Chapter 8: The Costs of Production

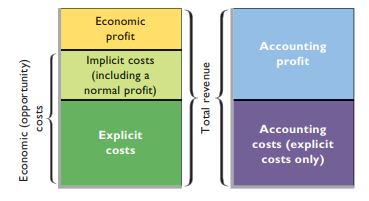

- Opportunity cost - Value of resource in best alternative use

- Explicit costs - Monetary payments for use of resources owned by others

- Implicit costs - Opportunity costs of using self-owned/self-employed resources; monetary payments that resources could’ve earned in best alternative use

- Accounting profit ignores implicit costs + overstates economic success

- Normal profit - Cost of doing business

- Economic costs = Explicit costs + implicit costs

- Economic profit = Total revenue - economic costs

- Short run - Period too brief for firm to alter plant capacity, but long enough to change resources like hourly labor, raw materials, etc.

- Long run - Period long enough to change quantities of all resources it employs, including plant capacity

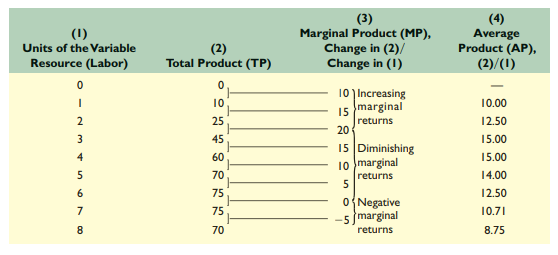

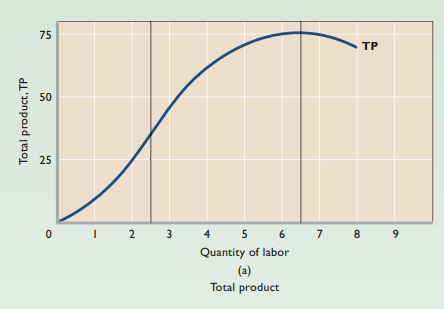

- Total product (TP) - Total output of good/service produced

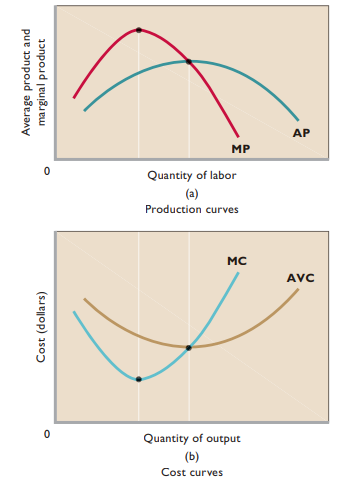

- Marginal product (MP) - Extra output of product with adding unit of variable resource

- Slope of total product curve

- Average product (AP) - Output per unit of labor input

- Law of diminishing returns - Successive units of variable resource added to fixed resource → Marginal product for each additional unit of variable resource will decline

- Marginal product greater than average product → Average product increasing

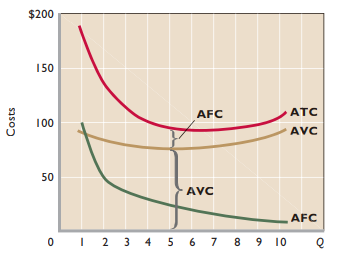

- Fixed costs - Aren’t affected by changes in output

- Must be paid even if output is zero

- Variable costs - Costs that change w/ level of output

- Total cost = Total fixed costs + total variable costs

- Average fixed cost (AFC) = Total fixed cost / output

- Average variable cost (AVC) = Total variable cost / output

- Average total cost (ATC) = Total cost / output

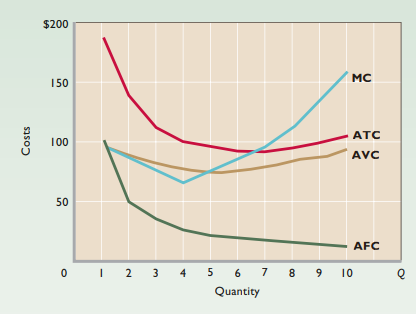

- Marginal cost - Extra cost of producing one more unit of output

- Graph’s shape is consequence of law of diminishing returns

- Marginal cost less than average total cost → ATC falls

- Changes in resource prices or technology → Costs change and cost curves shift

- Discovery of new technology → Productivity of all inputs increase

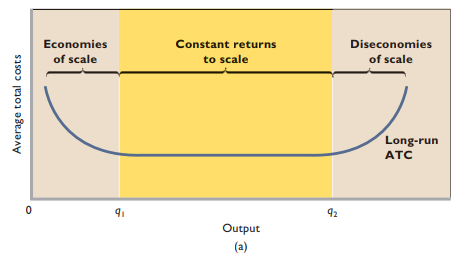

- Economies of scale - Down-sloping part of long run ATC curve; as plant size increases, a number of factors will for a time lead to lower average costs of production

- Labor specialization - Increased specialization in the use of labor becomes more achievable as a plant increases in size

- Managerial specialization - Large-scale production also means better use of, and greater specialization in, management

- Efficient capital - Large-scale producers have a high volume of production, resulting in effective use of equipment

- Diseconomies of scale - Difficulty of efficiently controlling and coordinating a firm’s operations as it becomes a large-scale producer

- Expansion of management hierarchy → Communication + cooperation problems

- Constant returns to scale - Long run average cost doesn’t change

- Minimum efficient scale (MES) - Lowest level of output at which a firm can minimize long-run average costs

- Natural monopoly - Average total cost is minimized when only one firm produces the particular good or service