1. Control Accounts

Control accounts used in the General Ledger:

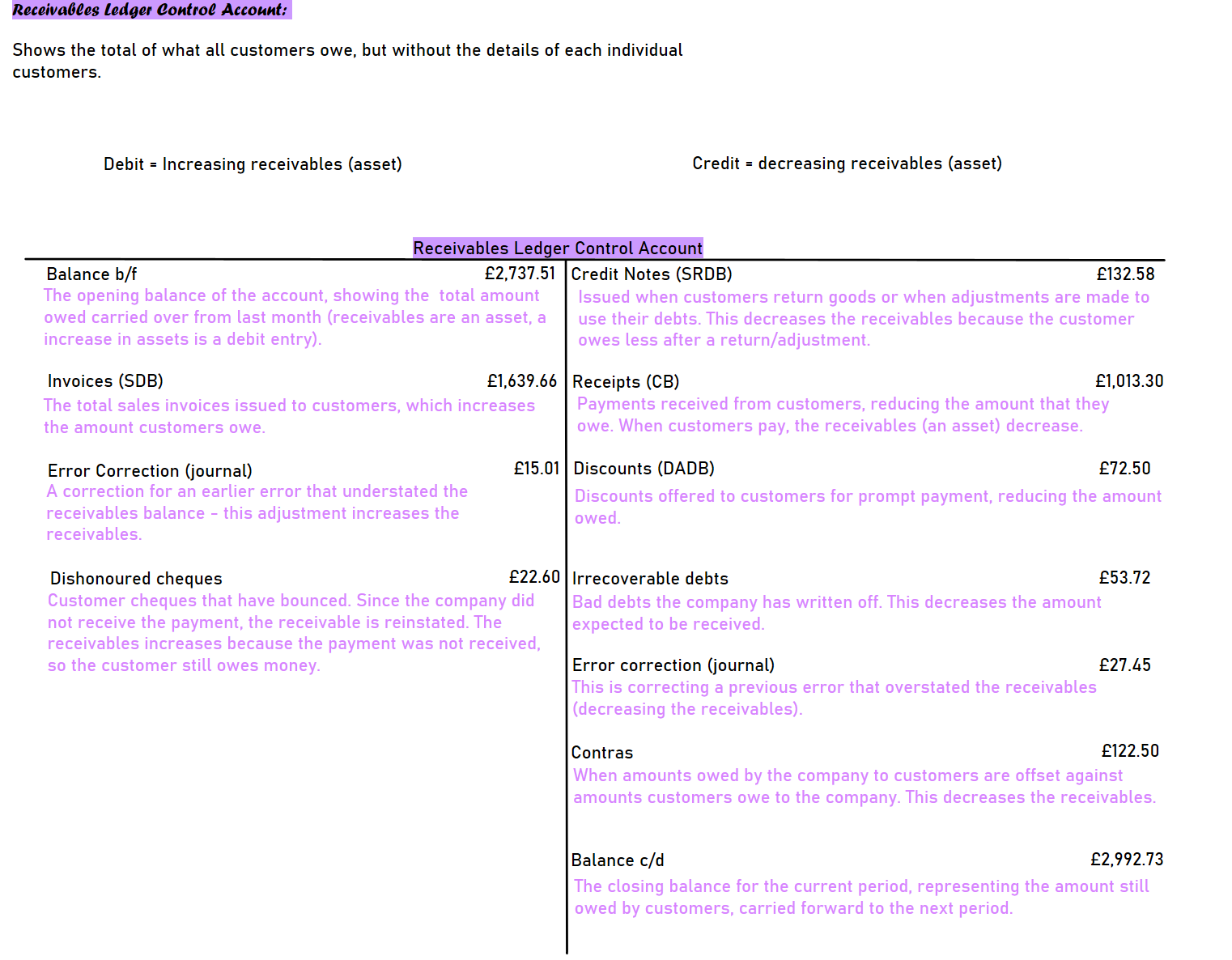

Receivables Ledger Control (trade debtors/sales ledger control): tracks the total amount customers owe (from sales made on credit)

Payables Ledger control (trade creditors/purchases ledger control): Keeps track of the total amount your business owes to suppliers (for purchases made on credit).

