Chapter 6 and 7

· Price Elasticity of Demand

o Consumers responsiveness to a price change is measured by a product's price elasticity of demand

§ For some products such as restaurant meals consumers are highly responsive to price changes. That is, modest price changes often cause very large changes in the quantity purchased. The demand for such products is relatively elastic or simply elastic

§ For other products such as toothpaste consumers pay much less attention to price changes. Substantial price changes often cause only small changes in the amount purchased. The demand for such products is relatively inelastic or simply inelastic

§ Price Elasticity of Demand: The ratio of the percentage change in quantity demanded of a product or resource to the percentage change in its price; A measure of the responsiveness of buyers to a change in the price of a product or resource

o The Price-Elasticity Coefficient and Formula

§ Economists measure the degree to which demand is price elastic or inelastic with the coefficient Ed defined as Ed = %change in quantity demanded of product X divided by %change in price of product X

§ The percentage changes in the equation are calculated by dividing the change in quantity demanded by the original quantity demanded and by dividing the change in price by the original price

§ TO AVOID COMPLICATIONS ALL COMPUTATIONS WILL USE THE MIDPOINT FORMULA FOR CALCULATING THE % CHANGE IN QD AND THE % CHANGE IN PRICE. THIS USES AVERAGES WHICH, WHILE NOT PERFECT, GIVE US A “GOOD ENOUGH” ESTIMATE OF ELASTICTY

· Midpoint Formula: Averages the two prices and two quantities given to you

· Ed = (change in quantity divided by (sum of two quanities/2)) ÷ (change in price divided by (sum of two prices/2))

§ Elimination of the Minus Sign: Always use the absolute value when calculating elasticity

o Interpretations of Ed

§ Elastic Demand: The % change in price results in a larger % change in demand.

· In short: Ed > 1

§ Inelastic Demand: The % change in prince results in a smaller % change in demand

· In short: Ed < 1

§ Unit Elasticity: The % change in price and demand are equal

· In short: Ed = 1

§ Perfectly Inelastic: Ed = 0

· In short: No matter the price, demand remains the same

· Demand curve is a straight vertical line

§ Perfectly Elastic: Ed = ∞

· In short: Qd is essentially infinite at a given price point

· Demand curve is a straight horizontal line

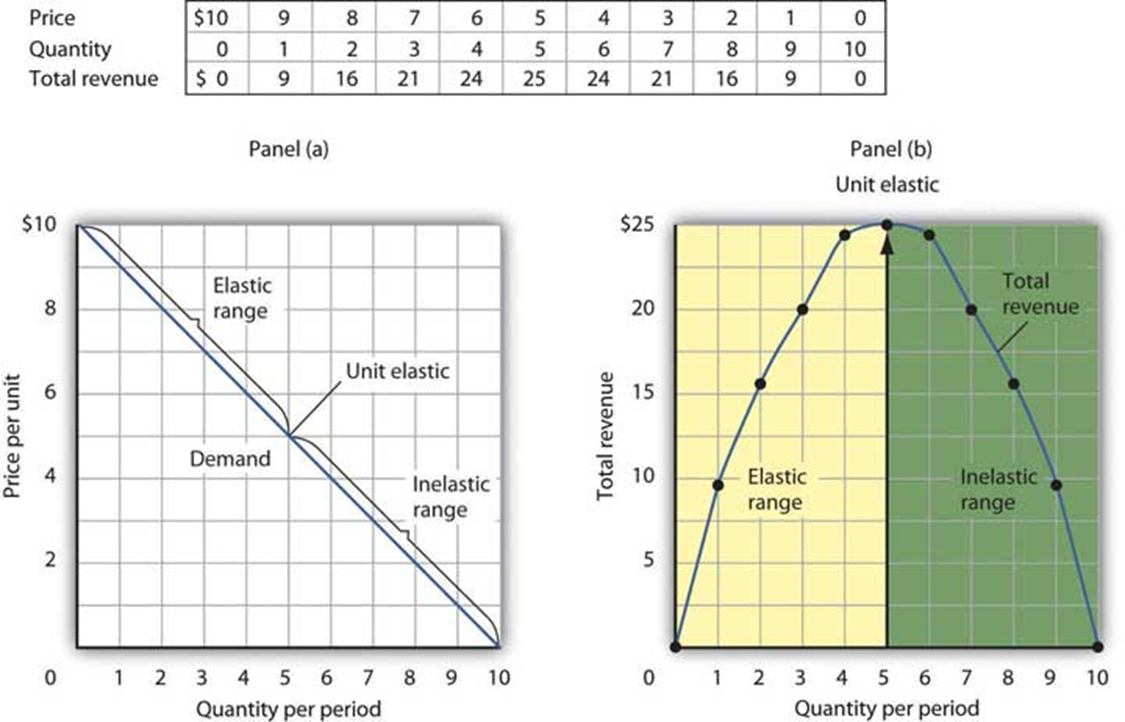

· Total-Revenue Test

o Firms what to know the effect of price changes on total revenue and thus on profits

