Unit 1: Basic Economic Concepts

1.1 Scarcity:

What is economics?

science of scarcity

scarcity - we have unlimited wants but limited resources

we must make choices on how to use our resources

economics is the study of choices

Ex: choosing how many people to hire, must choose how much to spend on welfare…

Social science concerned with the efficient use of scarce resources to achieve maximum satisfaction of economic wants

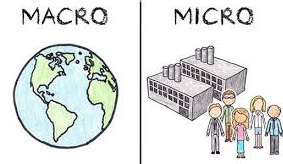

Micro vs. Macro

Micro - study of small economic units such as individuals, firms, and markets

Ex: supply and demand in specific industries, production costs, labor markets

Macro - study of the large economy as a whole or economic aggregates

Ex: economic growth, government spending, inflation, unemployment, international trade

How is Economics used?

theoretical economics - scientific method to make generalizations and abstractions to develop theories, then applied to fix problems or meet economic goals called policy economics

Positive vs. Normative

Positive statements - based on facts, avoids value judgement (what is)

Ex: Climate change is influencing newly made policies

Normative statements - includes value judgement (what ought to be)

Ex: The government should focus on climate change

5 Key Economic Assumptions

society has unlimited wants and limited resources (scarcity)

due to scarcity, choices must be made. Every choice has a cost (trade-off)

everyone’s goal is to make choices that maximize their satisfaction. Everyone acts in their own “self-interest”

everyone makes decisions by comparing the marginal costs and marginal benefits of every choice

real-life situations can be explained and analyzed through simplified models and graphs

Economic Terminology

utility - satisfaction

marginal - additional

allocate - distribute

Price vs. Cost (What’s the price? vs. How much does that cost?)

price - amount buyer (or consumer pays)

cost = amount seller says to produce a good

Investment

the money spent by businesses to improve their production

Ex: $1 million new factory

consumer goods - created for direct consumption

Ex: pizza

capital goods - created for indirect consumption

Ex: oven, blenders, knives, etc.

The Four Factors of Production

all resources can be classified as one of the following factors of production

land - all natural resources that are used to produce goods and services

payment for the use of land is called rent

Ex: water, sun, plants, animals

labor - any effort a person devotes to a task for which that person is paid

payment for the use of labor is called wages

Ex: manual laborers, lawyers, doctors, teachers, waiters, etc

capital:

physical capital - any human-made resource that is used to create other goods and services

Ex: tools, tractors, machinery, buildings, factories, etc

human capital - any skills or knowledge gained by a worker through education and experience

payment for the use of capital is called interest

entrepreneurship - ambitions leaders that combine the other factors of production to create goods and services

payment for entrepreneurship is called profit

Ex: Henry Ford, Bill Gates, Inventors, Store Owners, etc.

Entrepreneurs take the initiative, innovate, and act as the risk bearers so they can obtain profit

Profit = revenue - cost

keep in mind that things such as money, stocks, and bonds are considered financial instruments, they facilitate trade but they have no part in the production process

Productivity

a measure of efficiency that shows the number of outputs per unit of input

since all resources are scarce, improving productivity allows use to produce more stuff with fewer resources

1.2: Resource Allocation and Economic Systems

The Three Economic Questions

what goods and services should be produced?

how should these goods and services be produced?

who consumes these goods and services

the way these questions are answered determines the economic system, method used by society to produce and distribute goods and services

Economic Systems

Command (Centrally-Planned) Economy, Communism

the government owns all the resources, answers the three economic questions,

Ex: Cuba, North Korea, former Soviet Union, and China?

little incentive to work harder and central planners have a hard time predicting preferences

Advantages:

low unemployment, everyone has a job

great job security, the government doesn’t go out of business

less income inequality

“free” health care

Disadvantages

no incentive to work harder

no incentive to innovate or come up with good ideas

no competition keeps the quality of goods poor

corrupt leaders

few individual freedoms

Exam[ple of why communism failed:

other business cannot start making computers, therefore no competition

means higher prices, lower quality, and less product variety

unless if government decides to make another factory, there will be a shortage of goods that consumers want

Free Market Policy (Capitalism)

little government involvement in the economy (laissez faire = let it be)

individuals own resources and answer the three economic questions

opportunity to make profit gives people INCENTIVE to produce quality items efficiently

wide variety of goods available to consumers

competition and self-interest work together to regulate the economy (keeps prices down and quality up)

Example of how the free market regulates itself:

if consumers want smartphones and only one company is making them, other businesses have the incentive to start making smartphones to earn profit

this leads to more completion, meaning lower prices, better quality, and more product variety

we produce goods and services that society wants because “resources follow profits”

End Result: most efficient production of goods that consumers want, produced at the lowest prices, and the highest quality

producers and consumers act in their own self-interest and make adjustments automatically

The Invisible Hand

concept that society’s goals will be met as individuals seek their own self-interest

Ex: if society wants fuel efficient cars, producers will make more of them without the government’s involvement

competition and self-interest act as an invisible hand that regulates the free market

