Unit 4

==4.1 The Role of Marketing==

Marketing - the management task that links the business to the customer by identifying and meeting the needs of customers profitably – it does this by getting the right product at the right price to the right place at the right time

Marketing functions:

- market research

- product design

- pricing

- advertising

- distribution

- customer service

- packaging

Market size - the total level of sales of all producers within a market

Market growth - the percentage change in the total size of a market (volume or value) over a period of time

Ease of entry - the lack of barriers for the establishment of new competitors in a market

Homogeneous products - goods that are physically identical or viewed as identical by consumers

Segmentation - dividing a market into distinct groups of consumers who share common tastes and requirements

Target marketing - focusing marketing activity on particular segments of the market

Mass marketing - selling to the whole market using a standardised product and the same marketing activities

Consumer good - tangible physical product marketed to end users (consumers)consumer service:intangible provision of an activity to end users (consumers)

Market orientation - an outward-looking approach basing product decisions on consumer demand, as established by market research

Product orientation - an inward-looking approach that focuses on making products that can be made– or have been made for a long time – and then trying to sell them

Social (societal) marketing - this approach considers not only the demands of consumers but also the effects on all members of the public (‘society’) involved in some way when firms meet these demands

Market share - the percentage of sales in the total market sold by one business

Market leadership - when a business has the highest market share of all firms that operate in that market

Marketing objectives - the goals set for the marketing department to help the business achieve its overall objectives

- ==For profit organisations==

The long-term objectives of a company can affect its marketing objectives and strategies. Companies that aim for short-term profits tend to prioritize high sales and prices, while those with longer-term objectives may prioritise both profitability and social responsibility, leading to a "societal marketing" approach

Examples of marketing objectives:

- market share – perhaps to gain market leadership

- total sales (value or volume – or both)

- average number of items purchased per customer visit

- frequency that a loyal customer shops

- percentage of customers who are returning customers (customer loyalty)

- number of new customers

- customer satisfaction

- brand identity

- ==Non-profit org==anisations

Not-for-profit organizations differ from profit-maximizing organizations in three main ways. Firstly, they do not have external shareholders providing risk capital. Secondly, they do not distribute dividends, and instead, any profits or surpluses are retained by the organization for further capital. Thirdly, their objectives typically include a social, cultural, philanthropic, welfare, or environmental dimension.

Examples of marketing objectives:

- maximise revenue from trading activities

- increase recognition of the organisation by society

- promote the work and aims of the organisation to a wide audience

What are the differences in marketing in non-profit-making organisations compared to marketing in profit-seeking ones?

- The importance of maintaining high ethical standards to avoid alienating the public

- Constant feedback on the success of charity campaigns – and future issues to be addressed – to maintain public interest and awareness

- Free publicity, with the aim of capturing the public’s imagination, for example for fundraising events and stunts, is much more important for charitable causes than for most consumer products.

==4.2 Marketing Planning==

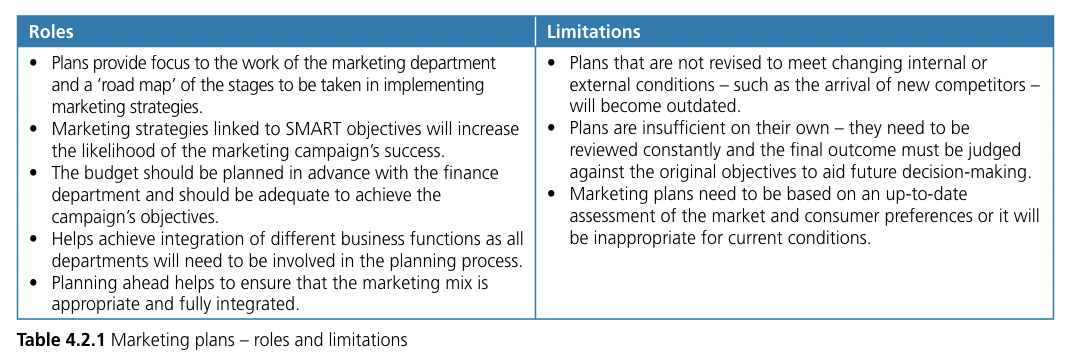

Marketing planning - the process of formulating appropriate strategies and preparing marketing activities to meet marketing objectives

The main elements of a marketing plan are:

details of the company’s (SMART) marketing objectives

sales forecasts to allow the progress of the plan to be monitored

marketing budget – how much finance is planned to be spent and how it is to be allocated

marketing strategies to be adopted to achieve the marketing objectives

detailed action plans showing the marketing tactics to be used to implement the strategies

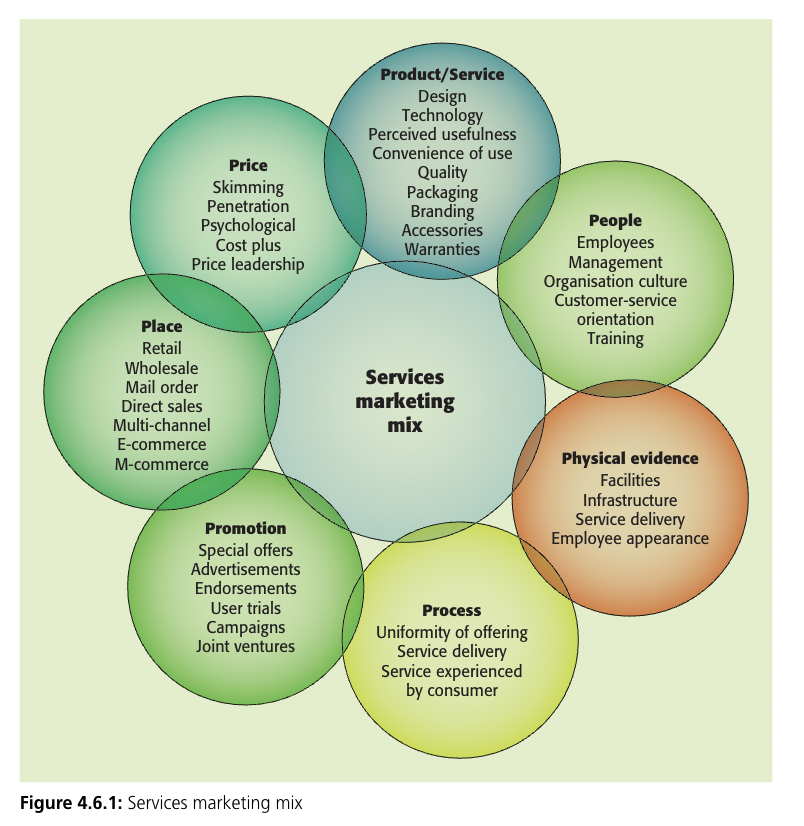

Marketing mix - the key decisions that must be taken in the effective marketing of a product

4 Ps:

- Product – consumers require the right good or service. This might be an existing product, an adaptation of an existing product or a newly developed one.

- Price - is important too. If set too low, then consumers may lose confidence in the product’s quality; if too high, then many will be unable to afford it.

- Promotion - must be effective and targeted at the appropriate market – telling consumers about the product’s availability and convincing them that ‘your brand’ is the one to choose. Packaging is often used to reinforce this image.

- Place - refers to how the product is distributed to the consumer. If it is not available at the right time in the right place, then even the best product in the world will not be bought in the quantities expected.

