Check Payments Overview

Defining Payments Terms

Check Payments Definitions

Acronyms and terms defined in this section are grouped by:

Financial institutions

Industry rules

Regulations

Standards

Check Definitions

Check Payments Terminology: Financial Institutions

Depository Financial Institution (DFI)

State or nationally chartered bank, savings, and loan association, savings bank, or credit union

Bank of First Deposit (BOFD): Depositary Bank

First DFI to which check is transferred; may also be the Paying Bank or Payee

Collecting Bank

Bank handling an item for collection except the Payor Bank; subsequent bank in forward collection process

Example: FRBs are collecting bank

Intermediary Bank

Bank to which an item is transferred in course of collection

Except the Depositary Bank or Payor Bank

Presenting Bank

Bank presenting an item to the Payor Bank

Payor Bank

Bank that is the Drawee of a draft; see also Paying Bank definition in Reg CC

Terminology: Industry Rules

ECCHO Operating Rules & Commentary

ECCHO, a service of The Clearing House, maintains a national set of Rules for private sector image exchange

Rules apply only to exchanges between ECCHO members that agree to use the Rules

FRB OC3: Federal Reserve Operating Circular 3

Governs the collection of cash items and returned checks through the Federal Reserve Banks (FRBs)

References Regulation J for related warranties

Terminology: State Law

Uniform Commercial Code (UCC)

Model state law as adopted in a state

Provides general business law of a state regulating sale of goods, commercial paper (checks), bank collections, and secured transactions in personal property

Articles 3 and 4 relate to negotiable instruments and bank deposits and collections

Article 1 includes general provisions and definitions

Terminology: Regulations/Federal Laws

Reg CC or Regulation CC

Federal regulation that governs availability of funds deposited in transaction accounts (e.g., demand deposit accounts), the collection and return of checks and substitute checks

Reg J or Regulation J

Federal regulation that governs collection of checks/other items by FRBs

Establishes procedures, duties, and responsibilities among FRBs, senders and payors of checks and other items and senders and recipients of Fedwire fund transfers

Terminology: Standards:

Accredited Standards Committee X9

X9 is accredited by the American National Standards Institute (“ANSI”) to develop and maintain open consensus standards for the financial services industry in the US

Facilitates creation/administration of standards that improve payments, protect data and interoperability between exchange parties.

X9 standard related to payments in this training include:

X9.100-140: Specifications for Image Replacement Document - IRD

X9.100-160: Magnetic Ink Printing (MICR) Parts 1 and 2

X9.100-187: Electronic Exchange of Check and Image Data

X9.100-188: Return Reasons for Check Image Exchange and IRDs

X9.100-160: Magnetic Ink Printing (MICR) Parts 1 & 2

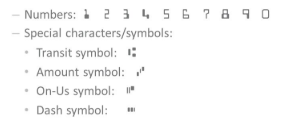

Magnetic Ink Character Recognition (MICR)

Descriptive information compromised of numbers and symbols printed at bottom of physical check

Generally printed in magnetic ink and designed to be recognized at high speed by automated processing equipment

Symbols printed in special font (E-13B)

Character set includes:

Terminology: Check - Negotiable Instrument

Written order

Written order directing a bank to pay money as instructed

Designed to transfer amount of money for which it is written on or after the date specified on the check and to specific payee (or to the bearer)

Promise to pay

An unconditional promise to pay

Includes a substitute check and an electronic check/electronic returned check

Defined by state & federal law

UCC definition:

Draft if it is an order to pay;

Within this definition it states check is a draft payable on demand

Reg CC definition:

Check covers several types of instruments including checks, money orders, etc.

Terminology: Checks

Remotely Created Check (RCC)

Defined by both UCC and Reg CC as check that is:

Not created by the Paying Bank; and

Does not bear signature applied, or purported to be applied, by person on whose account check is drawn

RCCs are considered unsigned drafts

Must be authorized by account holder;

Must be printed (a physical item) to meet Reg CC definition

RCCs are not created by a Paying Bank or agent of the Paying Bank

Negotiable Instrument

Negotiable Instrument - Draft/Check

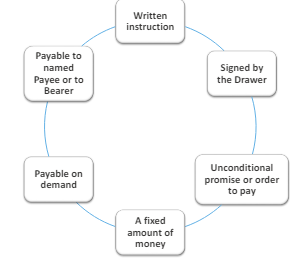

UCC 3-104 defines the check within the definition of a negotiable instrument as a draft that is:

Written instruction

Must be a writing/physical item

Signed by the drawer

Person giving the instruction

Order to pay fixed amount of money

Value of instrument

Payable on demand

Negotiable Instrument & Drafts

UCC divides instruments into two general categories:

Drafts and Notes

An instrument is a:

Note if it is a promise to pay; and

Draft if it is an order to pay

Draft is further defined in UCC as:

Written order signed by the drawer; an unconditional order to pay

Checks are drafts

Check: Demand Draft

Reg CC check definition covers several categories of instruments:

Negotiable demand draft drawn on:

Or payable through or at, an office of a bank;

Federal Reserve Bank or Federal Home Loan Bank;

US Treasury;

Demand draft drawn on:

State or unit of general local government not payable through or at a bank;

U.S. Postal Service money order;

Traveler’s check; and

An original check and a substitute check

Electronic check/electronic returned check defined as:

Electronic image of an electronic information derived from a paper check or paper returned check

Must conform with X9.100-187 standard

Must have agreement for exchange between sender and receiving bank

Summary

UCC and Reg CC define checks, electronic checks, returned checks, noncash items and electronically created items (ECIs)

Check: Defined as a negotiable demand draft

Checks include an original paper check and a substitute check

Electronic check and electronic returned check: Defined as

Electronic image of, and electronic information derived from paper check or paper returned check; that is sent to a receiving bank by agreement; and that conforms to X9.100-187 standard

Electronically-created Item

Electronic image that has all the attributes of an electronic check or electronic returned check but was created electronically and not derived from a paper check

ECI not considered a check under Reg CC

Currently not eligible for exchange under ECCHO Rules or Fed Operating Circular 3 (OC3)

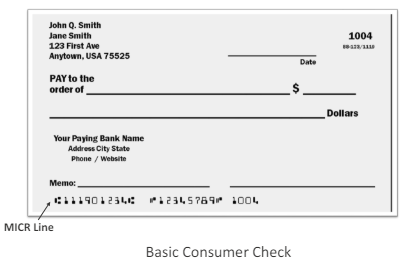

Parts of a Check

Blank Check Example

MICR and MICR Line

Magnetic Ink Character Recognition (MICR)

Common machine language for automated check handling

Descriptive info comprised of numbers and symbols designed to be recognized at high speed by automated processing equipment

Printed in magnetic ink according to standards

E-13B font

For magnetic ink printing in USA, Canada, others

Consists of ten numeric characters and four symbols

MICR line: Located at the bottom of the physical check; key fields include:

Amount: 10-digit field

On-Us: Includes drawer’s account number & check serial number

Routing Number: ABA assigned identifier

EPC: External processing code; optional, single-digit field

Definition of MICR also includes:

MICR line data in an electronic record

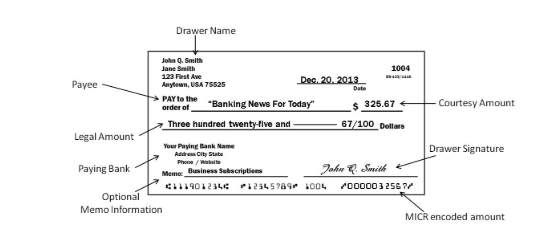

Processed Check Example

Consumer Check (6-inch check)

Processed check: completed and signed by drawer

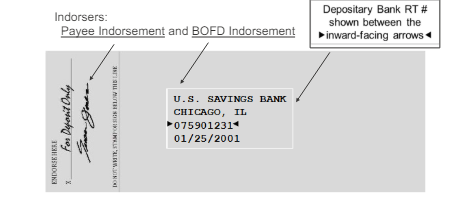

Note: In UCC and Reg CC, indorsement is spelled with an “I”

ECCHO incorporates UCC and Reg CC within the ECCHO rules and maintain that spelling

Endorsement with an “E” is a term generally used outside of banking laws and regulations

Drawer or Maker?

Usage of terms Drawer and Maker (see UCC and Reg CC)

Drawer: Person who signs or is identified in a draft as a person ordering payment (e.g., person who signs the check)

Maker: Person who signs or is identified in a note as a person undertaking to pay (e.g., person to pay on a note)

Other check terms:

Drawee: Person or bank ordered in a draft to make payment

Payor Bank: The bank that is the drawee of a draft

Note:

UCC defines person to mean an individual, public corporation, or any other legal or commercial entity

UCC defines bank as a person engaged in the business of banking

Paying Bank

Paying Bank: A Reg CC definition 229.2 (z)

Bank to which check is sent for payment or collection

May be designated as a payable-at bank or payable-through bank that is responsible for the expedited return of checks and notice of nonpayment requirements

