Chapter 11: Stockholders' Equity

Objective 11.1: Explain the role of stock in financing a corporation.

Corporate Ownership

- The major advantage of the corporate form of business is the ease of raising capital as both large and small investors can participate in corporate ownership.

- Advantages include:

- It is simple to become an owner of a corporation:

- You just have to buy a share of the company’s stock.

- You can easily transfer ownership:

- Sell the stock to someone else.

- A corporation provides limited liability.

- A shareholder is not responsible for a company’s debt.

- It the company goes bankrupt, you lose the amount you paid for the initial stock, but you are not liable for company’s liabilities.

- Because a corporation is a separate legal entity, it can:

- Own assets

- Incur liabilities

- Sue and can be sued

- Enter into contracts

- Corporations are .

- You must submit an application to the state government to create a corporation. When a corporation is approved, the state issues the articles of incorporation which holds information about the corporation.

- Stockholder benefits include:

- Voting rights - being able to vote on important issues at annual meetings.

- Dividends - Stockholders have the right to receive dividends when declared by the board of directors.

- Residual claims (liquidation rights) - If the corporation goes bankrupt, stockholders share in any remaining assets after creditors are paid.

- Preemptive rights - Existing stockholders have the first chance to purchase newly issued stock before it is issued to the public.

Equity vs Debt Financing

- Equity financing is issuing new stock to investors.

- Advantages:

- Equity does not have to be repaid, but debt does.

- Dividends are optional, but there is interest on debt.

- Debt financing is borrowing money from lenders.

- Advantages:

- Interest on debt is tax deductible.

- Debt does not change shareholder control.

Objective 11.2: Explain and analyze common stock transaction.

Stockholders’ Equity

- Contributed Capital

- Retained Earnings

- Treasury Stock

- Accumulated Other Comprehensive Income or Loss

- Contributed Capital (Common Stock and APIC)

- The company receives capital from investors when they sell stock to them.

- APIC is Additional Paid in Capital, which is the amount collected over par.

- Retained Earnings

- It is earned capital.

- Cumulative net income means less cumulative dividends.

- Treasury Stock

- Shares that were issued, but the company decided they wanted to buy them back.

- This is a contra accounts that has a normal DEBIT balance and reduces Stockholders’ Equity.

- It is a account.

- A contra account that is “stuck like glue” to Common Stock and APIC.

- Accumulated Other Comprehensive Income or Loss

- Recorded unrealized gains and losses that cause temporary changes in the value of assets and liabilities of the company.

- The may involve pensions, foreign currencies, and financial investments.

- It holds everything else (what we can’t squeeze into Common Stock because it can only hold par value).

Authorization, Issuance, and Repurchase of Stock

- A corporation can only issue a certain number of shares, which are known as authorized shares.

- Issued shares are permanently for the stockholder unless:

- They sell them to another company

- The corporation buys them back (treasury stock)

- Unissued shares are shares that haven’t been traded.

- Outstanding shares are owned by stockholders. They are .

Stock Authorization

- Par value is assigned to each share of stock that is authorized.

- It is not the same at market price, which is the value of what shares can sell for to the public.

- It is always a small number, like $0.01 per share.

- Some states require par value.

- No-Par value stock does not have a determined price.

Stock Issuance

- The first time a corporation’s stock is available to the public is called an initial public offering (IPO).

- When new stock is issued to the public, this is called seasoned new issue.

- Issuing stock at par value,

- Debit cash

- Credit Common Stock (shares x par value amount)

- Credit Additional Paid In Capital (cash - common stock)

- Example: A company issued 100,000 shares of $0.01 par value common stock for $30 per share.

- Step 1: Calculate cash received.

- Shares x Price per share

- 100,000 x $30

- Cash = 3,000,000

- Step 2: Calculate Common Stock.

- Shares x Par value

- 100,000 x $0.01

- Common Stock = $1,000

- Step 3: Calculate Additional Paid-In Capital (APIC).

