ap macro chapter 1

1.1 Scarcity

scarcity - having unlimited wants but limited resources

textbook definition of economics - social science concerned with the efficient use of scarce resources to achieve maximum satisfaction of economic wants

the science of scarcity, the study of choices (individuals, firms, governments)

study of how individuals and societies deal with scarcity

microeconomics - study of small economic units such as individuals, firms, and markets

examples - supply and demand in specific industries, production costs, labor markets

macroeconomics - study of the large economy as a whole or economic aggregates

examples - economic growth, government spending, inflation, unemployment, international trade

positive statements - based on facts; avoids value judgments (what is)

normative statements - includes value judgments (what ought to be)

theoretical economics - when economists use the scientific method to make generalizations and abstractions to develop theories

policy economics - applying economic theories to fix problems or meet economic goals

5 key economic assumptions

society’s wants are unlimited, but ALL resources are limited

scarcity

due to scarcity, choices must be made. every choice has a cost

every choice has a trade-off

everyone’s goal is to make choices that maximize their satisfaction. everyone acts in their own “self-interest”

everyone’s goal is to maximize satisfaction. we act in our own self-interest

everyone acts rationally by comparing the marginal costs and marginal benefits of every choice

everyone makes decisions by comparing marginal costs and marginal benefits

real-life situations can be explained and analyzed through simplified models and graphs

marginal analysis - making decisions based on increments

you will continue to do something as long as the marginal benefit is greater than the marginal cost

marginal benefit - the maximum amount of money a consumer is willing to pay for an additional good or service

marginal cost - the change in cost when an additional unit of a good or service is produced

trade-offs - all the alternatives that we give up when we make a choice

opportunity costs - the most desirable alternative given up when you make a choice

utility - satisfaction

marginal - additional

allocate - distribute

price - the amount the buyer (or consumer) pays

cost - the amount the seller pays to produce a good

consumer goods - created for direct consumption

capital goods - created for indirect consumption

allows the potential for more resources to be made

four factors of production

land - all natural resources that are used to produce goods and services

labor - any effort a person devotes to a task for which that person is paid

capital

entrepreneurship - ambitious leaders that combine other factors of production to create goods and services

physical capital - any human-made resource that is used to create other goods and services

examples - tools, tractors, machinery, factories, etc.

human capital - any skills or knowledge gained by a worker through education and experience

productivity - a measure of efficiency that shows the number of outputs per unit of input

increasing productivity allows the production of more items with fewer resources

1.2 OC and PPC

production possibilities curve (PPC, frontier) - a model that shows alternative ways that an economy can use its scarce resources

demonstrates scarcity, trade-offs, opportunity costs, and efficiency

4 key assumptions of the PPC

only two goods can be produced

full employment of resources

land

labor

capital

fixed resources (ceteris paribus)

fixed technology

point on the PPC curve - represents a specific combination that can be produced given full employment of resources

point inside of the PPC curve - inefficient because not all labor resources are being used (unemployment)

point outside of the PPC curve - not attainable because of scarcity, not enough materials at the moment

opportunity cost - the benefit missed out when choosing an alternative; the next best thing

constant opportunity cost - when resources are easily adaptable for producing either good

results in a straight-line PPC, not common

law of increasing opportunity costs - as you produce more of any good, the opportunity cost (forgone production of another good) will increase

happens because resources are NOT easily adaptable to producing both goods

results in a bowed-out PPC

3 shifters of the PPC

change in resource quantity or quality

change in technology

change in trade (allows more consumption)

change in demand does NOT shift the PPC

decrease in resources - decrease production possibilities for both

quality of resources improves - shifting the curve outward (change in technology)

unemployment is just a point inside the curve - no shift

quality of labor is improved - curve shifts outward

human capital is impacted significantly, making capital more productive

1.3 Comparative Advantage

trading - everyone specializes in the production of goods and services and trades with others (we don’t produce anything ourselves); more access to trade means more choices and a higher standard of living (no trade = limited materials)

per unit opportunity cost = opportunity cost/units gained

when calculating opportunity cost we give up what we get (down)

absolute advantage - the producer that can produce the most output or requires the least amount of inputs (resources)

comparative advantage - the producer with the lowest opportunity cost

goods that a country should specialize in - the good that is “cheaper” for them to produce (the one with comparative advantage)

trade can occur if they have a relatively lower opportunity cost

output questions - the amount of inputs, like time, workers, or other resources, are the same for both countries. only the output of each country is different

