B4002 - Chapter 12

Accounting for NFPOs and Public Sector Organizations

November 27, 2023

Only MC on the final exam

Wednesday – Chapter 10/11 review

Monday – Exam prep

Introduction

Not-for-profit organizations (NFPOs) are defined in Part III of the CPA Canada Handbook as entities, normally without transferable ownership interests, organized and operated exclusively for social, educational, professional, religious, health, charitable or any other not-for-profit purpose

“Entities, normally without transferable ownership interests” are corps without shareholders or shares

A not-for-profit organization’s members, contributors and other resource providers do not, in such capacity, receive any financial return directly from the organization

This is a problem from an accounting POV – contributors provide money to the entity, but they get nothing back & there is no reciprocity

NFPOs differ from profit-oriented organizations in the following ways:

In fulfilling their objectives, they typically provide services or goods to identifiable segments of society without the expectations of profit

Example: homelessness, soup kitchens

When looking at FS, a surplus at the end of the year has a lot of scrutiny as to what it will be spent on – not uncommon to see a zero

The goal is to not have continuous surpluses

Their resources are provided by individual and government contributors without the expectation of gain or repayments; often these contributors have restrictions attached to them

They have no readily identifiable ownership interests that can be sold, transferred, or redeemed

They are governed by volunteers although many NFPOs also have paid employees

Not-For-Profit Reporting Today

In December 2010, the Handbook was restructured into five parts

The not-for-profit (NFP) sector was classified into two sectors:

(1) The public NFP section

Example: hospitals that are controlled by the government

NFPOs that have a choice to follow the CPA Canada Public Sector Accounting (PSA) Handbook including the 4200 series or the PSA Handbook without the 4200 series

Appendix 12C discusses accounting standards applicable to the public sector

Cannot use ASPE – it doesn’t make sense

(2) The private NFP sector

Includes NFPOs that are not controlled by the government

Anyone can open a NFPO

They have the choice to follow either Part I (IFRS) or Part III – accounting standards for NFPOs of the CPA Canada Handbook

Note: Do not need to memorize section numbers – they’re handy to know

Section 1001 – Financial Statement Concepts for NFPO

This section describes the …

Objectives of FS

Qualitative characteristics of financial info

Elements of FS

Recognition and measurement in FS the cost of service and how the cost was funded are key info needs for the users of a NFPO

Section 1101 – GAAP for NFPO

This section describes the primary and other sources of GAAP for NFPOs

Part II of the Handbook provides a substantial portion of GAAP for NFPOs

A NFPO should present only one set of general-purpose FS prepared under Part III of the Handbook

Section 1401 – General Standards of FS Presentation for NFPO

This section describes fair presentation in accordance with GAAP, going concern, FS required for NFPOs, and comparative info

The FS for an NFPO is similar to the FS required under ASPE

Section 1501 – First Time Adoption by NFPO

This section applies when an NFPO is adopting Part III for the first time

Changes in policies would normally be applied retrospectively when first adopting Part III of the Handbook

Section 3032 – Inventories Held by NFPO

This is an example of the problem with reciprocity

How do you value it? FMV

What would you credit? Donations/Contribution (this is an IS account – revenue)

Except as otherwise provided for in this section, an NFPO applies the section on inventories in Part II

A NFPO may receive inventory without any cost and may have no intention of ever selling the inventory

Section 3463 – Reporting Employee Future Benefits by NFPO

This section provides guidance for defined benefit plans on the recognition and presentation of remeasurements and other items that differ from the guidance in Section 3462

Section 4400 – Financial Statement Presentation by NFPO

An NFPO must present the following FS for eternal reporting purposes:

Statement of operations

Statement of financial position

No equity 🡪 net assets

Statement of changes in net assets

Statement of cash flows

Section 4410 – Contributions, Revenue Recognition

An NFPO can have two basic types of revenues:

(1) Contributions (in cash or in kind)

(2) Other types (investments, the sale of goods and services)

Contribution revenue is a type of revenue that is unique to NFPOs, because it is non-reciprocal

Important terms** NFPOs receive three different types of contributions:

(1) Restricted

“You can only use this money for soccer purposes”

DR. Cash; CR. Deferred Contributions (liability account)

