Unit 5

Internal sources of business finance

Financial departments as one of four key functions of business:

records transactions

forecasts cash-flow

prepares accounting information

prepares final accounts

makes financial decisions

What do businesses need finance for?

start up capital → Start a business

working capital → Increase production

capital expenditure → expand business

Start up capital - financial sources (financial capital) needed by an entrepreneur when first starting a business to buy fixed + current assets.

Assets - items of value which are owned by the business

Fixed Assets - resources owned by a business which will be used for a period longer than a year. e.g. Land, Buildings, equipment, vehicles

current assets - resources owned by a business which will be used for a period shorter than a year. e.g cash, inventories and account receivables(inflows)

Intangible assets - assets that do not exist physically but can have value. e.g. brand name, patent, copyright.

Working capital - finance needed by business to pay its day to day costs which do not involve the purchase of long term, fixed assets. e.g wage,bills,materials

Capital expenditure - spending by a business on fixed assets which will last for more than one year. Used during start-up or during expansion. e.g product development, R&D

Revenue Expenditure - money spent ba a business on day to day expenses which don’t involve purchase of long term assets. e.g wage/rent.

Short term finance - loans or debts to overcome cash flow problems and tthe business expects to pay them back within one year. e.g short term bank loans,overdrafts,etc.

long term finance - loans or debts to finance purchases of ixed assets or business expansion and the business expects to pay them back in 5 years or longer.

Internal sources of finance

Owners saving - money put in the business by the owner during start up or for expansion.

Also known as owners equity.

it is possible for both limited and unlimited businesses

Benefits

available quickly

no costs/ interests paid by the business

Disadvantage

Amount of money might be too low

Retained profit

profit remaining after all expenses, tax and dividends have been paid out and which is reinvested back into the business.

Possible in poth limited and unlimited businesses

Benefits

no cost/interest to the business

does not have to be repaid

Disadvantages

cannot be used to start up a business

might not be enough money

only possible if the business is profitable

decreases dividends - shareholders receive less profit

Sale of fixed assets

Sale of unwanted fixed assets

no direct cost to a firm

amount of $ raised depends on :

Land + buildings - often raises a lot of money

Highly specialised machines - hard to find customers → harder to sell

Sale and leaseback

selling fixed assets and then renting them from new owner

New rent → future fixed costs higher

risk of higher rent or need to relocate once the rental contract ends

Use of working capital

Cash balances

use cash to finance capital expenditure, but make sure you have enough cash for day to day operations

Reducing inventories

e.g buying less materials for production → less money tied in stock yet keep enough to sell

reducing accounts receivables

limit selling goods on credit (buy now pay in 30 days) or make credit period shorter

big firms can use more working capital

beware of cash flow issues

Practice

1) IE decided not to use any of the cash balance to buy the new machine as the money used to buy the machine cannot be used for something else. Such as the components used to make the mechanical components and domestic appliances IE makes. If demand increases IE cannot buy more components to make the products and therefore loses current and future capital.

2) if the demand for mechanical components increases IE looses the possibility for current and future profit as they cannot sell mechanical components as they dont have the materials to make more.

3) The marketing director disagrees with the operations director as the marketing director might believe that there might be an increase in demand for mechanical components and if they were to decrease their level of finished good inventories

4)

a) A private limited company cannot sell shares to the public additionally it has limited liability

b) capital expenditure is the spending of a business on fixed assets which will last for more than one year.

c) Retained profit and

External sources of business finance

Short term sources

Overdraft

Agreement with a bank that allows a business to spend more money than iz has in its account up to an agreed limit. The loan must be payed within 12 months

Able to take short notice → very flexible fro business

High interest rate → taken only in case of short-term cash flow problems

Trade credit

agreement between a business and its supplier that the business can pay for the supplied materials at agreed time in the future

e.g. buy now pay later

Business pays later -

regular delayed payments → risk of demanding payment upfront

No further deliveries until old deliveries are paid

any discount will be lost

Debt factory

selling trade receivables to improve business liquidity

Trade account receivables - amount owed to a business by its customers who bought goods on credit

longer credit periods offered to customers on trade receivables → need for more cash from other resources to pay day to day expenses → potential issues.

