Chapter 13: Measuring and Evaluating Financial Performance

Objective 13.1: Describe the purpose and uses of horizontal, vertical, and ratio analyses.

Horizontal, Vertical, and Ratio Analyses

- Horizontal analyses help financial statement users recognize important financial changes that unfold over time.

- They %%compare individual financial statement%% line items (from one period to the next, aka horizontally) to trends.

- These changes can be translated in dollar amounts or percentages.

- Vertical analyses show relationships between items on a financial statement.

- They are compared “vertically” by comparing the balance of one account to another.

- Theses changes are translated as percentages.

- Ratio analyses are used to understand relationships between items on one or more financial statements.

- This analyses shows a company’s performance from using their resources.

- An analysis is considered “complete” once it is successfully able to create a better understanding for those who review financial statement and its results.

Objective 13.2: Use horizontal (trend) analyses to recognize financial changes that unfold over time.

Horizontal (Trend) Computations

- Horizontal (trend) analyses show how changes unfold over a period of time.

- Significant changes are the focus.

- It is also called the time-series analysis because of the comparison of results over a period of time.

- %%Presented as year to year dollars or percentages%%.

- ==Equation to calculate change (%):==

- (Current year’s total - Prior year’s total)/ Prior year’s total

- Make sure to examine both the dollar amount and percentage to get your final results/conclusion.

- Example: A company’s cash total in 2022 was $819 and in the previous year was $614.