- Cash - Common stock

- 3,000,000 - $1,000

- APIC = 2,999,000

- Step 4: Make the journal entry.

| Cash | $3,000,000 | ||

|---|---|---|---|

| Common Stock | $1,000 | ||

| APIC | $2,999,000 |

Stock Exchanged Between Investors

- A transaction between two investors does not involve the corporation, so the corporation does not need to record anything.

- The corporation still has the same amount of shares issued to shareholders.

Stock Used to Compensate Employees

- Employees pay packages may include exclusive stock options for a “discount” price compared to what the market price is.

- Employees are later able to buy stock and the value will be higher.

- They can also sell their stock at a higher price.

Repurchase of Stock

- Treasury stock is the repurchase of issued stock.

- :

- Making a company believe the stock is worth getting.

- Buy back the shares just to reissue them at a higher price to other companies.

- Buy back shares to reissue them to employees.

- Reduce the number of outstanding shares to increase per-share measures of earnings.

- When it is bought back, it is .

- It has no voting or dividend rights.

- Cash dividends paid is reduced when Treasury Stock is purchased.

- Stock transactions are only on the balance sheet.

- :

- Debit Treasury Stock

- Credit Cash

- Example for reacquiring stock: A company reacquires 20,000 shares of its common stock at $20 per share.

- Step 1: Calculate cash paid.

- 20,000 x $20

- $400,000 is paid.

- Step 2: Make the journal entry.

| Treasury Stock | $400,000 | ||

|---|---|---|---|

| Cash | $400,000 |

- :

- Debit Cash (shares x new price of share)

- Credit Treasury Stock (shares x initial price of stock)

- Credit Additional Paid-In Capital (shares x (new price - old price))

- Example for reissuing stock: A company reissues 10,000 shares of Treasury Stock at $35 per share.

- Step 1: Calculate cash received.

- Shares x New cost per share

- 10,000 x $25

- Cash = $250,000

- Step 2: Calculate Treasury Stock that will be issued.

- Shares x Initial price of stock (from reacquiring example)

- 10,000 x $20

- Treasury Stock = $200,000

- Step 3: Calculate APIC.

- (Shares x (new price - old price))

- (10,000 x ($25 - $20))

- 10,000 x $5

- APIC = $50,000

- Step 4: Make the journal entry.

| Cash | $250,000 | ||

|---|---|---|---|

| Treasury Stock | $200,000 | ||

| APIC | $50,000 |

- Stock transactions NEVER generates gains or losses.

Objective 11.3: Explain and analyze cash dividends, stock dividends, and stock split transactions.

Cash Dividends on Common Stock

- If investors get common stock then they will get a return on their investment.

- Returns on Common Stock investments can come in two forms:

- Dividends

- Increases in stock price

- Growth investment is buying stock that pay a small amount of dividends or no dividends at all.

- Income investments are from common stock that do pay dividends.

- Before a dividend is declared, a company must have:

- Enough retained earnings

- Enough cash

- Dividends are…..

- Declared by a board of directors.

- Not legally required.

- Liabilities once declared

- .

Dividend Dates

- The declaration date is the day when the Board of Directors decide to issue a cash dividend. This is the day the liability is established. Journal entry:

- Debit Dividends

- Credit Dividends Payable

- The date of record is an administrative responsibility.

- No journal entry

- The date of payment reduces the liability and cash. Journal entry:

- Debit Dividends Payable

- Credit Cash

- The year end is when the temporary accounts are closed to Retained Earnings. Journal entry:

- Debit Retained Earnings

- Credit Dividends

- Example:

- Declaration Date: A company declares a cash dividends of $115,000,000 during its 2021 fiscal year.

| Dividend | $115,000,000 | ||

|---|---|---|---|

| Dividend Payable | $115,000,000 |

- Date of record: NO JOURNAL ENTRY

- Date of payment: The previously declared dividend is paid off by the company.

| Dividend Payable | $115,000,000 | ||

|---|---|---|---|

| Cash | $115,000,000 |

- Year end: The company’s temporary accounts are closed into Retained Earnings at the end of their accounting period.