Mixed Economy

as system with free markets but also some government intervention

almost all countries, including the US, have mixed economies

countries with free markets, property rights, and The Rule of Law have historically seen greater economic growth because they are more productive

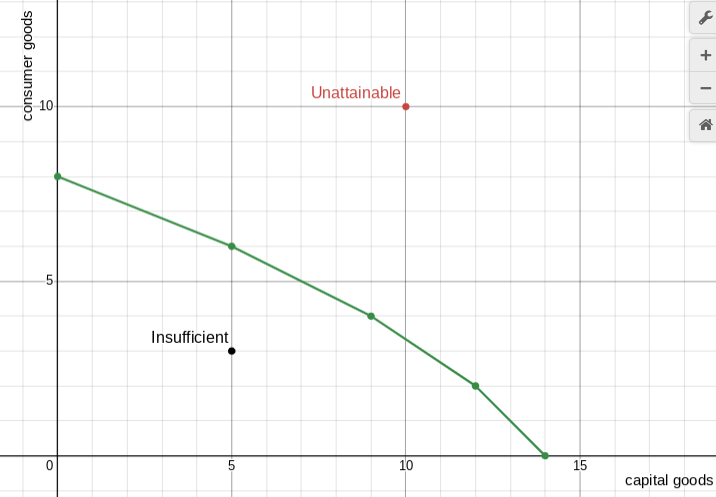

1.3: Production Possibilities Curve (PPC)

use economic models to explain concept in words, use numbers as example, and generate graphs from numbers

PPC (or frontier) is a model that shows alternative ways that an economy can use its scarce resources

graphically demonstrates scarcity, trade-offs, opportunity costs, and efficiently

4 Key Assumptions

only two goods can be produced

full employment of resources

fixed resources (Ceteris Paribus)

fixed technology

PPC graphically shows scarcity with the fixed resources given as points

anything inside the curve is insufficient, this could mean employment

combinations outside the curve is impossible with the resources currently

you can also calculate the opportunity costs

Ex: As the curve goes down, your opportunity costs for consumer goods increase

constant opportunity costs - resources are easily adaptable for producing either good, resulting in a straight line instead of a curve (which is not common)

Law of Increasing Opportunity Cost - as you produce more of any good, the opportunity cost (forgone production of another good) will increase

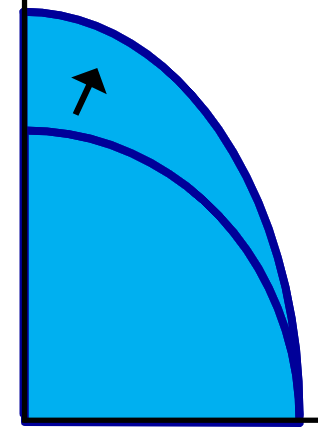

3 Shifters of The PPC

change in resource quantity or quality

change in technology

change in trade (allows more consumption)

let’s say something happened that made the consumer goods go up, the PPC curve will change so that the capital goods remain the same and consumer goods increase

The curve change will depend on how the factors are affected

1.4: Comparative Advantage and Gains from Trade

Specialization and Trade, Why do people trade?

everyone specializes in the production of some goods and serves and trades for others

more access to trade means more choices and a higher standard of living

Absolute and Comparative Advantage

per unit opportunity cost = opportunity cost/units gained

Ex: costs you $50 to make 5 t-shirts, per unit opportunity cost is $10 (50/5)

Absolute Advantage - producer that can produce the most output OR requires the least amount of inputs (resources)

Comparative Advantage - producer with the lowest opportunity cost

to determine how to calculate comparative advantage, you need to figure out one thing

if you are given the INPUTS (time, resources), you calculate by putting the other good UNDER the same good you are finding

Ex: opportunity cost for soybeans = soybeans/coffee

if you are given OUTPUTS (overall production), you calculate by putting the other good OVER the same good you are finding

Ex: opportunity cost for soybeans = coffee/soybeans

countries should trade if they have a relatively lower opportunity cost

they should specialize in the good that is “cheaper” for them to produce (the one they have comparative advantage in)

Terms of Trade

both countries can benefit from trade if they each have relatively lower opportunity costs

the agreed upon conditions that would benefit both countries

1.5: Cost-Benefit Analysis

Trade-offs vs. Opportunity Cost

trade-offs - ALL the alternatives that we give up when we make a choice

opportunity cost - most desirable alternate given up when you make a choice

Explicit Costs vs. Implicit Costs

explicit Costs - traditional out of pocket costs associated with making a decision

implicit Costs - opportunity costs of making a decision

Benefits and Cost on a Graph

1.6: Marginal Analysis and Consumer Choice

Marginal Analysis

thinking on the margin, making decisions based on increments

you will continue to do something as long as the marginal benefit is greater than the marginal cost

Consumer Choice and Utility Maximization

law of diminishing marginal utility states as you consume anything, the additional satisfaction that you will receive will eventually start to decrease

the more you buy of any good, the lesson satisfaction you will feel

you will consume until marginal benefit = marginal cost

Utility Maximizing Rule - the consumer’s money should be spent so that the marginal utility per dollar of each goods equal each other (MUx/Px = MUy/Py)