- (Current year’s total - Prior year’s total)/ Prior year’s total

- ($819 - $614)/$614

- $205/$614

- Cash had an increase of 0.334 or 33.4%

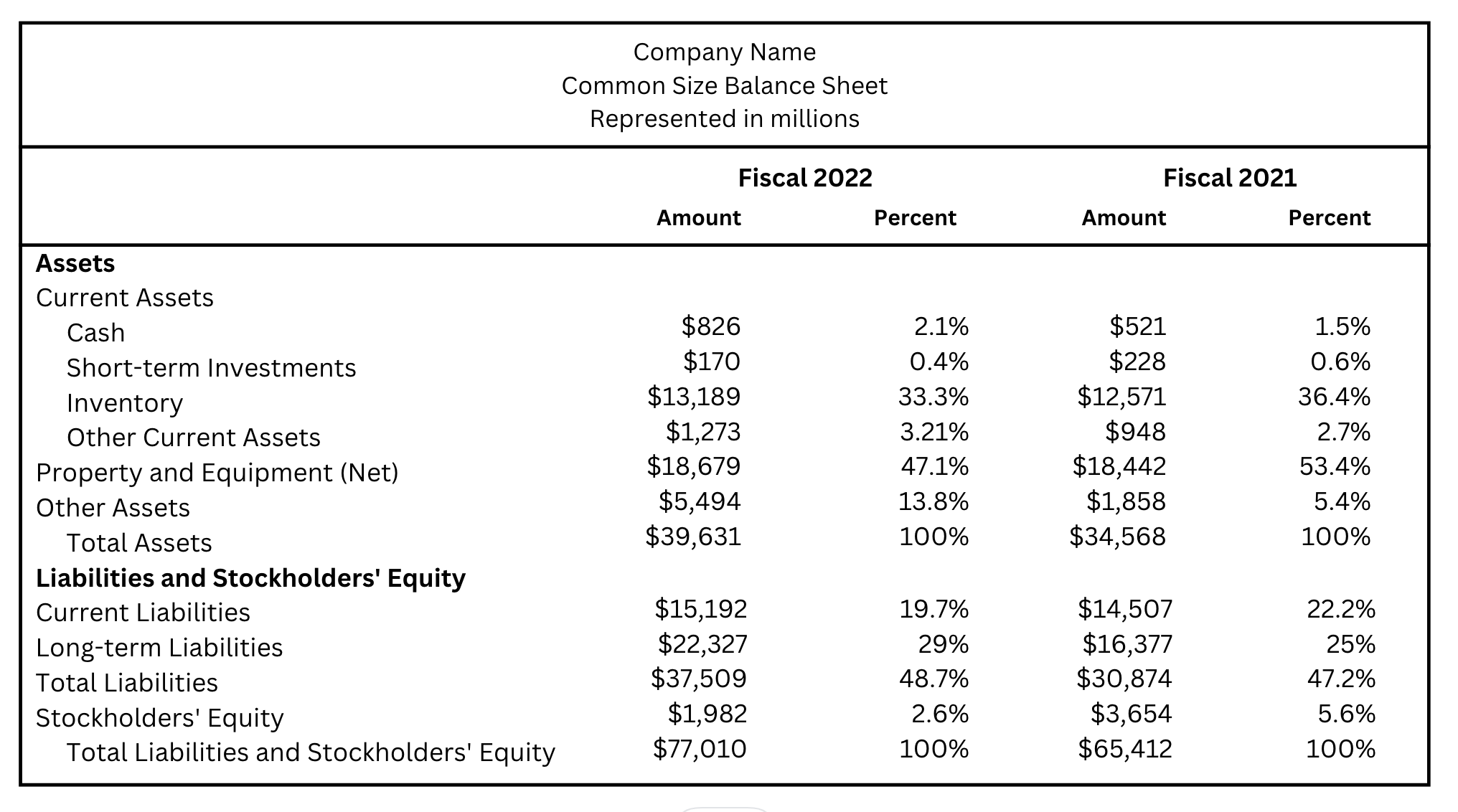

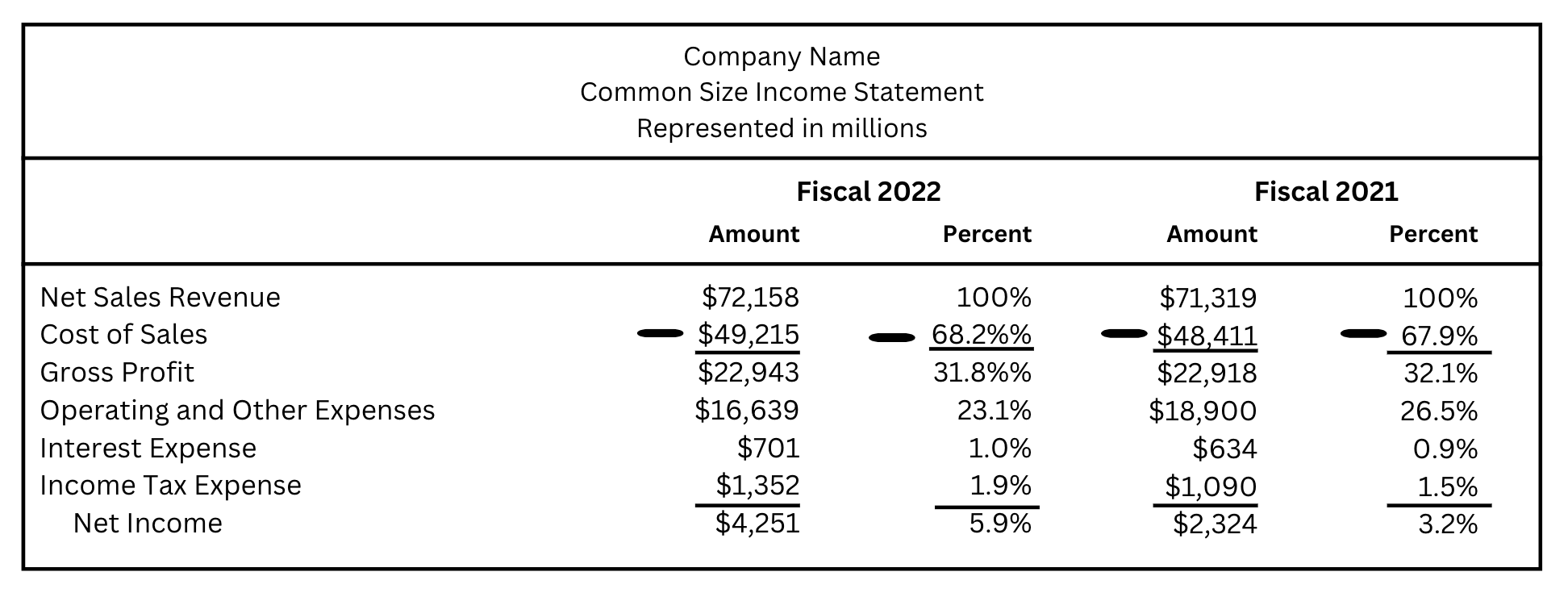

Objective 13.3: Use vertical (common size) analyses to understand important relationships within financial statements.

