PRINCIPLES OF MARKETING NOTES Chapters 10-12

Chapter X: Product, Branding, and Packaging Concepts

What Is a Product?

A product is a good, a service, or an idea received in an exchange.

Good: A tangible physical entity

Service: An intangible result of the application of human and mechanical efforts to people or objects

Idea: A concept, a philosophy, an image, or an issue (MADD agency; public service group)

Classifying Products

Products fall into one of two general categories:

Consumer products: Products purchased to satisfy personal and family needs

Categorized according to how buyers generally behave when purchasing a specific item

Business products: Products bought to use in an organization’s operations, to resell, or to make other products

Classified according to their characteristics and intended uses in an organization

Purchased to satisfy the goals of the organization

Consumer Products

Convenience Products: Relatively inexpensive, frequently purchased items for which buyers exert minimal purchasing effort

Examples: Bread, soft drinks, chewing gum, gasoline, newspapers

Shopping Products: Items for which buyers are willing to expend considerable effort in planning and making purchases

Examples: Appliances, bicycles, furniture, stereos, cameras, shoes

Specialty Products: Items with unique characteristics that buyers are willing to expend considerable effort to obtain

Examples: Fine jewelry, limited-edition collector’s items

Unsought Products: Products purchased to solve a sudden problem, products of which customers are unaware, and products that people do not necessarily think about buying

Examples: Emergency medical services, automobile repairs

Product Line and Product Mix

Product Item: A specific version of a product that can be designated as a distinct offering among a firm’s products

Product Line: A group of closely related product items viewed as a unit because of marketing, technical, or end-use considerations

Product Mix: The total group of products that an organization makes available to customers

Width of Product Mix: The number of product lines a company offers

Depth of Product Mix: The average number of different product items offered in each product line

Product Life Cycles and Marketing Strategies

Product Life Cycle: The progression of a product through four stages: introduction, growth, maturity, and decline

Introduction

Introduction Stage: The initial stage of a product’s life cycle—its first appearance in the marketplace—when sales start at zero and profits are negative

Two difficulties may arise during the introduction stage:

Sellers may lack the resources, technological knowledge, and marketing expertise to launch the product successfully.

The initial product price may have to be high to recoup expensive marketing research or development costs, which can depress sales.

Most new products start off slowly and seldom generate enough sales to bring immediate profits.

It is estimated that only 15 to 25 percent of new products succeed in the marketplace.

Growth

Growth Stage: The stage of a product’s life cycle when sales rise rapidly and profits reach a peak and then start to decline

The growth stage is critical to a product’s survival because competitive reactions to the product’s success during this period will affect the product’s life expectancy.

A typical marketing strategy should seek to strengthen market share and position the product favorably against aggressive competitors by emphasizing product benefits.

Marketers should analyze competing brands’ product positions relative to their own and adjust the marketing mix in response to their findings.

The goal of the marketing strategy in the growth stage is to establish and fortify the product’s market position by encouraging adoption and brand loyalty.

Maturity

Maturity Stage: The stage of a product’s life cycle during when the sales curve peaks and starts to decline as profits continue to fall

This stage is characterized by intense competition because many brands are now in the market.

Producers who remain in the market are likely to change promotional and distribution efforts.

Marketers of mature products sometimes expand distribution into global markets, in which case products may have to be adapted to fit differing needs of global customers more precisely.

During this stage, marketers actively encourage resellers to support the product.

Maintaining market share during this stage requires promotion expenditures, which can be large if a firm seeks to increase market share through new uses.

Decline

Decline Stage: The stage of a product’s life cycle during when sales fall rapidly

Marketers must consider eliminating a product that no longer earns a profit or repositioning it to extend its life.

Marketers may also cut promotion efforts, eliminate marginal distributors, and finally, plan to phase out the product.

Usually, a declining product has lost its distinctiveness because similar competing or superior products have been introduced.

During a product’s decline, spending on promotion efforts is usually reduced considerably.