If check is sent for forward collection based on the routing number, bank associated with that routing number in considered the Paying Bank under the regulation

Federal Reserve (FRB): Cash Items

Checks, including postdated checks

Government checks, postal money orders

Other demand items acceptable to Paying Bank’s FRB

Demand items payable outside of a State, acceptable to the last collecting FRB, that are accepted as cash items (foreign cash items)

Electronic checks that conform to Operating Circular 3 and FRB technical requirement

Substitute checks

Certain redeemed savings bond (see OC3 Appendix C)

Noncash items FRB has agreed to handle

Agreement or authorization required before sending noncash items

Noncash Items

Would otherwise be checks except for:

Attachments or special instructions

Printed on more than a single thickness of paper - don’t qualify for automated check processing

Not preprinted or post-encoded in magnetic ink with routing number of Paying Bank

Key takeaways:

Determining if item is a check or noncash item

Does the item qualify for handling by automated check processing equipment?

Does the item have the routing number of the Paying Bank pre-printed or post-encoded in magnetic ink?

Check Processing Overview

Level Set: General Processes

Cashing a check

Process by which check is negotiated by the holder for cash

Depositing a check

Process by which check is negotiated by the holder to the DFI for credit to the depositor’s account

Remote Deposit Capture (RDC)

Banking service which allows a user to scan checks and transmit the scanned images to a financial institution for posting and clearing

RDC described in FFIEC guidance as a transaction delivery system

Images may be created using a scanner or via a mobile device app

General Check Payment Processes

Clearing a Check

Process by which check moves through payment systems from DFI where it was deposited to Payor/Paying Bank (institution on which it’s drawn)

Note: May involve one or more collecting banks in the process

Collection of a Check

Process by which Depositary or Collecting Bank transfers a check to another collecting bank or presents it to the Paying Bank for payment

Presentment of a check:

Exchange of value for the amount of that check

Return of a Check

Process by which Paying Bank may determine not to pay for check presented due to NSF, Stop Pay, or other reasons

Must be returned timely to be a return

Return timing based on UCC and Reg CC requirements

Claim Adjustment

Process by which a bank may send/receive a claim to adjust settlement for a paid check

Must be for a valid reason

Adjustments are by agreement

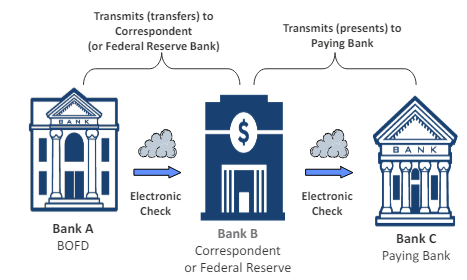

Check Collection Process

Simple image exchange process (forward) with three banks

Depositary Bank (BOFD) = Bank A

Intermediary (Correspondent or FRB) = Bank B

Paying Bank = Bank C

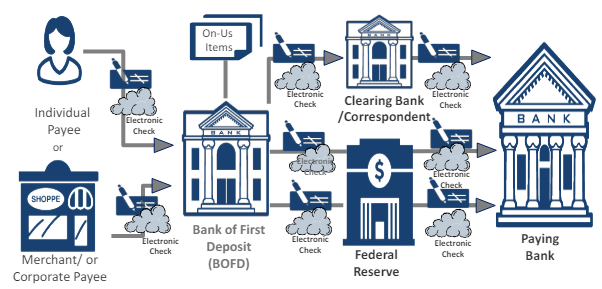

Check Processing

Detailed example with paper check then image exchange

Paper processes shown from individual/corporate Payor → Payee → Depositary Bank → through clearing network → Paying Bank

Overlay with image exchange: Medium changes (from paper check to electronic check) but general processes are the same

Daily cycle includes various steps - Processes and timing differ for:

Depositary Bank; Intermediary or Collecting Bank and Paying Bank

Sources of work: Where are checks cashed, deposited, or used for purchase or other payments?