Vertical (Common Size) Computations

- Vertical (Common Size) analysis focuses on relationships regarding financial statements.

- It relies on percentages to translate results and relationships.

- A common size balance sheet shows the percent of total assets and each liability or stockholders’ equity as a percent of their total.

- A common size income statement gives the percentage of sales for items on the income statement.

Objective 13.4: Calculate financial ratios to assess profitability, liquidity, and solvency.

Ratio Computations

- Ratio analyses helps create a better understanding of relationships between line items on financial statements to other items within the same year.

- Ratio analyses is similar to common size in the manner of how they both consider size in comparisons.

- %%There are three categories of ratios%%:

- Profitability ratios focus on a company’s net income within a current period.

- Liquidity ratios indicate how well a company can use or sell current assets to pay the liabilities they have.

- Solvency ratios assure that a company can repay lenders and interest payments.

Objective 13.5: Interpret the results of financial analyses.

Interpreting Horizontal and Vertical Analyses

- A financial statement user should be able to view the statement, understand the relationships, activities, and overall results presented.

- Financing for assets come from debt and stockholders’ equity.

Interpreting Ratio Analyses

- It is important to compare your company’s performance to other years or companies.

- By comparing, it helps see what companies will have a long life due to good performance or which ones will have a downfall.

- All of the following equations are from past chapters, just categorized.