Cash and/or bank control (if the cash book is used solely as a book of prime entry): used to record cash and bank transactions

Petty cash control (if the petty cash book is used solely as a book of prime entry): Manages the petty cash book

VAT control: Records value added tax, both from sales (output VAT) and purchases (input VAT), and any payments or refunds involving HMRC.

Wages control: records all payroll transactions such as salaries and wages for employees.

RLCA= A summary account used to track money that a business is owed by its customers.

It is part of the General Ledger and gives a total figure of all customer debts without showing individual customer balances.

Receivables (debtors) are customers who bought goods/services on credit but haven't paid yet.

The Receivables Ledger lists details of each customers account: how much each customer owes and any payments that they make. This is not part of the double entry system. The receivables ledger is a 'breakdown' of the receivables ledger control account.

In an assessment, the receivables ledger may be referred to as a 'list of balances'.

The Receivables Ledger Control Account shows the total of what all customers owe, but without the details of each individual customer.

It is part of the double entry system, so if you have a debit in the RLCA, another account in the GL will need to be credited.

The RLCA is made up of all the customer accounts in the receivables ledger.

The brought down balance in the RLCA represents the total amount owed to us by our credit customers. This balance will be made up from all the individual balances in the receivables ledger.

Reconciliation:

List out all the individual balances from the receivables ledger and total up.

Balance off the receivables ledger control account.

The two totals should be equal.

Balances that do not reconcile:

If the totals do not agree, then errors need to be corrected in:

The control account

The individual receivables ledger account

Or, they need to be corrected in both.

Why do we carry out the reconciliation?:

The brought down balance on the receivables ledger control account will be transferred to the trial balance, so it is important that this figure is correct. Performing a reconciliation with the receivables ledger is a good way of checking for accuracy.

It helps us to identify errors to ensure that our double entry is correct.

Errors affecting the Receivables ledger control account:

There are a number of errors that could cause an imbalance in the reconciliation including:

A book of prime entry has been undercast (when you calculated the total column of the receivables ledger control account, the amount was less than it should have been) or overcast (the amount was more than it should have been). All the entries are correct, you have added them up incorrectly. Given that the figures are correct, the postings to the receivables ledger will be correct; it is only the posting to the RLCA that will be incorrect.

Postings have been made to the wrong side of the receivables ledger control account; e.g. you posted a receipt, credit note, discount or irrecoverable debt on the debit side instead of the credit side or, you posted an invoice on the credit side instead of the debit side.

Any entry may have been recorded in the receivables ledger, but not in the receivables ledger control account e.g. discounts allowed, irrecoverable debt.

An incorrect amount has been posted to the receivables ledger control account.

Errors affecting the receivables ledger:

An entry from a book of prime entry has not been posted to the receivables ledger

Postings have been made to the wrong side of the receivables ledger: you posted a receipt, credit note, discount or irrecoverable debt on the debit side instead of the credit side or, you posted an invoice on the credit side instead of the debit side.

An incorrect amount has been posted to the receivables ledger

The balance on a receivables ledger account has been incorrectly cast e.g. you made a calculation error when balancing off an account.

Errors affecting both:

An invoice or credit note that hasn’t been recorded in the relevant book of prime entry, so it hasn’t been recorded in the RLCA or receivables ledger.

A receipt hasn’t been recorded in the cash book, so it hasn’t been posted to the RLCA or the receivables ledger

An incorrect amount has been to both the RLCA and the receivables ledger

A discount hasn’t been recorded in the discounts allowed daybook, so it hasn’t been posted to the RLCA or the receivables ledger.

Both the Receivables Ledger Control Account and the Receivables ledger must be updated from the:

Sales Daybook: invoices to credit customers

Sales returns daybook: Credit notes to credit customers

Cash book: receipts from credit customers

Discounts allowed daybook: VAT Discount credit notes to credit customers.

Posting - The gross amount of the invoices/credit noted must be posted:

Receivables ledger control account: column totals

Receivables ledger: individual gross amounts.

Why its useful:

It provides a quick overview of how much the business is owed.

It helps ensure the total in the control account matches the total of the individual accounts in the Receivables ledger.

Items that appear in both the Receivables ledger and the Receivables ledger Control account:

Insert RLCA & Subsidiary receivables ledger A.N. OTHER (SL456)

On the debit side, you record primarily

the balance brought forward and any

further invoices that have been sent

to credit customers (these will have

been recorded in the sales daybook).