Solution - sell the loan to debt factoring business with discount

Long term sources

Bank loan

finance provided by a bank which the business will repay with interest over agreed period of time

fixed vs variable interest rate

small businesses riskier for banks (smaller revenue + unlikely to pay collateral)

Mortgage

long term loan used to buy land or buildings

interest payed every year

similar to bank loans

Debenture

bond issued by a company to raise long term finance usually at fixed interest rate

used to raise large sums of money

owner of the bond gets interest + full price upon maturity date

security against the value of bond is usually provided by the firm

Leasing

using a fixed asset by paying a fixed amount per time period for a fixed period of time. Ownership remains within the leasing company.

used with cars/machines

often monthly payments

leasing company responsible for maintenance + repairs

benefit - no big one time payment needed → payed from working capital

disadvantage - higher interest rates

Hire purchase

purchase of an asset by paying a fixed repayment amount per time period over an agreed period of time. The asset is owned by the purchasing firm on completion of the final repayment.

used to obtain cars/machines

purchasing firm responsible for maintenance + repairs

benefit - no big one time payment needed → pay from working capital

disadvantage - high interest rates

Share issue - source of permanent capital available to limited liability companies after they sell their shares

only available for limited companies

private limited companies - shares sold to existing shareholders/ private investors

How to choose suitable source of business finance

Debt financing - most external finance except for share issue

benefits

does not change ownership of the company

lenders have no say in running the company

limitations

amount borrowed must be paid

interest is charged on the amount borrowed → increases costs

installments must be paid even if business makes a loss

Equity financing - permanent finance provided by the owners of a limited company

benefits

it never has to be repaid

no ongoing cost

no dividends have to be paid out if loss is made

limitations

original owners might loose influence in business after more/ other shareholders provide equity

expensive to produce a prospectus to offer shares for sale

Factors influencing choice of finance

Amount of finance required -

Large amount - debenture or share issue

small amount - bank loan, hire purchase, overdraft

Length of time when finance is needed

Long time - debenture, share issues, mortgage, maybe loan

Short time - overdraft, trade credit, debt factoring, maybe loan

Size and legal form of business

sole traders + partnerships - riskier ( their revenues might not be high enough to pay monthly installments + unable to provide collateral to secure debt) pay higher interest rates on loans

Existing borrowing

limited amount can be borrowed if the business already has many loans

Profitability of the business

profitable business - chance to finance from retained profit ( yet dividends would have to decrease for limited companies), profit - less risky debtor → more likely to be offered a loan from a bank

Type of assets to purchase

mortgage only to buy land / houses

Hire purchase / leasing only for physical assets such as cars, machinery

Desire to keep ownership of the business

Degree of ownership and control might decrease if equity is added / shares are issued.

shift from sole trader to partnership, shift from private limited company to public limited company

Practice

A) long term finance is sources of finance which are payable in more than 1 year

B) overdraft, trade credit

C) Akram could sell any unwanted fixed assets such as unused or old machinery or since he is determined he could use his retained profit too.

D)A bank is likely to look at Akram’s profit which is very varied and small as well as what collateral he has such as the farm and it’s land.

E) Akram could make his business a public limited company and issue shares this allows him to receive a large amount of money without the risk of going into debt. The capital Akram receives can then be used to buy and take over the neighboring farm. Additionally Akram could use debenture as it can raise a large amount of capital which Akram needs to take over the neighboring farm which could be better than issuing shares as Akram would retain full ownership.

Cash Flow forecasting

Cash - money / short term current assets to finance everyday operations

Cash inflow - sums of money received by a business during a period of time. e.g sales revenues, payment by debtors, borrowing, sales of assets, investments

Cash outflow - sums of money paid by a business during a period of time. e.g expenditures to buy materials. paying wages + bills, paying off debts, buying fixed assets

Cash flow - cash inflow and outflow over a period of time.