| Retained Earnings | $115,000,000 | ||

|---|---|---|---|

| Dividends | $115,000,000 |

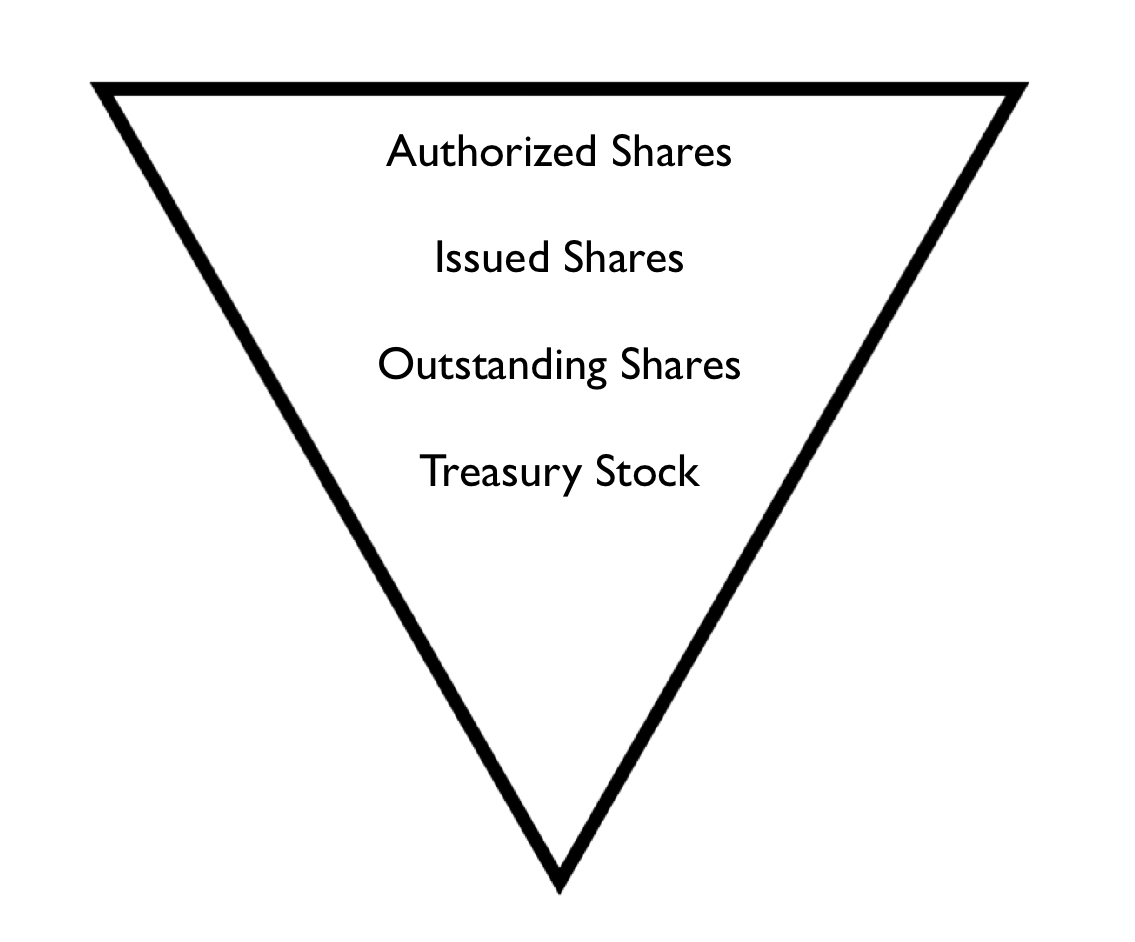

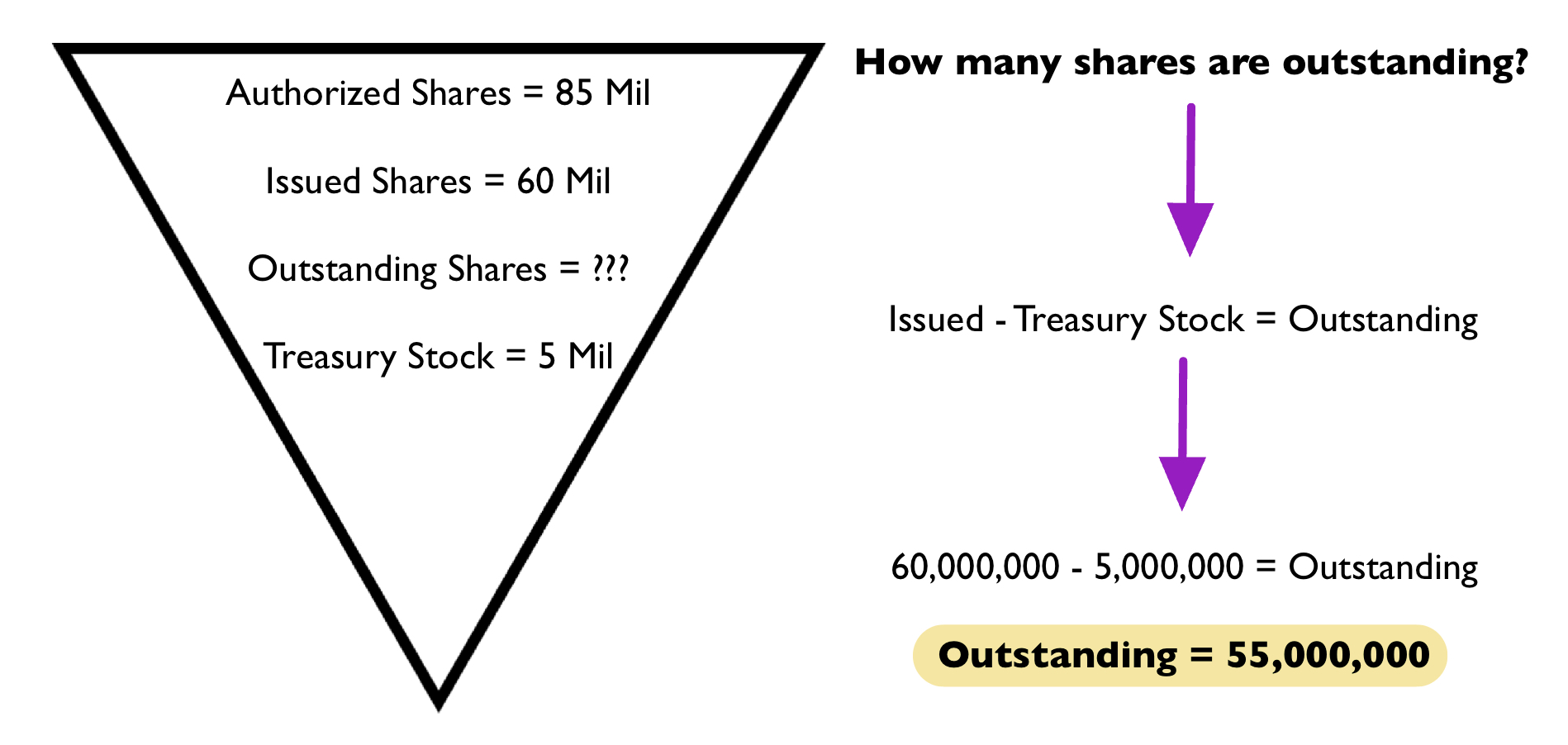

The Common Stock Triangle 🔽

- Authorized shares are the max amount of shares that can be issued.

- Issued shares are given to shareholders.

- Outstanding shares are what has not been issued.

- ==Equation to calculate outstanding shares:==

- Issued - Treasury shares = Outstanding Shares

- Example:

Objective 11.4: Describe the characteristics of preferred stock and analyze transactions affecting preferred stock.

Preferred Stock

- Preferred stock is given to a special group of investors.

- Preferred stock has different features such as:

- It has different voting rights (none or a lot).

- Dividends may be paid at a fixed rate.

- It has priority over normal common stock.

- Preferred Stock Issuance increases cash and stockholders’ equity.

Preferred Stock Redemption

- Preferred stock that was issued can be bought back.

