Chapter 8: Receivables, Bad Debt Expense, and Interest Revenue

Objective 8.1: Describe the trade-offs of extending credit.

Pros and Cons of Extending Credit

- Advantage: Encourages the customer to buy more goods/services, so revenue goes up.

- Disadvantages:

- Increase in wage costs: Employees are hired to see if someone is creditworthy, see how much money people owe, and to collect from customers.

- Bad debt costs: Sometimes people don’t pay what they owe.

- Delays receipt of cash: Receiving cash from customers can take 30-60 days.

Objective 8.2: Estimate and report the effects of uncollectible accounts.

Accounts Receivable and Bad Debts

- When accounts receivables aren’t fully paid off, it results in bad debt.

- There are %%two objectives%% in relation to accounts receivable and bad debts:

- Accounts Receivable is recorded at the value that is expected to be collected, aka “net realizable value”.

- Match (matching principle) the estimated cost of bad debts to the accounting period related credit sales are made.

- Both objectives result in a decrease in Accounts Receivable and Net Income by the credit estimated to not be collected.

- You must record Sales Revenue and Bad Debt Expense in the %%same period of the sale%%. This is called the expense recognition principle (matching).

- The allowance method is estimating bad debts that may not be collected and adjusting these estimations later.

- Allowance for Doubtful Accounts is a contra account to Accounts Receivable and has a normal credit balance.

- When an account can not be collected, the account must be written off.

- The balance is removed from Accounts Receivable and Allowance for Doubtful Accounts.

- Debit Allowance for Doubtful Accounts

- Credit Accounts Receivable

- Write offs DO NOT appear on the Income Statement.

- ==Equation to calculate net receivable value:==

- Accounts Receivable - Allowance for Doubtful Accounts = Net Receivable Value

- %%Journal entries:%%

- Record sales on account:

- Debit Accounts Receivable

- Credit Sales Revenue

- Record estimate of bad debts:

- Debit Bad Debt Expense

- Credit Allowance for Doubtful Allowance

- Bad debt know (“write off” day):

- Debit Allowance for Doubtful Accounts

- Credit Accounts Receivable

- Example: A company sells a bike for $300 to a customer who pays on account. An asset increases and revenues increases.

| Accounts Receivable | $300 | ||

|---|---|---|---|

| Sales Revenue | $300 |

- Example: The company expects to receive $300, but records it estimated bad debt. An expense increases and a contra account increases.

| Bad Debt Expense | $300 | ||

|---|---|---|---|

| Allowance for Doubtful Accounts | $300 |

- Example: The company writes off the bad account. A contra account decreases and the asset decreases.

| Allowance for Doubtful Accounts | $300 | ||

|---|---|---|---|

| Accounts Receivable | $300 |

Methods for Estimating Bad Debts

- There are %%two methods%% to calculate the estimate of bad debt: Percentage of Credit Sales Method and Aging of Accounts Receivable

- Percentage of Credit Sales Method

- Aka the Income Statement Account.

- Estimates Bad Debt Expense for the period.

- Not very precise.

- ==Equation for estimating bad debt expense (% of credit sales method):==

- Historical percentage of bad debt loss x Current period’s credit sales

- Example: A company has bad debt loss of 3/4. Their credit sales in March totaled $150,000.

- Historical percentage of bad debt loss = 75%

- Current period’s credit sales = $150,000

- $150,000 x 0.0075 = $1,125

- Aging of Accounts Receivable

- Aka the Balance Sheet Method.

- Estimates the ending balance in the Allowance for Doubtful Accounts.

- Bases its estimate off of the age of each amount in Accounts Receivable at the end of the accounting period.

- If the account receivable is old and overdue, it is less likely to be collected.

- More complicated than the first one, but it more accurate.

- Steps for the Aging of Accounts Receivable:

- Prepare an aged listing of accounts receivable.

- Estimate the bad debt loss percentages for each category.