Net cash flow - cash inflow - cash outflow

positive cash flow - cash inflow > cash outflow

negative cash flow - cash inflow < cash outflow

Cash flow management - ensures that the business has enough cash whenever they need to pay their employees, suppliers, etc.

Responsible for cash flow forecast

cash flow forecast - an estimate of future cash inflows and cash outflows of a business

necessary to

prevent negative cash flow

convince banks to provide bank loans

to help managers plan ahead (e.g likely level of overdraft/loan needed)

Opening balance - amount of money a business has at the beginning of a month. Last months closing balance

Closing balance - amount of money a business has at the end of a month. Net cash flow - opening balance.

solving cash flow problems

hire purchase, leasing

bank loan

overdraft from bank

ask customers to pay trade receivables quicker by offering them discounts

negotiate longer credit terms with suppliers

Liquidity and working capital

Working capital measures liquidity of business

liquidity - ability of a business to pay its short term debts

enough working capital to pay debts → business is liquid

not enough working capital to pay debts → business is illiquid → need to borrow and pay additional interests

How much is enough working capital?

depends on working capital cycle

time it takes from buying raw materials, making these into goods for sale, finding buyers for them and receiving payments from customers

Amount of working capital depends on :

level of inventories held by a business

fewer inventories → less working capital needed

Trade credit terms

longer credit terms (paying back later)→ less working capital needed

Length of production process

short production process → less working capital needed

how quickly the business finds customers

finding customers quickly → less working capital needed

trade credit receivables terms

shorter credit sales → less working capital needed

practice

In $ 000s | Jan | Feb | Mar | Apr |

Credit sales | 230 | 250 | 200 | 180 |

Total cash inflows | 230 | 250 | 200 | 180 |

Payments | 160 | 350 | 230 | 160 |

Total cash outflows | 160 | 350 | 230 | 160 |

Net cash flow | 70 | -100 | -30 | 20 |

Opening balance | 20 | 90 | -10 | -40 |

Closing Balance | 90 | -10 | -40 | -20 |

ABC could ask their customers to pay their trade receivables on the phones they bought now by giving them discounts. This would be a good way to. improve their cash flow as if they would take a bank loan they would have to then pay interest. Additionally for the future they could decrease the days that customers have to pay ABC to decrease the possibility of going into negative again.

A) the working capital cycle for a business is the time it takes from buying raw materials, making these into goods for sale, finding buyers for them and receiving payments from customers

B) A = -5, B = -4, C = -2, D = -2, E = 4, F = 5, G = 9, H = 6

C)

Revenues and costs and profit

Quantity | Price | FC | VC | TC | TR | P/L |

$10 | $15 | $20 | $80 | $100 | $150 | $50 |

Total costs - sum of fixed and variable costs / sum of cost of goods sold and expenses

cost of goods sold - direct costs of producing the goods sold by a company - costs of material + production labor. e.g costs of flour, sugar to make a cake, baker’s wages

expenses = overhead costs - day to day operating expenses of a business but not directly related to creating a product. e.g rent, insurance, marketing, wages of sales people

Types of profit

Profit - difference between revenues and total costs

gross profit - difference between revenues and direct production costs.

formula = gross profit - expenses = net profit

Dividend - payment out of profit to shareholders as a reward for their investment

Retained profit - profit remaining after all expenses, tax and dividends have been paid which is then reinvested back into the business

| January | February | March |

Sales (loaves) | 500 | 400 | 550 |

Cost of sales ($) | $400 | $300 | $450 |

Expenses ($) | $300 | $300 | $300 |

Total Revenues | $1000 | $800 | $1100 |

Total costs | $700 | $600 | $650 |

Why is profit important?

acts as a reward for business owners for the risk of investing into the business

to attract investors who provide additional funds for business expansion

a measure of success of a business and performance of managers

source of finance - retained profit as an internal source of finance

to decide wether to continue making and selling a product or not

to decide if to expand the business / buy fixed assets

Profit vs Cash

cash flow does not = profit

Cash : pays day to day expenses → important to business in short term + long term