Coordinated marketing mix - key marketing decisions complement each other and work together to give customers a consistent message about the product

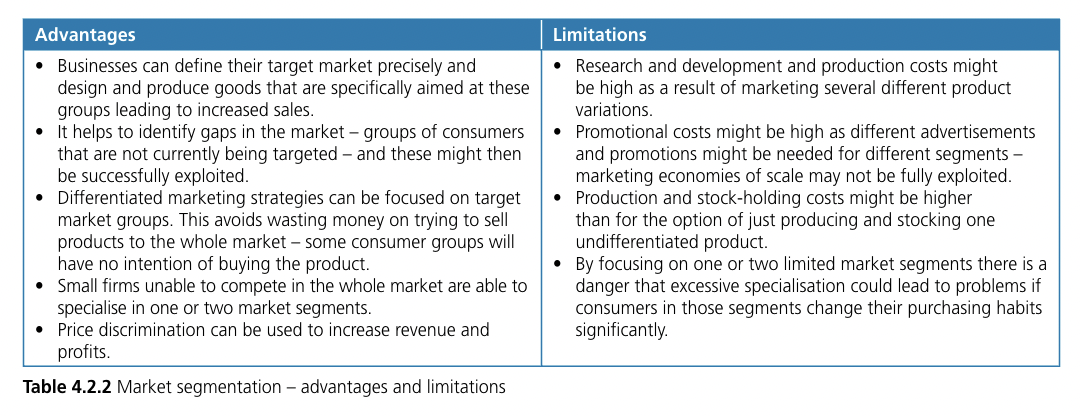

Market segment - a sub-group of a market made up of consumers with similar characteristics, tastes and preferences

Target market - the market segment that a particular product is aimed at

Market segmentation - identifying different segments within a market and targeting different products or services to them

Consumer profile - a quantified picture of consumers of a firm’s products, showing proportions of age groups, income levels, location, gender and social class

Identifying the different consumer groups:

Geographical differences

Demographic differences

here are just few examples:

- DINKY – double income no kids yet

- NILK – no income lots of kids

- WOOF – well-off older folk

Psychographic factors

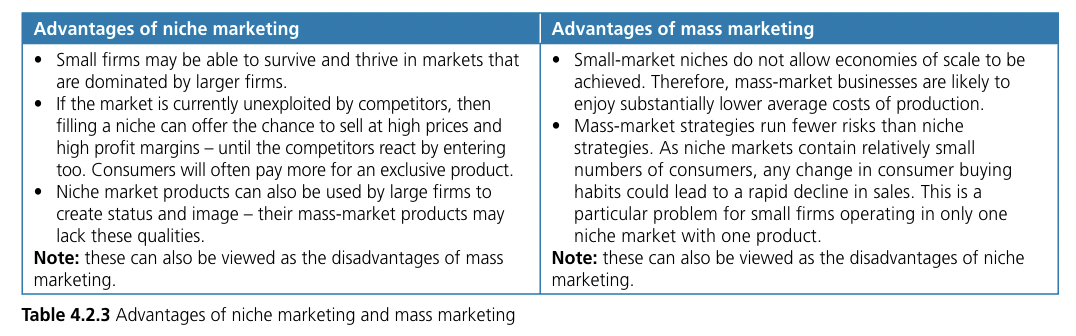

Niche market - a small and specific part of a larger market

Niche marketing - identifying and exploiting a small segment of a larger market by developing products to suit it

Mass market - a market for products that are often standardised and sold in large quantities

Mass marketing - selling the same products to the whole market with no attempt to target groups within it

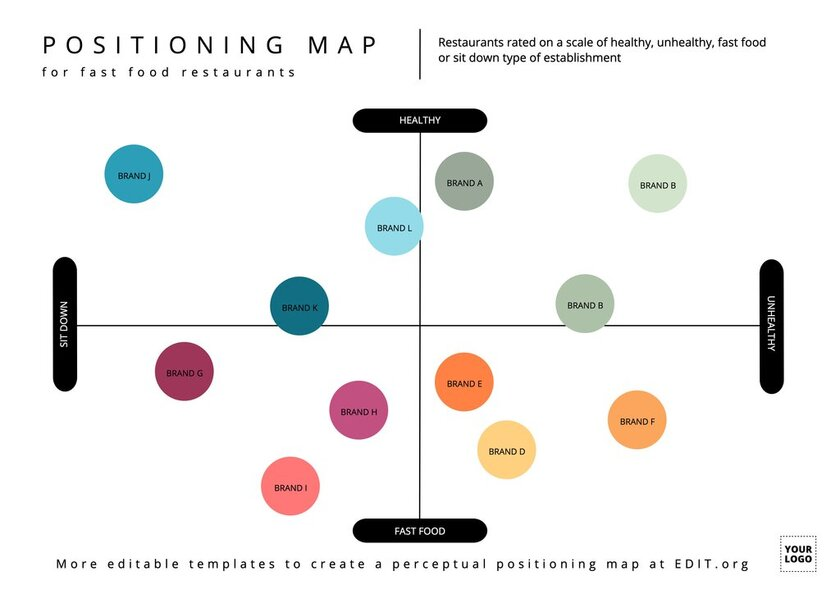

Product position map or perception map - a graph that analyses consumer perceptions of each of a group of competing products in respect of two product characteristics

This product-positioning analysis could be used in a number of ways:

- It identifies potential gaps in the market.

- Having identified the sector with the greatest ‘niche’ potential the marketing manager is then made aware of the key feature(s) of the product that should be promoted most heavily.

- This analysis is used to monitor the position of existing brands a firm can easily see if a repositioning of one of them is required.