Recognize revenue (contributions) as the NFPO spends the cash on the “sporting goods”

To get rid of the Deferred Contribution, you would CR. Contribution/Donations

(2) Endowment

You can’t touch the principal

DR. Cash; CR. Endowment fund (liability account)

(3) Unrestricted

“Here is money, do whatever you want with it”

As long as the money is spent in the mandate of the NFPO

DR. Cash; CR. Contribution/Donations

Many NFPOs receive a major source of their revenues from endowment earnings

Section 4420 – Contributions Receivable

This section provides guidance on how to apply accrual accounting concepts to contributions

A contribution should be recognized as an asset when the amount to be received can be reasonably estimated and ultimate collection is reasonably assured

The only time this makes sense is when you have a funding agreement

Pledges are promises to donate cash or other assets to an NFPO, but they are legally unenforceable

Bequests are normally not recorded until a will has been probated

If the NFPO is borrowing from the bank, it would be best to have AR to show that they can pay back the credit

Section 4433 – Tangible Capital Assets Held by NFPO

Section 4433 requires that Part II Section 3061, PPE and Section 3110, Asset Retirement Obligations should be used to account for tangible capital assets and Part II Section 3041 Agriculture should be used to account for productive biological assets unless otherwise provided in the section

An NFPO should capitalize all tangible capital assets in the statement of financial position and amortize them as appropriate in the statement of operations

This is the starting point

When an asset no longer contributes to the organization’s ability to provide services or when the value of future economic benefits or service potential associated with the tangible capital assets are less than their net carrying amounts, it should be written down to FV or replacement cost

Disclosures for impairments of tangible capital assets should be provided in accordance with Section 3063, Impairment of Long-Lived Assets

Section 4434 – Intangible Assets Held by NFPO

This section was introduced to clarify that Part II Section 3064 Goodwill and Intangible Assets applies to an NFPO’s intangible assets

The same requirements as discussed in the previous slides for tangible capital assets also apply for intangible assets

Small NFPOs

GAAP require large NFPOs to capitalize and amortize their capital assets

An exemption from the requirement to capitalize is granted to small NFPOs (those whose 2-year average of annual revenues is less than $500,000)

Section 4441 – Collections Held by NFPO

Collections are works of art and historical treasures:

Held for public exhibition, education, or research

Protected, cared for, and preserved

Subject to organizational policies that require any proceeds from their sale to be used to acquire other items for the collection, or for the direct care of the existing collection

Under Section 4441, collections should be recorded as either cost or nominal value and the same policy is normally applied for all collections

Section 4449 – Combinations by NFPO

This section outlines the accounting for the initial measurement of a combination depending on whether the combination is a merger of equals or an acquisition of one party by another party

The following five criteria must all be met to classify the combination as a merger:

(1) No party is characterized as the acquirer or acquiree

(2) Both parties participate in determining the terms of the combination

(3) No consideration flows to a third party

(4) The combined organization encompasses the purposes of the combining organizations

(5) There is no significant decline in the client communities served

A merger is accounted for by aggregating the carrying amount of the assets, liabilities, and the net assets of the combining entities as though the entities have always been combined

The combined entity presents comparative info showing the aggregated results for the prior period

Uniform accounting policies should be applied for each of the combining entities at the date of the merger and retrospectively for the comparative period

Section 4450 – Reporting Controlled and Related Entities by NFPO

This section outlines the FS presentation and disclosures required when an NFPO has a control, significant influence, joint venture, or economic interest type of relationship with both profit oriented and NFPOs

The breakdown used is similar to that for profit-oriented organizations, but the required financial reporting has some differences

A control investment is one that gives an NFPO control over either profit-oriented organizations or other NFPOs

Control over NFPOs is consolidated of an NFPO where one of the three alternatives are allowed – the alternatives apply to each controlled NFPO

Control over profit-oriented companies is when a controlled profit-oriented organization can either be consolidated or reported using the equity method

Joint control is when a jointly controlled organization can be either proportionately consolidated or reported using the equity method

Significant influence investment is a profit-oriented organization that is reported using the equity method

When an organization has an economic interest in another NFPO, the nature and extent of this interest should be disclosed

Section 4460 – Disclosure of Related Party Transactions by NFPO

Related parties include those over which control, joint control, significant influence, or other economic interests exist