- Compute the total estimated bad debts

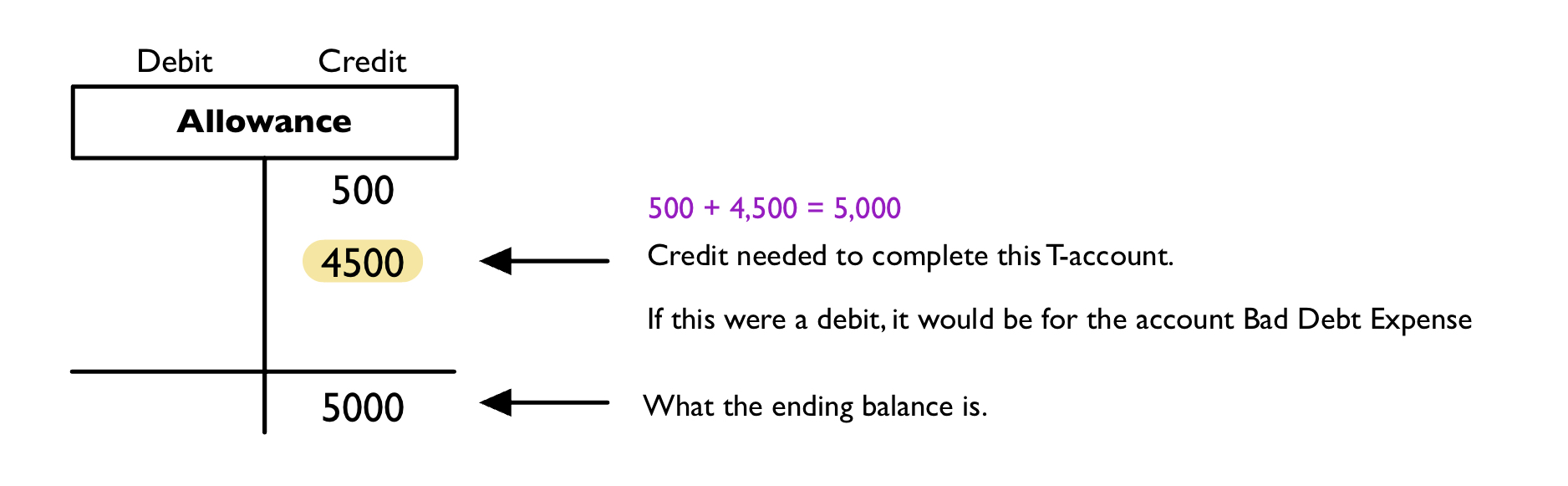

- Example: $5,000 of a company’s Accounts Receivable are estimated to be uncollectible. The unadjusted credit balance for Allowance of Doubt Accounts is $500.

- We know that the beginning balance in the Allowance for Doubtful Accounts is $500.

- We know the ending balance is $5,000.

- We want to fill in what the adjusted entry should look like on the T-account.

Other Issues

- We never expect the estimate to match perfectly. There is always going to be a little bit of a difference. If we are significantly off, we have to increase our percentages.

- Revising estimates is when a company revises their bad debt estimates for the current period.

- Account recovery is reviving written off accounts. The receivable is put back on the books by recording the opposite of what is done for writing off an account. After, a company records the collection of the account.

- An example of an account recovery is getting a check in the mail after writing off an account. The company initially thought they would not receive payment, but they did so a journal entry is needed.

- There will %%always be 2 journal entries for a recovery%%.

- Journal entry for reversing the write off:

- Debit Accounts Receivable

- Credit Allowance for Doubtful Accounts

- Journal entry for the collection of the account:

- Debit Cash

- Credit Accounts Receivable

- Example: A company collects $300 for a bike sold, but previously written off. Write the two journal entries: reverse the write off and collect the cash.

| Account Receivables | $300 | ||

|---|---|---|---|

| Allowance | $300 | ||

| Cash | $300 | ||

| Accounts Receivable | $300 |

Objective 8.3: Compute and report interest on notes receivable.

Notes Receivable and Interest Revenue

- A Notes Receivable is reported when a promissory note is used for a transaction. It has a stronger legal claim.

- Notes receivables %%charge interest%% from the date they are created to when they are due.

- The day the Notes Receivable is due is called the maturity date.

- A company may use a Notes Receivable for:

- Loaning money out to employees or businesses.

- Receiving extended payment on expensive items.

- Switching from Accounts Receivable to Notes Receivable to extend the payment period.

Calculating Interest

- Three numbers are needed to calculate interest:

- Principal - the amount of the Note Receivable.

- Interest Rate - interest percentage charged on the note. They are always an annual percentage.