o Total Revenue (TR) is calculated by multiplying the product price by quantity sold

§ TR = P x Q

o Total-revenue test: Test to determine elasticity of demand. Is elastic if total revenue moves in the opposite direction from a price change; It is inelastic when it moves in the same direction as a price change; And it is of unitary elasticity when it does not change when price changes

o Price Elasticity Along a Linear Demand Curve

§ It is important to understand that elasticity typically varies along any given demand curve

· Determinants of Price Elasticity of Demand

o Substitutability: generally the more substitute goods that are available the greater price elasticity of demand. Various candy bar brands are generally substitutable for one another making the demand for one brand of a candy bar say Snickers highly elastic. Toward the other extreme the demand for tooth repair is quite inelastic because there simply are no close substitutes when that procedure is required.

o Proportion of income: other things equal, the higher the price of a good relative to consumers incomes, the greater the price elasticity of demand. A 10% increase in the price of low priced pencils or chewing gum amounts to a few more pennies spent from a consumer's income, and quantity demanded will probably decline only slightly. Thus, price elasticity for low price items tends to be low. But a 10% increase in the price of a relatively high-priced product like a car or house means additional expenditures of perhaps $3000 or $30,000 respectively. These price increases are significant fractions of most families annual incomes and quantities demanded will likely diminish significantly. The price elasticities for such items tends to be high.

o Luxuries versus necessities: in general, price elasticity of demand is higher for luxury goods than it is for necessities. Electricity is generally regarded as a necessity; It is difficult to get along without it. A price increase will not significantly reduce the amount of lighting and power used in a household. In contrast, vacation travel in jewelry or luxuries, which, by definition, can easily be foregone

o Time: generally, product demand is more elastic over longer periods of time period consumers often need time to adjust to price changes. For example, when the price of a product rises, consumers need time to find and experiment with other products. Consumers may not immediately reduce their purchases very much when the price of beef rises by 10%, but in time they may shift to chicken, pork, or fish

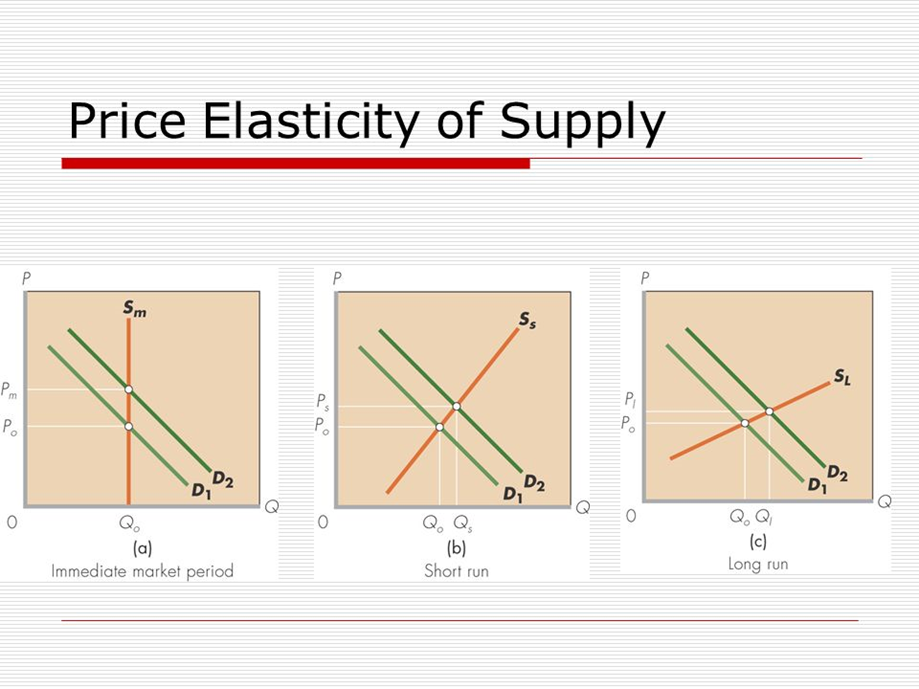

· Price Elasticity of Supply

o Price elasticity also applies to supply. If the quantity supplied by producers is relatively responsive to price changes, supply is elastic. If it is relatively insensitive to price changes, supply is inelastic.

