The Factors of Production - chapter 16

16.1. The Factors of Production: Land, Labour, and Capital

- Factors of production: the ingredients that go into making a good or service

- Can be divided into 3 major categories: land, capital, and labour

- Capital: manufactured goods that are used to produce new goods

- Factors of production are rented, bought, and sold in markets, at prices and in quantities that are determined by supply and demand

- Firms choose to produce using the combination of factors that will maximize profit

16.2. Demand for Labour

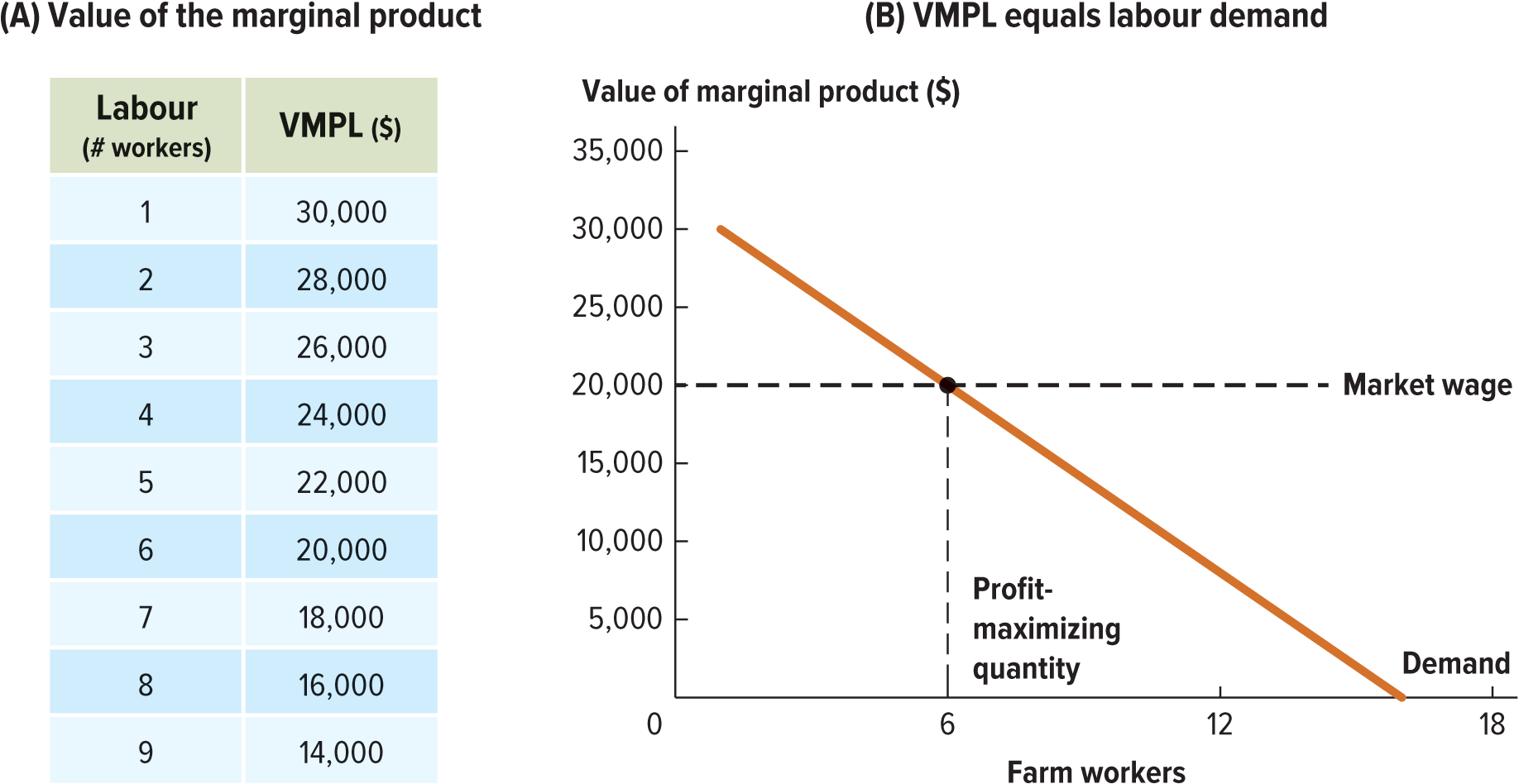

- The demand for factors of production is determined by their contribution to the value of a firm’s output