the same amount of workers - the US produces 10 planes, China produces 3 planes

output questions hack

output

other goes

over

input questions - the amount of output, like cars, planes, or corn, are the same for both countries. only the inputs for each country are different

the US takes 20 workers for 1 plane, China takes 40 workers for 1 plane

input questions hack (variable is resources, like time)

input

other goes

under

terms of trade - agreed upon conditions that benefit both countries

both benefit from trade if they each have relatively lower opportunity costs

5 comparative advantage hacks

Cars | Planes | |

|---|---|---|

US | 5 | 1 |

China | 3 | 2 |

spotting output vs input questions

output - want higher numbers

input - want lower numbers

o.o.o and i.o.u

output other goes over - 1/5

input other goes under - 5/1

it’s 50/50

one country can only have one comparative advantage

finding the terms of trade

one country wants another country’s item. if produced in the country, it’s expensive so trading benefits both

1 plane for 4 cars 1 car for ¼ plane basically 1p for any number between 5 and 3/2 c

quick and dirty

multiply across to see which two have the comparative advantage

3 × 1 = 3 comparative advantage for input

5 × 2 = 10 comparative advantage for output

input would be smaller number, output higher

1.4 Demand

demand - different quantities of goods that consumers are willing and able to buy

law of demand - there is an inverse relationship between price and quantity demanded

price goes up, quantity goes down, etc.

why does the law of demand occur?

substitution effect - if the price goes up for a product, consumers buy less of that product and more of another substitute product (and vice versa)

pepsi vs coke - if pepsi goes up, people buy more coke

income effect - if the price goes down for a product, the purchasing power increases for consumers — allowing them to purchase more

law of diminishing marginal utility - states that as you consume anything, the additional satisfaction that you receive will eventually start to decrease

the more you buy of any good, the less satisfaction you get from each new unit consumed

we buy goods because we get utility from them

demand curves

graphical representation of a demand schedule

downward sloping, showing the inverse relationship between price (y-axis) and quantity demanded (x-axis)

the x-axis is always quantity and the y-axis is always price; if switched then the graph is wrong

when reading a demand curve, assume all outside factors, such as income, are held constant (ceteris paribus)

shifts in demand

when the ceteris paribus assumption is dropped

movement no longer occurs along the demand curve. the entire demand curve shifts

shift means that at the same prices, more people are willing and able to purchase that good

change in demand, not quantity demanded - PRICE DOESN’T SHIFT THE CURVE

difference between a change in demand and a change in quantity demanded

change in demand - the whole curve shifts (inward/outward, all points shift)

change in quantity - only one point shifts, moving along the existing curve

change in price - moves along the curve

causes of shift in demand

market size (number of consumers)

expectations

related prices

substitutes

complements

income

normal goods

inferior goods

tastes and preferences

prices of related goods - the demand curve for one good can be affected by a change in the price of ANOTHER related good

substitutes - goods used in place of one another

if the price of one good increases, the demand for the other will increase (or vice versa)

complements - two goods that are bought and used together

if the price of one increases, the demand for the other will fall (or vice versa)

falls are different

income - the incomes of consumers change the demand, but how depends on the type of good

normal goods (proportional)

as income increases, demand increases

as income falls, demand falls

ex. luxury cars, seafood, jewelry, homes

inferior goods (inverse)

demand is higher when income is low

as income increases, demand falls

as income falls, demand increases

ex. Top Ramen, used cars, used clothes

different behavior than normal goods

impacts on the demand curve

changes in market size (number of consumers)

if… | demand of A… | |

|---|---|---|

the number of consumers rises | ↑ | |

the number of consumers falls | ↓ |

changes in expectations

if… | demand of A… | |

|---|---|---|

the price of A is expected to rise in the future | ↑ | |

the price of A is expected to fall in the future | ↓ | |

if A is a normal good | and income is expected to rise in the future and income is expected to fall in the future | ↑ ↓ |

if A is an inferior good | and income is expected to rise in the future and income is expected to fall in the future | ↓ ↑ |

changes in the prices of related goods or services

if… | demand of A… | |

|---|---|---|

if A and B are substitutes | and the price of B rises and the price of B falls | ↑ ↓ |

if A and B are complements | and the price of B rises and the price of B falls | ↑ ↓ |

