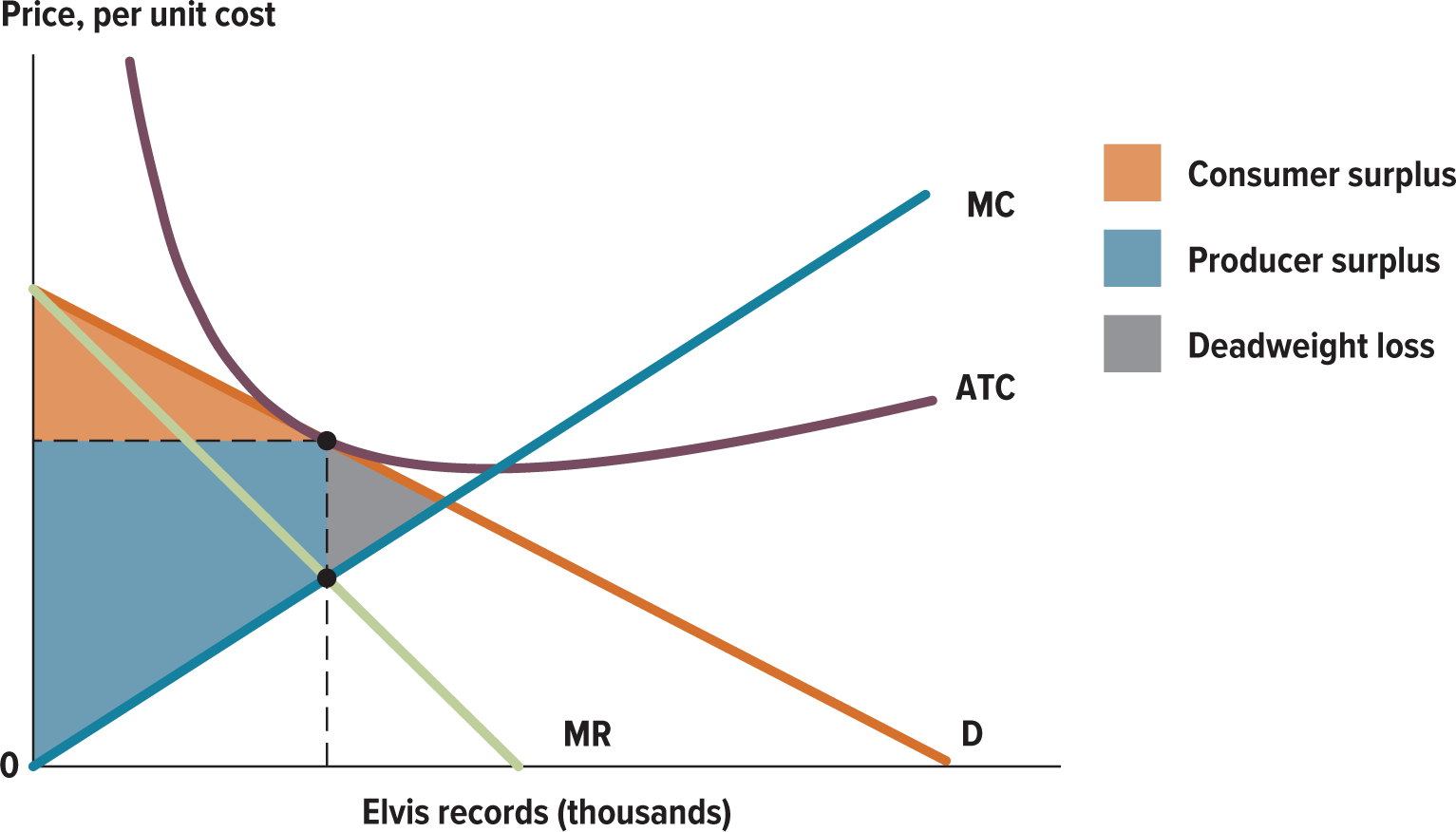

15.3. Monopolistic Competition in the Long Run

- In the long run, monopolistic competition has some features in common with monopoly and others in common with perfect competition

- Just like a monopoly, a monopolistically competitive firm faces a downward-sloping demand curve, which means that marginal revenue is less than price

- Marginal cost is also less than price

- Like a firm in a perfectly competitive market, however, a monopolistically competitive firm earns zero economic profits in the long run