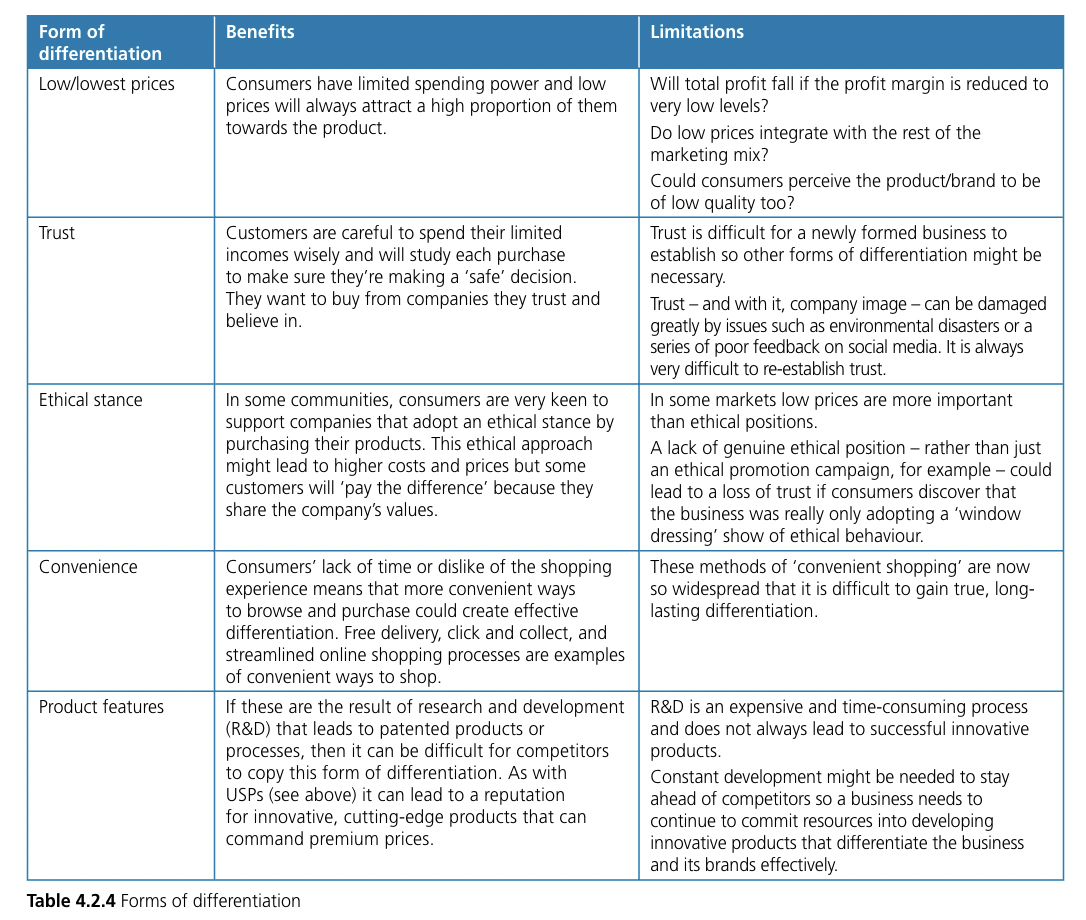

Unique Selling Point/Proposition (USP) - a factor that differentiates a product from its competitors, such as the lowest cost, the highest quality or the first-ever product of its kind; a USP could be thought of as “what you have that competitors don’t”

%%Pros of a good USP%%:

effective promotion which focuses on the differentiating feature of the product or service

opportunities to charge higher prices due to exclusive design/service

free publicity from business media reporting on the USP

higher sales than undifferentiated products

customers more willing to be identified with the brand because “it’s different”

==4.3 Sales Forecasting (HL ONLY)==

Sales forecasting - predicting future sales levels and sales trends

%%Potential Pros of Sales Forecasting%%:

- The operations department would know how many units to produce and what quantity of materials to order and the appropriate level of stock to hold.

- The marketing department would be aware of how many products to distribute and whether changes to the existing marketing mix were needed to increase sales.

- Human resources workforce plan would be more accurate, leading to the appropriate number of workers and the most appropriate employment contracts – permanent or temporary.

- Finance could plan cash flows with much greater accuracy and make accurate profit forecasts.

- Strategic decision-making – such as developing new products or entering new markets– would become much better informed

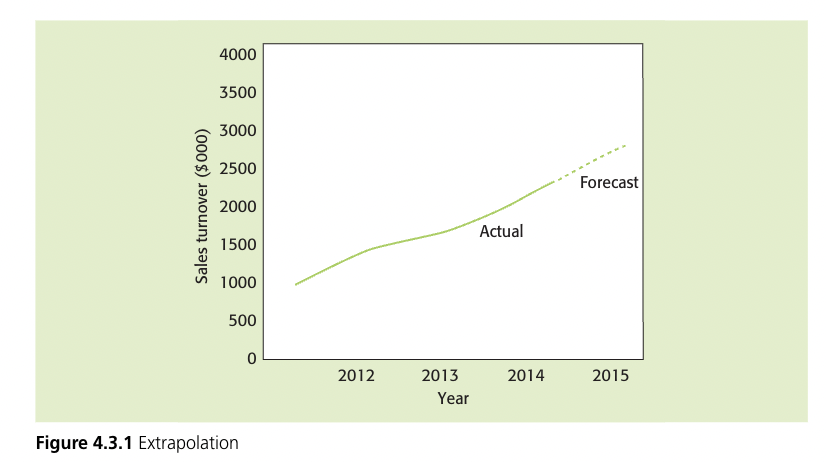

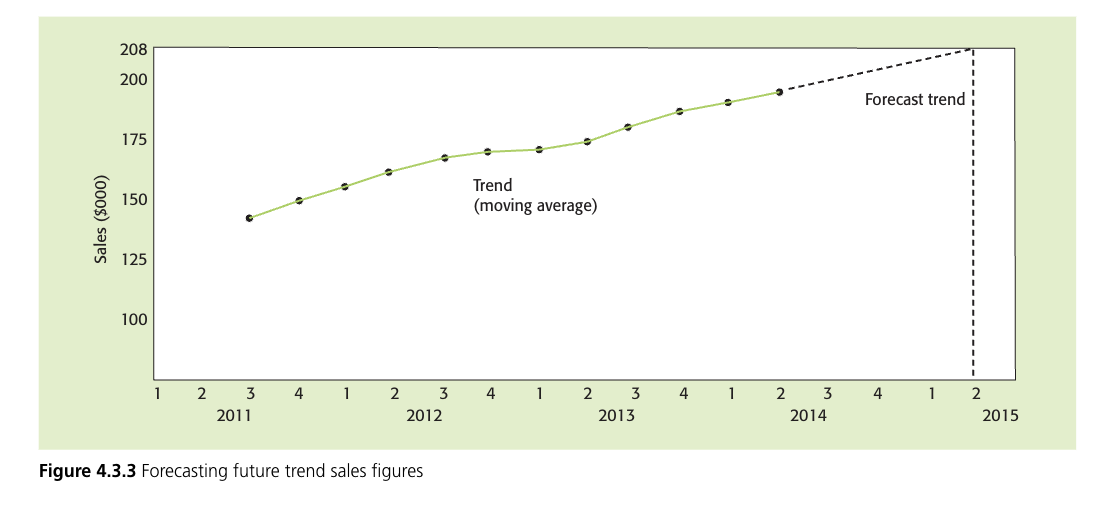

Extrapolation - involves basing future predictions on past results. When actual results are plotted on a time-series graph, the line can be extended, or extrapolated, into the future along the trend of the past data (see Figure 4.3.1). This simple method assumes that sales patterns are stable and will remain so in the future. It is ineffective when this condition does not hold true.

Seasonal variations - regular and repeated variations that occur in sales data within a period of 12 months or less

Cyclical variations - variations in sales occurring over periods of time of much more than a year – they are related to the business cycle

Random variations - may occur at any time and will cause unusual and unpredictable sales figures, e.g. exceptionally poor weather, or negative public image following a high-profile product failure