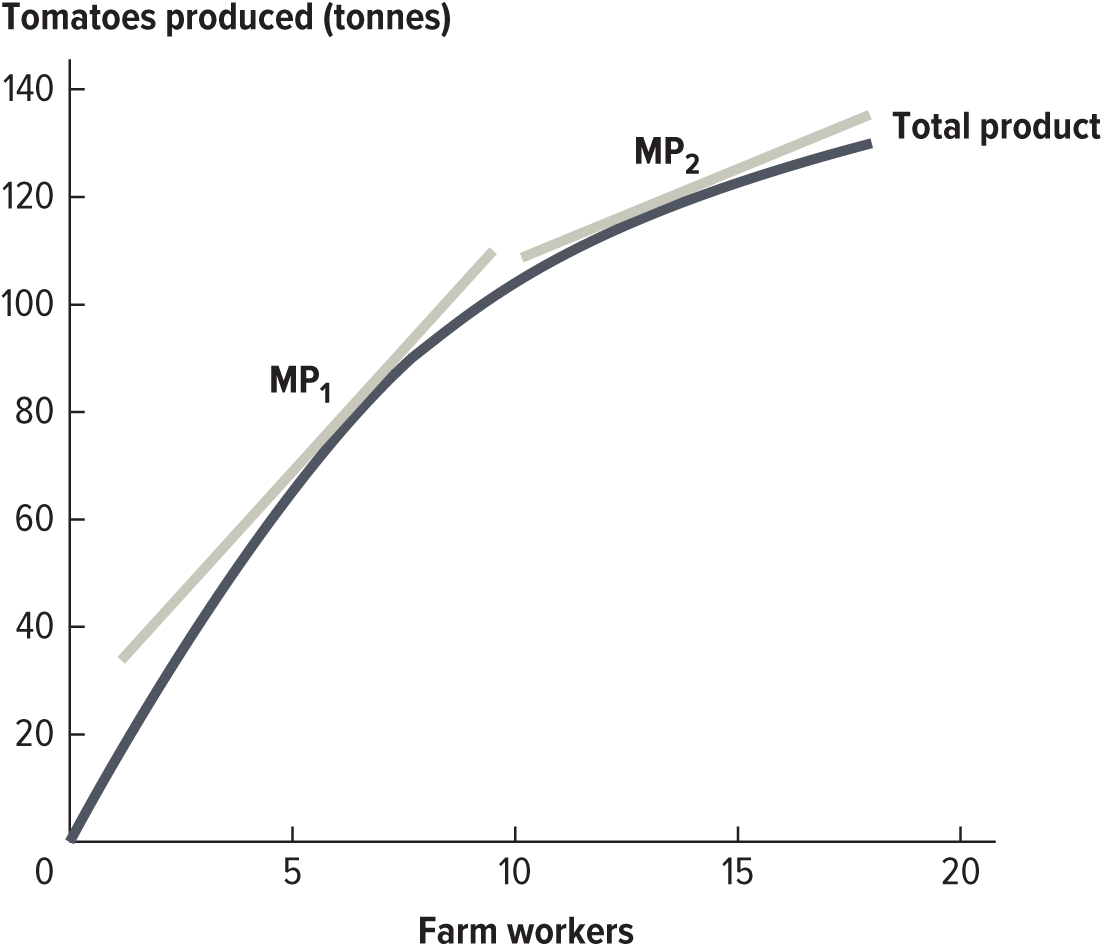

- We can use the marginal product of labour (or land or capital) to measure the increase in output gained by using one more unit of production

- value of the marginal product: the marginal revenue generated by an additional unit of input times the price of the output

- Firms will hire workers up to the point where the wage equals the value of the marginal product of labour (MR = MC)

- If we graph the value of the marginal product against the number of workers, we get a downward-sloping relationship that is the same as the demand curve for labour

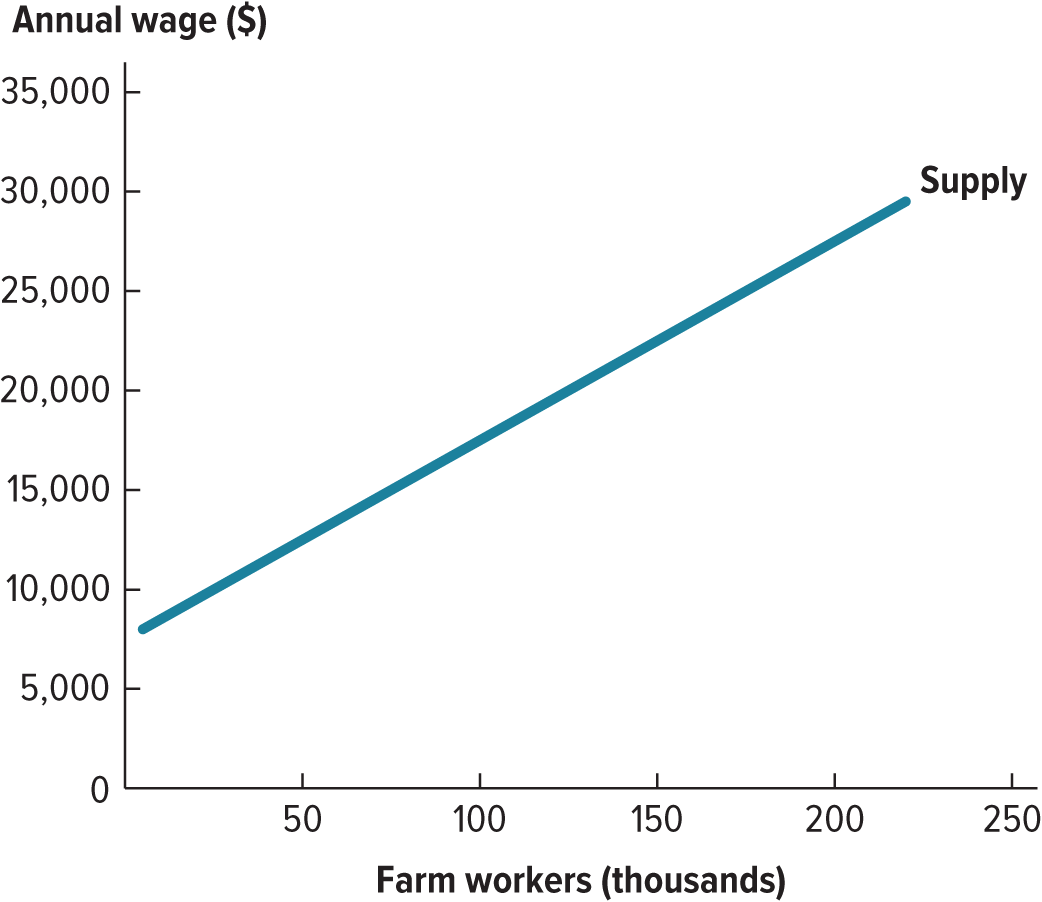

16.3. Supply of Labour

- The supply of a factor of production is driven by the opportunity cost of using that factor in a given market

