Short-Run Production Costs

Fixed, Variable, and Marginal Cost

Fixed Cost: costs that do not change with the level of output produced

Variable Cost: costs that vary with the level of output produced

Marginal Cost: the cost of producing one additional unit of output

MC, AVC, ATC

Marginal cost : cost difference of one additional unit of output (∆TC/∆Q)

Average fixed cost (AFC) : FC/Q

Average variable cost (AVC) : VC/Q

Average total cost (ATC) : TC/Q or AFC + AVC

Total Cost = TFC + ATC

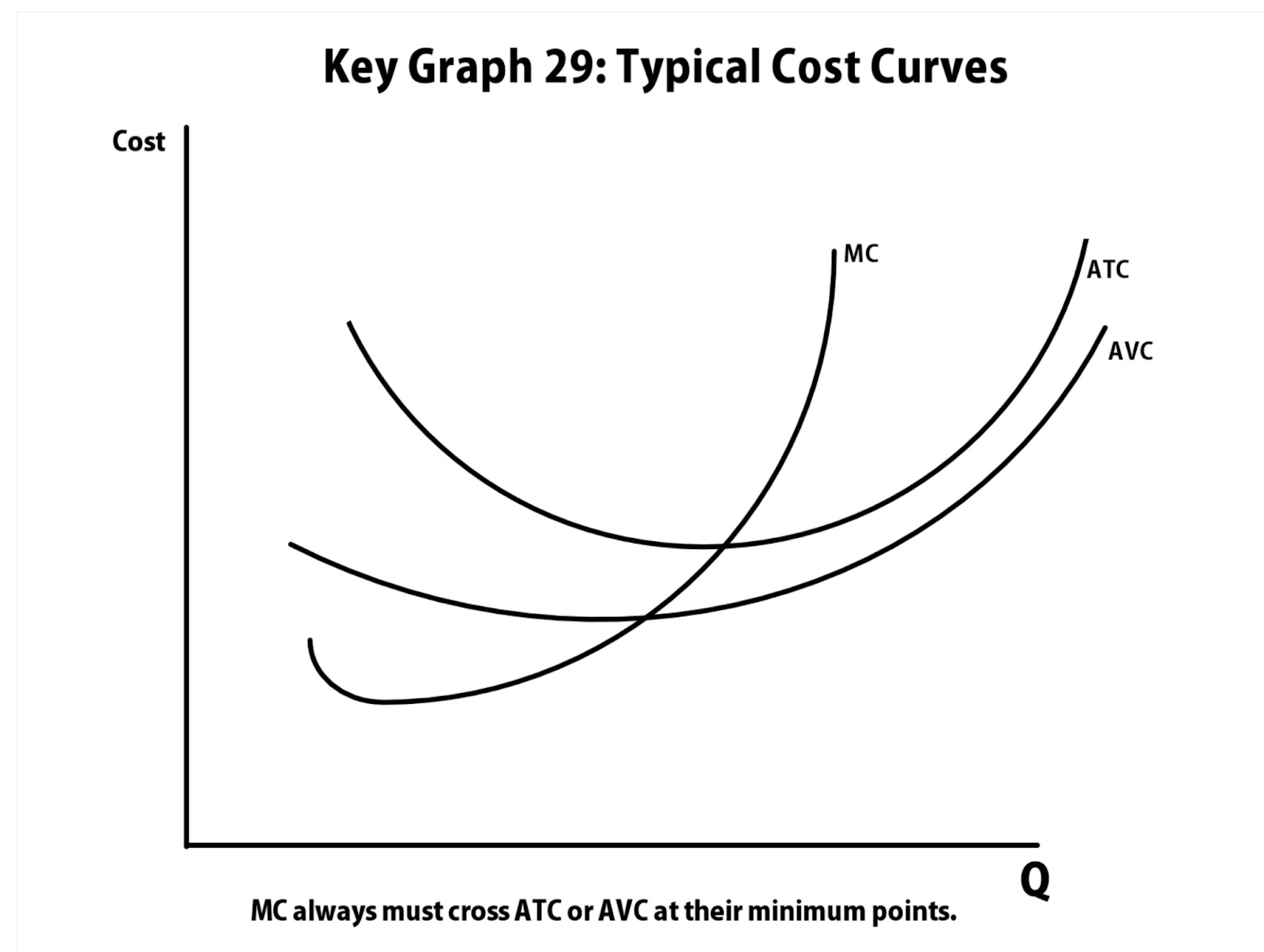

Graph

The MC curve intersects both the AVC and ATC curves at their respective lowest points

This intersection signifies the output level where average costs are minimized

Marginal Revenue and Marginal Cost

Marginal Revenue: the additional revenue a firm earns by selling one more unit of a good or service; (change in TR/change in Q)

Marginal Cost: the additional cost incurred by producing one more unit of a good or service (change in TC/change in Q)

MC typically decreases initially due to increasing returns, then increases due to diminishing returns.

Profit Maximization Rule is when MR = MC

TR is at maximum when MR goes negative

MR Below ATC

When MR < ATC, the firm is not covering its total costs and is operating at a loss

Even if a firm is incurring losses (MR < ATC), it may continue operating in the short run if it can cover its average variable costs (AVC).

continuing operations allows the firm to contribute to fixed costs, potentially reducing overall losses compared to shutting down immediately

if losses persist in the long run, the firm may exit the market, as it's unsustainable to operate without covering total costs over time

How Costs Change when Fixed and Variable Costs Change

1. Changes in Fixed Costs:

Fixed costs (e.g., rent, salaries) remain constant regardless of output

Increasing fixed costs raises the AFC and ATC

However, MC and AVC remain unaffected because fixed costs don't change with production levels

2. Changes in Variable Costs:

Variable costs (e.g., raw materials, hourly wages) fluctuate with output

An increase in variable costs raises AVC, MC, and ATC

These changes directly impact the cost of producing each additional unit

3. Graphical Representation:

An increase in fixed costs shifts the ATC curve upward, while MC and AVC curves remain unchanged

An increase in variable costs shifts the AVC, MC, and ATC curves upward

4. Changes in Productivity:

Improved productivity (e.g., better technology) allows more output with the same input

This causes the AVC, MC, and ATC curves to shift downward, indicating lower costs per unit

Conversely, reduced productivity shifts these curves upward