Product Adoption Process

Product Adoption Process: The stages buyers go through in accepting a product

When an organization introduces a new product, consumers in the target market enter into and move through the adoption process at different rates.

Depending on the length of time it takes them to adopt a new product, consumers tend to fall into one of five major adopter categories:

Innovators: First adopters of new products

Early adopters: Careful choosers of new products

Early majority: Those adopting new products just before the average person

Late majority: Skeptics who adopt new products when they feel it is necessary

Laggards: The last adopters, who distrust new products

Branding

Brand: A name, term, design, symbol, or any other feature that identifies one marketer’s product as distinct from those of other marketers

Brand Name: The part of a brand that can be spoken

Brand Mark: The part of a brand not made up of words

Trademark: A legal designation of exclusive use of a brand

Trade Name: The full legal name of an organization

Value of Branding

Brands help buyers recognize specific products that meet their criteria for quality, reducing the time needed to identify and purchase products.

For many consumers, brand is a form of self-expression.

A brand indicates a quality level and image and reduces a buyer’s perceived risk of purchase.

Customers might receive a psychological reward from owning a brand that symbolizes status.

Brand Equity: The marketing and financial value associated with a brand’s strength in a market

Four major elements underlie brand equity:

Co-Branding: Using two or more brands on one product

Effective co-branding capitalizes on the trust and confidence customers have in the brands involved.

Packaging

A package can be a vital part of a product, making it:

More versatile

Safer

Easier to use

Packaging also conveys vital information about the product and is an opportunity to display interesting graphic design elements.

Like a brand name, a package can influence a customers’ attitudes toward a product and their decisions to purchase.

Can/does promote a product by communicating its features, uses, benefits, or image.

Packaging can be a major component of a marketing strategy.

The right type of package for a new product can help it gain market recognition very quickly.

When considering the strategic uses of packaging, marketers must analyze the cost of packaging and package changes.

Labeling

Labeling: Providing identifying, promotional, or other information on package labels

Labeling is very closely interrelated with packaging; information on the label may include:

Brand Name and Brand Mark

Registered Trademark Symbol

Package Size and Content

Product Features

Nutritional Information

Presence of Potential Allergens

Type and Style of the Product

Number of Servings

Care Instructions

Directions for Use

Safety Precautions

Manufacturer Name and Address

Expiration Dates

Seal of Approval

Several federal laws and regulations specify information that must be included on the labels of certain products:

Garments must be labeled with the name of the manufacturer, country of manufacture, fabric content, and cleaning instructions.

Labels on nonedible items, such as shampoos and detergents, must include both safety precautions and directions for use.

The Nutrition Labeling Act of 1990 requires the FDA to review food labeling and packaging for nutrition content, label format, ingredient labeling, food descriptions, and health messages.

The Federal Trade Commission requires that “all or virtually all” of a product’s components be made in the United States if the label says “Made in USA.”

Chapter XI: Developing and Managing Goods and Services

Managing Existing Products

To provide products that satisfy target markets and achieve the firm’s objectives, a marketer must develop, alter, and maintain an effective product mix.

An organization’s product mix may require adjustment for a variety of reasons:

Because customers’ attitudes and product preferences change over time, their desire for certain products may wane.

A company may need to alter its product mix for competitive reasons.

A marketer may delete a product from the mix because a competitor dominates the market.

A firm may introduce a new product or modify an existing one to compete more efficiently

Line Extension: Development of a product closely related to one or more products in the existing product line but designed specifically to meet somewhat different customer needs

Are less expensive and less risky than introducing a new product

May focus on a different market segment or attempt to increase sales within the same market segment by more precisely satisfying the needs of people in that segment

Success is enhanced if the parent brand has a high-quality brand image and if there is a good fit between the line extension and its parent.

Many of the so-called new products introduced each year are actually line extensions.