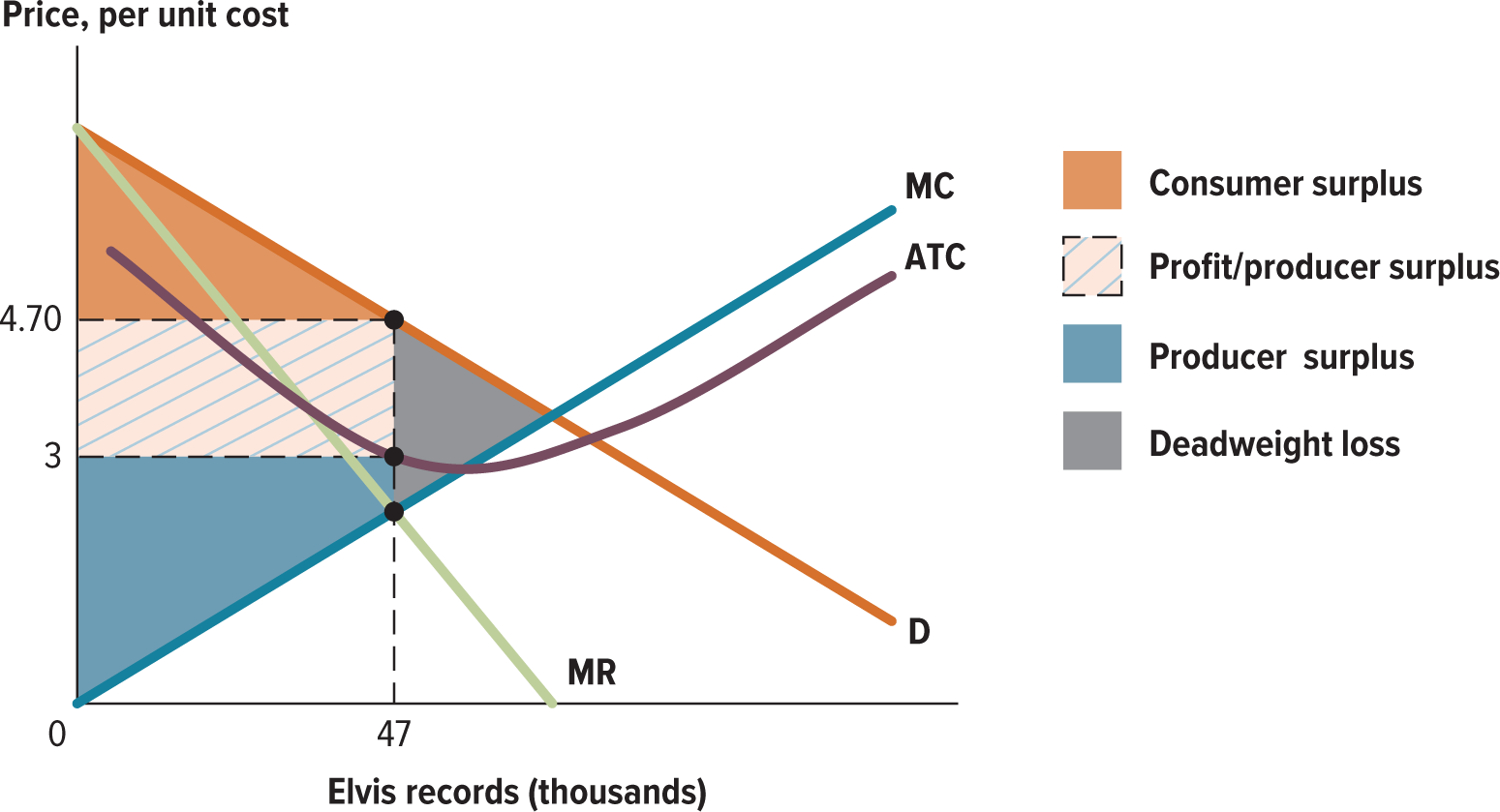

15.4. The Welfare Costs of Monopolistic Competition

- Like any deviation from the equilibrium price and quantity that would prevail under perfect competition, monopolistic competition is inefficient

- Because firms maximize profits at a price that is higher than marginal cost, some mutually beneficial trades never occur

- This means that there is a deadweight loss

- The market doesn’t maximize total surplus

- Regulating monopolistically competitive markets to increase efficiency is difficult, and it usually comes at the expense of product variety

15.5. Product Differentiation, Advertising, and Branding

- Producers invest in advertising to convince consumers that their products are different from other similar products

- The less substitutable a good seems with other goods, the less likely consumers are to switch to other products if the price increases

- Producers have an incentive to differentiate their products, either by making them truly different or by convincing consumers that they are different

- Through advertising and branding, firms either explicitly give the desired information to the consumer or signal the quality of their products

15.6. Oligopolies in Competiton

- Oliogopolists make strategic decisions about price and quantity that take into account the expected choices of their competitors

- Unlike price-taking firms in a competitive market, an oligopolist produces a quantity that affects the market price