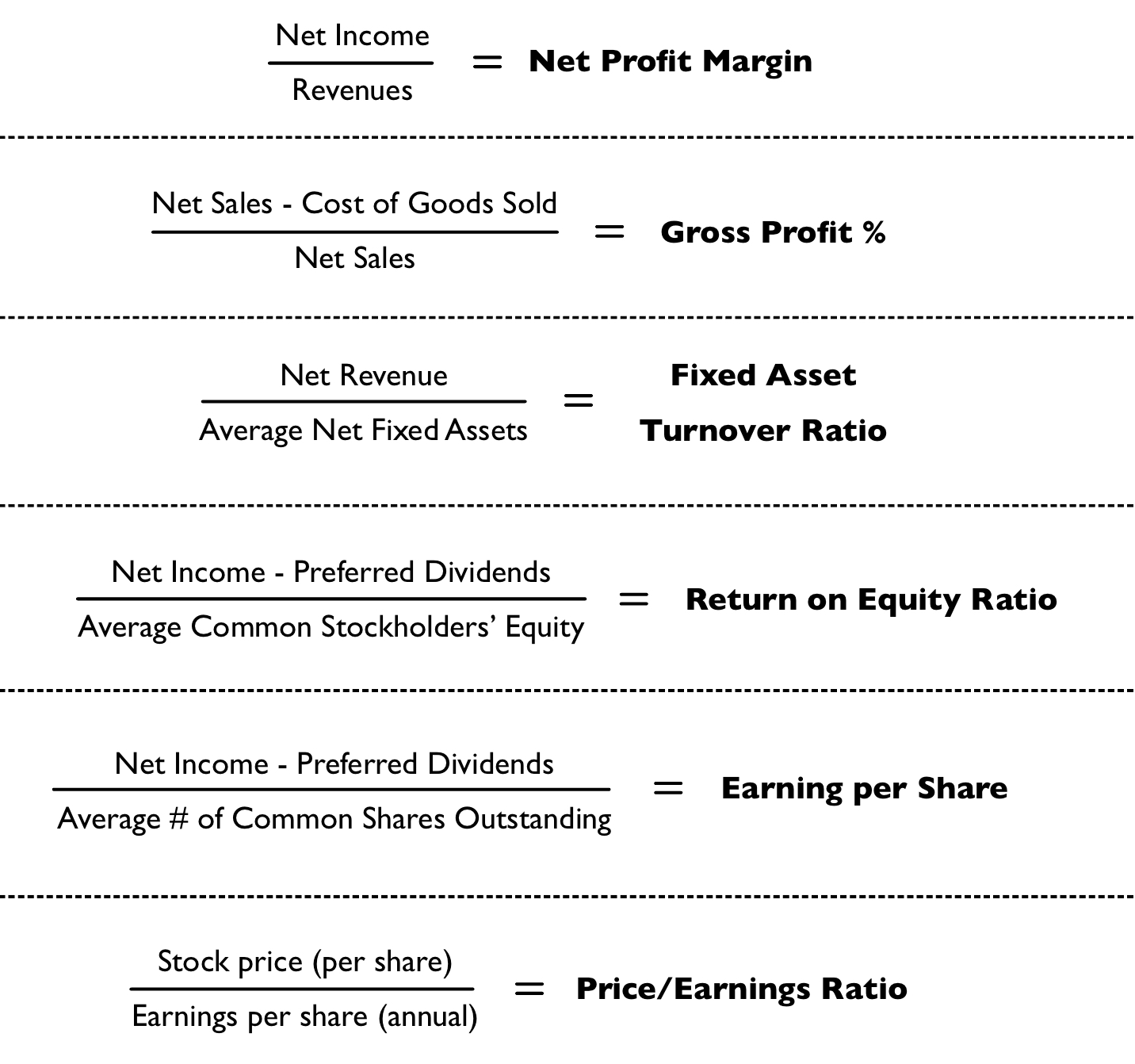

Profitability Ratios

- Net Profit Margins help when evaluating a company and shows the percentage of revenue a company generates.

- A gross profit percentage shows the overall profit made on sales.

- The fixed asset turnover ratio tells us the revenue earned for the amount of money a company puts into fixed assets.

- The return on equity ratio compares earned income for stockholders to the average amount of equity. It is reported as a percentage.

- Earnings per share gives the amount of earnings from outstanding shares.

- The price/earnings ratio correlates the stock price to the stock’s earnings per share.

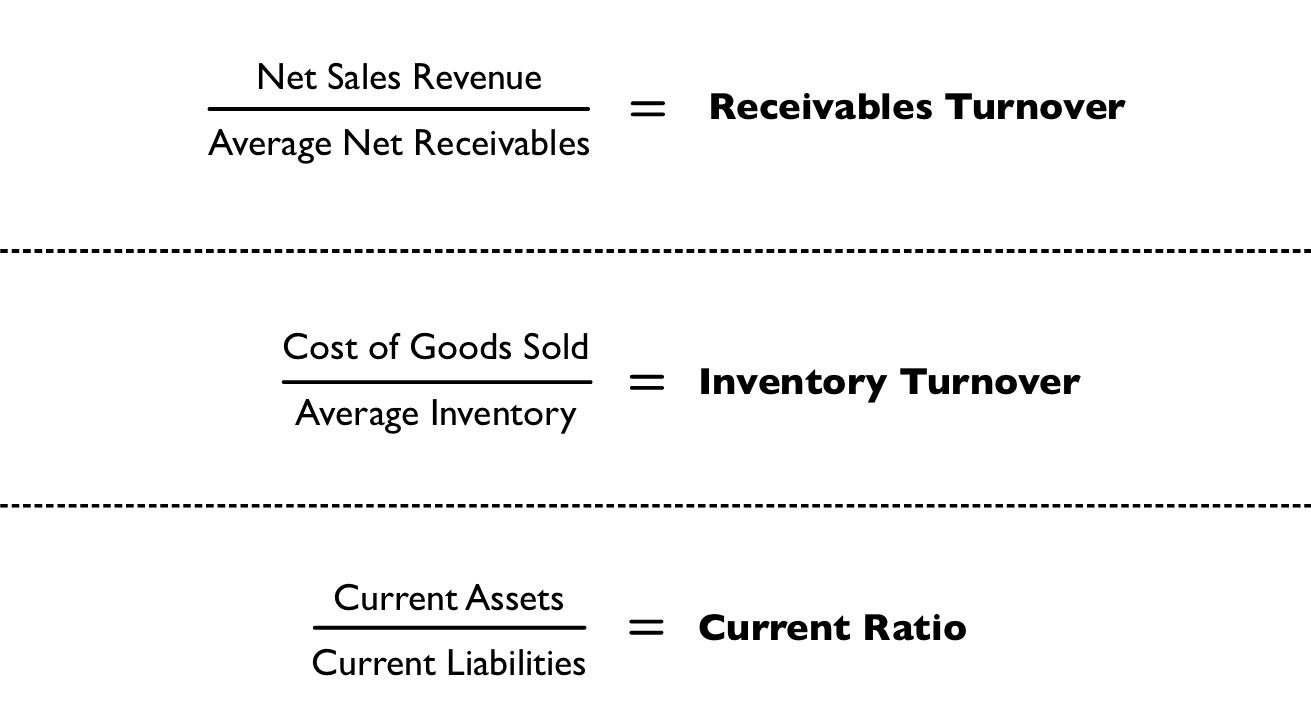

Liquidity Ratios

- Each ratio correlates to seeing if a company can use assets to cover it liabilities.