Profit : measure of success of a business → important in long term

practice : how do the following directly affect cash flow and profit

Business takes a bank loan : cash increases, profit unchanged

Business buys a new machine : cash decreases, profit unchanged

Business sold goods, but will receive money for it next month : cash unchanged, profit increased

Profitable businesses can run out of cash if :

they buy too many fixed assets at once

they offer too long trade credit periods

expanding too quickly / too many inventories

Sales of goods

$45,000 (50% for cash, 50% on one month’s credit )

Cost of sales

$12,000 (all paid in cash)

Expenses

$10,000 (all paid in cash)

1) Calculate Gross profit and profit made by the business in this month. 33,000

2) Calculate closing balance (of cash flow) at the end of the month. Assume that the business held no cash at the beginning of the month. Profit - 23000, cash inflows - 22500, cash outflow - 22000, closing balance - 500.

3) Explain why the answers to questions a) and b) are different. Gross profit is the difference between revenues and direct production costs whereas cash flow is cash inflow (22500) - cash outflow (22000)

Income statement - financial statement which records the revenue, costs and profits of a business for a given period of time (usually 1 year)

Necessary for strategic decision-making - e.g where to set up a business? What products to sell?

Important for

shareholders : high profit → high dividend + value of shares in the market increases

Employees : high security → job security + bonus to wages

Managers : higher profit → higher taxes received

Lenders : higher profit → safe to pay the loans on time and in sufficient amount

suppliers : higher profit → promise of future purchases of their supplies

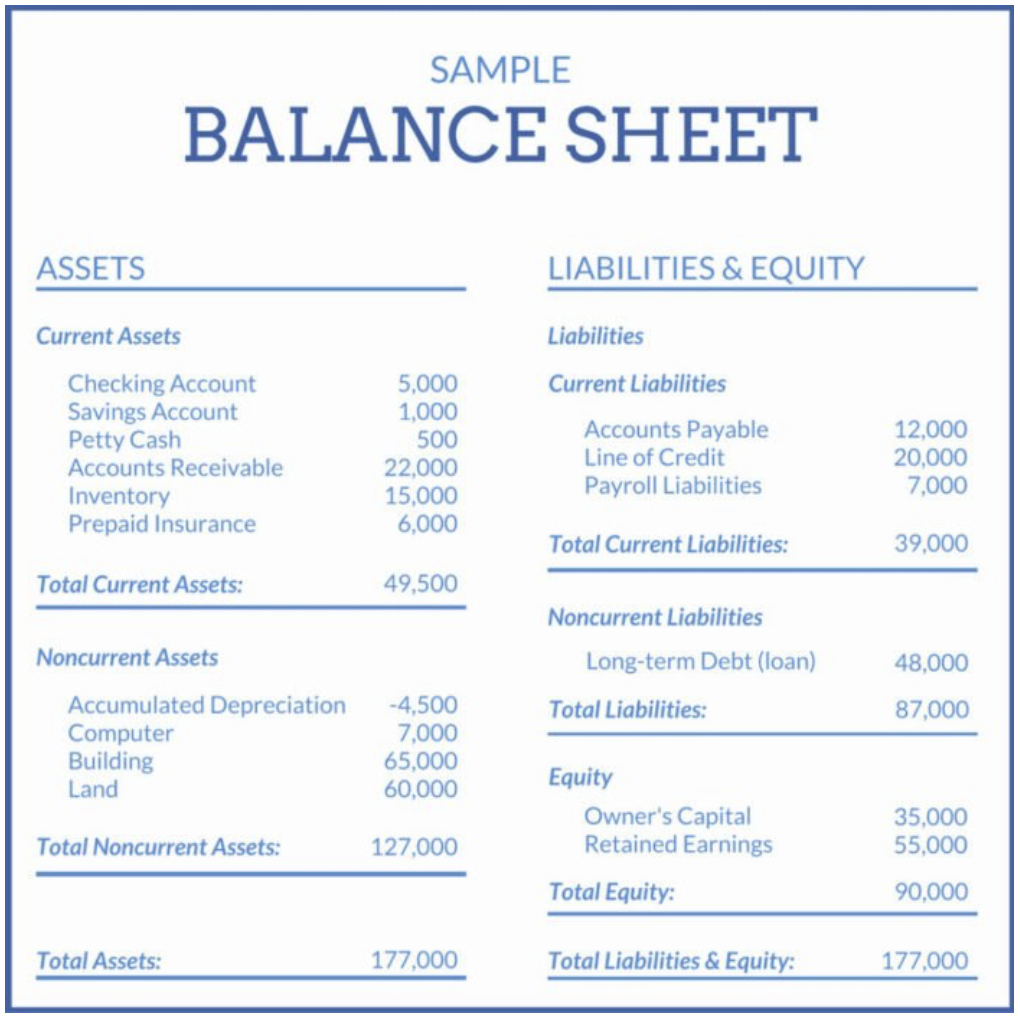

statement of financial position (balance sheet)

Vocab

statement of financial position/balance sheet - an accounting statement that records assets, liabilities and owner’s equity of a business at a particular date.

assets - resources which are owned by a business

liabilities - debts of a business that will have to be paid sometime in the future

owner’s equity (total equity) - amount owed by business to its owners, including capital and retained profit. - needs to be done by an incorporated business at the end of each financial year

The balance sheet measures how much a business owns and where the money comes from on one particular day.

current assets - resources that the business owns and expects to convert to cash before the date of the next balance sheet. (up to 1 year)

e.g cash, inventories, trade receivables

non-current (fixed) assets - resources that a business owns and expects to use for more than one year.

e.g land, buildings, machinery, cars, computers, depreciation

current liabilities - short term debts of the business which it expects to pay before the date of the next balance sheet (up to 1 year)