- The opportunity cost of supplying labour in a particularly labour market is the time you would otherwise have spent on leisure or working at another job

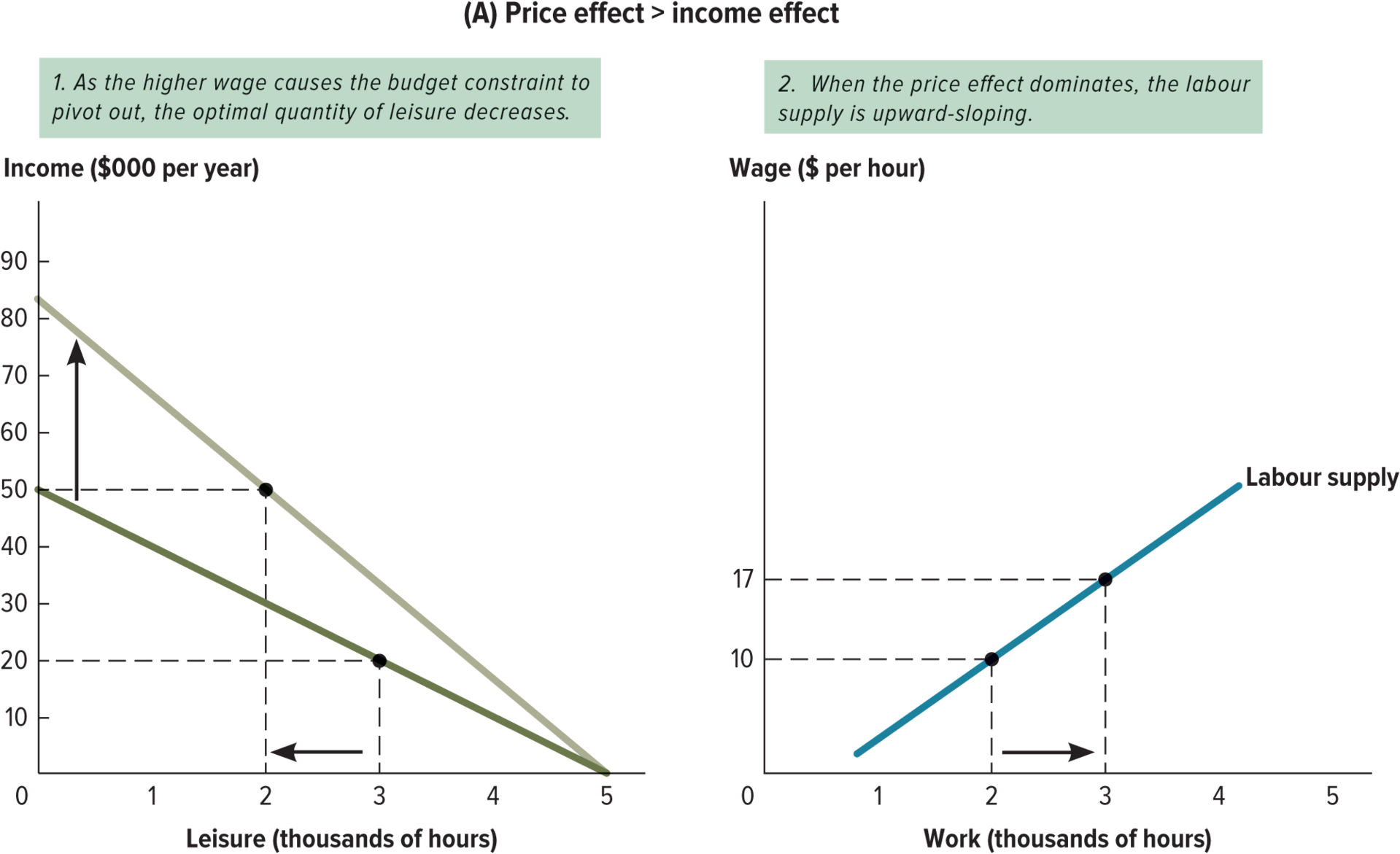

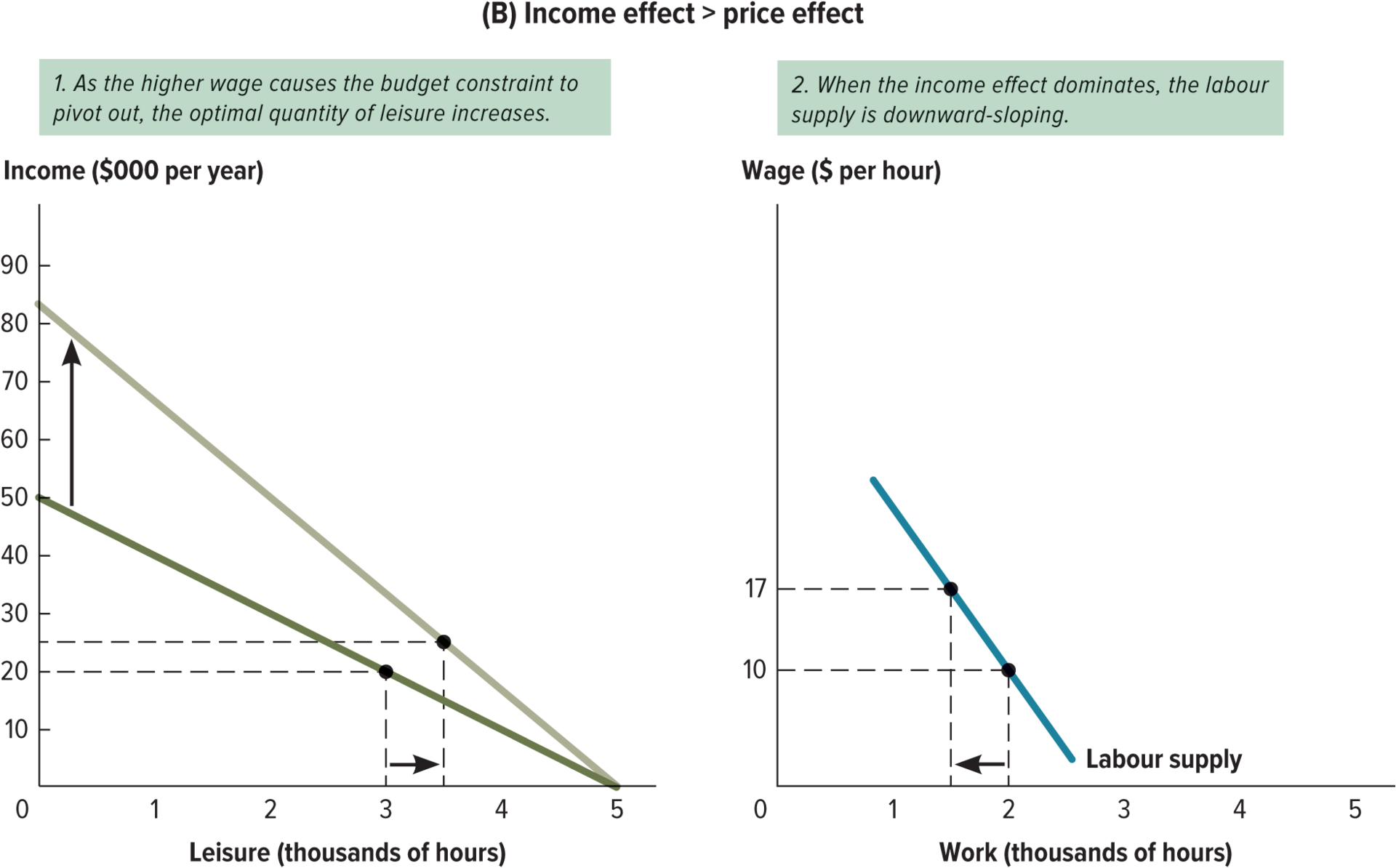

- An increase in wages has two effects on the labour supply, a price effect and an income effect

- The price effect causes the quantity of labour supplied to increase, all else held equal

- The income effect decreases the labour supply, as workers demand more leisure time

- In general, the price effect outweighs the income effect, which means that the labour supply curve slopes upward