The only other item that might be

shown on the debit side is

dishonoured cheques - where a

customers cheque has bounced.

We would have originally recorded

the cheque on the credit side as a

receipt, but now we don’t have this

money, we need to remove it from

the Receivables Ledger and the RLCA

by recording it as a debit entry. The

customer owes us this money again,

so we increase the receivable on the

debit side.

The debit side increases what is owed to

Us (an increase in the asset of receivables/

Debtors).

The differences between the Receivables Ledger Control Account and the Receivables are:

The RLCA records transactions relating to all of our credit customers

The Receivables Ledger records individual transactions relating to individual customers (each have their own account).

The RLCA is part of the double entry system (General Ledger)

The Receivables Ledger is not part of the double entry system.

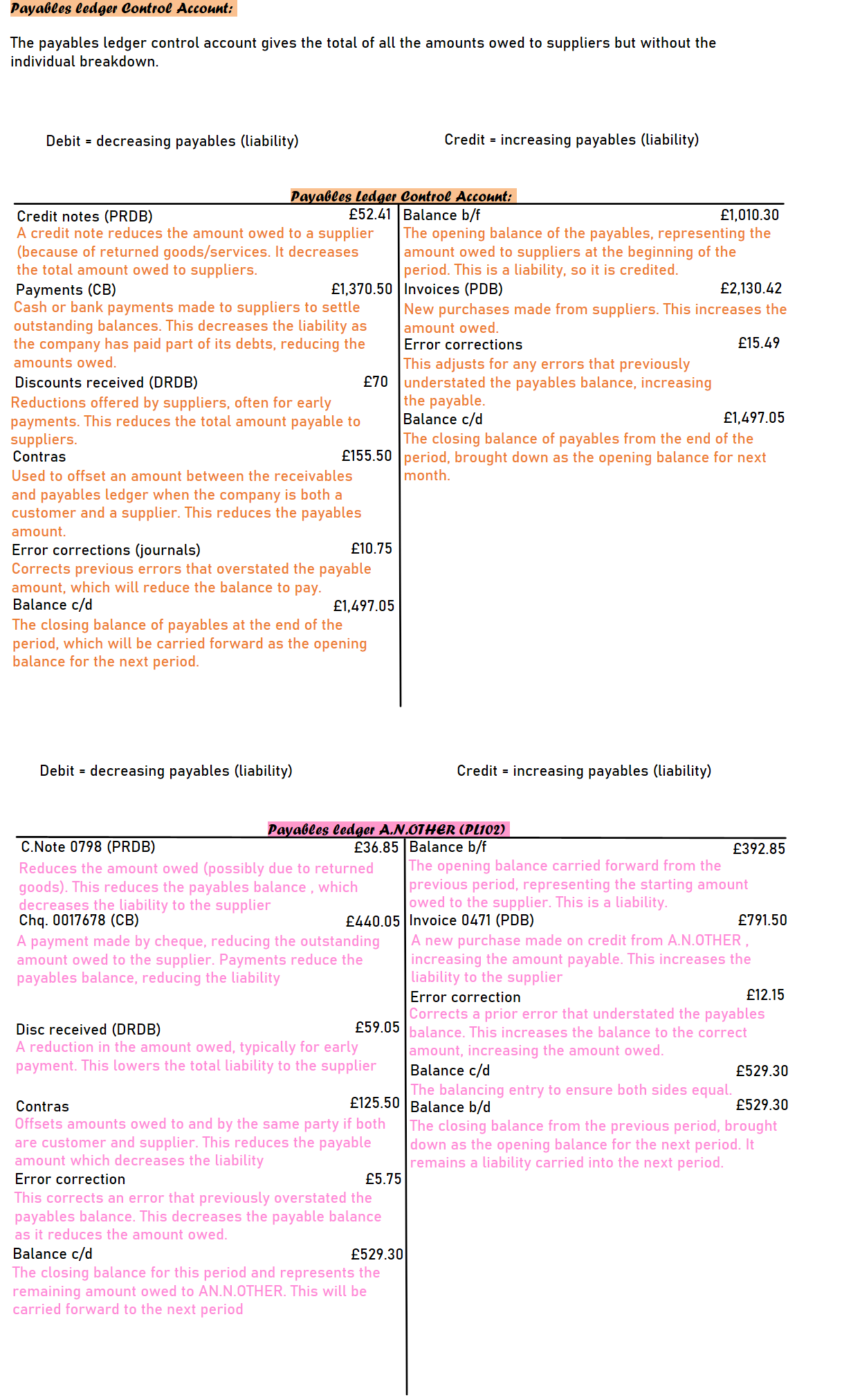

PLCA= A summary account used to track the money the business owes to its suppliers (also called creditors). Its part of the General ledger and shows the total amount the business owes to all suppliers, but without the details of individual supplier balances.