ATM

Vault

Lockbox

Bank branch

Merchants

Capture process: Collecting check info via either physical or electronic (virtual) cycle

Reject/repair re-entry: Correcting errors (if possible) to get an item back into the processing cycle

Imaging: Create digital image of front and back of check

Required by standards to capture all info from both the front and back of the physical check to create an electronic check

Virtual (electronic process) to capture the check info

May also use some form of physical scanning of paper checks

Dispatch process: Sending out checks drawn on other banks for collection and final settlement

Majority sent electronically (no paper transportation today)

Clearing process: Process, prepare and release data files to move check data forward from point of deposit for collection

May go through intermediaries before final presentment to Payor/Paying Bank

Settlement process: Exchange of funds for the value of cash letters sent/received

May be net or gross settlement via clearinghouse, provider, or the FRB

Exception handling: Processing/resolution of returns or adjustments

Determine not to pay a check presented - based on timing

Return check with proper reason code or send as an adjustment

Exceptions and Check Fraud

Exceptions - Returns

Exception: An error or an exception to the normal operational process

Any paper or electronic check that requires further investigation before disposition can be determined

Exceptions deal with both returns and adjustments

Timing is a primary determining factor in whether an item is handled as a return or must be handled as an adjustment

Returns: Governed by statutory and regulatory requirements

UCC midnight deadline (UCC 4-301)

Reg CC expeditious return requirement (221.31(b))

Return of a check unpaid:

Items that are being sent back by the Paying Bank

Must state it is a return and the reason for the return

Must meet timing requirements or may be considered a late return

Exceptions - Adjustments

Adjustments: Handled by agreement of parties

FRB OC3; The Clearinghouse/ECCHO Rules

Errors that occur during item processing generally require some research to resolve; depending on timing and type of adjustment, may adjust settlement for a paid check either:

With entry (with financial settlement)

Without entry (without immediate financial settlement)

Must state specific adjustment type for each case

Adjustment types, timing and related requirements may differ depending on adjustment provider and adjustment rules:

FRB, Viewpointe, The Clearing House/ECCHO Rules, etc.

What is Fraud?

Fraud exists in all payment systems

Occurs when following elements exist:

Intentional untrue representation about an item, fact or event

Untrue representation is believed by the victim

Victim relies upon and acts upon the untrue representation

Victim suffers a loss of money and/or property as a result of reliance on untrue representation

Check fraud:

Refers to a category of criminal acts that involve making the unlawful use of checks in order to illegally acquire funds that do not exist within the account balance or account holder’s legal ownership

Other Payment Systems

Multiple Channels/Options

Checks can be cleared via multiple channels

Different channels (FRB vs. private sector): different rules may apply

Check can be cleared in different forms:

As a physical check

As an electronic check

As a substitute check (IRD)

As an ACH debit (if check is eligible for conversion) using appropriate SEC code:

ARC - Accounts Receivable entry

POP - Point of Purchase entry

BOC - Back Office Conversion entry

Automated Clearing House (ACH) - Simple Overview

Funds transfer system governed by Nacha Rules

Provides for interbank clearing of electronic entries for participating financial institutions

ACH transactions: Debits or credits

Examples include:

Direct deposit of payroll, government, and social security benefits

Scheduled payments for mortgage, insurance, or other bill payments

Participants in ACH exchange

Originator: Individual, corporation or another entity

Initiate either a deposit or payment transaction

ODFI: Originating Depository Financial Institution

RDFI: Receiving Depository Financial Institution

ACH Operators: Two central clearing facilities:

FRB

The Clearing House (EPN)

Sample ACH Process Example

ACH credits may be consumer or corporate payments:

Interest payments

Payrolls

Social security payments

Government vendor payments

Pensions

Dividends

State tax payments

Annuities

Originator initiates payment instructions to move funds into a Receiver’s account

Common use: Direct deposit of payroll

Other Payment Systems

Debit Card: May use term bank card or check card

Generally, uses shared ATM networks that offer payment services associated with a financial institution’s DDA system

Similar to a credit card, but unlike a credit card, the money comes directly from the user’s DDA account

Credit Card: Issued by a company to allow a user to purchase good/services from merchants who accept the card

Major networks include:

American Express, Discover, MasterCard, and Visa

Merchants generally pay fees to accept credit cards

Card-issuing banks receive part of the fees as revenue

Card Processing: When the card is used, card-holder is technically using the bank’s money instead of their own to pay for a product or service

Over time must repay with interest

Wire: Electronic payment service for transfer of funds

Characteristics of large dollar transactions, immediate availability, and irrevocable payments

To wire funds is to make a funds transfer from one bank to another with almost immediate availability

Credit transfer (crediting funds)

Contrast to checks which are debits

Funds transfer defined in UCC 4A-104 as:

Series of transaction, beginning with originator’s payment order, for purpose of making a payment to beneficiary of the order

Term includes payment order issued by originator’s bank, or an intermediary bank, intended to carry out originator’s payment order

Completed by acceptance of payment order by the beneficiary’s bank for the benefit of the beneficiary

Wires governed by provisions in UCC 4A and:

Regulation J for Fedwire

Rules and procedures for Clearing House Interbank Payment System (CHIPS)