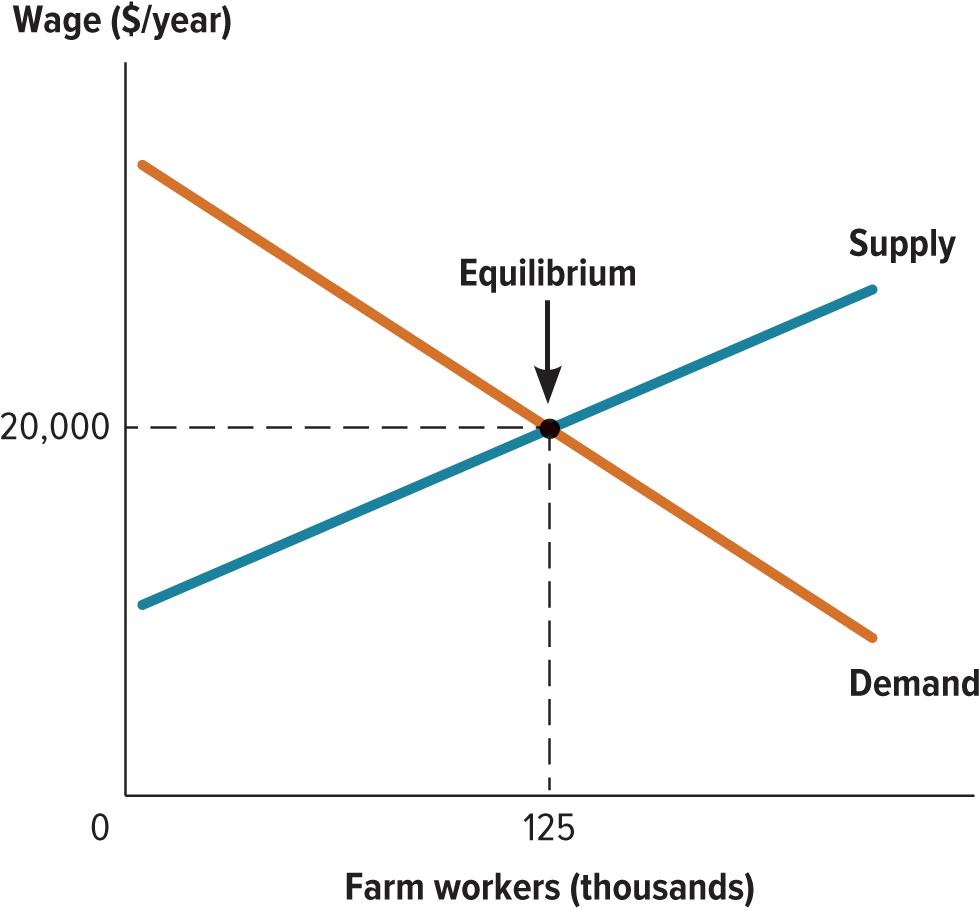

16.4. Reaching Equilibrium

- Factor markets reach equilibrium at the point where

- the demand curve intersects the supply curve

- The quantity demanded equals the quantity supplied at a given price or wage

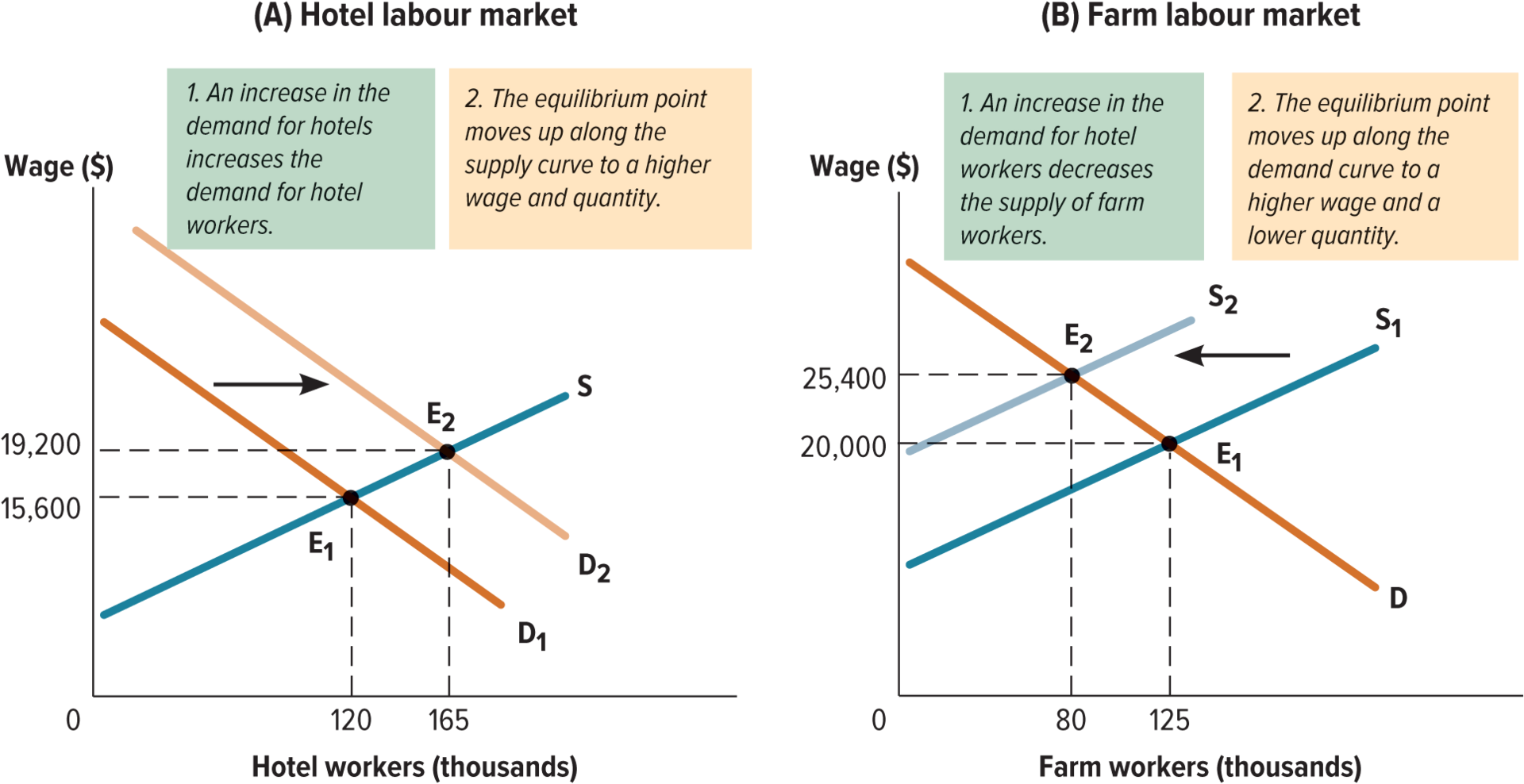

16.5. Shifts in Supply and Demand

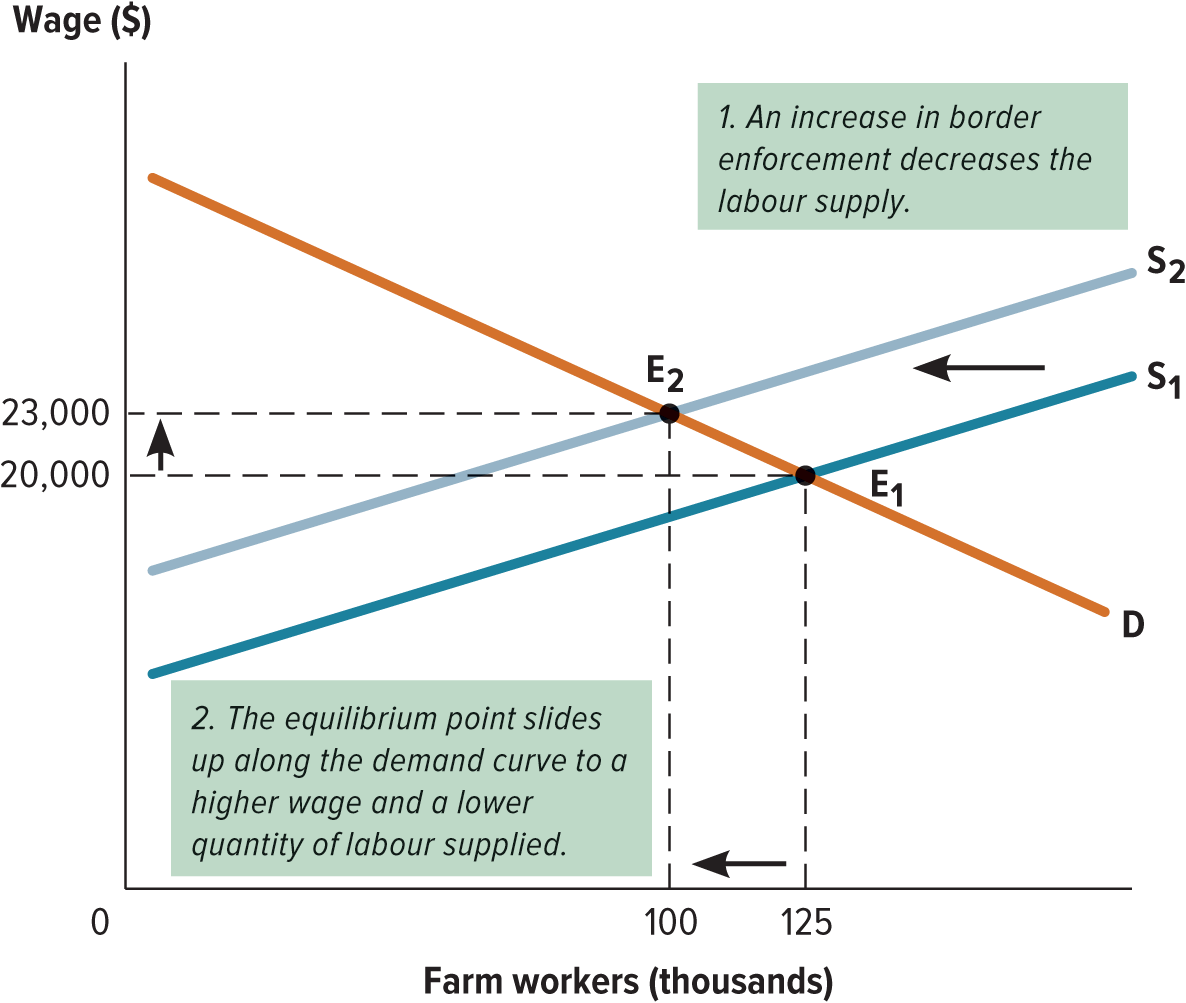

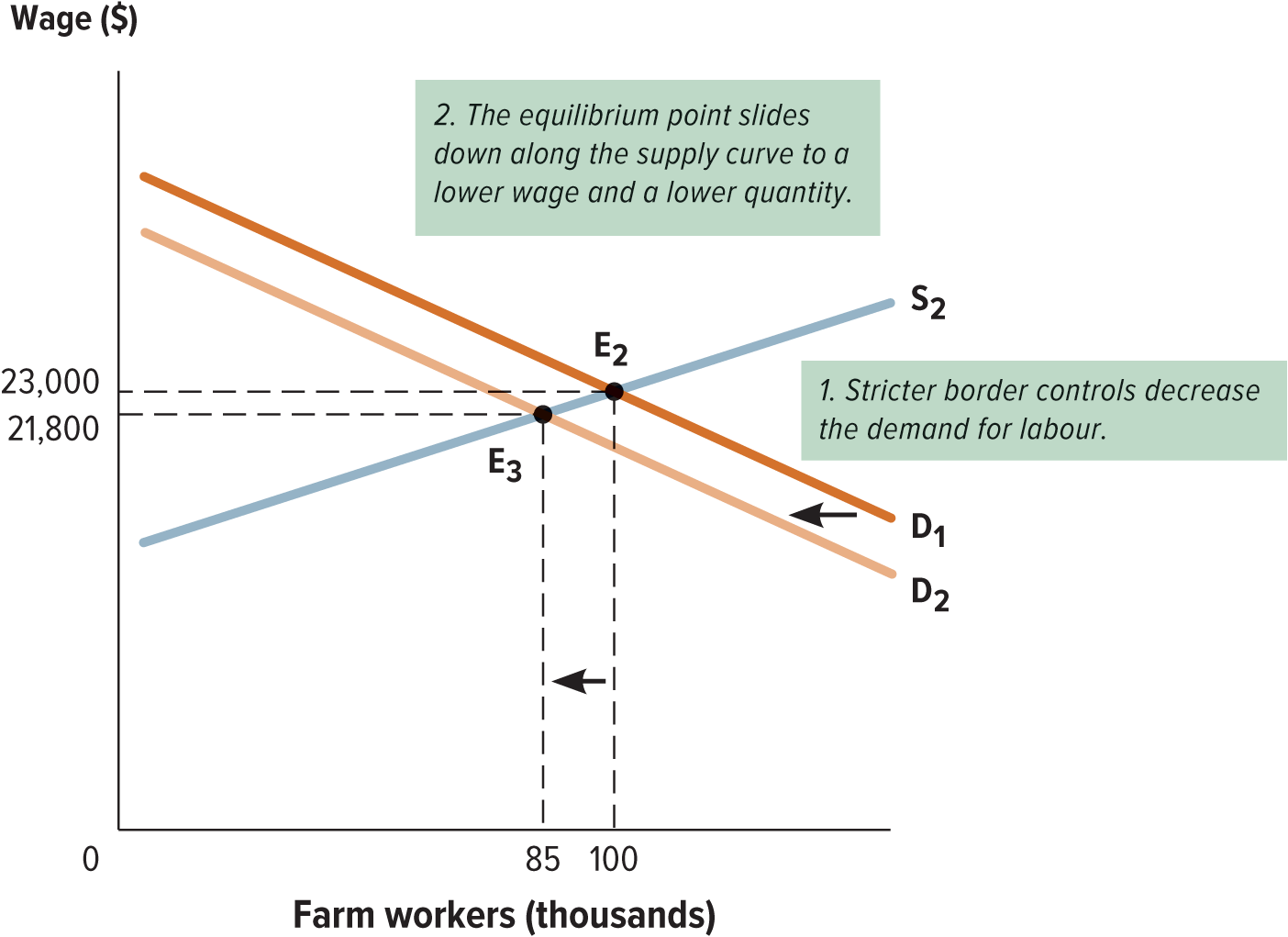

- If the underlying determinants of supply or demand change, the equilibrium point can shift

- The determinants of labour demand include anything that affects the value of the marginal product, including the supply of other factors, changes in technology, and output prices

- The determinants of labour supply include culture, population, and the availability of other opportunities

16.6. Human Capital

- human capital: the set of skills, knowledge, experience, and talent that determine the productivity of workers

- Workers differ from one another because they have different amounts of and types of human capital to offer

- Allow them to be more or less productive than others at different tasks

- Some types of human capital makke workers more productive at a wide range of jobs; others relate to very specific tasks

- Differences in human capital are a key determinant of wages, and therefore of differences in people’s incomes