overdraft, taxes, dividends, trade payables

non-current liabilities - long term debts of the business which will be payable in more than one year

e.g long term bank loans, mortgages, debentures

Owner’s equity - money invested by owners (own savings + retained profit )

known as shareholders equity in limited liability companies

Capital employed = not current liabilities + shareholders equity

Net assets = total assets - total liabilities

how to interpret balance sheets

a balance sheet shows :

assets

assets that the business owns and their value

what the business is owed and its value

liabilities

what the business owes and it value

how the business finances its activities

amount of working capital as a key indicator of business liquidity

working capital = net current assets = current assets - current liabilities

decreasing the amount of net current assets = problem if left unchecked

limitations of balance sheets

only shows the financial position of a business for one particular day

values of assets/liabilities can change quickly

values of non current (fixed) assets displayed on the balance sheet might not reflect market value of these assets

does not show trends/flows

not a good indicator of how much a business is worth

Use of balance sheets

How can various stakeholder groups use data

from the Balance Sheet?

Banks : if you have lots of current/non current liabilities lending more money to you is risky. If you have lots of non current assets you can use them as collateral for your new loan (debt)

Shareholders : to know how much a business is worth. To know if the business is managed well. e.g do they have enough working capital (net current assets)?

Government : to see if a business is doing well or if the government needs to interfere. e.g subsidies

A

A - 30,000

B - 35,000

C - 400

D - 700

E - 37700 - 8300 = 29400

F - 31,300

B

Clear Ver could have bought new machinery for the value of 2 thousand $. Additionally the market value of the machinery could have increased

C

As we can see from 2016 to 2018 the value of machinery increased. This means it is likely that they bought new machinery. Because of the new/more machines productivity might have increased and from that revenue and retained profit leading to the increase of shareholders equity. Additionally, the demand for glasses might have increased from 2016 to 2018 this means that revenue would increase and therefore have higher profit and retained profit this lead to higher shareholders equity.

D

Yes the bank should be concerned with Clear Ver’s existing borrowing as they have a lot of both current and non current liabilities (7800$) . This means that the bank is taking a high risk when lending money to Clear Ver as it is less likely that they will pay bank the bank. This would make it unlikely for the bank to give Clear Ver a loan and if they do it is likely to be at a high interest rate. They do however have some fixed assets which could be used as collateral.