- Time Period - the amount of time covered in the interest. Can be in months or days (12, 365)

- ==Equation to calculate interest:==

- Principal (P) x Interest Rate (R) x Time (T) = Interest (I)

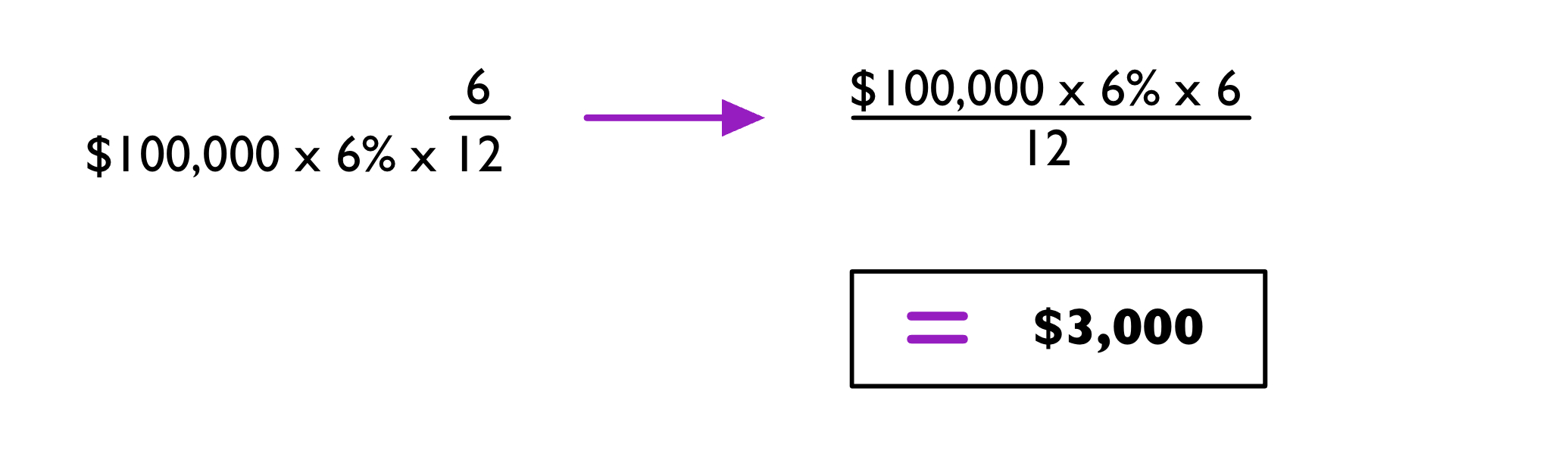

- Example: The interest period for a company is from January 1 - June 1 (6 months). The principal is $100,000 and the rate is 6%. What would equation look like and what is the interest?

- Principal (P) x Interest Rate (R) x Time (T) = Interest (I)

- Time is in terms of months in this example. The interest period (# of months) goes over 12 (total # of months in a year).

- $100,000 x 6% x 6/12 = $3,000

Recording Notes Receivable and Interest Revenue

- %%The four key events for a Note Receivable:%%

- Establishing the note.

- Accruing interest earned but not received (make an adjusting journal entry).

- Recording interest payments received.

- Recording principal payments received.

- First, do a journal entry that shows the increase of the Note Receivable.

- Debit Notes Receivable

- Credit Cash

- Interest revenue is earned over time.

- For this next step, use the formula P x R x T = Interest.

- Do the journal entry:

- Debit Interest Receivable

- Credit Interest Revenue

- Third, we calculate the rest of the interest for the remaining time period.

- Create the journal entry:

- Debit Cash

- Credit Interest Receivable

- Credit Interest Revenue

- Lastly, we create the journal entry for the principal amount of the note

- Debit Cash

- Credit Note Receivable

- Example (part A): On November 1st, 2021, a company lent $100,000 to a business using a note. The business must pay the company 6% interest and $100,000 principal on October 31st, 2022.

| Notes Receivable | $100,000 | ||

|---|---|---|---|

| Cash | $100,000 |

- Example (part B): Accrue the interest at the end of the year (December 31, 2021).

- Find the amount of interest to be paid at this time.

- P = 100,000; R = 6%; T = 2 months

- $100,000 x 6% x 2/12 = $1,000

| Interest Receivable | $1,000 | ||

|---|---|---|---|

| Interest Revenue | $1,000 |

- Example (part C): Received interest at the maturity date (October 31, 2022).

- Find the total amount of interest the company earns.

- $100,000 x 6% x 12/12 = $6,000

- We already received 2 months of interest, so we subtract the $1,000 from $6,000.

- $5,000 is the amount we earned in 2022.

| Cash | $6,000 (total earned) | ||

|---|---|---|---|

| Interest Receivable | $1,000 (earned 2021) | ||

| Interest Revenue | $5,000 (earned 2022) |

- Example (part D): Record the principal amount from the note that is received on October 31, 2022.

| Cash | $100,000 | ||

|---|---|---|---|

| Note Receivable | $100,000 |

Objective 8.4: Compute and interpret the receivables turnover ratio.