- This redemption means the preferred stock is retired, which results in the issuance being reversed.

Preferred Stock Dividends

- Preferred stock gives two dividends preferences:

- Current dividend preference

- Cumulative dividend preference

- A current dividend preference states that preferred dividends must be paid before paying dividends to stockholders.

- A cumulative dividend preference states if a current dividends is not paid, the unpaid amount has to be paid before other common dividends.

- Dividends in arrears regard cumulative preferred stock that has not been paid yet. They are not on the balance sheet.

Retained Earnings

- Retained Earnings are the collective earnings of a company.

- Net income increases Retained Earnings.

- Net loss decreases Retained Earnings.

- Giving cash or dividends to stockholders also decreases Retained Earnings.

- The negative balance of Retained Earnings is called accumulated deficit.

Statement of Stockholders’ Equity

- The statement of stockholders’ equity shows each stockholders’ equity account so we can track increases and decreases for each account.

- Examples of what may be included:

- Issued shares

- Treasury stock

- Net income

- Cash dividends

- Stock dividends

- Common stock

- APIC

- Retained Earnings

Objective 11.5: Analyze the earnings per share (EPS), return on equity (ROE), and price/earnings (P/E) ratios.

Earnings Per Share (EPS)

- Earnings per share provides information on the profit earned from common stock that is outstanding.

- Recent earning ratios can look into how dividends and stock prices may be in the future.

- Using EPS, you can compare the financial ratio to other years.

- You can not compare companies using this ratio.

- The higher that ratio, the better.

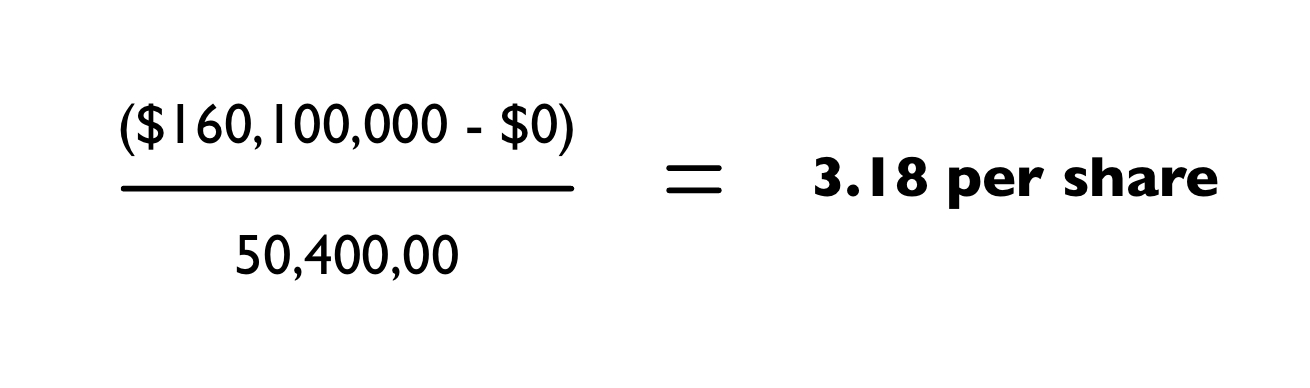

- ==Equation to calculate earnings per share:==

- (Net Income - Preferred Dividends)/ Average number of Common Shares Outstanding

- Example: A company’s income for 2022 was $160,100,000. It has $0 of preferred dividends. The average number of its outstanding shares was 50,400,000.

Return on Equity (ROE)

- Return on Equity reports a company’s return to stockholders.

- The ratio can be compared across companies.

- The higher the ratio, the better.