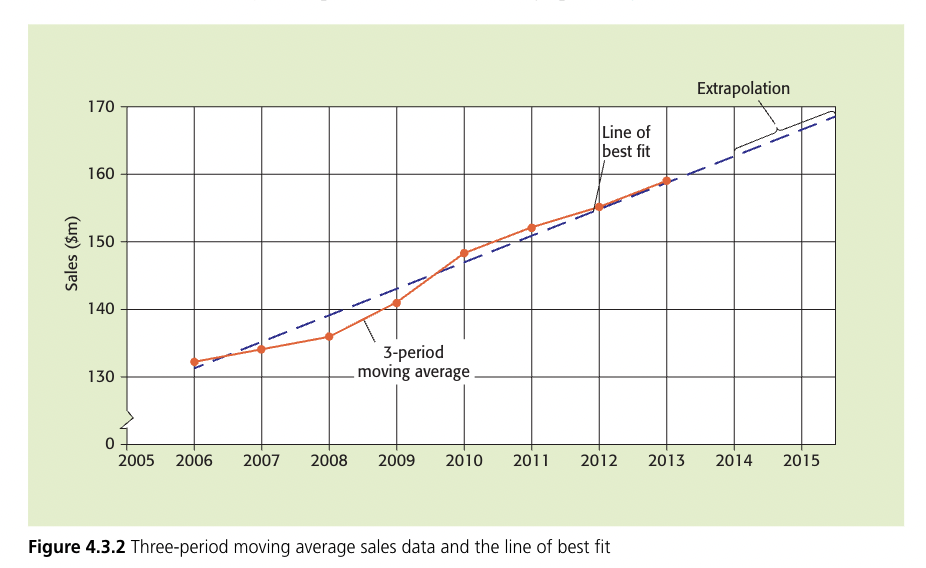

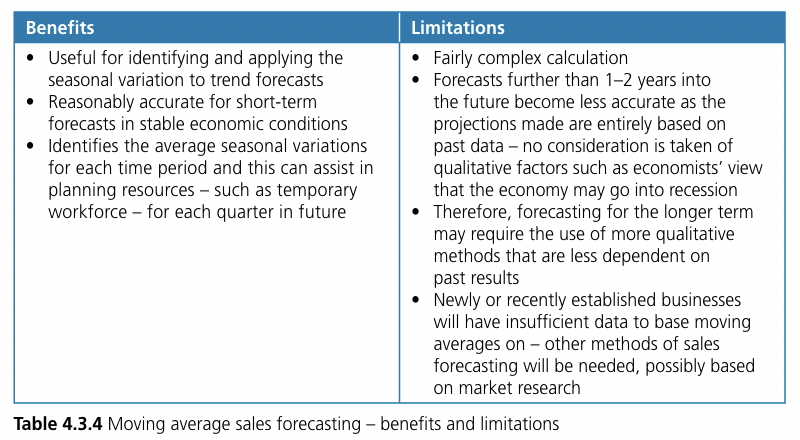

Four-period moving average - This is possibly the most widely used technique as it is often employed when forecasting from quarterly data. Much macro-economic data is released quarterly but if it is collected as monthly sales then a 12-period moving total can be used.

Trend - underlying movement of the data in a time series

[[Forecasting using the moving average method:[[

Plot the trend (moving average) results on a time-series graph

Extrapolate this into the future – short-term extrapolations are likely to be the mostaccurate

Read off the forecast trend result from the graph for the period under review, e.g. quarter 2 in year 2015.

Adjust this by the average seasonal variation for quarter 2. Thus, for quarter 2 in the year 2015: the actual forecast will be the extrapolated trend forecast for this quarter, $208000, plus the average seasonal variation of –$4580 =$203420

==4.4 Market Research==

Market research - process of collecting, recording and analysing data about customers, competitors and the market

Why is market research needed?

- To reduce the risks associated with new product launches

- To predict future demand changes

- To explain patterns in sales of existing products and market trends

- To assess the most favoured designs, flavours, styles, promotions and packages for a product

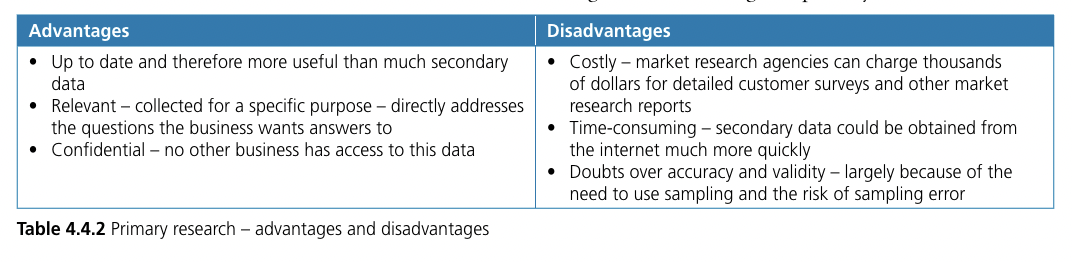

Primary research - the collection of first-hand data that are directly related to a firm’s needs

Secondary research - collection of data from second-hand sources

Qualitative research - research into the in-depth motivations behind consumer buying behaviour or opinions

Quantitative research - research that leads to numerical results that can be presented and analysed

==Methods of primary research==:

- Surveys - detailed study of a market or geographical area to gather data on attitudes, impressions, opinions and satisfaction levels of products or businesses, by asking a section of the population

- Questionnaire design:

- open questions - those that invite a wide-ranging or imaginative response

- closed questions - questions to which a limited number of preset answers is offered

Interviews

Focus groups - a group of people who are asked about their attitude towards a product, service, advertisement or new style of packaging

Observation

- Observational technique - a qualitative method of collecting and analysing information obtained through directly or indirectly watching and observing others in business environments’ e.g. watching consumers walk round a supermarket

Test marketing - marketing a new product in a geographical region before a full-scale launch

==Secondary data can be obtained from the following sources:==

- Market intelligence analysis reports

- Academic journals

- Government publications

- Local libraries and local government offices

- Trade organisations

- Media reports and specialist publications

and etc…

Sample - group of people taking part in a market research survey selected to be representative of the target market overall

Sampling error - errors in research caused by using a sample for data collection rather than the whole target population

Selecting an appropriate sample. The ones below are the most commonly used:

- Quota sampling - gathering data from a group chosen out of a specific sub-group, e.g. a researcher might ask 100 individuals between the ages of 20 and 30 years

- Random sampling - every member of the target population has an equal chance of being selected

- Stratified sampling - this draws a sample from a specified sub-group or segment of the population and uses random sampling to select an appropriate number from each stratum

- Cluster sampling - using one or a number of specific groups to draw samples from and not selecting from the whole population, e.g. using one town or region

- Snowball sampling - using existing members of a sample study group to recruit further participants through their acquaintances

- Convenience sampling - drawing representative selection of people because of the ease of their volunteering or selecting people because of their availability or easy access

==4.5 The Four Ps==

1. Product

the end result of the production process sold on the market to satisfy a customer need

Consumer durables - manufactured products that can be reused and are expected to have a reasonably long life, such as cars

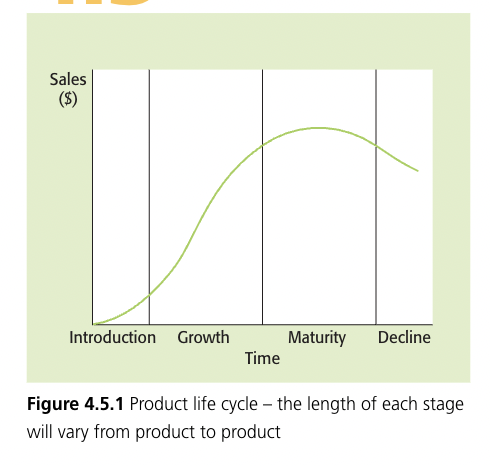

Product life cycle - the pattern of sales recorded by a product from launch to withdrawal from the market