Receivables Turnover Analysis

- A receivables turnover analysis helps see the effectiveness of a company’s credit-granting and collection activity.

- Selling goods or services makes the receivables balance increase.

- Collecting the money from customers makes the receivables balance decrease.

- Receivables turnover is the constant selling and collecting cycle.

- The receivables turnover ratio indicates how many times the cycle is repeated during the accounting period.

- The higher the ratio, the faster the collection of receivables.

- When the ratio is low, the company is giving their customers too long of a period to pay. Uncollected accounts become a risk.

- Days to collect is the number of days to collect receivables.

- A higher ratio means it takes more days to collect, but we want a lower ratio.

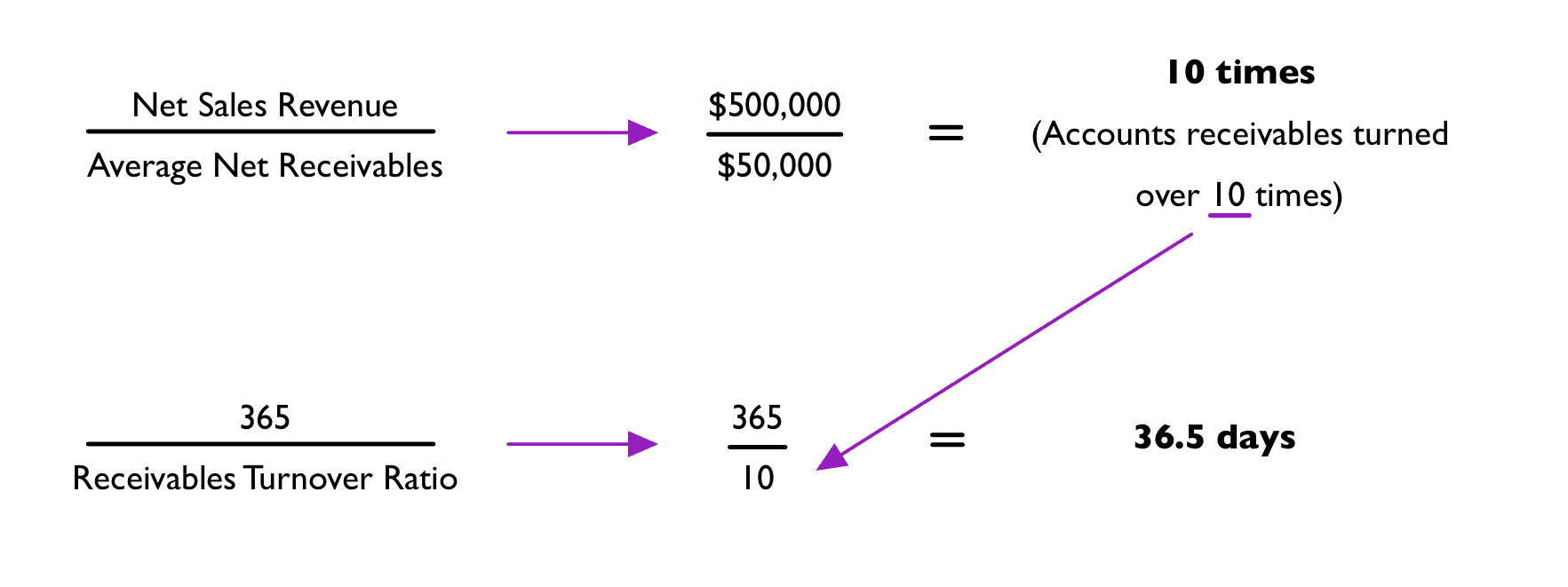

- ==Equation to calculate the receivable turnover ratio:==

- Net Sales Revenue/Average Net Receivables = Receivable Turnover Ratio

- ==Equation to calculate days to collect:==

- 365/Receivables Turnover Ratio = Days to Collect

- Example: A company has Net Sales Revenue of $500,000 and Average Net Receivables of $50,000.

Comparison to Benchmarks

- Credit terms is an agreement between the buyer and seller about the timings and payment to be made for the goods bought on credit.

- You can compare the numbers of days to collect to the length of the credit period to see if credit terms are being followed.

Speeding Up Collections

- %%There are two ways you can speed up collections%%:

- Factoring Receivables

- Credit Card Sales

- A factor is when you sell outstanding accounts to a different company. By doing so, your company is paid for the receivables it sells to the factors. A factoring fee must be considered.

- Credit cards speed up cash collection and make it less likely to receive bad checks from customers. Credit card companies so however charge a fee for their services.