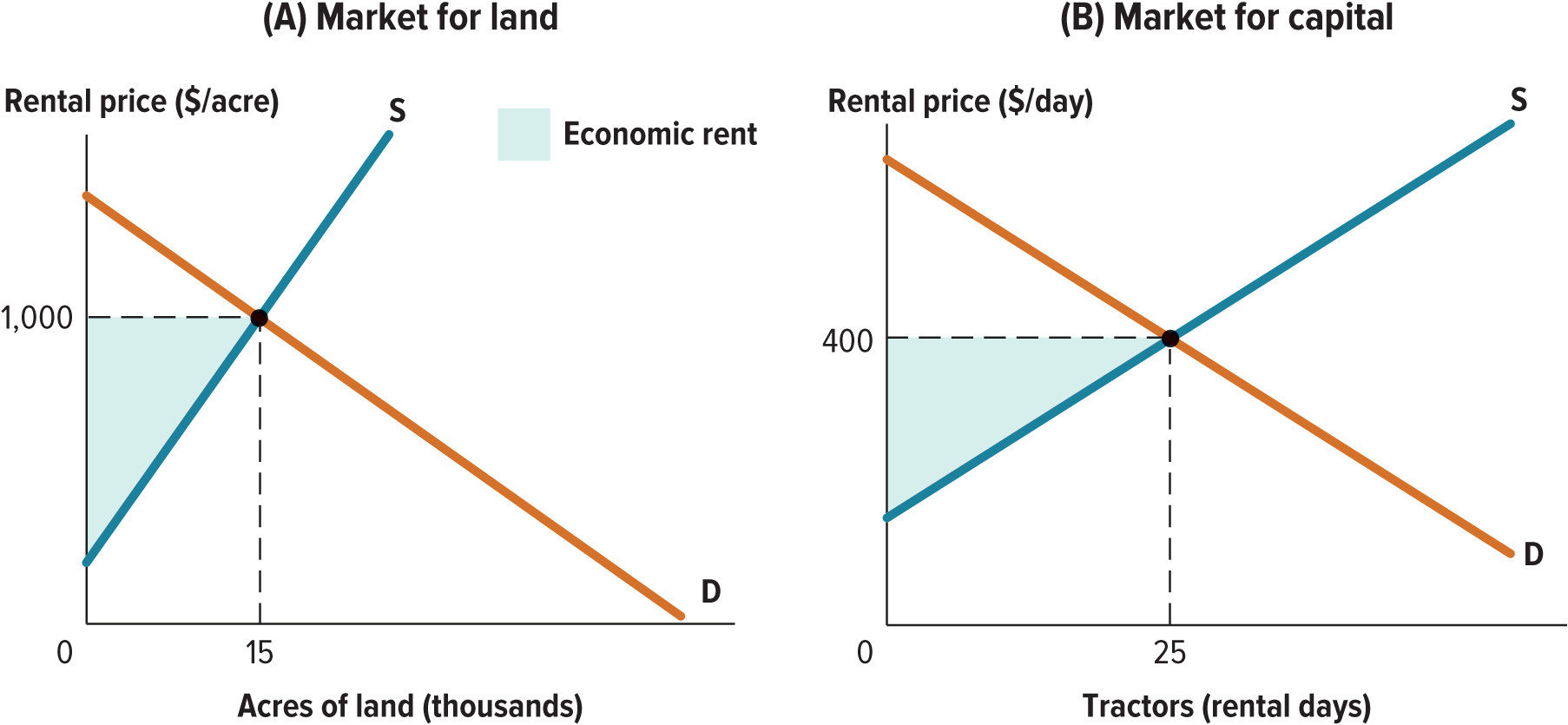

16.7. Markets for Land and Capital

- The markets for land and capital are similar to markets for labour; the major difference is that land and capital can be purchased as well as rented

- rental price: the price paid to use a factor of production for a certain period or task

- purchase price: the price paid to gain permanent ownership of a factor of production

- The word capital is often used loosely to refer to financial capital as well as physical capital

- When people invest money in the stock market or a company, they are using financial capital to purchase a share of the company’s physical capital

- economic rent: the gains that workers and owners of capital receive from supplying their labour or machinery in factor markets

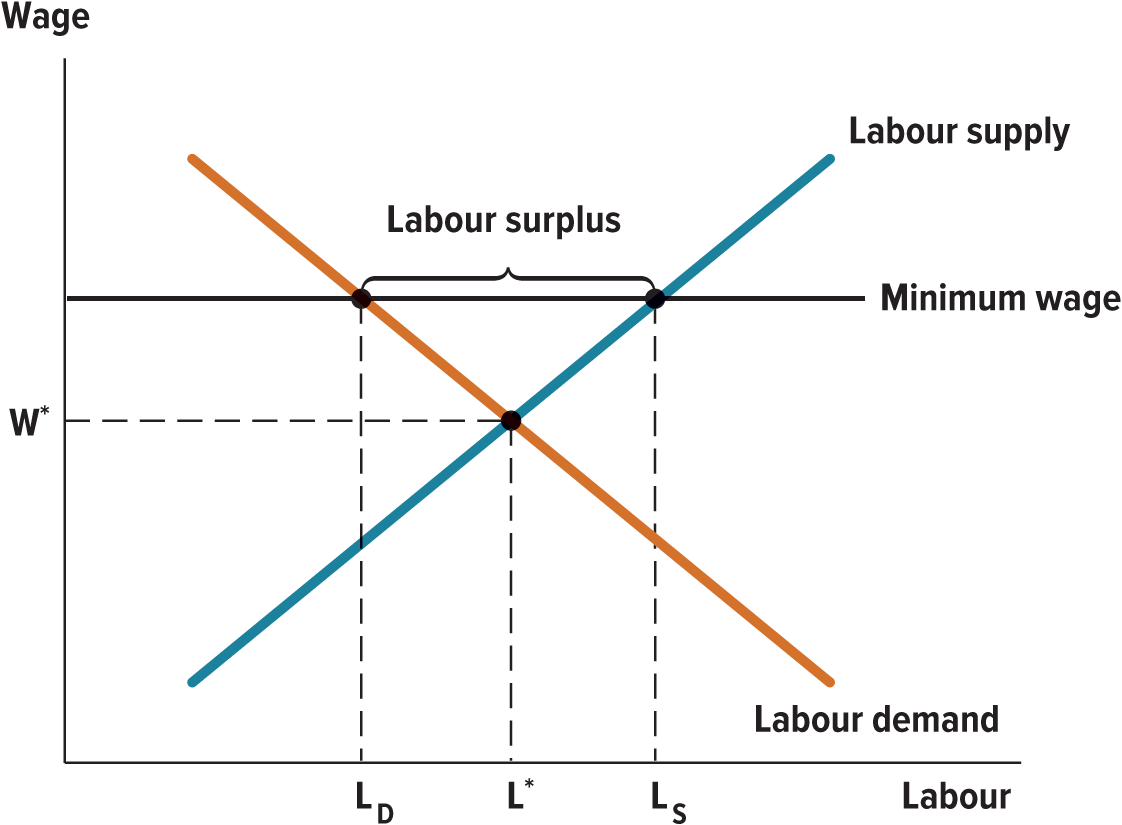

16.8. Minimum Wages and Efficiency Wages

- There are two common reasons for a wage to rise above the market equilibrium: minimum wages and efficiency wages

- A minimum wage is a price floor on the price of labour

- In an efficient labour market, a price floor causes excess supply and unemployment

- efficiency wage: a wage that is deliberately set above the market rate to increase worker productivity

16.9. Company Towns, Unions, and Labour Laws

- Just as markets for goods and services are not always perfectly competitive, neither are labour markets

- Monopsony: a market in which there is only one buyer but many sellers

- A monopsonist has the market power to push wages below the market equilibrium

- Workers can also gain market power, by banding together to make joint labour supply decisions and push their wages above the equilibrium

- Through regulations, the government can also impose costs on labour markets