§ Es = %change in quantity supplied in product X divided by %change in price of product X

§ As with demand the averages, or midpoints, of the before and after quantities supplied and the before and after prices are used as reference points for the percentage changes.

o Price Elasticity of Supply: the ratio of the percentage change in quantity supplied of a product or resource to the percentage change in its price; A measure of the responsiveness of producers to a change in the price of a product or resource

§ The degree of price elasticity of supply depends on how quickly and easily producers can shift resources between alternative uses. The more easily and rapidly producers can shift resources between alternative uses, the greater the price elasticity of supply.

o In analyzing the impact of time on elasticity, economists distinguish among the immediate market period, the short run, and the long run.

o The Immediate Market Period

§ The immediate market period is the length of time over which producers are unable to respond to a change in price with a change in quantity supplied

· The supply curve will be perfectly inelastic (vertical)

· It is important to note that not all products’ supply curves are perfectly inelastic immediately after a price change. If a product is not perishable and the price rises, producers may be able to increase quantity supplied by drawing from inventories of unsold, stored goods if they have any

o The Short Run

§ The short run in microeconomics is a period of time too short to change plant capacity but long enough to use the fixed sized plant more intensively or less intensively.

o The Long Run

§ The long run in microeconomics is a time period long enough for firms to adjust their plant sizes and for new firms to enter or existing firms to leave the industry

· Cross Elasticity and Income Elasticity of Demand

o Cross Elasticity of Demand

§ Measures the sensitivity of consumer purchases of one product (X) to a change in the price of some other product (Y)

§ Exy = %change in quantity demanded of product X divided by %change in price of product y

§ Cross elasticity allows us to quantify and more fully understand substitute and complementary goods.

§ Important: The coefficient of cross elasticity of demand can be either positive or negative

o Substitute Goods

§ If cross elasticity of demand is positive, meaning that sales of X move in the same direction as a change in the price of Y, then X&Y are substitute goods. An example is Evian Water X and Dasani Water Y.

§ An increase in the price of Evian causes consumers to buy more Dasani, resulting in a positive cross elasticity. The larger the positive cross elasticity coefficient, the greater is the substitutability between the two products

o Complementary Goods

§ When cross elasticity is negative, we know that X&Y “go together”; an increase in the price of one decreases the demand for the other. So the two are complementary goods.

§ For example, a decrease in the price of digital cameras will increase the number of memory sticks purchased. The larger the negative cross elasticity coefficient, the greater is the complementarity between the two goods.

o Independent Goods

§ A 0 or near 0 cross elasticity suggests that the two products are unrelated or independent goods. An example is walnuts and plums: we do not expect a change in the price of walnuts to have any effect on purchases of plums, and vice versa.

o Income Elasticity of Demand

§ Measures the degree to which consumers respond to a change in their incomes by buying more or less of a particular good. The coefficient of income elasticity of demand Ei is determined with the formula:

· Ei =%change in demand divided by %change in income

o Normal Goods

§ For most goods, the income elasticity coefficient Ei is positive, meaning that more of those goods are demanded as incomes rise. Such goods are called normal or superior goods.

§ But the value of Ei varies greatly among normal goods. For example, income elasticity of demand for cars is much higher than the income elasticity for produce

o Inferior Goods

§ A negative income elasticity coefficient designates an inferior good. Cabbage, long distance bus tickets, and used clothing are likely inferior goods. Consumers decrease their purchases of inferior goods as incomes rise.