Analysis of Final Accounts : profitability

Gross Profit = Revenues - cost of sales

Profit = TR-TC

Profit = Revenues - ( Costs of sales + overhead costs)

capital employed = Non current liabilities + total equity

total equity = total assets - total liabilities

Key financial objectives of every business

Profitability - measurement of profit made relative to value of sales or capital invested in the business ( not same as profit )

Liquidity - ability of a business to pay its short term debts - need to have enough cash/working capital to pay for day to day operations and debt

Tools to measure business profitability

1) Gross Profit Margin - ratio between gross profit and revenue

gross profit earned per 1$ of revenue

(gross profit/revenues) x 100

higher gross profit margin -

higher revenues without similar increase in cost of sales

keeping revenues and lowering costs of goods sold

Added value = selling price - direct costs

Higher gross profit margin → business added more value to the good

2) Profit Margin - ratio between profit before tax and revenue

profit earned per 1$ revenue

(profit/revenues) x 100

affected by revenues + cost of goods sold + expenses

higher profit margin - higher revenues without similar increase in costs of sales, keeping revenues and lowering cost of goods sold

lowering expenses (overheads)

profit margin < gross profit margin : difference between profit margin and gross profit margin reflects expenses,

small difference → expenses are low → costs controlled well,

big differences → expenses are high → need to control them better

3) Return on capital employed - ratio between profit before tax and capital employed

profit earned per 1$ invested into the business

(profit/capital employed) x 100

Most used to measure efficiency → used most often to assess profitability

Analysis on ROCE :

ROCE increases overtime → business getting more profitable

if ROCE of business A > ROCE of business B → Business A more profitable

If ROCE is high, business uses its resources efficiently

Analysis of Final Accounts : Liquidity

Tools to measure business liquidity

1) Current ratio - ratio between current assets and current liabilities

= current assets/current liabilities

best values = 1.5:1<current ratio< 2:1

if less → risk of not having enough cash to pay short term debts → cash flow problems

if more → business has too much cash in unprofitable assets → missing on potential gains

Limitation - inventories are the least liquid form of current assets → including them can skew the current ratio significance

inventories are less liquid because :

it takes time to sell finished goods

when goods are sold on credit → business needs to wait for customer to pay

2) Acid test ratio - ratio between liquid assets and current liabilities

eliminates the problem with considering inventories as the least liquid form of current assets

better indicator of liquidity than current ratio

= (current assets - inventories) / current liabilities

Best value = 1:1

if less → risk of not having enough cash to pay short term debts → cash flow problems

if more → business has too much cash in unprofitable assets → missing on potential gains

Profitability vs Liquidity

Need to keep a balance between profitability + liquidity , but the problem is…

a lot of cash increases liquidity but limits future profitability (as it is not used to buy profit making assets)

having a lot of non current (fixed) assets improves profitability in long run but limits liquidity in short run

benefits and limitations of Ratio analysis

Benefits

stakeholders can compare ratios over time → can identify trends

No need to investigate all financial statements to get the information → information received quickly

Stakeholders can compare results with other businesses to see how well it is doing

Limitations

Ratios compare past data, does not predict the future

Ratios do not include all strengths + weaknesses that affect profitability e.g quality of human capital

Financial statements prepared in different ways from company to company → harder to compare

Effect of external factors e.g laws,exchange rates,economic factors are not considered

Who cares about Ratio analysis

Owners + shareholders

More profit → higher dividends (return on investment). Hoe does it compare with returns if we invested the money elsewhere?

If the businesses market balue rises, value of shares goes up → wealth building

Potential inventors

More profit → higher dividends. How does it compare with returns if we invested the money elsewhere?

Lenders

Higher profit + liquidity → safe that lenders will recieve money + interest back

Managers

Are financial objectives (e.g revenue targets,cost controlling) achieved?

Identify strengths & weaknesses → decide if any strategies need to be changed

How to improve future business performance?

More retained profit → chance to buy new technologies in the future

Trade Payables

does the business have enough working capital to pay for the goods on credit?