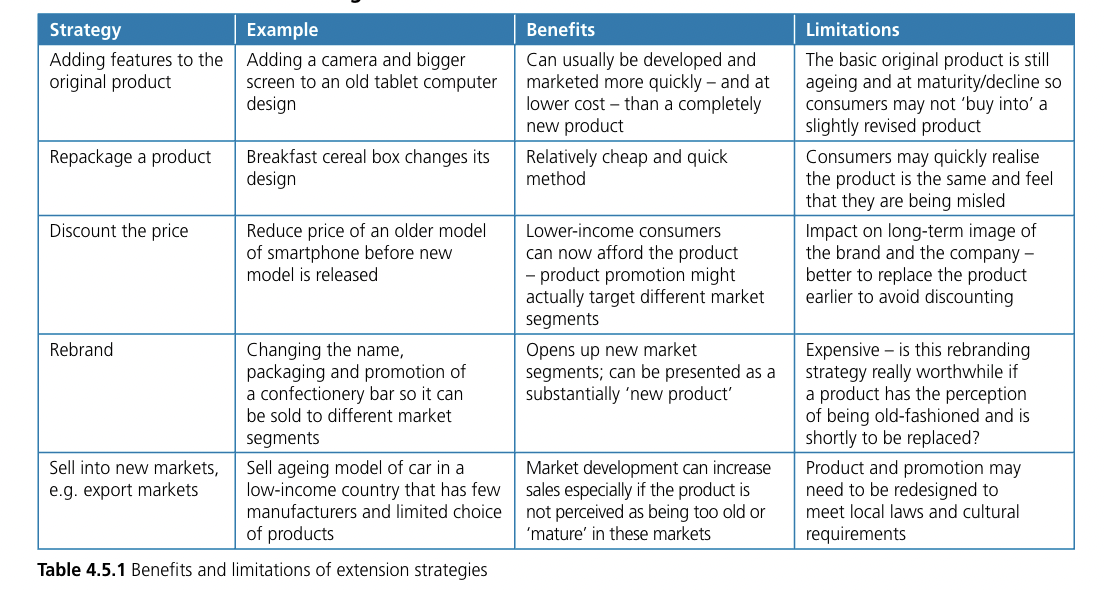

Extension strategies - marketing plans that extend the maturity stage of the product before a brand new one is needed

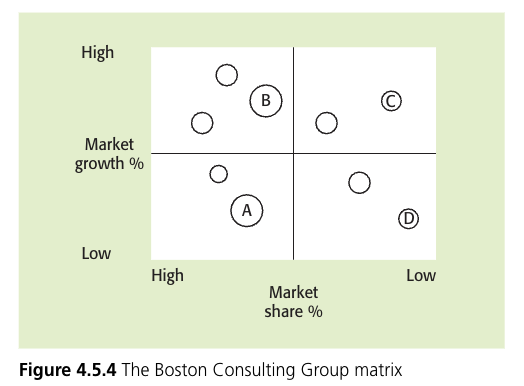

Boston Consulting Group matrix - a method of analysing the product portfolio of a business in terms of market share and market growth

- Cash Cow

- The product is well-established in a mature market, with high sales and low promotional costs due to consumer awareness. It generates a high positive cash flow and is profitable, making it a "cash cow" that can be used to fund other products in the portfolio. The business aims to maintain these products as long as possible, especially if they can maintain their high market share without much additional promotional spending

- Star

- The product is successful in an expanding market and is referred to as a "star." The company will aim to maintain its market position and may invest heavily in promotion to differentiate it and reinforce its brand image. Despite these costs, the product is likely to generate high income. If the product's status and market share can be maintained, it could become a future "cash cow" as the market matures and growth slows

- Problem Child

- The "problem child" is a product that requires significant resources but generates little return, particularly in the short term. If it's a new product, heavy promotional costs may be required, which could be funded by the cash cow. The future of the product may be uncertain, and quick decisions may need to be taken if sales do not improve, such as revising the design, relaunching or withdrawing from the market. However, the product may have potential as it's in a growing market sector, and businesses need to carefully analyze which problem children are worth developing and investing in, and which ones to drop and stop selling.

- Dog

- "Dogs" are products that offer little to the business in terms of existing sales, cash flow, or future prospects because the market is not growing. The business may decide to replace these products shortly or withdraw from the market sector altogether and position itself into faster-growing sectors

Boston Consulting Group matrix and strategic analysis:

- Holding – continuing support for star products so that they can maintain their good market position. Work may be needed to ‘freshen’ the product in the eyes of the consumers so that high sales growth can be sustained.

- Building – supporting problem child products with additional advertising or further distribution outlets. The finance for this could be obtained from the established cash cow products.

- Milking – taking the positive cash flow from established products and investing in other products in the portfolio.

- Divesting – identifying the worst performing dogs and stopping the production and supply of these. This strategic decision should not be taken lightly as it will involve other issues such as the impact on the workforce and whether the spare capacity freed up by stopping production can be used profitably for another product.

Brand - an identifying symbol, name, image or trademark that distinguishes a product from its competitors

Brand awareness - extent to which a brand is recognised by potential customers and is correctly associated with a particular product – can be expressed as a percentage of the target market

Brand loyalty - the faithfulness of consumers to a particular brand as shown by their repeat purchases irrespective of the marketing pressure from competing brands

Brand development - measures the infiltration of a product’s sales, usually per thousand population; if 100 people in 1000 buy a product, it has a brand development of 10

Brand value (or brand equity) - the premium that a brand has because customers are willing to pay more for it than they would for a non-branded generic product

Family branding - a marketing strategy that involves selling several related products under one brand name (also known as umbrella branding)

Product branding - each individual product in a portfolio is given its own unique identity and brand image (also known as individual branding)

Company or corporate branding - the company name is applied to products and this becomes the brand name

Own-label branding - retailers create their own brand name and identity for a range of products

Manufacturers’ brands - producers establish the brand image of a product or a family of products, often under the company’s name

2. Price

Pricing Strategies:

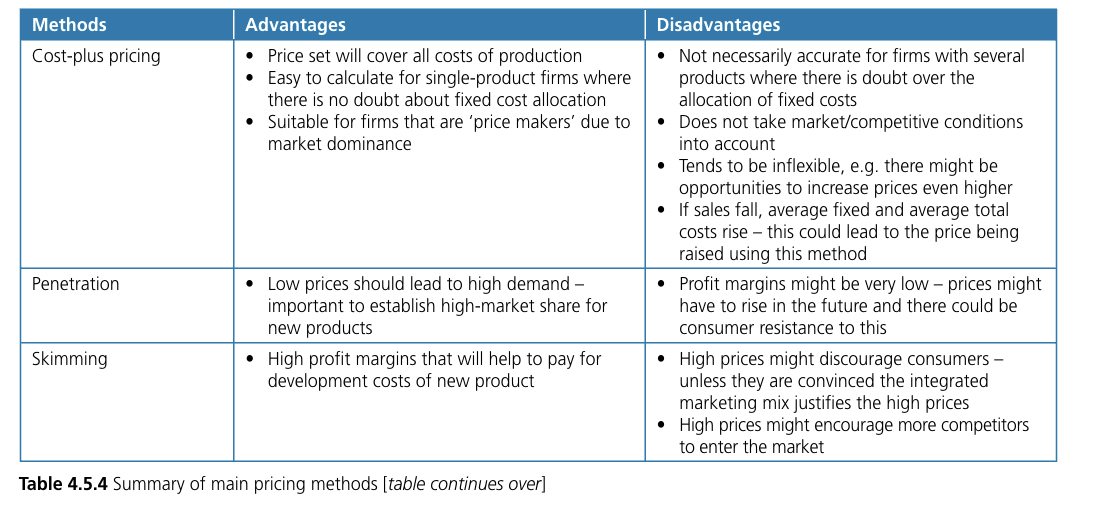

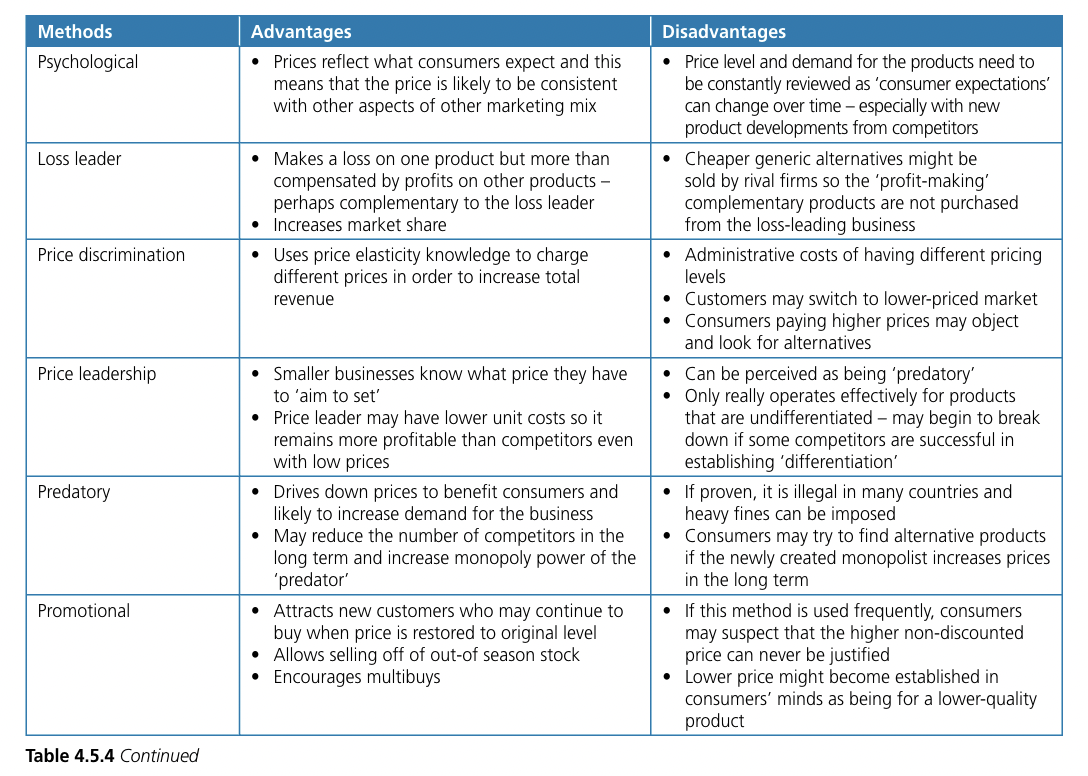

Cost-plus pricing - adding a fixed mark-up for profit to the unit price of a product

Penetration Pricing - setting a relatively low price often supported by strong promotion in order to a achieve high volume of sales

Market Skimming - setting a high price for a new product when a firm has a unique or highly differentiated product with low price elasticity of demand

Psychological Pricing - setting prices that take account of customers perception of value of the product

Loss leader - products sold at a very low price to encourage customers to buy them

Price discrimination - occurs when a business sells the same product to different customers at different price

Promotional pricing - special low price to gain market share or sell off excess stock “buy one get one free”

Price leadership - exists when one business sets a price for its products and other firms in the market set the same or similar prices

Predatory pricing - deliberately undercutting competitors prices in order to try and force them out of the market

3. Promotion

Promotion - the use of advertising, sales promotion, personal selling, direct mail, trade fairs, sponsorship and public relations to inform consumers and persuade them to buy

Promotion Strategies:

- Above-the-line promotion - a form of promotion that is undertaken by a business by paying for communication with consumers, e.g.advertising

- Below-the-line promotion - promotion that is not a directly paid-for means of communication but based on short-term incentives to purchase, e.g. sales promotion techniques

- Sales promotion - incentives such as special offers or special deals directed at consumers or retailers to achieve short-term sales increases and repeat purchases by consumers

- Promotion mix - the combination of promotional techniques that a firm uses to communicate the benefits of its products to customers

- Internet (online) marketing - refers to advertising and marketing activities that use the internet, email and mobile communications to encourage direct sales via electronic commerce

- Viral marketing - the use of social media sites or text messages to increase brand awareness or sell products

- Guerrilla marketing - an unconventional way of performing marketing activities on a very low budget

4. Place

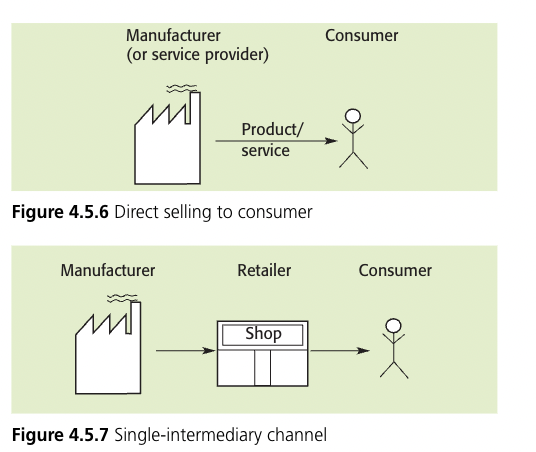

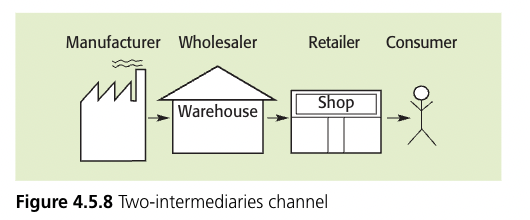

Channel of distribution - the chain of intermediaries a product passes through from producer to final consumer

Agent - a business with the authority to act on behalf of another firm, e.g. to market its products

==4.6 The Extended Marketing Mix of Seven Ps==

- People

- This element of the marketing mix refers to the employees and managers of a business and how they relate to customers and communicate with them. The people employed by a business – especially service businesses where customers cannot judge a company by the attributes of physical products – can either give it a competitive advantage or can lead to poor customer reaction and disloyal consumers.