Section 4460 provides disclosure standards virtually identical to those set out in Section 3840 for profit-oriented enterprises

An NFPO must disclose all related-party transactions with another NFPO or a profit-oriented entity

Section 4470 – Disclosure of Allocated Expenses by NFPO

When an NFPO classes its expenses by function on the statement of operations, it may need or want to allocate certain related expenses to those functions

Certain expenses, however, may relate directly to more than one function, in particular fundraising expenses and general support expenses

When these two types of expenses are allocated to other functions, disclosure is required of the allocation accounting policy, the nature of the expense, the basis on which the allocations have been made, the amounts of each that have allocated, and the functions to which they have been allocated

The Basics of Fund Accounting

Fund accounting can be and has been used very successfully to keep track of restricted resources and/or programs, and to convey info through the FS about the restrictions placed on the organization’s resources, either by specific donors or by the terms of government grants

The fund is responsible for a particular activity or a line in the NFPO

Provides the user the goal of the activities that the NFPO is trying to accomplish

Fund accounting comprises the collective accounting procedures resulting in a self-balancing set of accounts for each fund established by legal, contractual, or voluntary actions of an organization

Elements of a fund can include assets, liabilities, net assets, revenues, and expenses (and gains and losses where appropriate)

Fund accounting involves an accounting segregation, although not necessarily a physical segregation, of resources

