Demand and Supply

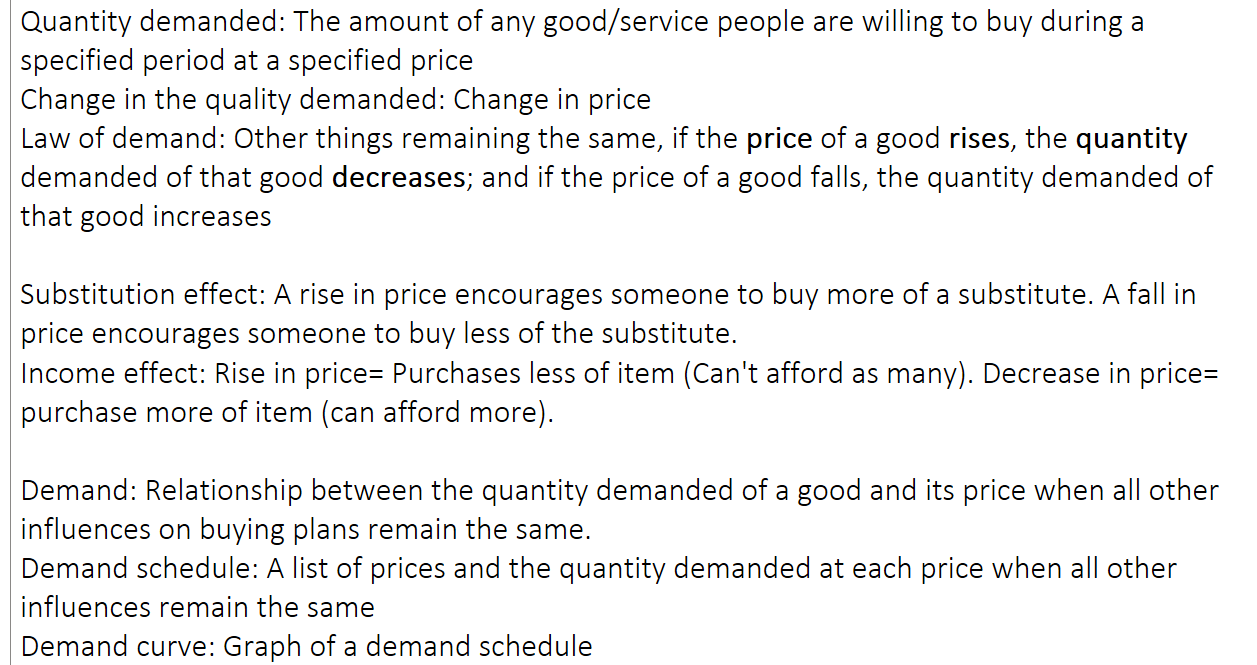

Quantity demanded: The amount of any good/service people are willing to buy during a specified period at a specified price

Change in the quality demanded: Change in price

Law of demand: Other things remaining the same, if the price of a good rises, the quantity demanded of that good decreases; and if the price of a good falls, the quantity demanded of that good increases

Substitution effect: A rise in price encourages someone to buy more of a substitute. A fall in price encourages someone to buy less of the substitute.

Income effect: Rise in price= Purchases less of item (Can't afford as many). Decrease in price= purchase more of item (can afford more).

Demand: Relationship between the quantity demanded of a good and its price when all other influences on buying plans remain the same.

Demand schedule: A list of prices and the quantity demanded at each price when all other influences remain the same