Product Modification: Change in one or more characteristics of a product

Differs from a line extension in that the original product does not remain in the product line

There are three major types of product modifications:

Quality Modifications: Changes relating to a product’s dependability and durability

Functional Modifications: Changes affecting a product’s versatility, effectiveness, convenience, or safety

Aesthetic Modifications: Changes to the sensory appeal of a product

Developing New Products

A firm develops new products as a means of enhancing its product mix and adding depth to a product line.

Developing and introducing new products is fairly expensive and risky.

Failing to introduce new products is also risky.

The term “new product” can have more than one meaning:

An innovative product that has never been sold by any organization

A modified product that existed previously

A product that a given firm has not marketed previously, although similar products are available from other companies

A product that is brought to one or more markets from another market

New-Product Development Process: A seven-phase process for introducing products

Idea Generation: Seeking product ideas that will help organizations to achieve objectives

New product ideas can come from several sources:

Internally through marketing managers, researchers, sales personnel, engineers, franchisees, or other organizational personnel

Externally through customers, competitors, advertising agencies, management consultants, and private research organizations

Increasingly, by bringing consumers into the product idea development process through online campaigns

Business Analysis: Evaluating the potential contribution of a product idea to the firm’s sales, costs, and profits (use a professional (outside) opinion!)

Product Development: Determining if producing a product is technically feasible and cost effective

To test its acceptability, the idea or concept is converted into a prototype, or working model.

A crucial question that arises during product development is how much quality to build into the product. The development phase of a new product is often a lengthy and expensive process.

As a result, only a relatively small number of products or product ideas are put into development.

Test Marketing: Introducing a product on a limited basis to measure the extent to which potential customers will actually buy it

Companies use test marketing to lessen the risk of product failure. (Note: it is expensive to do)

Commercialization: Deciding on full-scale manufacturing and marketing plans and preparing budgets

Early in this phase:

Marketing management analyzes the results of test marketing to find out what changes in the marketing mix are needed before introducing the product.

Marketers must make decisions about warranties, repairs, and replacement parts.

Products are not usually launched nationwide overnight but are introduced in stages through a process called a rollout, where a product is introduced in one geographic area or set of areas and gradually expands into adjacent ones

Gradual product introduction is desirable for several reasons:

It reduces the risks of introducing a new product.

A company cannot introduce a product nationwide overnight, because a system of wholesalers and retailers to distribute the product cannot be established so quickly.

If the product is successful from launch, the number of units needed to satisfy nationwide demand for it may be too large for the firm to produce in a short time.

General introduction allows for fine-tuning of the marketing mix to satisfy target customers.

Gradual product introduction can also create problems:

A gradual introduction allows competitors to observe what the firm is doing and monitor results just as the firm’s own marketers are doing.

As a product is introduced region by region, competitors may expand their marketing efforts to offset promotion of the new product.

Delay in launching a product can cause the firm to miss out on seizing market opportunities, creating competitive offerings, and forming cooperative relationships with channel members

Product Differentiation through Quality, Design, and Support Services

Product Differentiation: Creating and designing products so customers perceive them as different from competing products

Quality: Characteristics of a product that allow it to perform as expected in satisfying customer needs

Two Dimensions of Quality:

Level of Quality: The amount of quality a product processes

Consistency of Quality: The degree to which a product has the same level of quality over time

Product Design: How a product is conceived, planned, and produced

Components of design:

Styling: The physical appearance of a product

Functionality

Usefulness

Product Features: Specific design characteristics that allow a product to perform certain tasks

For a brand to have a sustainable competitive advantage, marketers must determine the product designs and features that customers desire.

Information from marketing research helps assess customers’ product design and feature preferences.

Customer Services: Human or mechanical efforts or activities that add value to a product

Product Positioning and Repositioning

Product Positioning: Creating and maintaining a certain concept of a product in customers’ minds

To simplify buying decisions and avoid a continuous reevaluation of numerous products, buyers tend to group, or “position,” products in their minds; marketers try to influence consumers’ concepts of product positions through advertising.

Marketers sometimes analyze product positions by developing perceptual maps to think like a customer.

Perceptual maps are created by questioning a sample of customers about their perceptions of products, brands, and organizations with respect to two or more dimensions.