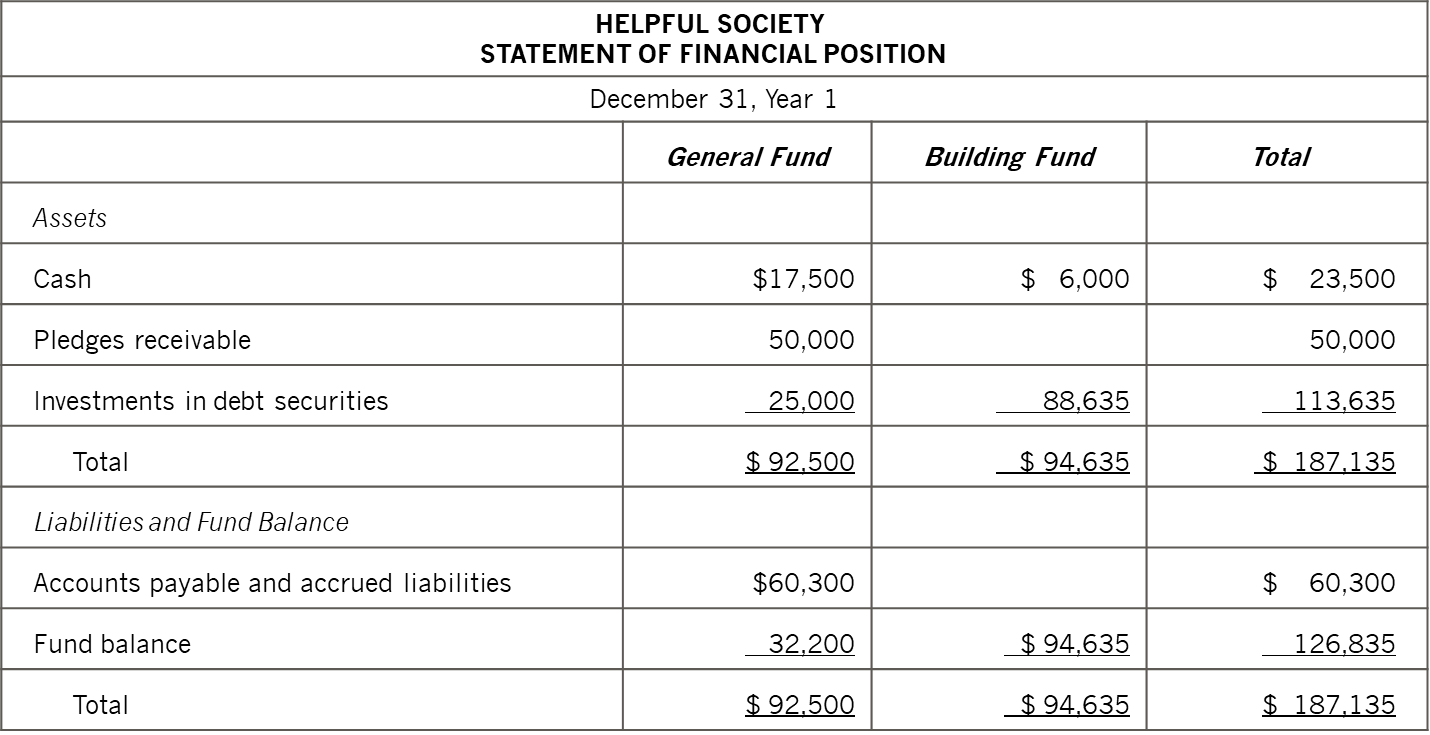

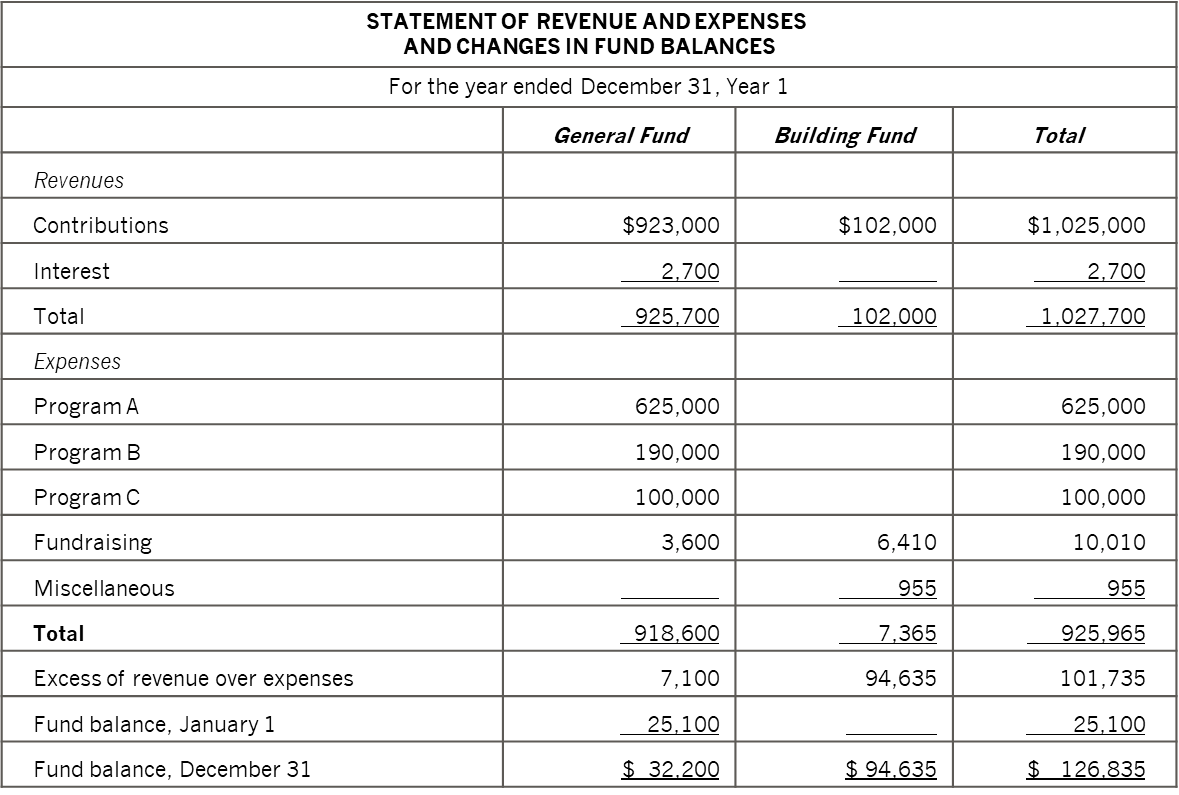

Note: look at exhibit 12.1, it illustrates the use of fund accounting as a means of reporting this form of stewardship

Exhibit 12.1 – Helpful Society

Building fund – can only be spent on the building they own, or they have an endowment

Large surplus = net assets = equity = RE

Suppose next year they get no donations, then they use what is in their fund balance

