Lecture 10

IV Estimation in Simple Regression

Regression Model:

yt = \alpha + \beta xt + u_tAssumption: {Cov}(xt, ut) ≠ 0

Existence of Instrument: Variable such that:

{Cov}(xt, zt) ≠ 0 (Relevance)

{Cov}(zt, ut) = 0 (Validity)

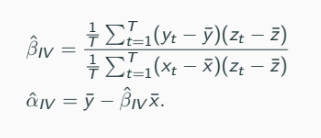

IV Estimators:

Properties of the IV Estimator

Consistent Estimators (TS1 - TS3):

is a consistent estimator of

is a consistent estimator of

Statistical Inference Result:

Conditional Variance:

If (Homoskedasticity),

In this case,

Other Issues Related to Stochastic Regressors

Model Specification:

Regression Model:

Assumptions Violations:

(xt, ut) is iid

If (Exogeneity Violation):

OLS Estimator fails.

Conditional Heteroskedasticity

If , the variance depends on .

Implications for OLS Estimator:

Unbiased:

Error:

Therefore,

Variance of the OLS Estimator:

When no conditional heteroskedasticity:

Estimated by instead of

Statistical Inference under Heteroskedasticity

Use of Robust Standard Errors:

Remedies for heteroskedasticity: use White’s or HAC Standard Errors.

Hypothesis Testing and Confidence Intervals are then valid.

Conditional Autocorrelation

Definition:

Correlation of Errors:

Implies OLS Estimator is unbiased but requires a careful derivation for the standard error.

Basics on Time Series

Importance in Economics:

Key Models: - Autocorrelation in linear regression framework must be understood.

Autocovariance and Autocorrelation

Definitions:

Autocovariance:

Autocorrelation:

Stationary Time Series

Definitions of Stationarity:

Strictly Stationary: Joint distributions invariant under time shifts.

Weakly Stationary: Mean, Variance constant, Autocovariance depends only on lag.

Autocovariance Function:

Examples of Time Series Models

White Noise:

Moving Average Processes (MA(1)):

AR(p) Models

Model Specification:

AR(1) Model and Covariance Stationary

Condition for Stationarity: |\phi1| < 1 \Rightarrow Cov(Xt) \text{ stationary}

If , series is generally not stationary, exemplified by random walk behaviour.