Marketers can use several bases for product positioning.

A product’s position can be based on specific product attributes or features.

Other bases for product positioning include price, quality level, benefits provided by the product, and target market.

A brand’s market share and profitability may be strengthened by product repositioning of existing products.

Repositioning requires changes in perception and usually changes in product features.

Repositioning can be accomplished physically by changing the product, its price, or its distributors.

A marketer may reposition a product by aiming it at a different target market

Managing Services

Services are usually provided through the application of human and/or mechanical efforts that are directed at people or objects.

The importance of services in the U.S. economy led the United States to be known as the world’s first service economy.

The need for time-saving services has increased as today’s busy consumers often want to simplify or outsource tasks.

Changes in information technology have also influenced and expanded the services sector.

Client-Based Relationships: Interactions that result in satisfied customers who use a service repeatedly over time

Word-of-mouth communication is a key factor in creating and maintaining client-based relationships.

It is important for service providers to maintain customers/clients over the long-term by taking steps to:

Build trust

Demonstrate customer commitment

Satisfy customers

Customer Contact: The level of interaction between provider and customer needed to deliver the service

High-contact services generally involve actions directed toward people who must be present during production.

Employee satisfaction is one of the most important factors in providing high service quality to customers.

Organizing to Develop and Manage Products

Managing products is a complex task, and often the traditional functional form of an organization does not fit a company’s needs.

Alternatives to the traditional functional form of business organization include:

Product Manager: The person within an organization responsible for a product, a product line, or several distinct products that make up a group

Brand Manager: The person responsible for a single brand

Venture Team: A cross-functional group that creates entirely new products that may be aimed at new markets

Chapter XII: Pricing Concepts and Management

Price and Nonprice Competition

Price Competition: Emphasizing price as an issue and matching or beating competitors’ prices

To compete effectively on a price basis, a firm should be the low-cost seller of the product.

A seller competing on price must have the flexibility to change prices rapidly and aggressively in response to competitors’ actions.

If competitors quickly match or beat a company’s price cuts, a price war may ensue.

Non-Price Competition: Emphasizing factors other than price to distinguish a product from competing brands

Non-price factors include distinctive product quality, excellent customer service, effective promotion, packaging, or other unique features.

Nonprice competition is effective only under certain conditions:

Buyers must not only be able to perceive these distinguishing characteristics but also deem them important.

Development of Pricing Objectives

Pricing Objectives: Goals that describe what a firm wants to achieve through pricing

Marketers must ensure that pricing objectives are consistent with the firm’s marketing and overall objectives because pricing objectives influence decisions in many functional areas.

A marketer can use both short- and long-term pricing objectives and can employ one or multiple pricing objectives

Profit: may be stated in terms of either actual dollar amounts or a percentage of sales revenues.

Return on Investment: Pricing to attain a specified rate of return on the company’s investment is a profit-related pricing objective.

Market Share: A product’s sales in relation to total industry sales

Cash Flow: Some companies set prices so they can recover cash as quickly as possible.

Status Quo: such as maintaining a certain market share, meeting competitors’ prices, achieving price stability, or maintaining a favorable public image.

Product Quality: customers perceived to be of high quality are more likely to survive in a competitive marketplace.

Profit

Specific profit objectives may be stated in terms of either actual dollar amounts or a percentage of sales revenues.

Return on Investment

Pricing to attain a specified rate of return on the company’s investment is a profit-related pricing objective.

A return on investment (ROI) pricing objective generally requires some trial and error, as it is unusual for all data and inputs required to determine the necessary ROI to be available when first setting prices.

Market Share

A product’s sales in relation to total industry sales

Maintaining or increasing market share need not depend on growth in industry sales:

An organization can increase market share even if industry sales are flat or decreasing.

Sales volume can increase while market share decreases if the overall market grows.

Cash Flow

Some companies set prices so they can recover cash as quickly as possible.

Choosing this pricing objective may have the support of a marketing manager if he or she anticipates a short product life cycle.