Demand curve: Graph of a demand schedule

Market demand: Sum of the demands of all buyers in a market

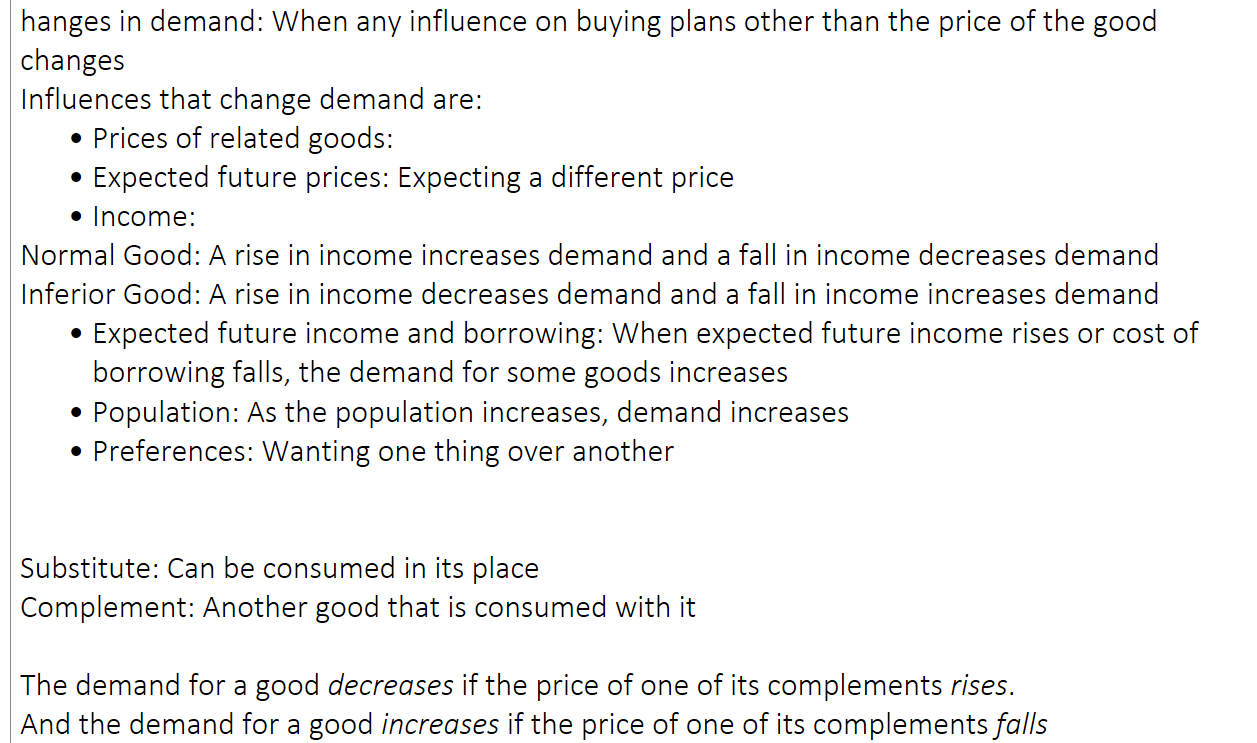

Changes in demand: When any influence on buying plans other than the price of the good changes

Influences that change demand are:

Prices of related goods:

Expected future prices: Expecting a different price

Income:

Normal Good: A rise in income increases demand and a fall in income decreases demand

Inferior Good: A rise in income decreases demand and a fall in income increases demand

Expected future income and borrowing: When expected future income rises or cost of borrowing falls, the demand for some goods increases

Population: As the population increases, demand increases

Preferences: Wanting one thing over another

Substitute: Can be consumed in its place

Complement: Another good that is consumed with it

The demand for a good decreases if the price of one of its complements rises.

And the demand for a good increases if the price of one of its complements falls

Change in quantity demanded: Change in prices when all other influences remain the same

Change in demand: Effect of a change in any of the other influences

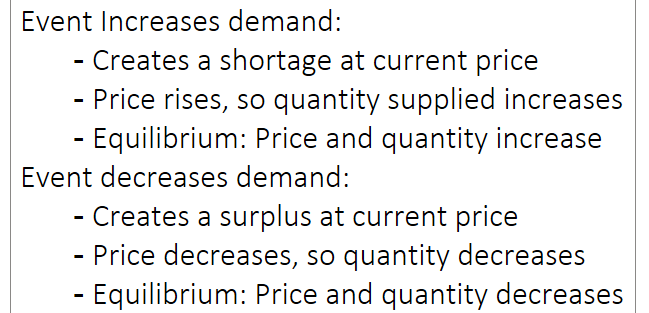

Event Increases demand:

Creates a shortage at current price

Price rises, so quantity supplied increases

Equilibrium: Price and quantity increase

Event decreases demand:

Creates a surplus at current price

Price decreases, so quantity decreases

Equilibrium: Price and quantity decreases

Quantity supplied: The amount that it is willing and able to sell during a specified period at a specified price.

