ECON 1103 EXAM 1 GUIDE

Principles of Microeconomics

Economics : study of satisfying our unlimited wants with limited resources

Unlimited wants: there is always someone else wants what you don’t, wants change overtime

Microeconomics: making decisions for themselves; small picture activities; balancing trade-offs between resources to use

Macroeconomics: making decisions for others as a group

Factors of production

Four factors:

Land

Labor

Capital

Entrepreneurship

Every choice has a cost – economists only worry about the chosen thing and the runner up

Opportunity cost — the cost of the next best option not chosen

Calculation: sacrifice / gain

PPF

Production possibilities frontier: possibilities of production using given, limited resources

Bows out because of increasing opportunity costs

As we use our resources more efficiently, curve bows out because opportunity costs change as quality changes

Points on PPF

Point under curve = inefficient (A)

Point on curve - efficient (B)

Point outside curve = unattainable ( C )

Determinants of PPF

Machinery

Trade

Labor

Allocative efficiency: resources allocated maximize happiness of consumers

Balance between marginal utility and marginal cost of one more unit

MU = MC

MC = change in costs / change in quantity

MU = change in utility / change in quantity

Circular Flow Model

Major components

Factor market: resources businesses use to produce goods or services

Households = suppliers (labor)

Firms = consumers

Product market

Households = consumers

Firms = suppliers

Economic systems:

Free market: supply and demand, competition determine market outcomes

Centrally planned economy: government allocates resources; restrictions

Mixed: free market with government regulations for fair trade

Demand

Law of demand

Price and quantity demanded have inverse relationship

Reasons for this law

Substitution Effect: as price rises, you may choose to buy from a different market

Income effect: as the price rises and your income doesn’t, you can buy less and less of the good

Determinants of Demand

Price of related goods

Substitutes

Complements

Expected future price

If you expect the future price to rise, demand for today increases

If you expect the future price to fall, demand for today lowers (waiting to purchase)

Income

Normal goods: income rises, demand rises

Inferior goods: income rises, demand falls

Population

Population increases, demand increases

Preferences of buyers

Changes in favor → demand increases

Change against → demand decreases

Change in Demand vs. Change in Quantity Demanded

Change in demand = movement of the curve (determinants change)

Change of quantity demanded = movement along the curve (happens because of price change)

Supply

Law of Supply: ceteris paribus, as the price of a good increases, quantity supplied of the good will increase

Determinants of Supply

Price of factor of production

as increases, supply decreases

Price of related goods

Price of related goods increase (more profit), supply decreases

Expected future price

If the price is expected to increase, supply today decreases

If price expected to decrease, supply today increases

Number of suppliers in the market

Number of suppliers increase, supply increases

Supply = horizontal sum of individual firm’s supply

Technology

Change in Supply vs. Change in Quantity Supplied

Change in supply = movement of curve (determinants change)

Change in quantity supplied = movement along curve (price change)

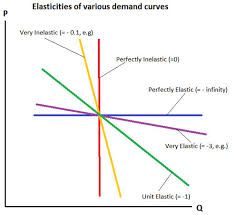

Elasticity

Price Elasticity of Demand

Measure of how much quantity demand changes with price change

ED = %Δ QD / %ΔP

Midpoint formula:

Types:

Perfectly Inelastic: quantity demanded doesn’t change with price change

Usually for necessities (gas, medication)

Elasticity = 0

Perfectly Elastic: extremely responsive to price changes

Elasticity = ∞

Unit elastic: quantity demanded is perfectly responsive to change in price

Elasticity = 1

Elastic: quantity demanded changes a lot because of price change

Elasticity > 1

Inelastic: quantity demanded doesn’t change much because of changes in price

0 < Elasticity < 1

Relationship between Elasticity and Total Revenue

Total revenue: P * Q

More elasticity = more revenue

More inelastic = less revenue

Unit elastic = no change in revenue

Other types of Elasticity

Income Elasticity: how responsive demand is with change in income

EI = %Δ Q / %ΔI

Cross Price elasticity: how responsive the demand for a product is to a change in price of another

EC = %Δ Q Product A / %Δ P Product B

Negative = complement

Positive = substitute

Price Elasticity of Supply - same as Demand but with Quantity Supplied

Advantage

Absolute advantage

Ability to produce more of a good or service than another using the same amount of resources

Comparative advantage

Producing a good at a lower opportunity cost compared to another, even if the other can produce more of both goods in absolute terms

Whoever has lower opportunity cost specializes in producing product