- Process

- procedures and policies that are put in place to provide the service or the product to the consumer

- Physical Evidence

the ways in which the business and its products are presented to customers

- intangible products - a non-physical product – a service – provided to a consumer such as an insurance policy or a car repair

- tangible products - a physical object that can be touched such as a building, car, tablet, computer, or clothing

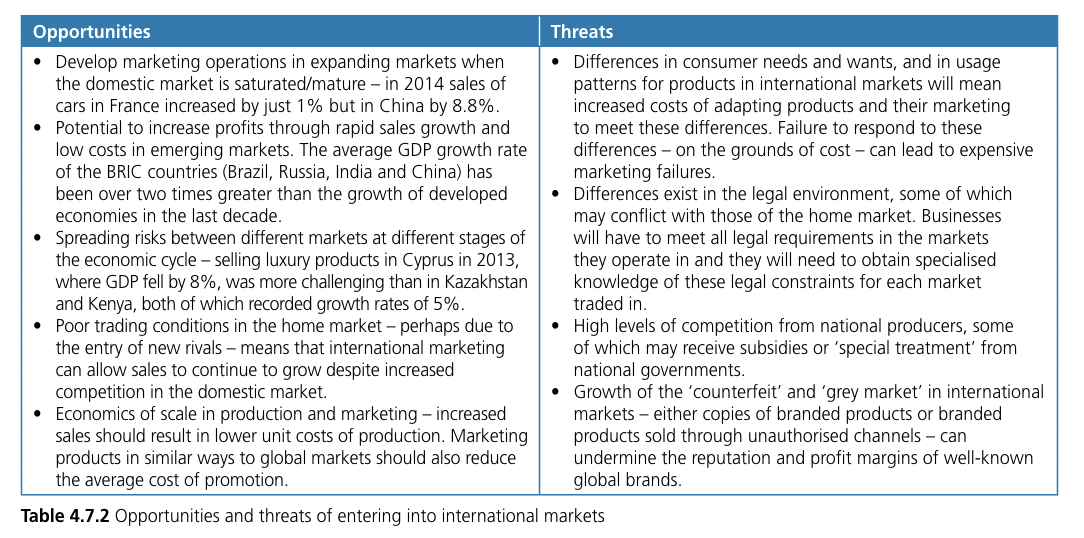

==4.7 International Marketing (HL ONLY)==

International marketing - selling products in markets other than the original domestic market

Globalisation - the growing trend towards worldwide markets in products, capital and labour, unrestricted by national barriers

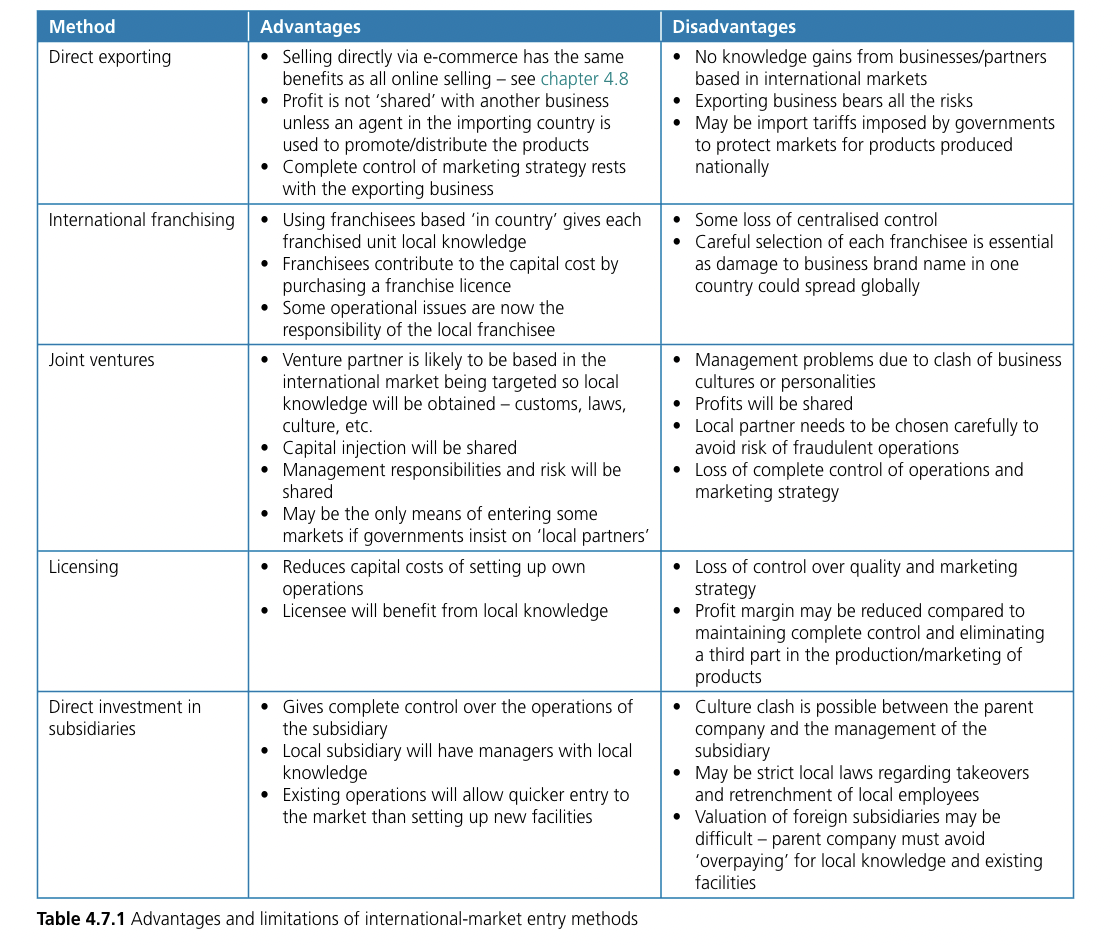

Methods of entry into international markets:

- Exporting

- International Franchising

- Joint Ventures

- Licensing - involves the business allowing another firm in the country being entered to produce its branded goods or patented products under licence, which will involve strictly controlled terms over quality

Direct investment in subsidiaries:

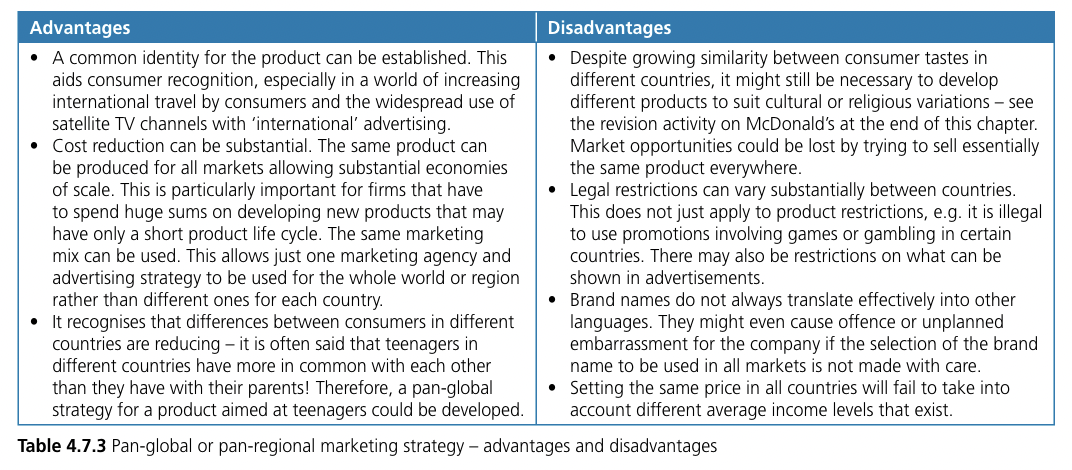

Pan-global marketing - adopting a standardised product across the globe as if the whole world were a single market – selling the same goods in the same way everywhere

Global localisation - adapting the marketing mix, including differentiated products, to meet national and regional tastes and cultures

Multinational companies - businesses that have operations in more than one country