Payables are suppliers who sold goods or services to the business on credit, but the business hasn’t paid yet.

The Payables ledger shows the details for each supplier, and how much the business owes each one.

Where we keep the individual supplier accounts.

It is a 'breakdown' of the Payables Ledger Control Account

It represents the amounts we owe to individual credit suppliers

It is not part of the double entry system.

In an assessment the payables ledger is likely to be referred to as 'list of balances'

The payables ledger control account gives the total of all the amounts owed to suppliers but without the individual breakdown.

The PLCA is part of the double entry system i.e. if you have a debit in the in the PLCA, another account in the general ledger will need to be credited.

The brought down balance on the PLCA represents the total amount we owe our credit suppliers. This balance will be made up from all the individual balances in the payables ledger.

Reconciliation:

List out all of the individual balances from the payables ledger and total up.

Balance off the PLCA

The two totals should be equal

Balances that do not reconcile:

If the totals do not agree, errors need to be corrected in:

The payables ledger control account

The individual payables ledger account

Or, they need to be corrected in both

Why do we carry out the reconciliation?

The brought down balance on the payables ledger control account will be transferred to the trial balance, so it is very important that this figure is correct. Performing the reconciliation with the payables ledger is a good way of checking for accuracy.

It helps us to identify errors to ensure that the double entry is correct.

Errors affecting the payables ledger control account:

There are a number of errors that could cause an imbalance in the reconciliation:

A book of prime entry has been undercast/overcast (the total column in the PLCA was either more or less than it should have been due to a calculation error when totalling up the total column. Given that the entries are correct, the postings to the payables ledger will be correct, it is only the postings to the payables ledger control account that will be incorrect.

Postings have been made to the wrong side of the PLCA: e.g. you posted a payment, credit note, or discount on the credit side instead of he debit side or, you posted an invoice on the debit side instead of the credit side.

An entry may have been recorded in the payables ledger, but not in the PLCA

An incorrect amount has been posted to the PLCA

Errors affecting the payables ledger:

An entry from a book of prime entry has not been posted to the payables ledger

Postings have been made to the wrong side of the payables ledger: you posted a payment, credit note or discount on the credit side instead of the debit side or, you posted an invoice on the debit side instead of on the credit side

An incorrect amount has been posted to the payables ledger

The balance on a payables ledger account has been incorrectly cast e.g. you made a calculation error when balancing off an account

Errors affecting both:

An invoice or a credit note that hasn’t been recorded in the relevant book of prime entry, so it hasn’t been recorded in the PLCA or payables ledger

A payment hasn’t been recorded in the cash book, so it hasn’t been posted to the PLCA or the payables ledger

An incorrect amount has been posted to both the PLCA and payables ledger

A discount hasn’t been recorded in the discounts received daybook, so it hasn’t been posted to the PLC A or payables ledger.

Both the PLCA and the payables ledger must be updated from:

Purchases daybook: invoices received from suppliers

Cash book: payments made to suppliers

Purchases returns daybook: credit notes received from suppliers

Discounts received daybook: VAT discount credit notes received from suppliers.

Posting - the gross amount on invoices/credit notes must be posted:

Payables ledger control account: column totals

Payables ledger: individual gross totals

Why its useful:

It provides a quick overview of how much the business owes in total to all suppliers

It helps to ensure that the total in the control account matches the total of all individual supplier balances in the payables ledger.

Insert pictures of plca & pl account

On the debit side, we record credit notes, payments, discounts and contras - all entries which decrease what we owe to our credit suppliers (a decrease in the liability of payables/creditors)

On the credit side, we record the balance brought forward and any invoices that have been sent to us by credit suppliers (which will have been recorded in the purchases day book). Invoices will increase what we owe to suppliers (an increase in the liability of payables/creditors).