Status Quo

Status quo objectives can focus on several dimensions, such as maintaining a certain market share, meeting competitors’ prices, achieving price stability, or maintaining a favorable public image.

Can reduce a firm’s risks by helping to stabilize demand for its products

Can increase risk of minimizing pricing as a competitive tool, which could lead to a climate of non-price competition

Product Quality

Attaining a high level of product quality is generally more expensive for the firm, as the costs of materials, research, and development may be greater.

Products and brands that customers perceive to be of high quality are more likely to survive in a competitive marketplace.

Assessment of the Target Market’s Evaluation of Price

The importance of price varies depending on the:

Type of product

Type of target market

Purchase situation

Value combines a product’s price with quality attributes, which customers use to differentiate among competing brands.

Consumers may perceive relatively expensive products to have great value if the products have desirable features or characteristics.

Consumers are generally willing to pay a higher price for products that offer convenience and save time.

Evaluation of Competitors’ Prices

Identifying competitors’ prices should be a regular part of marketing research.

Regardless of actual costs, a firm does not want to sell its product:

At a price that is significantly above competitors’ prices, because the products may not sell as well

At a price that is significantly below competitors’ prices, because customers may believe the product is of low quality

In some instances, an organization’s prices are designed to be slightly above competitors’ prices to lend an exclusive image and to signal product quality to consumers.

Selection of a Basis for Pricing

The three major dimensions on which prices can be based are cost, demand, and competition.

An organization generally considers at least two, or perhaps all three, dimensions.

Setting appropriate prices can be a difficult balance for firms:

A high price may reduce demand for the product.

A low price will hurt profit margins and may instill in customers a perception that the product is of low quality.

Firms must weigh many different factors when setting prices, including:

Costs, Competition, Consumer Buying Behavior and Price Sensitivity, Manufacturing Capacity, Product Life Cycles

Cost-Based Pricing

Cost-Based Pricing: Adding a dollar amount or percentage to the cost of the product

Does not necessarily take into account the economic aspects of supply and demand, nor must it relate to just one pricing strategy or pricing objective

Cost-Plus Pricing – Adding a specified dollar amount or percentage to the seller’s cost

Markup Pricing: Adding to the cost of the product a predetermined percentage of that cost

Can be stated as a percentage of cost of making the product or as a percentage of selling price:

Selection of a Pricing Strategy

Demand-Based Pricing

Demand-Based Pricing: Pricing based on the level of demand for the product

Customers pay a higher price when demand for the product is strong and a lower price when demand is weak.

Marketers must be able to estimate the quantity of a product consumers will demand at different times and how demand will be affected by changes in the price; the marketer then chooses the price that generates the highest total revenue.

Appropriate for industries in which companies have a fixed amount of available resources that are perishable

Effectiveness depends on the marketer’s ability to estimate demand accurately

Competition-Based Pricing

Competition-Based Pricing: Pricing influenced primarily by competitors’ prices

A common method among producers of relatively homogeneous products, particularly when the target market considers price to be an important purchase consideration

Firms may choose to set prices below competitors’ or at the same level

New-Product Pricing

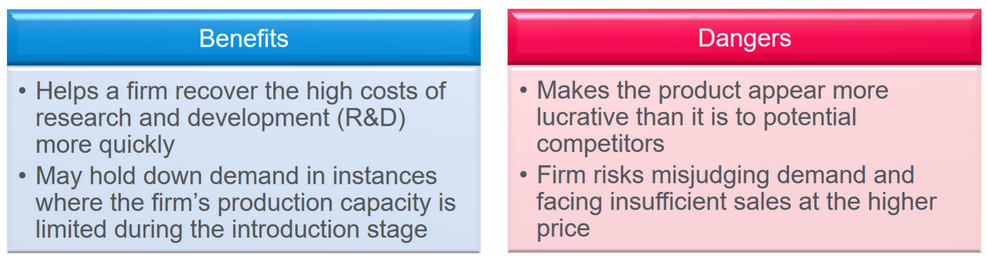

Price Skimming: Charging the highest possible price that buyers who most desire the product will pay

Some consumers are willing to pay a high price for an innovative product, either because of its novelty or because of the prestige or status that ownership confers.