Change in the quality supplied: Change in price

Law of supply: Other things remaining the same, if the price of a good rises, the quantity supplied of that good increases; and if the price of a good falls, the quantity supplied of that good decreases.

Supply: Relationship between the quantity supplied and the price of a good when all other influences on buying plans remain the same.

Supply schedule: A list of the quantities supplied at each different price when all other influences remain the same

Supply curve: A graph of a supply schedule

Why? Because of Profit Effect.

Pricier items= stronger incentive to produce more

Market Supply: The sum of the supplies of all the sellers in a market

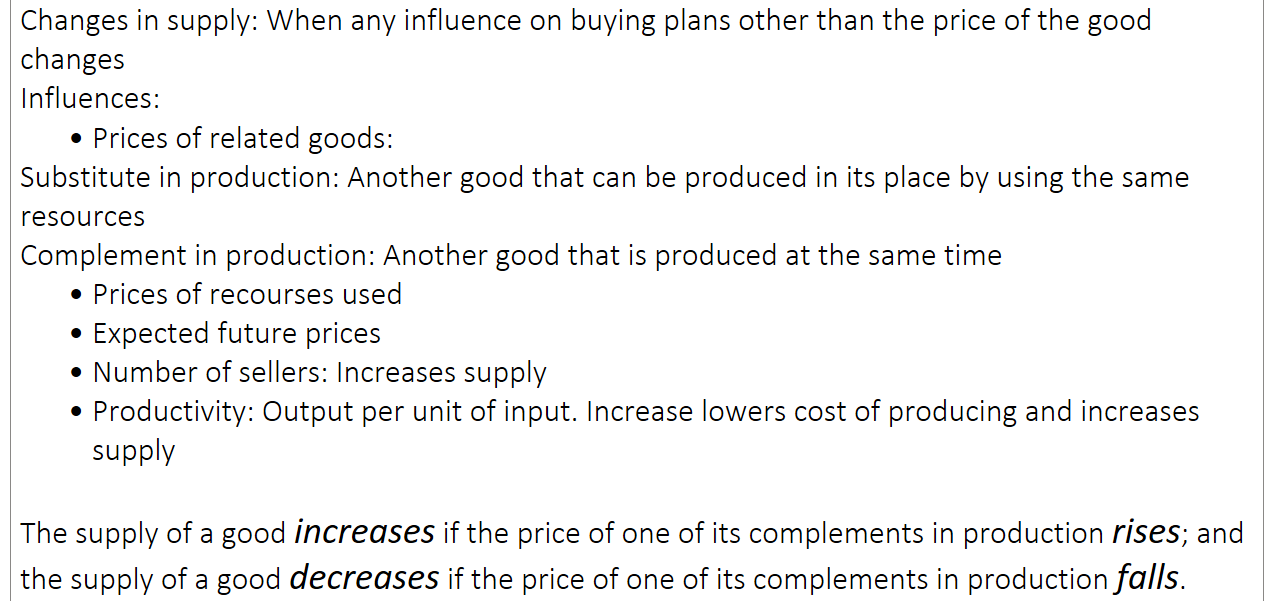

(the sum of the quantities supplied at each price by all produces of the good)Changes in supply: When any influence on buying plans other than the price of the good changes

Influences:

Prices of related goods:

Substitute in production: Another good that can be produced in its place by using the same resources

Complement in production: Another good that is produced at the same time

Prices of recourses used

Expected future prices

Number of sellers: Increases supply

Productivity: Output per unit of input. Increase lowers cost of producing and increases supply

The supply of a good increases if the price of one of its complements in production rises; and the supply of a good decreases if the price of one of its complements in production falls.

Market equilibrium: When quantity demanded equals the quantity supplied

Equilibrium quantity: The quantity bought and sold at the equilibrium price

Law of market forces: When there is a surplus of a good, its price falls; and when there is a shortage of a good, its price rises.