· Law of Diminishing Marginal Utility

o The principle that as a consumer increases the consumption of a good or service, the marginal utility obtained from each additional unit of the good or service decreases

§ Ex. Getting a car will give a huge amount of utility but any additional utils for a second or third car will be very small in comparison for most people

o Three Characteristics of Utility

§ “Utility” and “Usefulness” are not synonymous. A Picaso painting will provide an art connoisseur lots of utility, but it is functionally useless

§ Utility is subjective (Not everyone needs a Ford F-150 for instance)

§ Utility is difficult to quantify (But for the sake of learning we’ll assume it can be measured in utils)

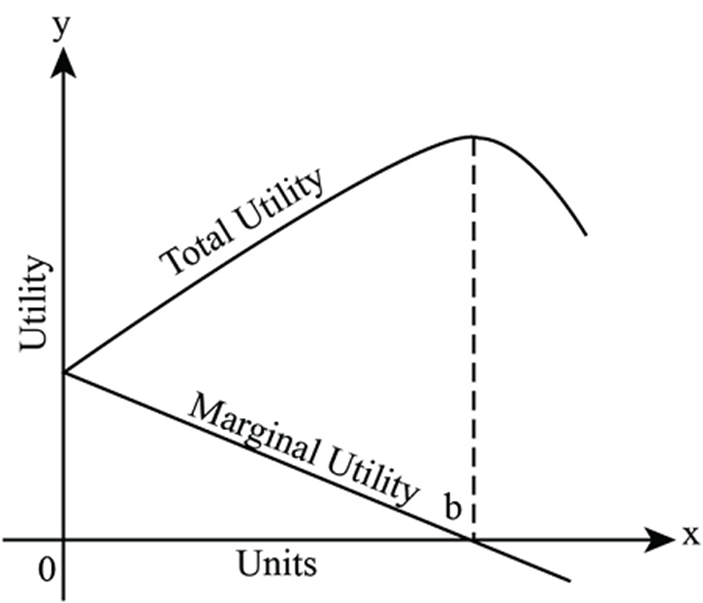

o Total Utility and Marginal Utility

§ Total Utility is the total amount of satisfaction or pleasure a person derives from consuming some specific quantity of a good or service

§ Marginal Utility is the extra satisfaction a consumer gains from an additional unit of that product

(Notice how Total Utility peaks and starts to decline right as Marginal Utility crosses the X-Axis

o Marginal Utility and Demand

§ The law of diminishing marginal utility explains why the demand curve for a given product slopes downward. If each additional unit of a good yields smaller and smaller amounts of marginal utility then consumers will only buy additional units of a product if the price falls

· Theory of Consumer Behavior

o Diminishing marginal utility also explains how consumers allocate their incomes among the many goods and services available for purchase

o Consumer Choice and the Budget Constraint

§ (For simplicity we will make the following assumptions about consumers)

· Rational Behavior: consumers try to use their income to derive the greatest amount of utility from it. Consumers want to maximize their total utility.

· Preferences: each consumer has clear cut preferences for certain goods and services that are available in the market. Buyers also have a good idea of how much marginal utility they get from each unit of the product they might purchase.

· Budget Constraint: at any point in time the consumer has a fixed limited amount of income

· Prices: goods are scarce relative to the demand for them, so every good carries a price tag. We also assume that the price of each good is unaffected by the amount purchased by any one particular person. Consumers must compromise, they must choose the most personally satisfying mix of goods and services

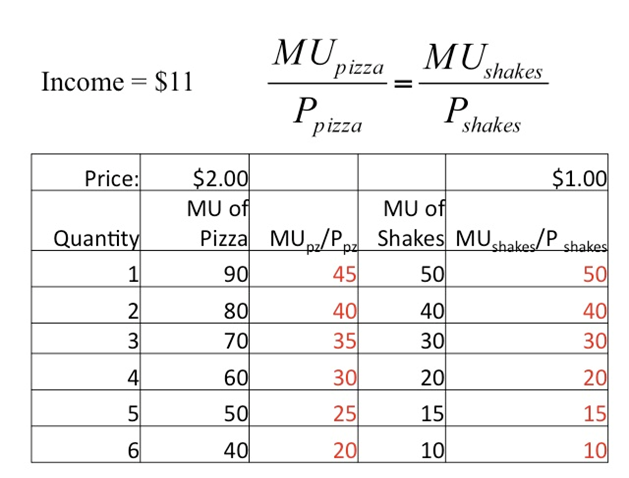

o Utility Maximizing Rule

§ The principle that to obtain the greatest total utility, a consumer should allocate income so that the last dollar spent on each good or service yields the same marginal utility (MU). For two goods, X and Y, with prices Px and Py Total Utility (TU) will be maximized when (MUx / Px) = (MUy / Py)

· This “balance” is called consumer equilibrium

§ Take note that the equation above is literally measuring Marginal Utility per Dollar

Utility Maximizing Rule: = (MU of product A divided price by A) = (MU of product B divided by price by B)