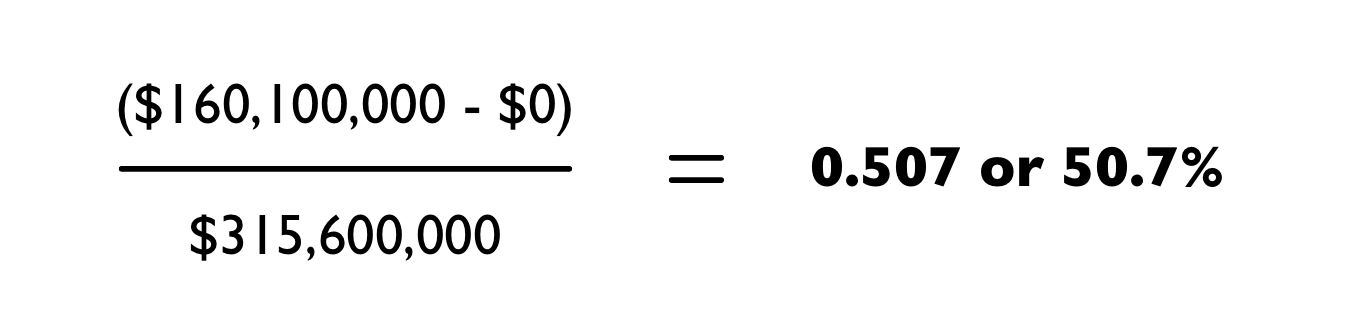

- ==Equation to calculate return on equity:==

- (Net Income - Preferred Dividends)/ Average Common Stockholders’ Equity

- Example: A company’s income for 2022 was $160,100,000. It has $0 of preferred dividends. The average common stockholders equity was $315,600,000.

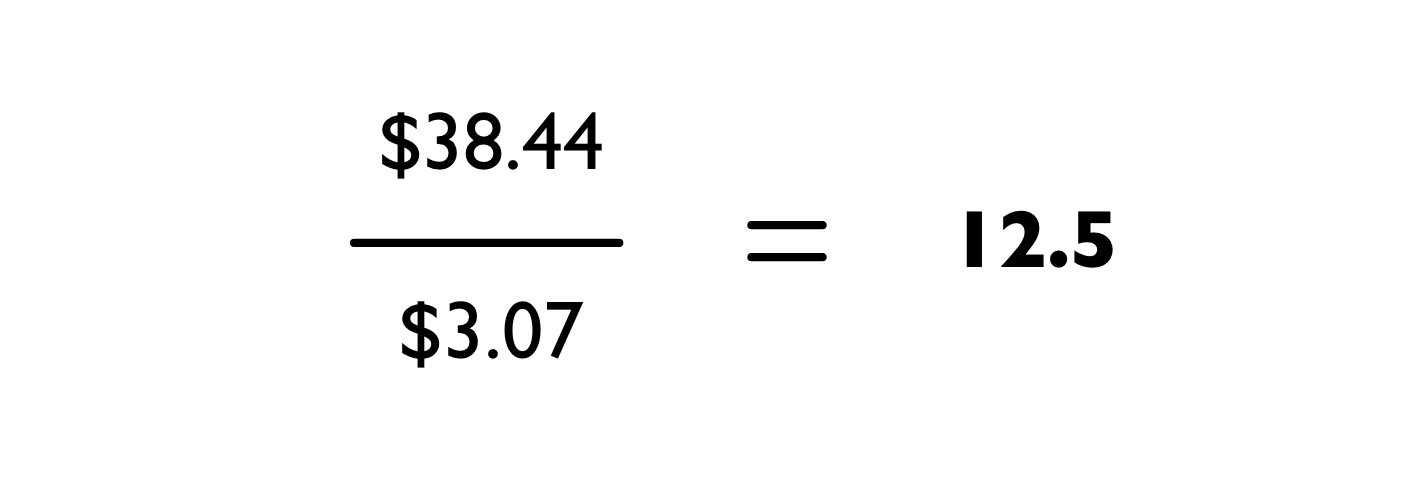

Price/Earnings (P/E) Ratio

- The Price/Earnings ratio is a measure of the value that investors place on a company’s common stock.

- The current stock price comes from the stock exchange.

- With this ratio, you need to calculate EPS before calculating P/E.

- ==Equation to calculate the price/earning ratio:==

- Current Stock Price (per share)/ Earning Per Share (annual)

- Example: A company’s stock price was $38.44 when the company reported its 2022 EPS of $3.07.