Differences between the payables ledger control account and the payables ledger:

The PLCA records transactions relating to all of our credit suppliers

The payables ledger records individual transactions relating to individual suppliers

The PLCA is part of the double entry system

The payables ledger is not part of the double entry system

Contra:

Where a customer is also a supplier. The lowest of the two amounts owed will be 'offset'.

We 'contra' the lower of the two accounts e.g. if you owe me £100 and I owe you £150, we will agree to do a contra for the lowest of the two amounts i.e the £100.

When the receivables ledger and the payables ledger accounts are balanced off, you will owe me nothing but I will still owe you £50.

Contras are always posted on the 'payment' side of the account, so this will be a credit in the receivables ledger control account and a debit in the payables ledger control account.

Insert photo of receivables ledger with contra

Contra Entry Demo:

Smithco is a customer who is also a supplier

We have sold goods to Smithco for £200

We have purchased goods from Smithco for £150

How the T-accounts are affected:

Insert t-accounts

Vat Control Account:

An accurate Vat Control Account is important as we use it to assist us in preparing the VAT return, so that we know how much is payable/reclaimable from HMRC.

It is also important to ensure that the VAT return is prepared promptly, in order to avoid paying penalties for late submission.

Output Tax = VAT on sales: The VAT that a business adds to the price of the goods/services it sells to customers. It’s the tax the business collects from its customers and later pays to the government.

Input Tax = VAT on purchases: The VAT that a business pays when it buys goods/services from other businesses. The business can often reclaim this amount from the government.

Posting to the VAT Control Account:

You will need to post VAT entries from all the books of Prime Entry, and any irrecoverable debt.

Insert VAT control a/c

Debit:

Vat on credit purchases (PDB): this figure comes from the VAT column (overall total) in the purchases day book. It is input VAT; therefore we can reclaim it from HMRC.

VAT on cash purchases (CPB): this figure comes from the VAT column (overall total) in the cash payments book. It is input VAT and can be reclaimed from HMRC.

VAT on petty cash purchases (PCB): this figure comes from VAT column (overall total) in the petty cash book - payments side. It is input VAT and can be reclaimed from HMRC.

VAT on sales returns (SRDB): this figure comes from the VAT column (overall total) in the sales returns daybook. It is input VAT and can be reclaimed from HMRC.

VAT on VAT credit notes (DADB): this figure comes from the VAT column (overall total) in the discounts allowed daybook. It is input VAT and so can be reclaimed from HMRC.

VAT on irrecoverable debts (journal): this debt will need to be removed from the accounts, so this means we can reclaim the VAT element of the debt. We will record the irrecoverable debt using a journal. It is input VAT and can be reclaimable from HMRC.

If the b/d balance is on the debit side, this will represent money payable by HMRC. Add explanation

Credit:

VAT on credit sales (SDB): this figure comes from the VAT column (overall total) in the sales day book. It is output VAT; therefore it is payable to HRMC.

VAT on cash sales (CRB): this figure comes from the VAT column (overall total) in the cash receipts book. It is output VAT; therefor it is payable to HMRC.

VAT on purchases returns (PRDB): This figure comes from the VAT column (overall total) in the purchases returns daybook. It is output VAT; therefore it is payable to HRMC.

VAT on credit notes (DRDB): this figure comes from the VAT column (overall total) in the discounts received daybook. It is output VAT and so it is payable to HMRC.

VAT reclaimed from HRMC: if we are in a 'reclaim situation', this could be because we purchased some costly machinery or equipment during the period, or the business isn't doing

very well.

If the b/d balance is on the credit side, this will represent money owed to HMRC.

VAT paid to HRMC: If we need to make a payment to HMRC (the VAT on sales is greater than VAT on purchases), then the double entry posting will be debit VAT and credit bank. Add explanation

If we are able to reclaim VAT from HMRC (the VAT on sales is lower than VAT on purchases), the double entry posting will be debit bank and credit VAT. Add explanation.

| |||

| Credit = decreasing receivables (asset) | ||

| Debit = Increasing receivables (asset) | ||

|

| |||

| Credit = decreases receivables (assets) | ||

| Debit = increases receivables (assets) | ||

|

| |||

| Credit = increasing payables (liability) | ||

| Debit = decreasing payables (liability) | ||

|

| |||

| Debit = decreasing payables (liability) | Credit = increasing payables (liability) |