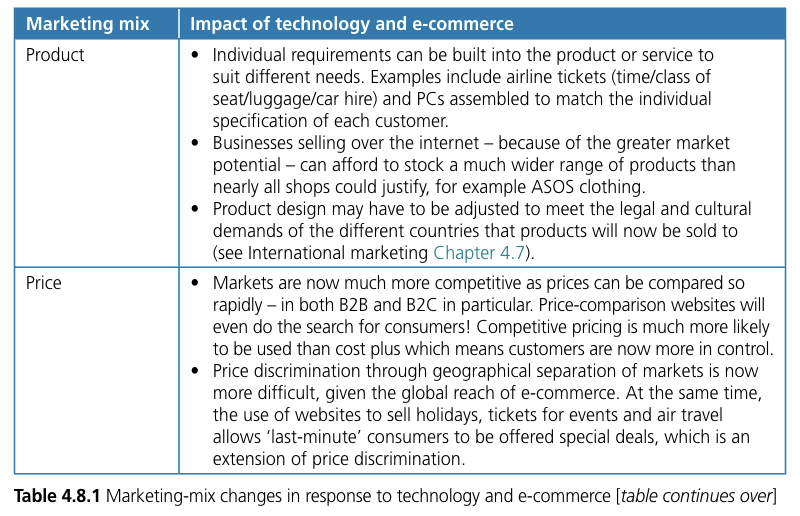

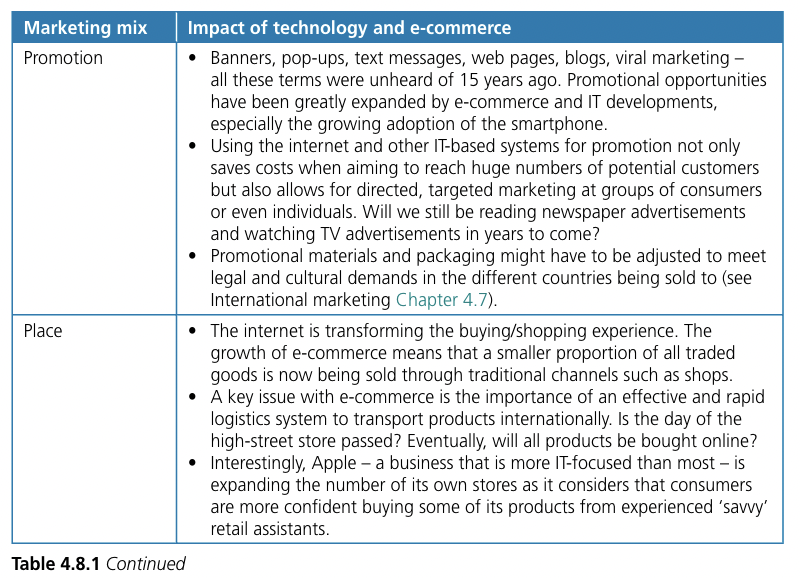

==4.8 E-commerce==

E-commerce - the buying and selling of goods and services on the internet

Global reach – internet technology reaches across national boundaries and opens up global markets with potentially billions of consumers. Consumers now have access to product details sold by businesses beyond local/national boundaries.

Ubiquity – the access to markets and consumer access to business is available at all times and (virtually) all locations. Shopping can take place anywhere and customer convenience is increased. The increasing use of smartphones has led to ‘m-commerce’ where mobile- phone shopping is now gaining greater popularity than PC or tablet shopping.

Interactivity – the internet allows for two-way communication between the business and the customer. The growth in the use of social media is further enhancing this.

Personalisation – marketing messages can now be targeted at individual consumers based on their previous spending habits, tastes and interests.

Information richness – complex and detailed promotional messages can be delivered by the internet via video, audio and text messages. This variety of media and the detail of the content cannot be equalled by other forms of promotion.

Universal standards – there is ease of access to the internet for both businesses and customers owing to the existence of a cheap universal internet system.

==Types of E-commerce:==

- Business to business (B2B) - transactions conducted directly between a supplying business and a purchasing business

- Business to consumer (B2C) - transactions conducted directly between a company and consumers who are the end-users of its products or services

- Consumer to consumer (C2C) - a business model based on e-commerce that creates a facility that allows consumers to trade with each other (sometimes known as customer to customer)

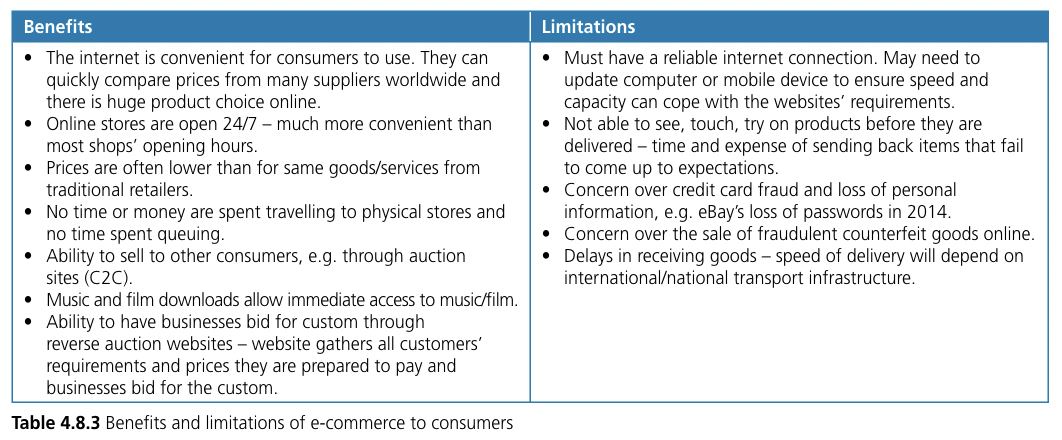

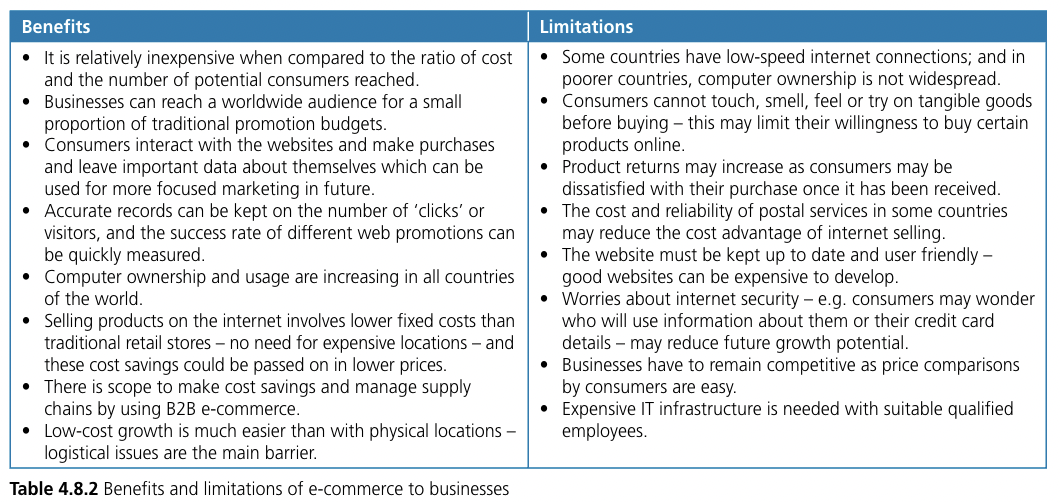

[[The Benefits and Limitations of E-commerce: [[

To businesses

To consumers