changes in income

if… | demand of A… | |

|---|---|---|

if A is a normal good | and income rises and income falls | ↑ ↓ |

if A is an inferior good | and income rises and income falls | ↓ ↑ |

changes in tastes

if… | demand of A… | |

|---|---|---|

tastes change in favor of A | ↑ | |

tastes change against A | ↓ |

1.5 Supply

supply - the different quantities of a good or service that sellers are willing and able to sell (produce) at different prices

law of supply - there is a DIRECT (or positive) relationship between price and quantity supplied

price increases, quantity (made by producers) increases

price falls, quantity (made by producers) falls

at higher prices, profit-seeking firms have an incentive to produce more

difference between change in supply and change in the quantity supplied

change in supply - shift the whole curve (inward/outward, all points shift)

change in quantity - movement along the curve (one point shifts)

causes of shift in supply

technology

inputs - prices/availability of resources

land

labor

capital

number of sellers

government action: taxes and subsidies

subsidy - government payment to a business or market. subsidies cause the supply of a good to increase

expectations of future profit

impacts on the supply curve

changes in technology

if… | supply of A… | |

|---|---|---|

the technology used to produce A improves | ↑ | |

changes in input prices

if… | supply of A… | |

|---|---|---|

the price of an input used to produce A rises | ↓ | |

the price of an input used to produce A falls | ↑ |

number of sellers

if… | supply of A… | |

|---|---|---|

the number of producers of A rises | ↑ | |

the number of producers of A falls | ↓ |

government action - taxes and subsidies

if… | supply of A… | |

|---|---|---|

if A and B are substitutes in production | the price of a good rises due to taxes the price of a good falls due to subsidies | ↓ ↑ |

changes in expectations

if… | supply of A… | |

|---|---|---|

the price of A is expected to rise in the future | ↑ | |

the price of A is expected to fall in the future | ↓ |

1.6 Equilibrium

surplus - quantity demanded is less than quantity supplied

shortage - quantity demanded is greater than quantity supplied

supply and demand analysis

before the change

draw supply and demand

label original equilibrium price and quantity

the change

did it affect supply or demand first?

which determinant caused the shift?

draw increase or decreases

after the change

label new equilibrium?

what happens to price? (increase or decrease)

what happens to quantity? (increase or decrease)

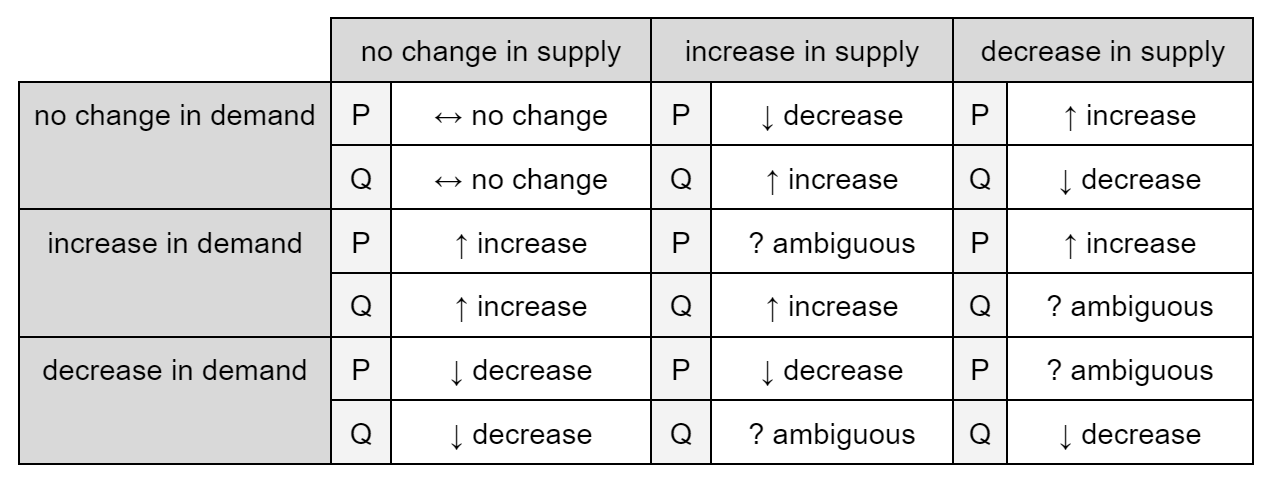

impact of simultaneous shifts of supply and demand on equilibrium price and quantity