- The increase in profit retained from an additional unit of output is called the price effect

- Typically, an oligopolistic firm will increase output until the positive quantity effect outweighs the negative price effect

15.7. Compete or Collude?

- An oligopolist has an incentive to produce more output than is profit maximizing for the market as a whole, driving down price and imposing costs on its competitors

- Collusion: the act of working together to make decisions about price and quantity

- Firms can maximize industry profits by producing the equivalent monopoly quantity and splitting revenues

- Each firm involved always has an incentive to renege on the agreements since a firm could earn higher profits by competing

- dominant strategy: the best strategy for a player to follow, no matter what strategy other players choose

- Nash equilibrium: an equilibrium reached when all players choose the best strategy they can, given the choices of all other players

- Will occur when all firms play their dominant strategies or when no players have a dominant strategy

- When the equilibrium is reached, no one has an incentive to break it by changing his strategy

- If firms recognize their production decisions as a repeated game, with future profits in mind, a firm may take an initial chance that the other firm will hold up its end of an initial agreement to collude

- Cartel: a number of firms or groups that collude to make production decisions about quantities or prices

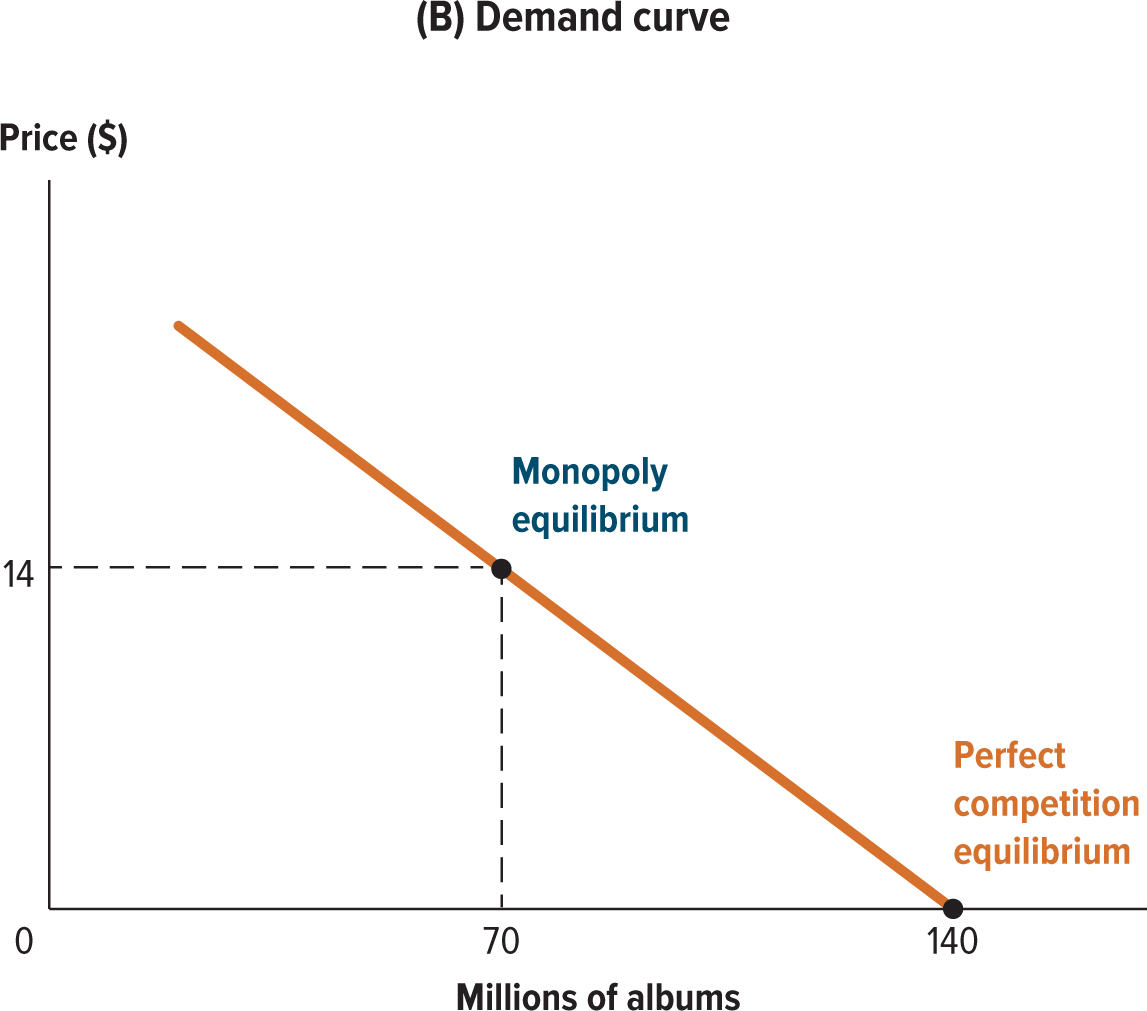

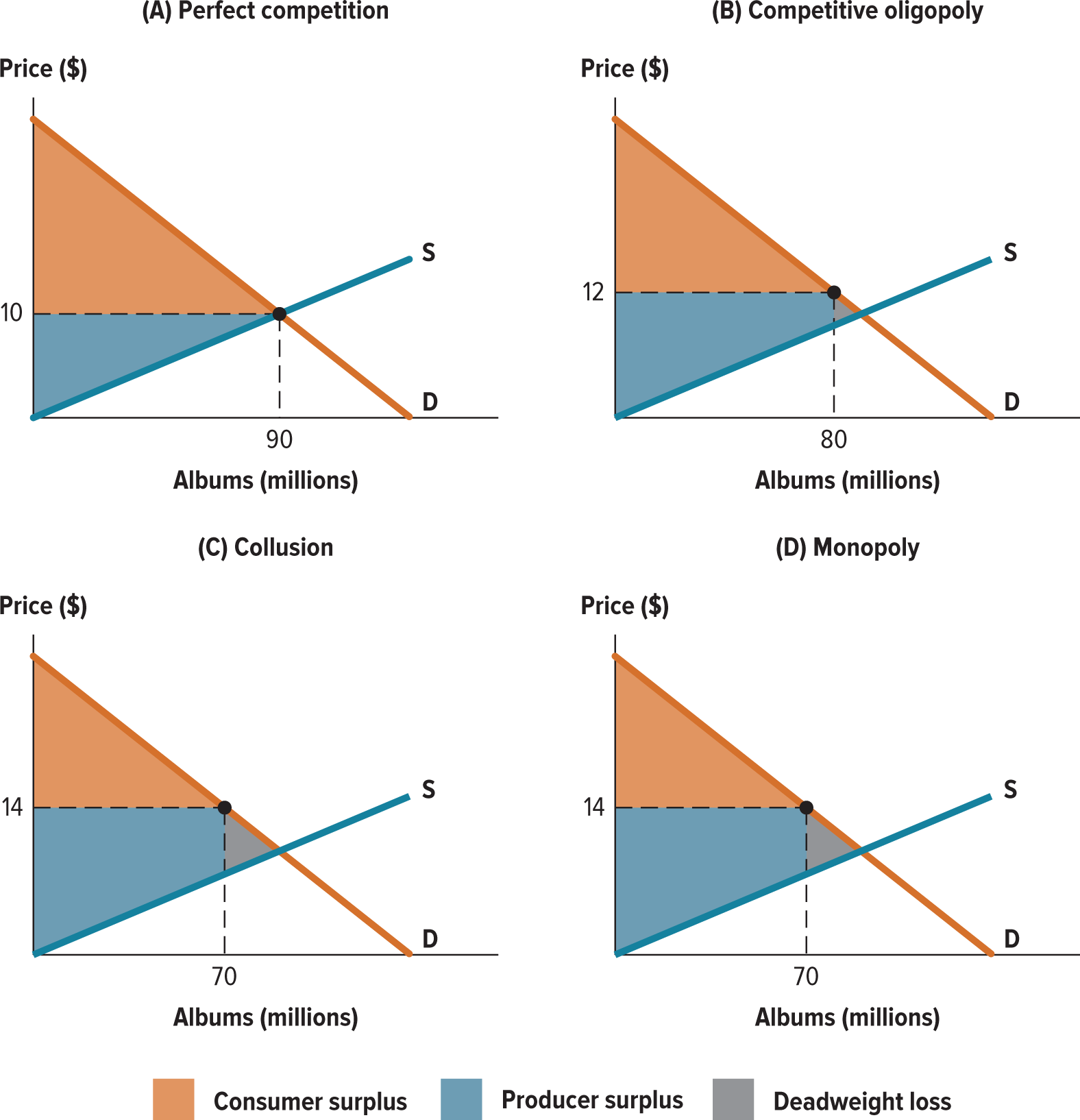

15.8. Oligopoly and Public Policy

- The competitive equilibrium in an oligopoly leads to a quantity and price that are somewhere between the outcomes of a perfectly competitive market and those of a monopoly

- Because the equilibrium is not the same as in a competitive market, oligopoly results in some deadweight loss and increases producer surplus at the expense of consumer surplus

- When oligopolists collude, the equilibrium looks like a monopoly outcome and results in even higher deadweight loss and higher producer surplus