- The receivables turnover ratio indicates how well a company can collect on its receivables.

- The inventory turnover ratio is the frequency of inventory being bought during the process of buying and selling items.

- The current ratio compares current assets to current liabilities to see if those assets can pay the liabilities.

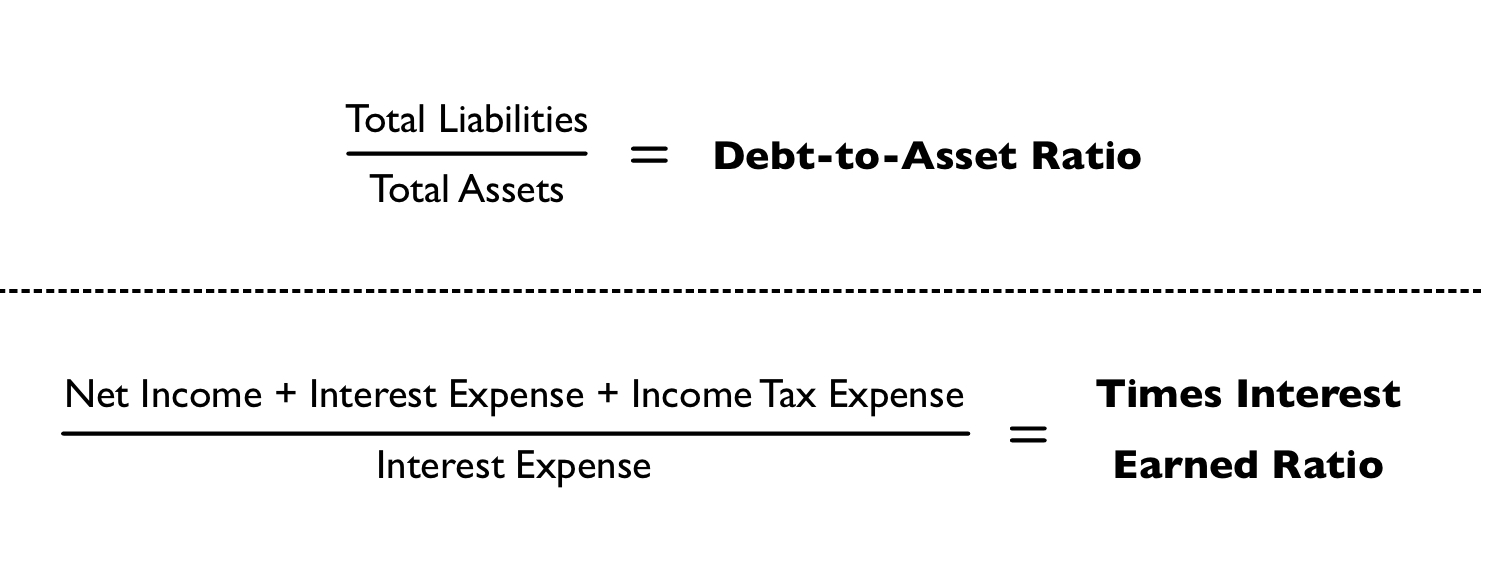

Solvency Ratios

- The debt-to-assets ratio is able to show how much of a company is funded by debt and financed by creditors.

- The times interest earned ratio indicates if a company’s current income can cover its debts.

Objective 13.6: Describe how analyses depend on key accounting decisions and concepts.

Accounting Decisions

- Each type of ratio can give insight in how and why companies may make the decisions they do.

- Different companies have different sales or services, customer demand, and policies.

- Choice of method for certain aspects of business are different from business to business.

Accounting Concepts

- Financial information communicates a lot about a company, so they must be reliable.

- The full disclosure principle demands that all appropriate information regarding a business’s operations must be included on their financial statements.

- The going-concern assumption lays out accounting rules. This is also known as continuity.