Building fund – donation

If it was an endowment, we wouldn’t see the total on the IS

Seems restricted – can only be used on the building to operate their NFPO

Fundraising is probably related to how they got the donation

“Excess of revenue over expenses” is the same as surplus 🡪 do not use “profit”

Accounting for Contributions

Part III has defined two methods of accounting for contributions

(1) The deferral method

Can be used with or without fund accounting

(2) The restricted fund method

Has to be used in combination with fund accounting

If the organization wants to present an overall picture of the organization, then it has to use the deferral method

If the organization wants to report on a fund accounting basis, it can choose the deferral method for all funds or the restricted fund method

The Restricted Fund Method

The restricted fund method requires a NFPO to repot a general fund, at least one restricted fund, and, if it has endowments or receives endowment contributions, an endowment fund

The restricted funds will be used to record externally restricted revenue as well as any restricted income generated from endowment fund investment

The endowment fund, which must be maintained in perpetuity will show only contribution revenue and no expenses

The general fund reflects all unrestricted contributions and investment income included any unrestricted income generated from endowment fund investments

Using the deferral method, the general fund also reports restricted contributions and investment income for which no separate restricted fund exists

Contributions are reported as revenue when received/receivable if a separate restricted or endowment fund has been established for these contributions

The provisions of the deferral method might have to be applied when the restricted fund method is used

Fund balances for the restricted and endowment funds represent the amount of net assets restricted for that fund’s purpose

General fund captures the agency’s operating activities

The Deferral Method

The deferral method matches contribution revenues with related expenses

Unrestricted contributions are reported as revenue in the period received or receivable, because there are no particular related expenses associated with them

Endowment contributions are not shown on the operating statement; rather, they are reflected in the statement of changes in net assets because they will never have related expenses

Restricted contributions are matched against related expenses

Restricted contributions for future expenses are deferred and recognized in revenue in the same periods as related expenses

The handling of restricted contributions for the acquisition of capital assets depends on whether related expenses are associated with them

Restricted contributions for expenses of the current period are recognized as revenue in the current period

Contributions for a depreciable asset are recognized as revenue as the asset is being amortized

Deferred contributions represent the unamortized amount of capital assets either donated or acquired with restricted contributions

The deferred contributions distinguish between unspent contributions and the unamortized portion of contributions being matched to amortization expenses

The FS presentation for contributions is substantially different under the two different reporting methods

Donated Capital Assets, Materials, and Services

An NFPO is required to record the donation of capital assets at FV

If FV cannot be determined, a nominal value will be used

A donated depreciable asset is reported as …

(1) Deferred contributions under the deferral method

DR. Buildings $500,000;CR. Deferred Contributions $500,000

YE: DR. Depreciation $50,000;CR. Accumulated Depreciation $50,000 & DR. Deferred Contribution $50,000; CR. Contributions $50,000 🡪 the depreciation model drives the revenue recognition

(2) Contribution revenue under the restricted fund method

An NFPO has the option of reporting or not reporting donated material and services

Reporting is permitted only if FV can be determined, and if materials and services would normally be used in the organization’s operations and would have been purchased if they have not been donated

Under the deferral method, donated materials and services should be reported as contribution revenue when the materials and services are expensed

Volunteer hours are tricky

NFPO do not record these hours

If they were to record it, they would have to put it into an asset account to go with the contribution entry and deplete the asset account when they have wage expenses

If no wages are expensed, then don’t record it at all

Analysis and Interpretation of Financial Statements

The cost per unit of output is a key ratio for many NFPOs

Ratios are significantly different between the two reporting methods

Ratios are significantly different between the general fund and the total of all funds under the restricted fund method

The organization looks most efficient using only the general fund under the restricted fund method

The solvency of the entity looks much better using all funds under the restricted fund method

The debt-to-equity ratio is usually higher under the deferral method because some contributions are reported as deferred contributions, which appears in the liability section of the statement of financial position

Disclosure Requirements

The disclosure requirements for NFPOs are extensive

The following summarizes the main disclosures required in Section 4410 related to revenue from contributions:

Contributions by major sources, including the nature and amount of contributed materials and services recognized in the FS

The policies followed in accounting for endowment contributions, restricted contributions, and contributed materials and services

The nature and amount of changes in deferred contribution balances for the period

How and where net investment income earned on resources held for endowment is recognized in the FS