Provides the most flexible introductory base price

Penetration Pricing: Setting prices below those of competing brands to penetrate a market and gain a significant market share quickly

Differential Pricing

Differential Pricing: Charging different prices to different buyers for the same quality and quantity of product

For differential pricing to be effective, the market must consist of multiple segments with different price sensitivities.

Caution should be used to avoid confusing or antagonizing customers.

Psychological Pricing

Psychological Pricing: Strategies that encourage purchases based on consumers’ emotional responses, rather than on economically rational ones

Used primarily for consumer products rather than business products

Odd-Number Pricing: The strategy of setting prices using odd numbers that are slightly below whole-dollar amounts

This strategy is not limited to low-price items.

Odd-number pricing has been the subject of various psychological studies, but the results have been inconclusive.

Reference Pricing: Pricing a product at a moderate level and positioning it next to a more expensive model or brand

Used in the hope that the customer will use the higher price as a reference price (i.e., a comparison price)

Because of the comparison, the customer is expected to view the moderate price more favorably than he or she would if the product were considered in isolation.

Bundle Pricing: Packaging together two or more complementary products and selling them for a single price

The single price generally is markedly less than the sum of the prices of the individual products.

Everyday Low Prices (EDLPs): Setting a low price for products on a consistent basis

EDLPs are set low enough to make customers feel confident they are receiving a good deal.

A major issue with this approach is that, in some instances, customers believe that EDLPs are a marketing gimmick and not truly the good deal that they proclaim.

Customary Pricing: Pricing on the basis of tradition

Product-Line Pricing

Product-Line Pricing: Establishing and adjusting prices of multiple products within a product line

Captive Pricing: Pricing the basic product in a product line low, but pricing related items at a higher level

Premium Pricing: Pricing the highest-quality or most versatile products higher than other models in the product line

Price Lining: The strategy of selling goods only at certain predetermined prices that reflect definite price breaks

Promotional Pricing

Price Leaders: Products priced below the usual markup, near cost, or below cost

Used in supermarkets and restaurants to attract customers by offering them especially low prices on a few items, with the expectation that they will purchase other items as well

Management expects that sales of regularly priced products will more than offset the reduced revenues from the price leaders.

Special-Event Pricing: Advertised sales or price cutting linked to a holiday, season, or event

Used to increase sales volume

Special sales events may be designed to generate necessary operating capital

Pricing for Business Markets

Setting prices for business products can be quite different from setting prices for consumer products.

Factors include: the size of purchases, transportation considerations, and geographic issues.

Geographic Pricing

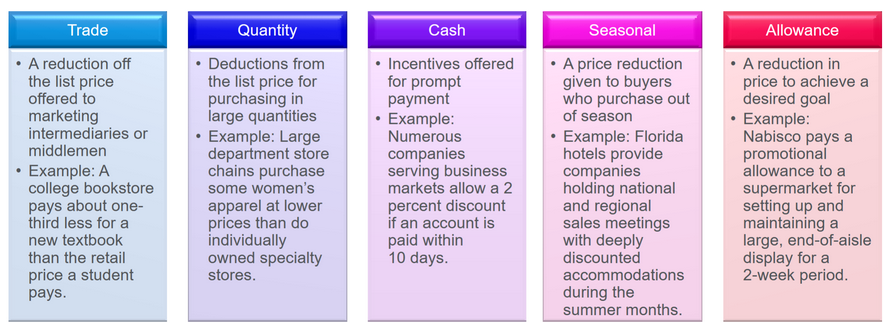

Geographic Pricing: Reductions for transportation and other costs related to the physical distance between buyer and seller

F.O.B. Origin: The product price does not include freight charges

F.O.B. Destination: The product price includes freight charges

Discounting

Discount: A deduction from the price of an item